META - ASG: A Great Diversifier In Today's Top-Heavy Market

2023-12-13 07:22:28 ET

Summary

- The Liberty All-Star Growth Fund focuses on long-term capital growth and has an 8.02% current yield.

- The fund's share price has declined by 43.23% since June 2021, underperforming the S&P 500 Index.

- The fund offers exposure to small-cap stocks, providing diversification for investors seeking a variety of company sizes.

- The fund pays out 2% of its NAV quarterly, which results in a variable distribution depending on the performance of the overall stock market.

- The fund's shares are currently trading at a reasonable discount to NAV and the fund has managed to fully cover its distribution year-to-date.

The Liberty All-Star Growth Fund ( ASG ) is a very interesting closed-end fund that focuses on the long-term growth of capital. It does not completely neglect income though, as the fund has an 8.02% current yield, but income is certainly not its priority, and the distribution tends to vary substantially from quarter to quarter based on the performance of the fund. This is not exactly atypical for a closed-end fund as the general business model for these entities is to maintain a relatively stable portfolio value and pay out all of their investment profits to the shareholders. As investment profits vary from period to period depending on the performance of the market, these distributions can also vary.

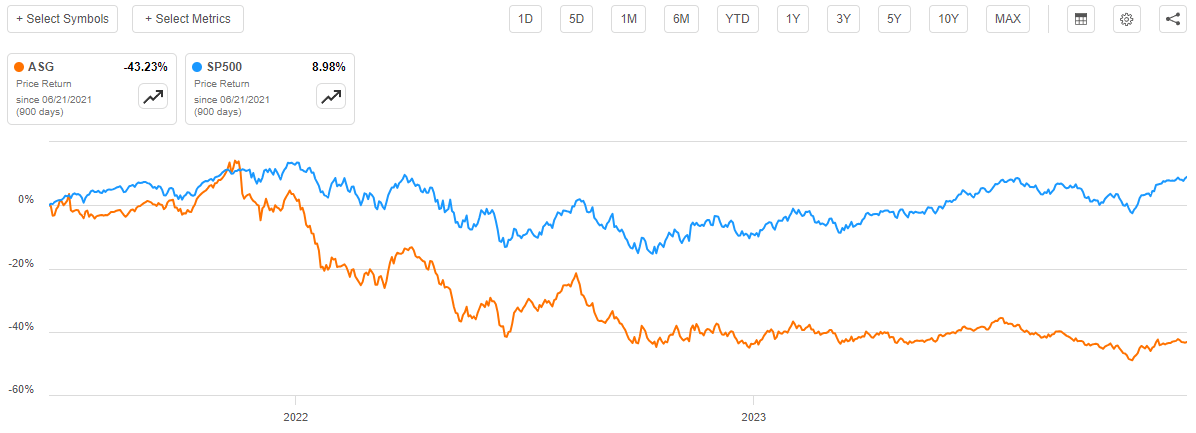

It has been quite some time since we last discussed the Liberty All-Star Growth Fund. My most recent article on this fund was published back in June 2021. It goes without saying that there was a very different market climate back then, as the newly printed money from the various pandemic-era programs was sloshing through the economy and interest rates were so low as to effectively render money free for most institutional borrowers. That changed in 2022 when the Federal Reserve tightened monetary policy and caused a widespread market decline. As such, we can expect the performance of a growth fund like this one to not be very impressive over the intervening period. This is certainly the case, as the Liberty All-Star Growth Fund has seen its price decline by 43.23% since the time that my previous article was published:

{kind=link}

As we can clearly see, that is worse than the S&P 500 Index ( SP500 ), which is actually up 8.98% since June 20, 2023. I must admit that it is rather surprising that the S&P 500 Index actually managed to register a gain over the period, but just under 9% in two-and-a-half years is not a particularly impressive gain.

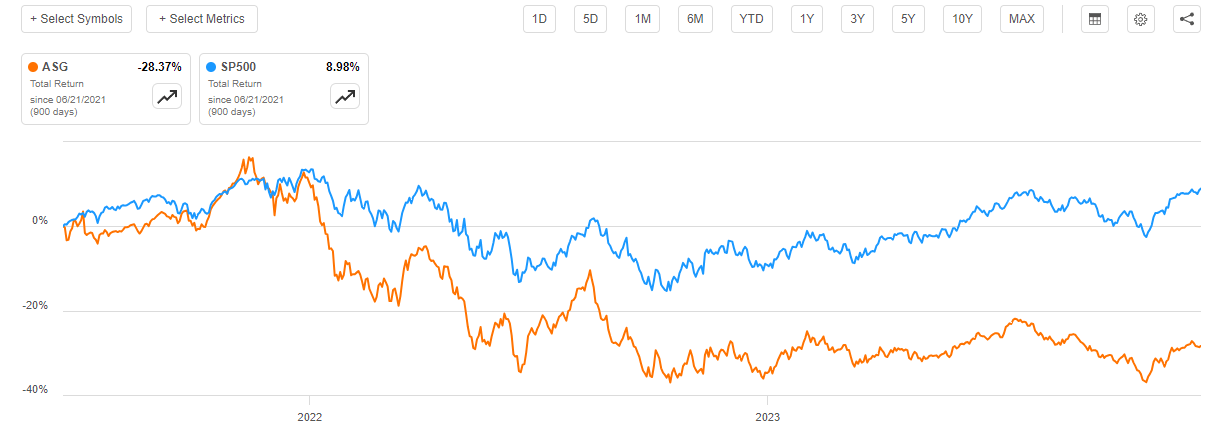

As already mentioned though, the Liberty All-Star Growth Fund has a tendency to pay out all of its investment profits during a given period to its shareholders. As such, we can generally expect that this would cause the fund’s share price to decline more than an index that does not. Thus, it is best to include the distributions that the fund paid out in any discussion of a fund’s performance. After all, a large enough distribution can actually offset declines in the share price, which has been the case with some energy infrastructure funds. If we do that with this fund, we see that shareholders only lost 28.37% since the date that my previous article was published:

{kind=link}

This is still not a performance that will endear anyone to the fund, especially considering that the S&P 500 Index was actually up over the same period. However, this fund does include exposure to a great many companies that the market index does not. This is especially true at the low end, with small-cap stocks accounting for a not insignificant percentage of the Liberty All-Star Growth Fund. That is something that could appeal to those investors who are seeking to diversify their portfolios across various company sizes.

About The Fund

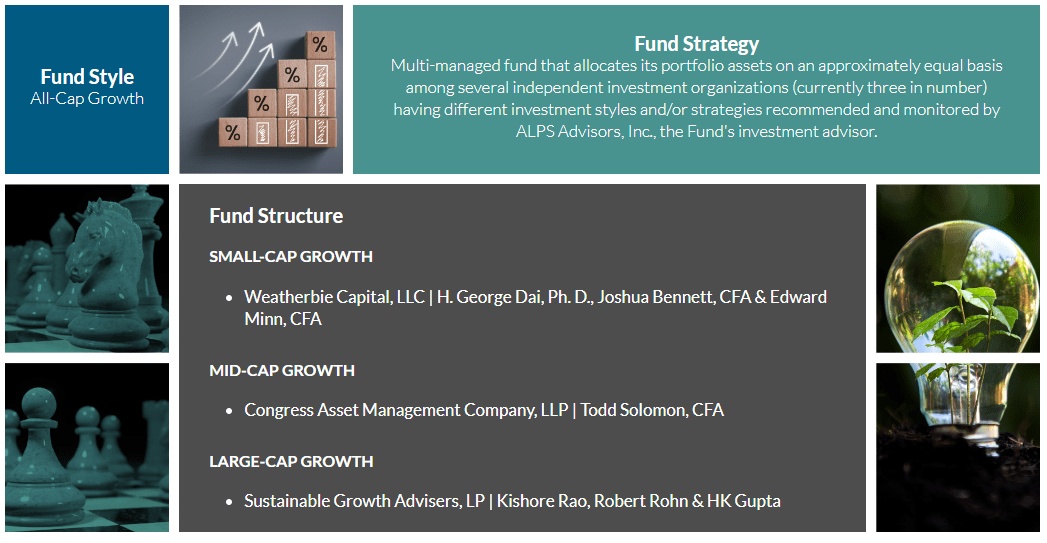

According to the fund’s website , the Liberty All-Star Growth Fund is an all-cap growth fund that employs a few different investment styles, objectives, and strategies. Here is how the website describes the fund:

Multi-managed fund that allocates its portfolio assets on an approximately equal basis among several independent investment organizations (currently three in number) having different investment styles and/or strategies recommended and monitored by ALPS Advisors, Inc., the Fund’s investment advisor.

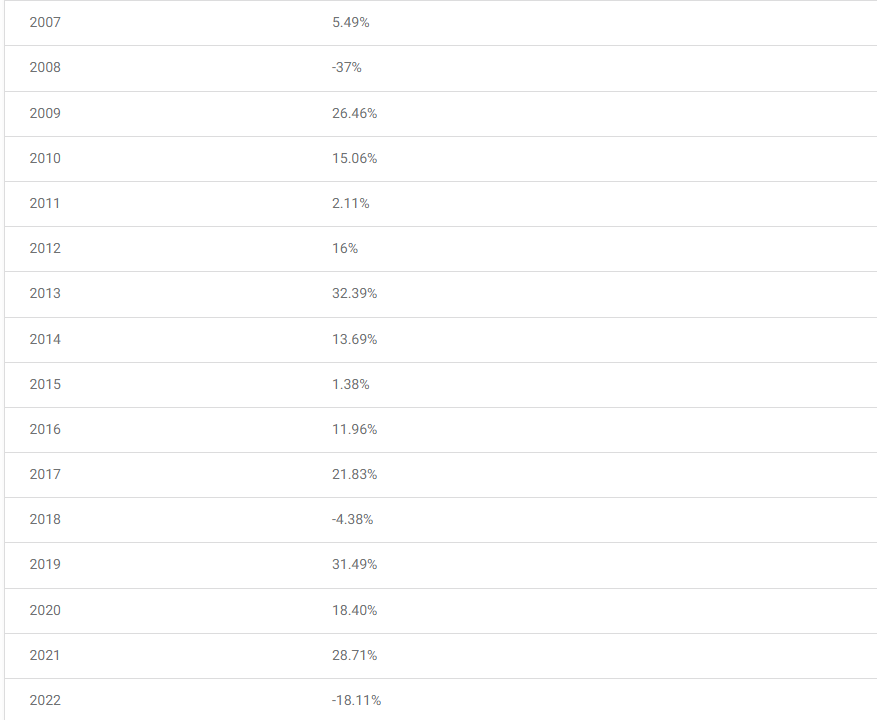

This is a somewhat unique fund considering that parts of the fund’s portfolio can be invested in different ways. As I pointed out in a recent article , it somewhat resembles the RiverNorth/DoubleLine Strategic Opportunity Fund ( OPP ) but that fund focuses primarily on income and it only has two investment advisors. This fund obviously has three (or potentially more). The Liberty All-Star Growth Fund is also not specifically focused on the generation of income for its shareholders, but it does tend to have a reasonably attractive yield. That yield comes from the fund’s habit of paying out its investment profits to the shareholders as opposed to relying on share price appreciation as an index exchange-traded fund does. As common stock indices can deliver fairly attractive total returns, we can quickly see how such a strategy can result in a fund having an attractive yield even though it is not really trying to provide its investors with income. For example, consider the following annual total returns for the S&P 500 Index:

{kind=link}

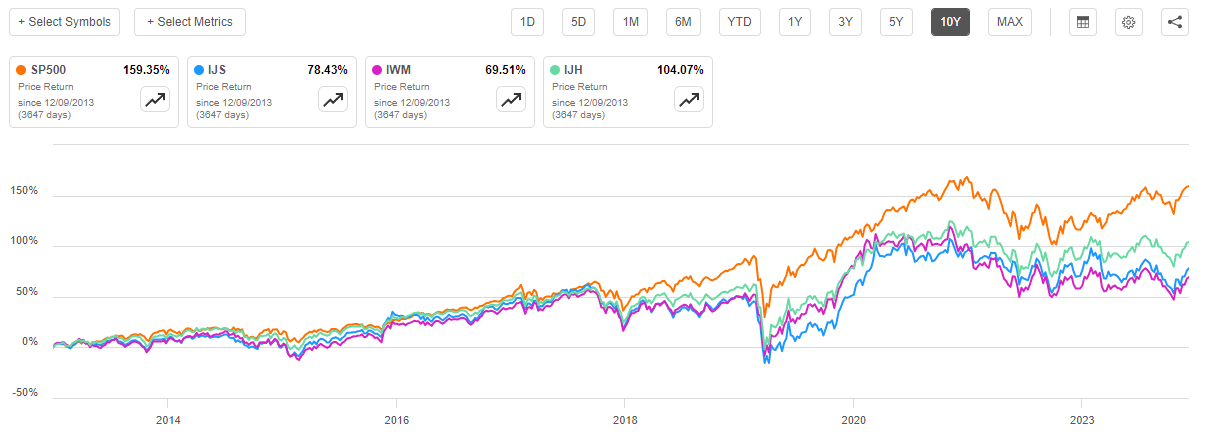

The S&P 500 Index has beaten both small-cap and mid-cap indices over the past decade, as shown here:

{kind=link}

This outperformance by large-cap stocks is generally considered an outlier, though. During most historic rolling ten-year or twenty-year periods, small-cap and mid-cap stocks have outperformed large-caps. This is due to the fact that small-cap and mid-cap companies are considered to be riskier than large-cap companies, and so they should theoretically give higher returns. This is in line with the primary rule of finance, which is “higher risk equals higher potential rewards.”

The Liberty All-Star Growth Fund invests in companies of all sizes, which we can very quickly see simply by looking at the largest positions in the fund. Here they are:

Fund Website

Obviously, Microsoft ( MSFT ), Amazon.com ( AMZN ), Visa ( V ), and UnitedHealth Group ( UNH ) are large-cap stocks. After all, these companies are generally found in the largest positions list of just about every domestic stock fund, including S&P 500 Index funds. The remaining companies on this list are not nearly as large, however.

| Company |

| Current Market Capitalization |

| SPS Commerce ( SPSC ) |

| $6.73 billion |

| Vertex Inc. ( VERX ) |

| $4.37 billion |

| FirstService Corp. ( FSV ) |

| $7.29 billion |

| Glaukos Corp. ( GKOS ) |

| $3.10 billion |

| Deckers Outdoor Corp. ( DECK ) |

| $17.89 billion |

| Progyny Inc. ( PGNY ) |

| $3.48 billion |

These are companies that are not going to be found in many other funds, as they are too small. Thus, this fund can provide exposure to a number of firms that an ordinary portfolio consisting of various large-cap or even broad-market funds will not provide. That is something that obviously is appealing from a diversification perspective. Over the past few weeks, I have seen a number of comments on my articles that suggest that there are several investors who wish to reduce their exposure to the ten or so enormous companies that are found in every domestic common equity fund. This fund appears to be one way to help someone obtain that desired diversification, as it invests in all market capitalizations equally.

This is, in fact, a core aspect of the fund’s strategy. As the description above suggests, this fund allocates its assets equally between three buckets. Each of these three buckets is managed by a different investment firm. At the moment, the three buckets are small-cap growth, mid-cap growth, and large-cap growth:

{kind=link}

As the fund allocates its assets relatively equally to the three sizes, we can expect that it will not be heavily weighted to large-cap stocks as a typical all-market fund would be. After all, the weightings of the largest positions in the Wilshire 5000 are not really that much different than the weightings of the largest positions in the S&P 500 Index:

| Company |

| Weighting in Wilshire 5000 |

| Weighting in S&P 500 Index |

| Apple ( AAPL ) |

| 6.21% |

| 7.09% |

| Microsoft |

| 6.15% |

| 7.10% |

| Amazon.com |

| 3.03% |

| 3.42% |

| Nvidia ( NVDA ) |

| 2.34% |

| 2.85% |

| Alphabet ( GOOGL ) |

| 1.80% |

| 2.08% |

| Meta Platforms ( META ) |

| 1.64% |

| 1.89% |

| Alphabet ( GOOG ) |

| 1.51% |

| 1.79% |

| Tesla ( TSLA ) |

| 1.33% |

| 1.57% |

| UnitedHealth Group |

| 1.21% |

| 1.40% |

As we can see, the presence of all of the additional stocks in the Wilshire 5000 does not bring down the weightings of the largest positions very much compared to their weightings in the S&P 500 Index. As such, we can assume that the S&P 500 Index itself is a substantial percentage of the total weighting of the Wilshire 5000. I cannot find an exact figure as of the time of writing, however. However, this still shows us that any fund that is benchmarking itself against either the Wilshire 5000 Index or the S&P 500 Index will almost certainly have very large weightings to the same handful of stocks. The fact that this fund is placing greater emphasis on small-cap and mid-cap companies than the Wilshire 5000 Index should improve its diversification compared to most other funds. That is something that should prove very attractive to any investor who is attempting to reduce their exposure to the “Magnificent 7” or the technology sector in general.

The fund’s diversity relative to the S&P 500 Index extends beyond simply the largest positions in the fund. Here are the holdings of the fund’s entire portfolio, organized by sector:

Fund Website

The Information Technology sector is 29.10% of the S&P 500 Index. As we can see, the Liberty All-Star Growth Fund is somewhat underweight in that sector relative to the index. However, it is overweight Healthcare and Financials, as Financials account for 12.93% of the index and Healthcare accounts for 12.66%. I will admit that I am not particularly worried about the Healthcare overweight, however. When we consider the demographics of the United States, Europe, and Japan, we can very quickly see that the wealthy nations of the developed world are all seeing their citizenry getting older. Older people tend to spend much more money on healthcare than younger people do. As such, it seems almost certain that this will cause the revenues and profits of many healthcare companies to grow over the coming years and even the coming decades. As such, a bit of an extra allocation to healthcare companies is probably not a bad thing.

Overall, this fund appears to be somewhat more balanced in terms of both its individual company weights and sector weightings than either of the two major indices that include large-cap domestic stocks. This is quite nice for any investor who is seeking to reduce their overall exposure to the relatively small number of companies that have come to dominate the market in recent years.

Distribution Analysis

As discussed earlier in this article, the Liberty All-Star Growth Fund appears to be focusing its investment objective on the long-term growth of capital. That objective does not lend itself very well to the generation of income. After all, most American growth companies do not have particularly impressive dividend yields since they reinvest most to all of their earnings. The high valuations in the American stock market also contribute to the general low yield of common equities. This fund does have a way around that though, as it employs what is known as a managed distribution. The website explains how this works:

The current policy is to pay distributions on its common shares totaling approximately 8 percent of its net asset value per year, payable in four quarterly installments of 2 percent of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. The fixed distributions are not related to the amount of the Fund’s net investment income or net realized capital gains or losses and may be taxed as ordinary income up to the amount of the Fund’s current and accumulated earnings and profits. If, for any calendar year, the total distributions made under the distribution policy exceed the Fund’s net investment income and net realized gains, the excess will generally be treated as a non-taxable return of capital, reducing the shareholders’ adjusted basis in his or her shares. If the Fund’s net investment income and net realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute net realized capital gains and pay income tax thereon to the extent of such excess.

The expectation is that this policy will result in the fund paying out its investment gains over time. The end result is that the fund’s distribution increases during periods of strong market performance and decreases during periods of weak market performance. This is due to the impact that market performance will have on the fund’s net asset value. The real downside to this policy, though, is that the fund will end up distributing capital even when it suffers net losses. That is obviously destructive to the fund’s net asset value if it persists for extended periods and will make it more difficult for the fund to claw its way back to even when the fund has suffered a string of losses. That could at least partially explain why the fund’s share price was so devastated by the bear market of 2022.

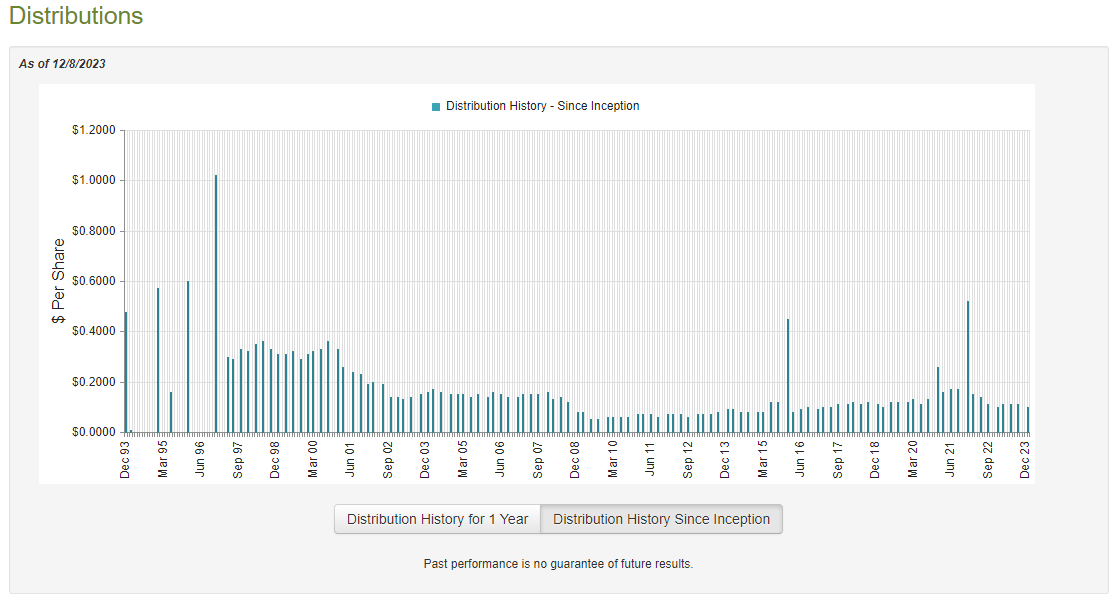

As the fund’s policy is to distribute roughly 2% of its net assets quarterly, we can expect that its distribution yield will probably be somewhere around 8%. This is indeed the case, as the fund’s most recent distribution was $0.10 per share, which gives it an 8.02% annualized yield at the current price. The fund’s distribution has naturally fluctuated quite a lot over time:

{kind=link}

This is exactly what we would expect considering the fund’s policy of distributing a percentage of its net asset value. During bull markets, the fund’s net asset value will obviously appreciate and cause that 2% to be a larger sum of money than it is during weak markets that reduce the fund’s net assets. This means that the fund is probably not a great investment for those investors who are seeking to earn a safe and secure income to use to pay their bills or finance their lifestyles, but it is reasonable for someone who wishes to use it as a common stock play that pays a distribution that can be reinvested into this fund or into something else.

As already mentioned, the fund’s distribution policy could prove to be destructive to its net asset value in weak markets and that is not something that is likely to be sustainable indefinitely. As such, we should still investigate the fund’s finances in order to determine how well it is actually doing.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is an interesting period of time because it covers the first half of this year. As everyone reading this can likely recall, growth stocks did fairly well during this period as the market widely assumed that the Federal Reserve would cut interest rates during the second half of 2023 and was bidding up stock prices accordingly. Growth stocks particularly benefited from this event as a bubble formed in artificial intelligence due to some investors believing that it would render large numbers of jobs effectively obsolete. While the market wisdom proved to be incorrect with respect to interest rates, it still could have provided the fund with the opportunity to realize some capital gains. This report will naturally give us a good idea of how well it managed to accomplish this.

During the six-month period, the Liberty All-Star Growth Fund received $12,716,612 in dividends and $33,624 in securities lending income from the assets in its portfolio. It surprisingly had no interest income during the period. As such, the fund reported a total investment income of $12,750,236 over the six-month period. The fund paid its expenses out of this amount, which left it with $5,139,076 available for shareholders. That was obviously nowhere close to enough to cover the distributions that the fund paid out, which totaled $80,040,153 over the period. At first glance, this might be concerning as the fund clearly did not have sufficient net investment income to cover its distributions.

However, there are other methods through which the fund can obtain the money that it needs to pay the shareholder distributions. For example, the fund might be able to realize capital gains that could be distributed. Realized capital gains are not considered to be part of net investment income, but they obviously represent money coming into the fund. Fortunately, the fund had a great deal of success at this task during the period. It reported net realized gains of $67,224,627 and had another $146,869,450 net unrealized capital gains over the first half of the year. Overall, the fund’s net assets increased by $172,210,073 after accounting for all inflows and outflows during the period. As might be expected considering that this fund is more growth than income-oriented, the fund had quite a bit of money come in via investors opting to reinvest their distributions into shares of the fund. The fund still managed to cover its distributions without this money, though.

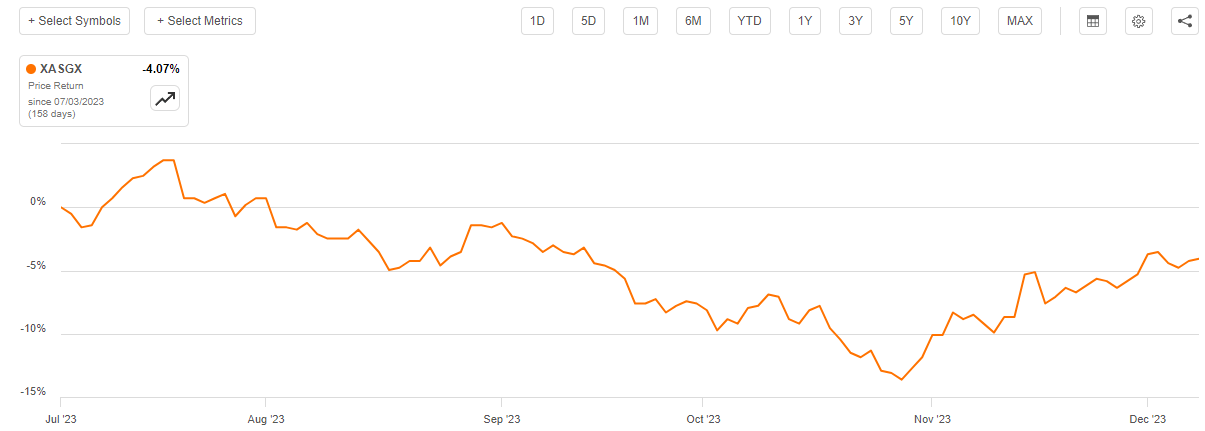

With that said, the fund did not have sufficient net realized gains and net investment income to fully cover the distributions. These two figures totaled $72,363,703 and that was not enough to completely cover all of the money that it paid out to the shareholders. As such, the fund was essentially relying on unrealized capital gains to partially fund the payout. As everyone reading this is well aware, unrealized capital gains can be erased very quickly in a market correction. It does appear that this happened to the Liberty All-Star Growth Fund during the second half of 2023.

As we can see here, the fund’s net asset value per share is down 4.07% since July 1, 2023:

{kind=link}

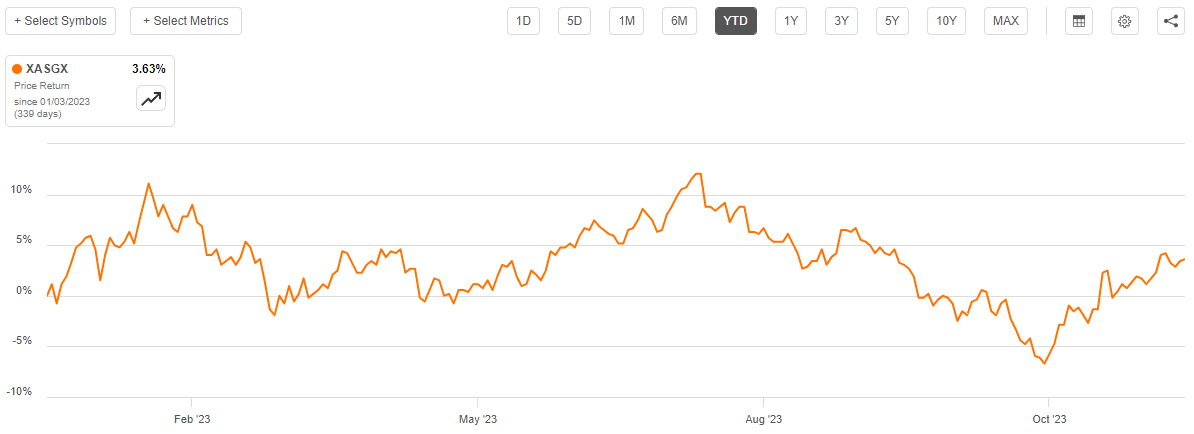

This strongly suggests that the fund has been paying out more than its total investment returns during the second half of this year. However, the fund’s net asset value per share is still up 3.63% year-to-date:

{kind=link}

Basically, the fund’s performance in the first half of this year was strong enough to cover all of the distributions that it has paid out so far this year as well as cover the losses that it has suffered during the second half of 2023. Thus, the fund is probably okay for the time being, but it is important to keep in mind that this fund’s distribution policy is destructive during extended periods of market weakness.

Valuation

As of December 8, 2023 (the most recent date for which data is currently available), the Liberty All-Star Growth Fund has a net asset value of $5.42 per share but the shares currently trade for $4.99 each. This gives the fund’s shares a 7.93% discount on net asset value at the current price. That is quite a bit better than the 6.17% discount that the shares have had on average over the past month. As such, the current entry point certainly appears to be reasonable if you wish to add this fund to your portfolio today.

Conclusion

In conclusion, the Liberty All-Star Growth Fund could be a great source of diversification for any portfolio that has a significant amount of money invested in common equities or other funds. This comes from its outsized allocation to both small-cap and mid-cap stocks, which tend to have only a minimal impact on today’s very top-heavy stock market. The fund’s yield is not particularly impressive for a closed-end fund right now, but it should be sustainable and varies based on market performance. Overall, this fund may not be great for someone who simply wishes to maximize their income but it could prove useful for someone who is still in the asset accumulation phase of their financial goals.

For further details see:

ASG: A Great Diversifier In Today's Top-Heavy Market