KFVG - ASE Technology: A Diversified Semiconductor Packaging Play

- ASX provides packaging services to semiconductors companies.

- Both its product and geographical diversification strategies deserve to be highlighted in light of the competition and supply chain issues.

- Revenues are also growing at double-digit figures for the world's number one OSAT play, and profitability metrics are also superior.

- On the flip side, there is the dividend cut warning by SA, plus potential stock volatility at the end of July when second-quarter financial results are announced.

- Offsetting the above two factors are diversification, profitability, operating cash flow generation, and valuations, which all make ASX a buy.

While we tend to focus our attention on the big foundry plays like Taiwan Semiconductor Manufacturing Company ( TSM ), there are other smaller chip plays like ASE Technology Holding Co., Ltd. ( ASX ), with a market cap of $13.6 billion. They tend to go unnoticed, but deserve our attention as supply chain problems come to the fore.

The company has become attractive after a drop of more than 30% from its July 2021 high of $9.6 as shown in the chart below. It now trades for around $6.

The aim of this thesis is to assess whether the company constitutes an investment case by considering the fundamentals, together with key data from the first quarter of 2022 financial results published at the end of April.

I start with ASX's strategy in a highly competitive semis (semiconductor) market which is now being increasingly geared by geopolitical factors like the trade war between the U.S. and China, amid more calls for regionalization of supply chains.

ASX's Strategy for a Competitive Environment

The company provides IC or integrated circuit packaging services. This is normally the final step in transforming semis manufactured by the likes of TSMC, for example, into functional smartphone processors for customers like Qualcomm ( QCOM ), which, as a fabless play, outsources the manufacturing of the chips it designs to foundry operators in East Asia.

Now, TSMC is a major foundry operator with a $424.7 billion market cap, which in addition to producing chips has also diversified into packaging technology and testing, and can be viewed as an integrated chip play in the semiconductor supply chain. Thus, with pure-plays as well as foundry operators diversifying into packaging, this is a highly dynamic and competitive marketplace.

Here, ASX's strategy has been two-pronged.

First, it has evolved from traditional packaging to more of an OSAT (outsourced semiconductor assembly and test) play, as it offers third-party IC packaging and testing services. In other words, it packages silicon devices made in foundries into finished products and also tests the devices prior to shipping them.

In this respect, the Taiwanese company competes with U.S.-based Amkor ( AMKR ) as another contract OSAT supplier, with the companies possessing a combined 43% of the global sales market share as of September last year.

However, in contrast to Amcor, ASX has diversified beyond OSAT, and is also a key provider of electronics manufacturing services, or EMS, with its USI (Universal Scientific Industrial) subsidiary. Additionally, it acquired French-based Asteelflash Group in December 2020 for $421.5 million . Consequently, with EMS revenues constituting 42% of overall sales in Q1, it can be said that the company has successfully diversified revenues away from the highly competitive packaging market.

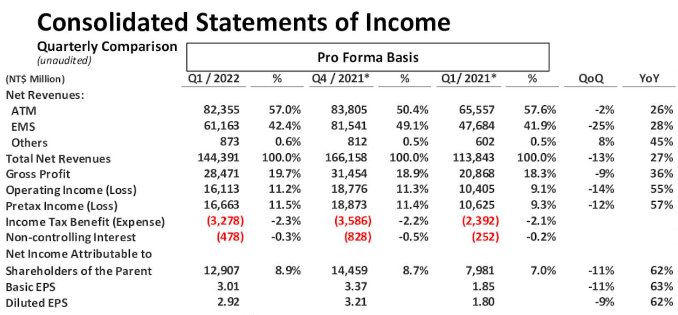

Segmental income in Q1-2022 (www.seekingalpha.com)

{kind=link}

The second part of ASX's strategy is that, in addition to product diversification, the company is also positioning itself to avert geopolitical risks. Thus, the Europe-based Asteelflash (with operations in the U.S.) acquisition was a judicious one in view of a rethink and redefining of the semiconductor supply chain from a globalized one centered around East Asia to a more regionalized one. At the same time, the company has been disposing of its factories in China since 2020, as I will further elaborate in the finances section below.

Revenues and Profitability

ASX is at the top spot in the list of the ten largest OSAT plays by revenues in the third quarter of 2021. Now, its double-digit rate of growth of 20.86% for the last reported quarter, compared to only 20.41% for Amkor, shows that it is growing much more rapidly. For this purpose, the Taiwan-based company was able to more than offset weakness in certain sectors with strength in others, such as networking, high-performance computing, and automotive. The upbeat revenue growth was also achieved on the back of China lockdowns, which resulted in component and chip shortages.

Now, due to high competition and the need to continuously innovate, OSAT implies a high level of capital expenses and R&D costs, signifying that it is also important to assess profitability.

In this case, operating profit margins have been trending slightly lower, as shown in the table below during the last two quarters as a result of the rising cost of business, which is in turn due to high inflation throughout the world. Operating expenses also increased by $1.9 billion as a result of the scaling of both the ATM (Assembly Testing and Material) and EMS businesses.

Still, when compared to Q1-2021, higher margins were obtained in the last reported quarter due to an improvement in operating efficiency and product mix.

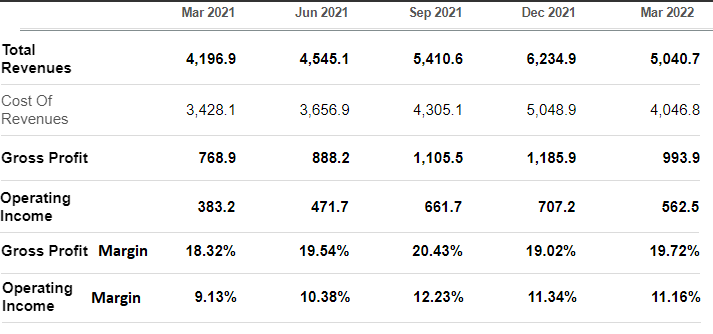

Revenues and profitability for Q1 (www.seekingalpha.com)

{kind=link}

Pursuing further, the company had cash and equivalents of $3.1 billion at the end of the first quarter with a debt of $5.3 billion. Part of the cash generated was due to selling assets in China amounting to $6.8 billion for the fourth quarter of 2021 and $5.6 billion during the same period in 2020. The net debt-to-equity ratio was 52% as reported in Q1.

Looking forward, while the company has reduced its Chinese footprint, it still faces potential disruptions for its manufacturing facilities in that country due to the strict nature of the Covid-19 mitigation strategy in place. Thus, lockdowns that started on March 27 and lasted for more than two months could have an impact on sales for the second quarter, which starts in April and ends in June of this year.

Therefore, expect some volatility in the stock price at the end of July when second-quarter financial results are disclosed. In this case, as seen with Cisco ( CSCO ) for its third quarter of 2022 financial results, component-related supply disruption from China caused a revenue shortfall of $300 million, sending the stock lower by about 15% in May. Consequently, as ASX's second quarter generally constitutes a seasonal trough signifying lower shipments, the company could either be impacted by lower production volumes or face higher expenditure incurred as a result of expedited shipping, which could in turn adversely impact profitability. Thus, there are risks of further downside.

Valuations and Key Takeaways

In this respect, the 30% downside shown in the introductory chart has resulted in attractive valuation metrics. Thus, ASX is undervalued with respect to the median for the IT sector by at least 60% as shown in the table below. The company could climb back to the $7-7.2 level after a 20% upside. Moreover, the company's profitability grade is very good with an EBITDA margin outclassing the sector median by nearly 7%.

Valuation and profitability grades (www.seekingalpha.com)

However, trailing free cash flow (levered) remains an issue as per the C score in the above table, and is more problematic given the fact that the company pays dividends at an enticing yield of 4.75%.

To this end, the company displays warning signs for dividends as, according to SA, the company has a dividend safety score of F . One of the reasons provided is that companies in this category have historically proceeded to dividend cuts, which could be detrimental to income-seeking investors, with SA stressing on the cash dividend payout ratio of 92.61%. This means that the company retains only a tiny amount of money after it makes distributions to shareholders.

However, I am not too worried at this moment, as ASE generates strong cash from operations of over $500 million per quarter during the last six quarters, with over $1 billion generated in the fourth quarter of 2020 and 2021 due to asset sales in China as I mentioned earlier on. Thus, after accounting for capital expenditures of around $619 million per quarter, the company has the financial capability to pay the $650 million of annual dividends to common stockholders. Thinking aloud, in the worst-case scenario, there could be a dividend cut as the company raises capital expenses in order to make an opportunistic acquisition. However, it should recoup costs rapidly. The reason for this is that it has a high CAPEX to Sales ratio as shown in the table above.

Finally, taking into consideration diversification, profitability, cash generation, and valuations, ASX makes for a buy, but do expect continued volatility as part of the contagion effect from the wider tech sector, especially at the end of July when Q2's revenues are announced.

For further details see:

ASE Technology: A Diversified Semiconductor Packaging Play