TAK - Ascendis: Neutral On Skytrofa's Market Launch Initiating With A Neutral Rating

Summary

- Ascendis is a mid-cap commercial biotech based in Denmark. Currently, it trades around $6.7B market cap, and the company holds $900M cash.

- Skytrofa (TransCon hGh) is Ascendis' lead approved agent for pediatric growth hormone deficiency (GHD), where the commercial update was lukewarm, and we continue to believe the ramp to be slow.

- Skytrofa is a best-in-class growth hormone that showed superior efficacy and a more convenient dosing schedule (weekly vs. daily) over standard-of-care agents.

- We believe the valuation (~$6.7B) seems to be exorbitant for the company's lackluster commercial performance shown so far and uncertainty around commercialization.

- We remain on the sidelines until we see a few positive quarters (beating consensus) of commercial print of Skytrofa's during 2023.

Background

Skytrofa (TransCon hGH) was approved in both US and EU in August 2021 for pediatric growth hormone deficiency ((GHD)) indication based on the positive phase 3 heiGHt trial. The indication described in the label are patient who is one year and older, weighing at least 11.5kg, and are diagnosed with growth failure due to inadequate secretion of the growth hormone ((GH)).

TransCon technology is a proprietary technology from Ascendis Pharma (ASND) that allows the drug formulation to be released through a) sustained systemic release and b) sustained localized release, which is why Skytrofa has an advantage around dosing cycles. The key selling point of Skytrofa is that it is weekly dosing vs. standard of care agents that are daily dosing. There are three trials ongoing or already conducted, a) the heiGHt trial, b) the fliGHt trial has been completed and showed robust data, and c) enliGHten trial is currently ongoing.

- HeiGHt trial analyzed the clinical evidence of Skytrofa in the treatment naïve patient population.

- FliGHt trial explored the potential of "switching" GHD patients from daily GH regimens to once-weekly TransCon hGH

- enliGHten trial is currently ongoing to analyze the long-term safety of the agent.

Interestingly the phase 3 HeiGHt trial showed superiority over Genotropin, 11.2 vs. 10.3 cm/year in annualized height velocity ((HV)) at 52 weeks, which was the key primary endpoint for the trial. In regards to safety, TEAEs related to the study drug were superior, 11.4% vs. 17.4% (Genotropin), which is the standard of care. Most importantly, the SAE rates were comparable, 1.9% vs. 1.8% (Genotropin). Both drugs were relatively safe, and no discontinuation was observed from initiating the drugs.

The company is steadfast in efforts for label extension and geographical expansion.

The company is conducting several additional trials in order to expand to the Asian markets, such as the pediatric GHD phase 3 riGHt Trial, where the enrollment seems to be ongoing based on the company's recent deck. The company also has another Pediatric GHD phase 3 trial in China, where the target recruitment has reached in Q1 2021 in Greater China. Furthermore, we note that the company is currently enrolling patients in the Global adult GHD phase 3 trial; with positive data, the company may be able to extend the label to the adult population.

hGH market seems to be a complex market for new players to penetrate into

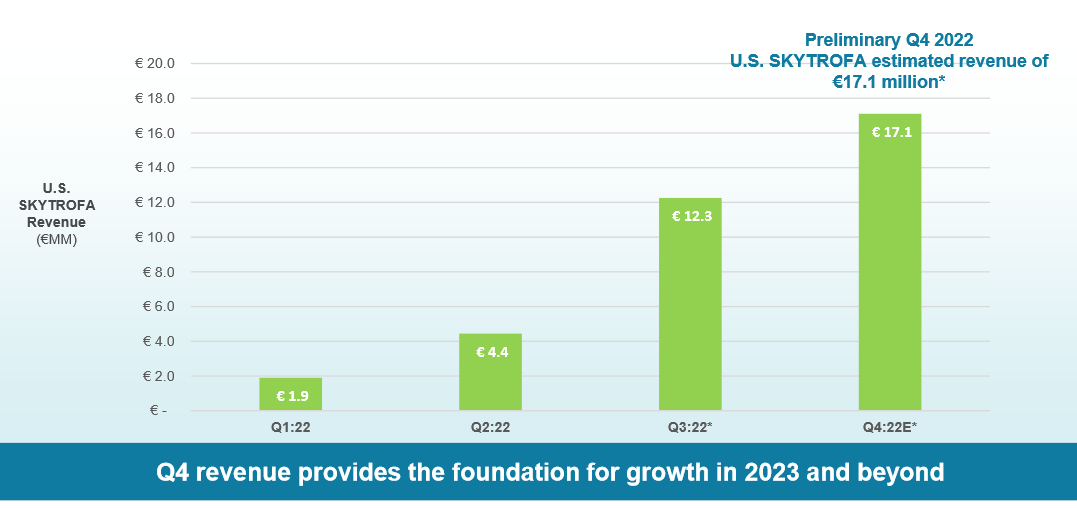

The global human growth hormone ((HGH)) market is estimated to be ~4Bn according to the company, and the US accounts for around 30% being 1.3Bn, and pediatric GHD is estimated to be ~700M in the US. Although the market size looks attractive, we believe there are several caveats to watch out for, the first being a high prescriber inertia from the pre-existing standard of care and market access hurdles (pricing). The company is commercializing TransCon hGH in-house in North America and European countries, although they seem to be planning to launch the products in other regions by finding a commercial partner with local expertise and infrastructure. As shown below, we believe the initial market launch during 2022 seems lackluster, with revenue only reaching <40M, which is significantly lower than what the street initially expected as the market's view around the opportunity seems to be dead set on this product is a "blockbuster" agent. The drug is about to get approved in the EU region, and the company plans to first launch the product in Germany during Q3 2023. We expect a slow EU launch because of notoriously frequent delays in market access in Europe. Moreover, based on the poor US performance, we are unsure how much additional revenue the EU region will add. Several trials are ongoing in the Asian regions, with two phase 3 planned/ongoing, but we believe Asia launch to take another 1-2 years, and uncertainty around market access lurks around the drug in those regions as well.

Sale of TransCon hGH (Company)

{kind=link}

The company's other pre-commercial candidate, TransCon PTH, seems to be addressing an attractive market opportunity

Company Pipeline overview JPM presentation (Company Source)

{kind=link}

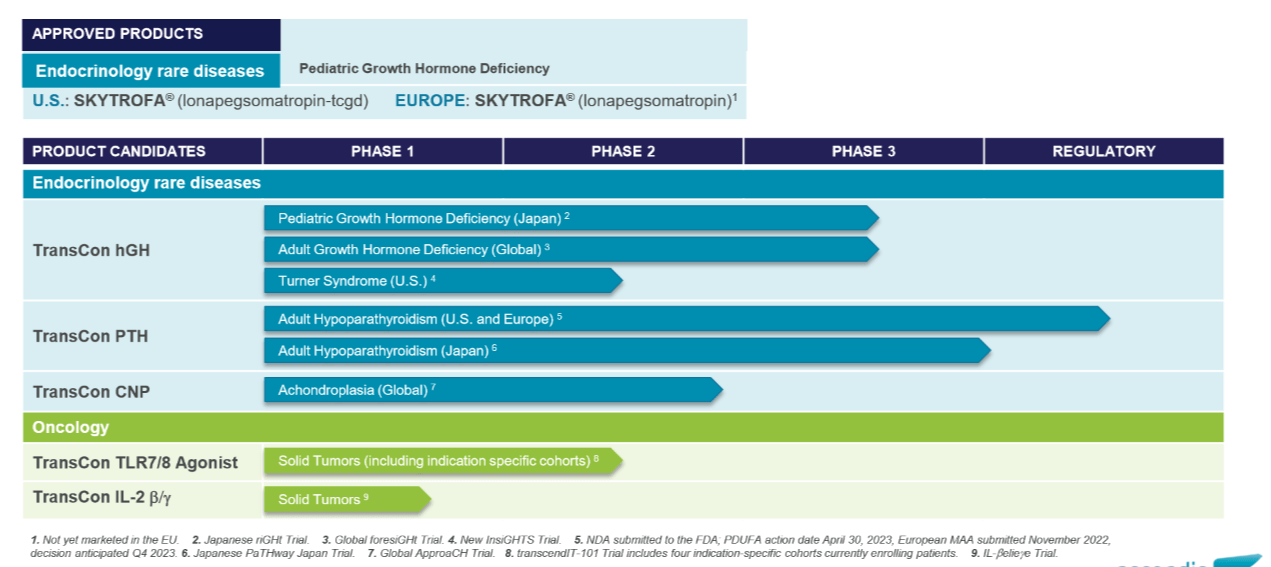

During the recent JPM presentation, the company described its strategy as "Vision 3X3," where the company targets to obtain regulatory approval for three independent endocrinology rare disease segments.

- TransCon hGH, as described above

- TransCon PTH targets adult hypoparathyroidism, and the main target regions are US, EU, and Japan for the company.

- TransCon CNP targets achondroplasia, although the clinical development process seems early (phase 2 is ongoing).

We believe the TransCon PTH, recombinant human PTH that is currently in phase 3 development, seems to be an exciting candidate with a differentiated clinical profile vs. SOC (i.e., Takeda's (TAK) Natpara), mainly around infusion like level of PTH that is stable over time achieved through slow release of the agent through TransCon technology. Furthermore, we believe the clinical data is highly compelling, basing off the phase 2 data that met all the key endpoints, and showed superior profile over Natpara around quality of life improvement, calcium hemostasis, and effect on bone. However, we note that Takeda's Natpara only generated peak sales of around $230M in 2019, before it got pulled out of the market due to manufacturing issue, therefore, the market opportunity in TransCon PTH is still in question and we expect the peak sales to be under $500M.

We are also fairly neutral on TransCon CNP's market potential because BioMarin's (BMRN) Voxzogo seem to have taken a big chunk of the patient bolus when it was first launched. TransCon CNP showed fairly robust data that may be potentially superior to BioMarin's drug Voxzogo , which is once daily subcutaneous agent that is approved in 2H 2021. BioMarin is guiding 2022 sale of Voxzogo to be around $ 130-160M , which we believe should be a good benchmark (upper end expectation) for TransCon's market launch during first few years as the patient bolus has already exhausted. We do believe the drug will sell, as there is always inflow of newly diagnosed patients, albeit the incidence rate (new diagnosis rate) of achondroplasia is fairly low, 1 in every 40,000 births per year.

Risks

Commercial risk, there could be slower than expected market adoption and market access hurdles. Financing risk, the company is yet to be cash flow positive and they may need to raise more capital for commercialization. Furthermore, there are several clinical trials ongoing, any regulatory clinical failure can impact the stock price to the negative side.

Conclusion

We are a fan of Ascendis' interesting technology and strategy to focus on endocrinology related rare diseases; however, we believe the market potential around the company's endocrinology pipeline remains uncertain and we believe the current valuation of the company (EV of 6.34B) is fairly expensive for the risk/reward. Until we see more clarity around the sales print of TransCon hgH during next few quarters, we remain on the sidelines.

For further details see:

Ascendis: Neutral On Skytrofa's Market Launch, Initiating With A Neutral Rating