ASEA - ASEA: China Down But It's Not All Doom And Gloom For Southeast Asia

2023-08-17 18:15:07 ET

Summary

- The growth and inflation outlook for Southeast Asia continues to diverge from the developed world.

- An ongoing external slowdown, particularly in China, is a major overhang, though it also pushes ASEAN central banks closer to a monetary policy pivot.

- The FTSE Southeast Asia ETF remains priced at undemanding levels relative to its underlying growth potential.

The Global X FTSE Southeast Asia ETF ( ASEA ), a proxy for the ASEAN ('Association of Southeast Asian Nations') economy comprising Singapore, Malaysia, Indonesia, Thailand, and the Philippines, has seen a marked pullback over the last month (but still up modestly since I last covered the name). While the long-term Southeast Asian bull case remains intact, the region's trade linkages to a slowing Chinese economy are proving to be a liability, and investors are, perhaps rightly, paring back exposure.

This needs to be balanced, however, against easing inflation throughout the region, which could pave the way for a series of policy rate cuts in the coming months. Surplus countries like Indonesia and Thailand are likely first in line for monetary easing, helped by their real policy rate differentials. ASEA's largest exposure, Singapore, on the other hand, will have limited room to diverge from the Fed, given its exchange rate targeting policy. But the ASEA ETF's outsized exposure to Singaporean banks also means 'higher for longer' rates isn't such a bad thing. In contrast, lower rates in Indonesia/Thailand bode well for overall growth, creating a compelling near-term setup for the region.

Plus, there's always optionality from the China stimulus, particularly on the services side (mainly tourism), which ASEAN countries over-index to. With the fund currently priced at ~11.7x P/E (vs. mid-teens % long-term earnings growth for emerging Asia) and offering a ~3% yield, ASEA is still worth a look.

Fund Overview – A Competitively Priced Portfolio of ASEAN Champions

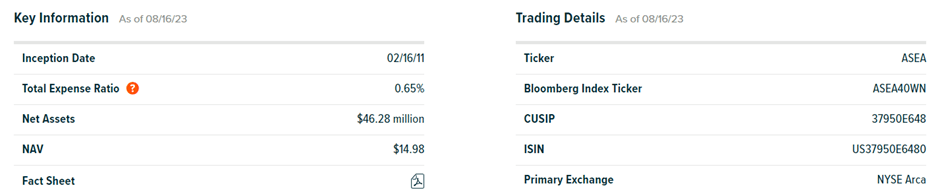

The Global X FTSE Southeast Asia ETF tracks, before expenses, the total return (yield and price) performance of the FTSE/ASEAN 40 Index, a basket of the forty largest ASEAN companies within the FTSE All-World Index (subject to size and liquidity criteria). The ETF's net asset base remains notably unchanged at ~$46m, along with its 0.65% expense ratio. Given the lack of ETF options for regional ASEAN exposure, ASEA remains a cost-effective option, in my view.

{kind=link}

The fund is spread across 41 holdings (including cash), with Financials still the largest sector allocation by far at 57.9%. The Financials split skews mainly toward regional banking (46.9%), with major banks contributing the remaining 11.6%. Other notable sector exposures include Communication Services (7.9%), Industrials (5.6%), and Energy (4.9%); the latter two sectors have gained share at the expense of Real Estate (4.8%) and Consumer Staples (4.8%) over the last quarter. The bank-heavy fund also maintains a low equity beta to comparable developed and emerging market indices, highlighting its defensive characteristics.

{kind=link}

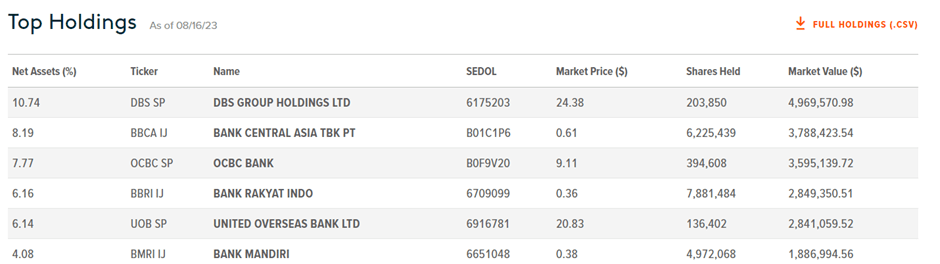

The single-stock allocation is also largely unchanged, with ASEA's six largest holdings still comprised of the largest banks in the region. Singapore-based bank DBS Group ( DBSDF ) leads the way at 10.7%, followed by Indonesia-based PT Bank Central Asia ( PBCRF ) at 8.2%, as well as another major Singaporean bank, OCBC ( OVCHY ) at 7.8%. Indonesian banking leaders PT Bank Rakyat Indonesia ( BKRKY ) and PT Bank Mandiri ( PPERY ) also feature prominently in the top-ten list. While the ASEA fund now trades at a wider premium to book value (justified by a higher 13.5% return on equity), its P/E remains undemanding at 11.7x 2023 earnings.

{kind=link}

Fund Performance – Near-Term Rebound; Strong Distribution Intact

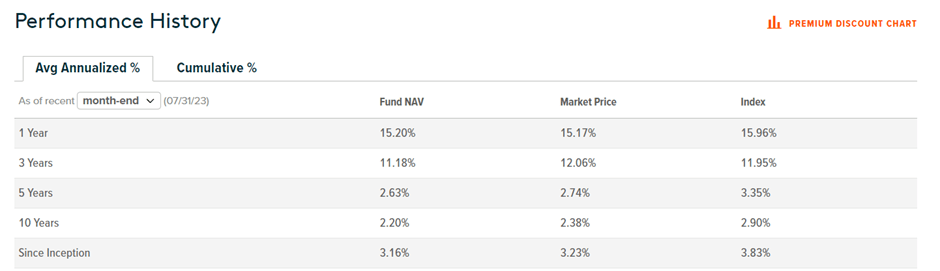

The ASEA ETF has outperformed comparable single-country Southeast Asian ETFs over short and longer time frames. The last year, in particular, has seen the fund's performance stand out at +15.2% (NAV and market price terms), mostly defying the China headwinds. And over a three-year time frame, the annualized compounding is similarly strong, at +11.2%. In turn, this near-term outperformance has further boosted the otherwise lackluster capital gains track record since inception (+3.2%).

{kind=link}

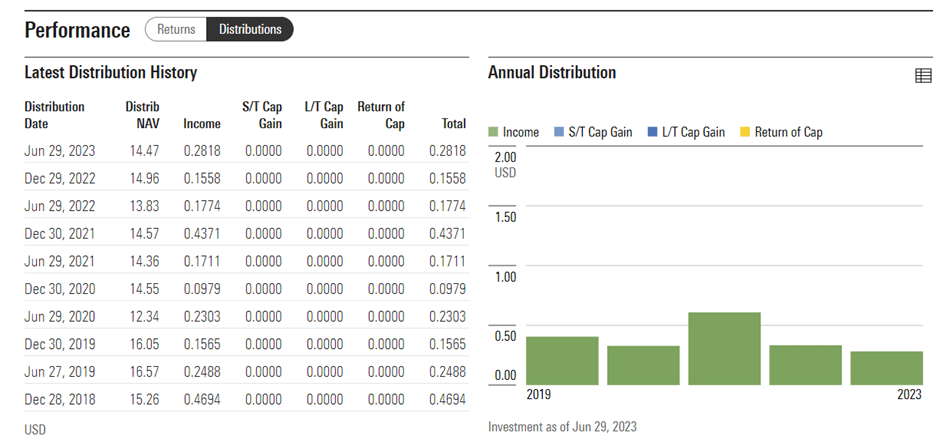

The fund also appeals for its stable income through the cycles, currently at a 30-day yield of 3.3%. Helped by its exposure to cash-generative bank franchises, ASEA generally sees limited drawdowns to its capital or income - even through last year's steep monetary tightening and the COVID pandemic. Yet, it tracks regional growth well, as evidenced by the upsized distribution in H1 2023. So in the likely event that GDP growth continues at a healthy clip into the coming years, ASEA investors should also benefit via attractive income growth.

{kind=link}

A Much Better Macro Setup for ASEAN as Tailwinds Loom

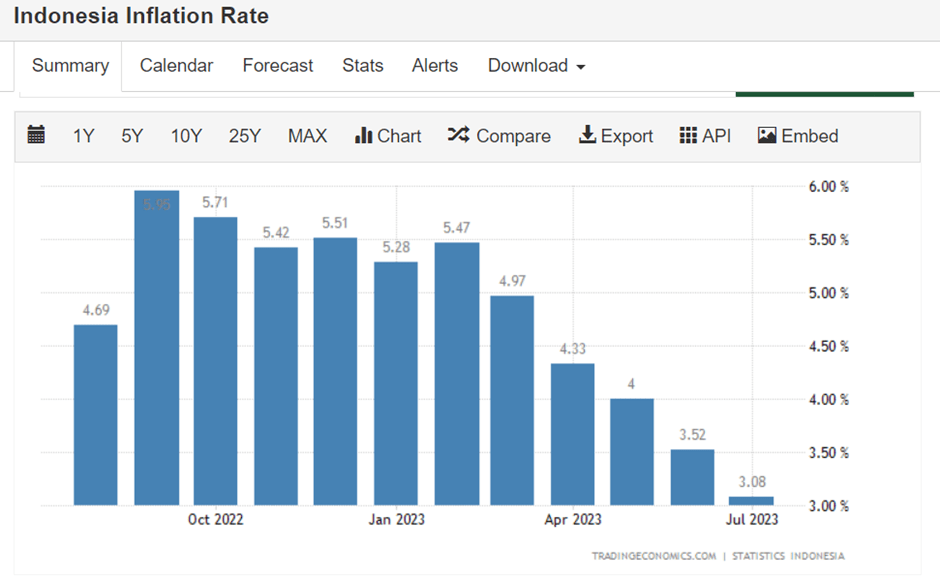

Amid an uncertain growth and inflation backdrop for much of the Western world, investors should perhaps consider looking east. Unlike the 'sticky' inflation seen in Europe/UK/US, the ASEAN nations have seen inflation pressures quickly revert to their respective inflation target ranges. Alongside the ongoing growth slowdown overseas, particularly in China, all signs now point to potential rate cuts into the back half of this year.

For surplus Southeast Asian countries like Indonesia, with a wide real rate differential cushion (an important consideration for capital flows), it's more a question of when not if. The case for rate cuts isn't quite as clear-cut for the rest of ASEAN, given their susceptibility to capital outflows, so outside of Indonesia and Thailand, a neutral stance is the most likely scenario.

Singapore is unique, as it is seeing stickier core inflation (relatively speaking) and implements an exchange rate-targeted monetary policy, essentially limiting its room to diverge from the Fed. Higher rates in Singapore are a good thing for the ASEA portfolio, though, given its Singaporean exposure is mainly via banks. As for the ex-Singapore portfolio (mainly Indonesia and Thailand), where non-banks feature more prominently, monetary easing bodes well for future upside.

{kind=link}

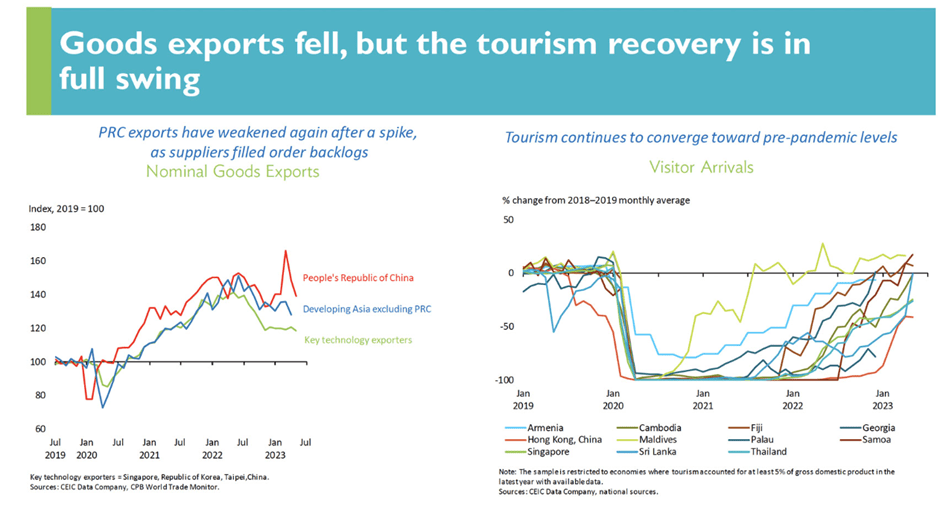

The flip side of the easing argument is growth – after all, rate cuts are also on the table because of the lower near-term growth outlook. Depending on the extent of the cyclical downturn once the lagged effects from global rate hikes kick in, downside earnings revisions could well be on the cards across the region. And then there's China, where the post-COVID reopening has underwhelmed in the face of a range of structural issues. In response, Beijing has committed to a multi-pronged stimulus (fiscal and monetary policy), but in the likely event there isn't a quick fix, ASEAN's linkage to China could prove to be a drag in the interim. Still, the region's exposure is services-based (specifically tourism), and given the continued tourism growth from China and the rest of the world, any fallout could also be less than feared. Plus, there's the growth impulse from supply chain 're-shoring,' which should keep a floor under the corporate earnings algorithm long-term.

{kind=link}

China Down, but It's Not All Doom and Gloom for Southeast Asia

ASEA has pulled back since its July rally, despite speculation that policy rate cuts may soon be on the horizon for the region's central banks. The key drag remains China, which has fallen well short of its post-reopening promises and driven earnings revisions lower. There is still long-term hope, however, as ASEAN remains a key beneficiary of the 'China+1' diversification strategy globally. And as key ASEA country exposures like Indonesia and Thailand see their real rate differentials widen, helped by a lack of core inflation' stickiness,' there's ample room for a monetary policy boost down the line.

Also helping is that ASEA mostly derives its banking exposure from Singapore, a country with limited monetary room to diverge from the Fed by virtue of its exchange rate targeting. So with the latter headed for a 'higher for longer' rate environment, concerns around Singapore bank margin headwinds from lower rates could be overblown. At ~12x this year's earnings, ASEA remains cheap relative to its underlying growth potential and could easily grow into its valuation from here.

{kind=link}

For further details see:

ASEA: China Down, But It's Not All Doom And Gloom For Southeast Asia