HRUFF - Artis: 6.4% Yield With A 50% Discount To NAV

Summary

- It has been a long time since we wrote about this intrepid REIT.

- Management has made some good moves but major challenges lie ahead.

- We look at the recent results and tell you why we are not fans of some portions of the current strategy.

All values are in CAD unless noted otherwise.

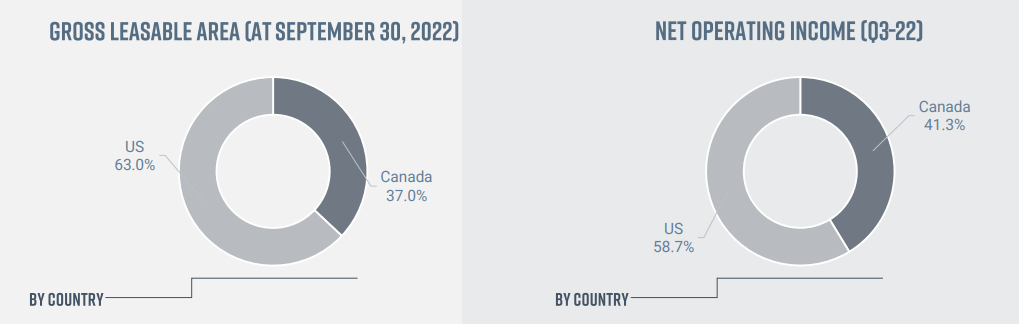

Artis Real Estate Investment Trust (OTCMKTS: ARESF ) ( AX.UN:CA ) owns and operates a 18 million square feet portfolio comprised of industrial, office and retail properties in North America.

{kind=link}

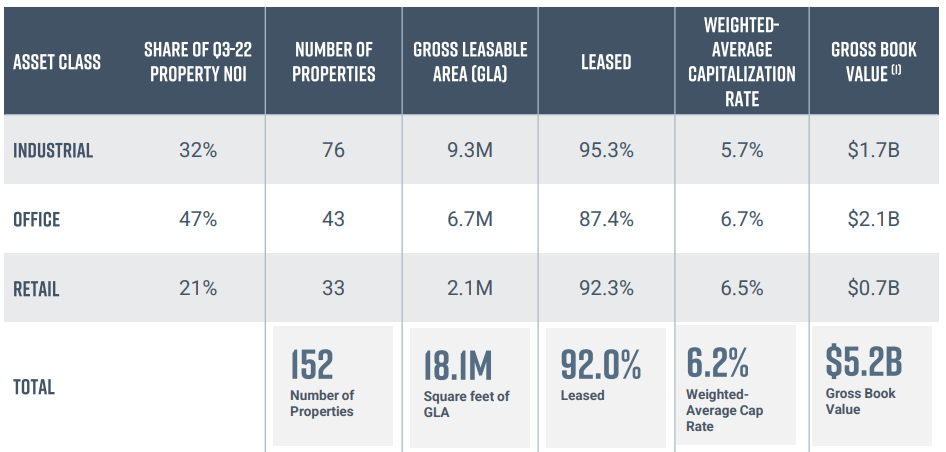

While 50% of its properties are of the industrial type, the office portfolio is the primary contributor to the net operating income or NOI.

{kind=link}

The gross book value total above also other corporate assets which are not part of the property type allocations.

{kind=link}

On the heels of a terminated plan to spin-off of its retail assets, Artis set in motion a " Business Transformation Plan " in early 2021. This initiative comprised a three pronged approach of strengthening the balance sheet, growing organically and focusing on value investing. That the REIT has been committed to their task is apparent when we compare the above graphic with what the portfolio looked like at the end of 2020.

{kind=link}

Exiting the Calgary office properties, taking a stake in Cominar Real Estate Investment Trust in March 2022 and Dream Office Real Estate Investment Trust ( DRETF ) (TSX: D.UN:CA ) in February 2022 have been part of this achieving this long term vision.

We have covered Artis several times on this platform, but not in the last couple of years. We were bullish in August 2020 as the stock price was discounting for an apocalypse. Artis has done adequately well since then in total returns and matched the diversified REITs like H&R ( HRUFF ) (TSX: HR.UN:CA ) and Morguard REIT (OTCMKTS: MGRUF ) (TSX: MRT.UN:CA ). It has also kept pace with the iShares S&P/TSX Capped REIT ETF ( XRE:CA ).

A fresh look at this REIT is long overdue and that is what we will do next.

Q3-2022

Artis' third quarter was a mixed take. On one hand, the same property net operating income (NOI) was quite strong with a year over year increase of 4.3%. This was powered by solid expansion of office and industrial rents. This also led to a 11% increase in funds per unit to 36 cents a share. All that was good. On the other hand the numbers were less impressive if you stripped out some items and started looking at what 2023 will hold. On the same property NOI growth, currency weakness was a big factor (Artis has USD exposure but reports in CAD). This has reversed in Q4-2022 and 2023 comparatives will be far more challenging. Even the FFO growth was far more subtle if you just stripped out lease termination income.

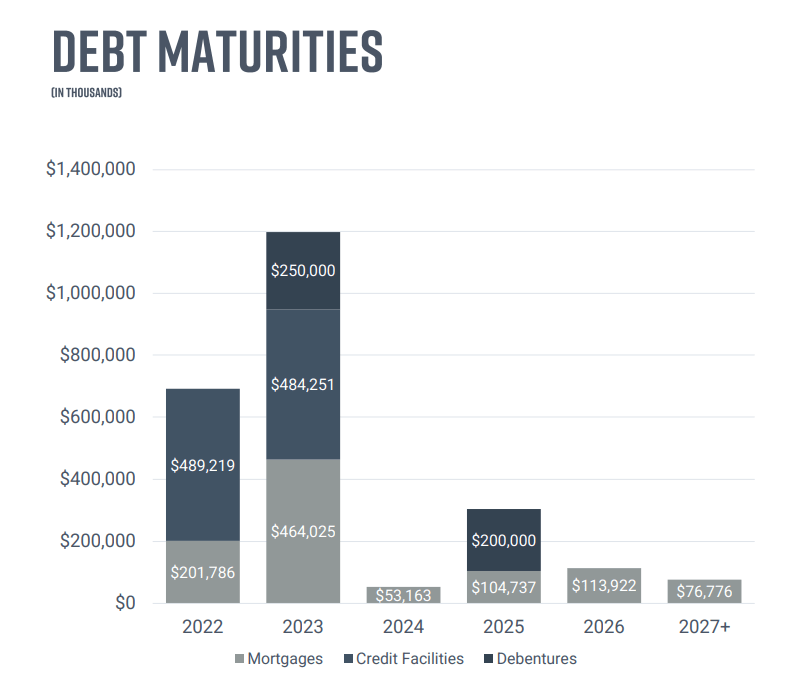

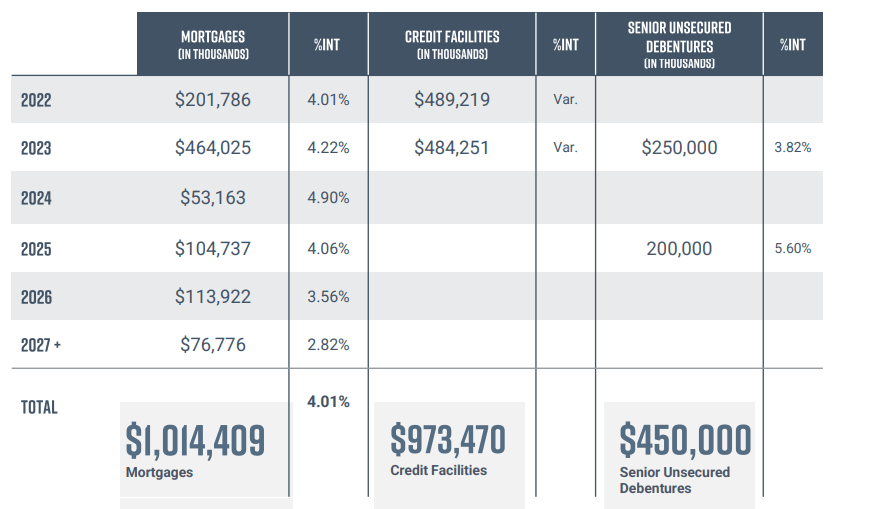

More problematic for Artis is the rate of change on its interest expense. Total financing costs were up almost $8 million vs Q3-2021. Looking out to 2023, year over year interest expenses should rise at least 25% based on where the curve is. Artis is primarily responsible for this and not the interest rate increases. What we mean by that is that Artis threw down the gauntlet on the interest rate bets by having more than half of its debt financed via floating rate credit facility. You can see those amounts here below and they have used close to a billion USD (facility size $1.1 billion).

{kind=link}

These rates have been on a rapid upward trajectory, unlike the rest of the debt.

{kind=link}

The tranche maturing in December 2022 was extended for two years.

On December 1, 2022, the REIT’s revolving term credit facilities agreement was amended to extend the maturity date of the first tranche of the facilities in the amount of $400 million from December 14, 2022 to December 14, 2024, pursuant to the same terms and conditions as the previous agreement.

Source: Q3-2022 Financial Report

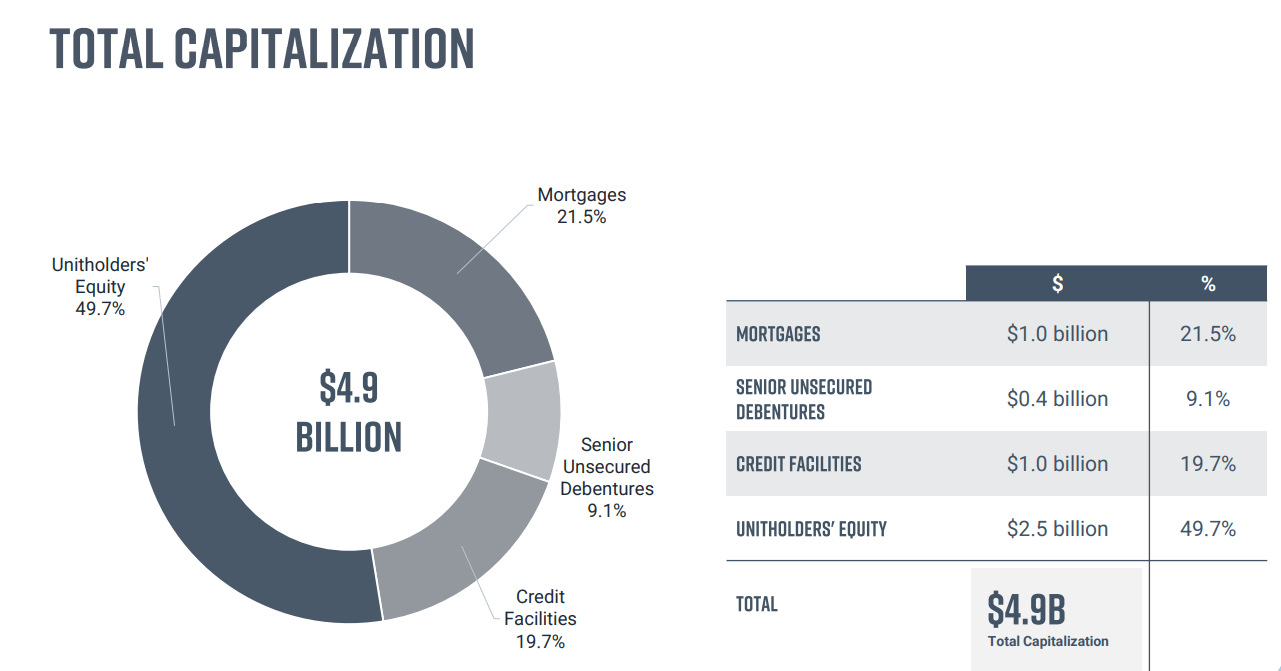

So that gives it some breathing room. However, looking at the numbers above, one thing becomes clear. Artis has the shortest debt maturity profile we have ever seen. This debt wall looks less intimating though when we consider two factors. The first being that the non-mortgage debt is modest in relation to total estimated fair value of the portfolio.

{kind=link}

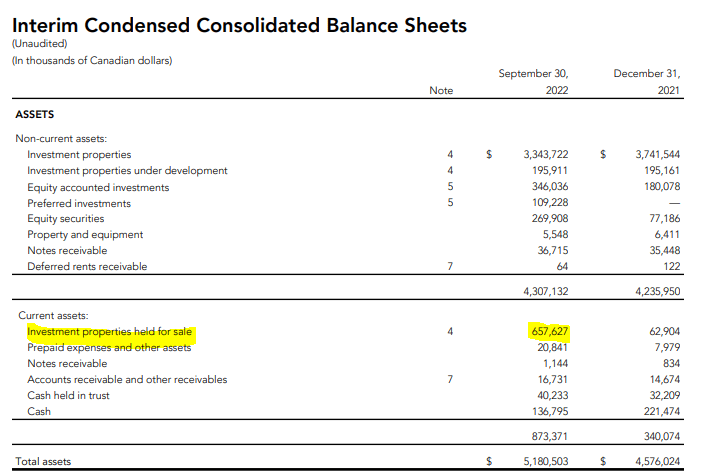

The second and more important being that Artis is working really hard to reduce this. At the end of Q3-2022, Artis had $657 million in assets up for sales with sales agreements of close to $450 million already in place.

{kind=link}

Considering that credit conditions have eased remarkably between the date of release of those results and today, we think some solid good news should be reported when Q4-2022 results are announced.

Outlook & Verdict

We really liked the Artis strategy of asset dispositions followed by accretive buybacks. This has been a good driver of value and most sales have come in at or above IFRS values.

The market seems to be ignoring this though with Artis priced at half of tangible book value. To be fair, it is extending a similar treatment to H&R. The slightly superior multiple for H&R likely comes from its higher industrial and residential exposure.

As long as Artis can manage to dispose assets and buyback units, we see no problem with the idea long term. Unfortunately the plan has taken a slight turn since our last coverage. Artis is focusing increasingly on equity ownership in discounted REITs.

{kind=link}

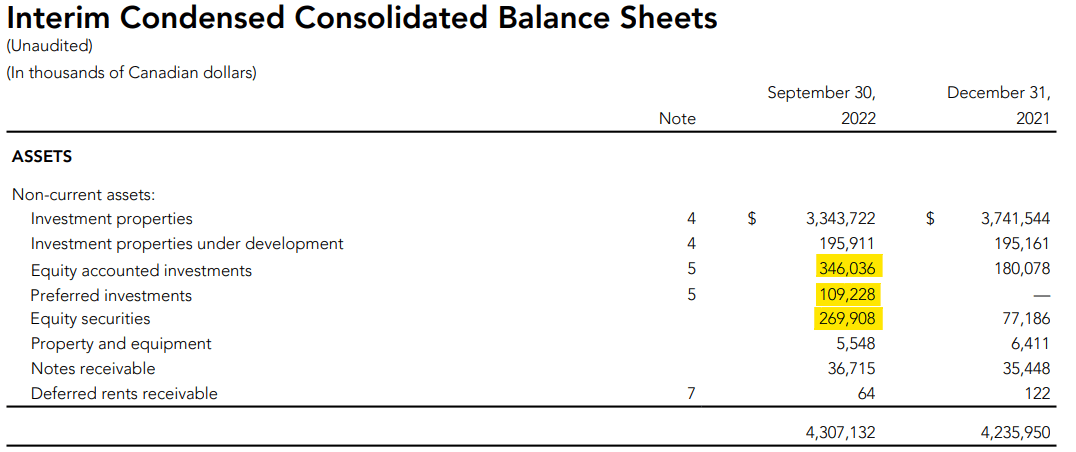

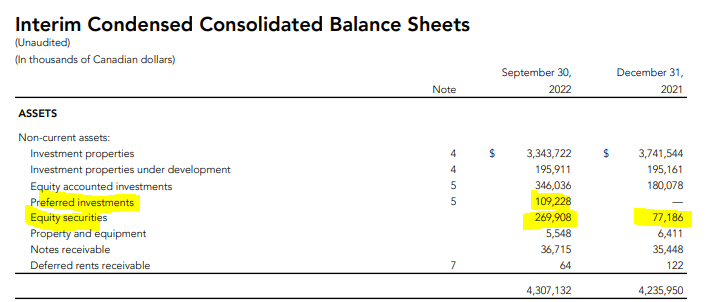

Not all positions are known within the equity securities, but we do have some idea of two major positions.

In 2021, compelling opportunities were identified in the public markets and during the first quarter of 2022, Artis participated in an investor group to acquire Cominar Real Estate Investment Trust ("Cominar"). The REIT's contribution to this transaction ("Cominar Transaction") was $112,000 to acquire approximately 32.64% of Iris Acquisition II LP ("Iris"), an entity formed to acquire the outstanding units of Cominar, and $100,000 of junior preferred units that carry a rate of return of 18.0% per annum. At September 30, 2022, Artis invested in equity securities with an aggregate fair value of $269,908. This includes equity securities of Dream Office Real Estate Investment Trust (“Dream Office”) ( D.UN:CA ) where, together with its joint-actors, Artis announced on June 22, 2022, that it had acquired a 14% ownership position.

Source: Q3-2022 Financial Report

We have covered Cominar before it went private and Dream Office more recently . We don't think this equity investment method is a good strategy here, regardless of the NAV discount. At least on the Cominar front the rate of return is extraordinary and possibly could justify the risk but increasing office exposure here is unwarranted via Dream Office. Even assuming that Dream Office is cheap, we rather Artis buyback its own units. This is because on IFRS NAV, both sets are equally undervalued and Artis' own portfolio has high quality industrial exposure.

The stock does offer a very solid yield of 6.4%. That yield is also very well covered. By our estimates FFO should be close to a $1.20 in 2023 so the 60 cents being paid is very comfortably covered. The NAV discount of over 50% appears juicy as well. Here, we are a little less bullish than the company. We think realistically, the NAV discount is a bit lower than that. Office cap rates are likely at least 0.5% wide of where the company is placing them. But our NAV is also near $15 and the stock is cheap. The overall metrics are quite positive at these levels. For us the biggest negative here is the strategy of using cash to buy other REIT stocks at this time.

Based on this wrinkle we are taking a backseat in this story. The company will still have challenges as the weighted average debt maturity even after this recent extension is about 2 years. Rents remain strong for now but we think a recession will test the company's mettle. Debt to EBITDA was still over 9.0X and we just cannot pull the trigger. We are neutral on this REIT for now and think a long case could have some merit at these depressed prices if done via covered calls.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Artis: 6.4% Yield With A 50% Discount To NAV