ASGI - ASGI: A Differentiated Approach Relative To Peers Creates Opportunity

2023-10-30 01:34:20 ET

Summary

- abrdn Global Infrastructure Income Fund has a unique positioning with overweighted industrial stocks, which has helped its performance relative to other infrastructure funds.

- The fund's lack of leverage is a positive in the current rising rate environment, and its deep discount presents a longer-term investment opportunity.

- ASGI has performed relatively well on a year-to-date basis, outperforming peers for what I believe is due to its differentiated positioning and lack of leverage.

Written by Nick Ackerman, co-produced by Stanford Chemist.

abrdn Global Infrastructure Income Fund ( ASGI ) is uniquely positioned where the fund has overweighted industrial stocks. This had deviated from the traditional infrastructure closed-end funds that often allocate their portfolios to utilities and energy infrastructure investments. That positioning has helped the fund this year relative to other infrastructure peers.

Not only did its differentiated positioning help, but the fact that the fund also isn't incorporating leverage at the fund level is another plus in this rising rate environment. The deep discount on an absolute basis relative to peers and even all CEFs can create a longer-term opportunity as well.

The Basics

- 1-Year Z-score: 0.06

- Discount: -14.79%

- Distribution Yield: 7.88%

- Expense Ratio: 1.75%

- Leverage: N/A

- Managed Assets: $544 million

- Structure: Term (anticipated liquidation date around July 28, 2035)

ASGI's investment objective is "to seek to provide a high level of total return with an emphasis on current income."

To achieve this objective, the investment strategy is quite simple. They will "invest in a portfolio of income-producing public and private infrastructure equity investments from around the world." Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

ASGI not employing leverage on the fund has been one of the main selling points of this fund, in my opinion. However, the discount relative to its older peers would indicate that the sentiment isn't shared more broadly. With no leverage, the fund could be considered relatively more conservative as it takes away an added layer of potentially making the fund more volatile. Additionally, with increasing interest rates, most funds are now paying over 6% for their borrowings, which is something ASGI investors don't have to consider at the fund level.

The fund's expense ratio was last reported at 1.75% ; however, due to the merger we discussed previously, that will be capped at 1.65% for the next year. The cap is positive, but in the end, this is still one of the highest expense ratios for a non-leveraged fund, which is an overall negative. One of the arguments for the justification of this higher expense ratio is that the fund also intends to invest in private investments, which takes a bit more work.

After becoming a larger fund earlier this year, the fund is set to become even larger again. Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund ( MFD ) is set to be merged with ASGI. This is expected to take place in February 2024. Of course, subject to the approval of MFD shareholders.

MFD is a much smaller fund than Macquarie Global Infrastructure Total Return Fund ( MGU ). MGU had nearly double the net assets that ASGI did, which made ASGI significantly larger on a relative basis. Still, even the ~$70 million in net assets that MFD would bring would make ASGI a larger fund. And a larger fund means potentially more liquidity for shareholders.

Relatively Strong Performance And Deep Discount Present Opportunity

Here is the YTD performance on a total share price and NAV return basis of ASGI relative to a few peers. Those peers include the more popular Cohen & Steers Infrastructure Fund ( UTF ) and Reaves Utility Income Fund ( UTG ). I've also included the MainStay CBRE Global Infrastructure Megatrends Fund ( MEGI ) - which I also believe has some appeal, and I looked at the last time when looking at ASGI as well.

MEGI is another infrastructure fund that strays from the more traditional asset allocation of what one would expect in the infrastructure CEF space. However, that differentiated approach has not yielded any benefits through this period of time as it was the worst performing on a total NAV return basis. Still, MEGI is an interesting fund. MEGI and ASGI are the newer infrastructure funds relative to UTF and UTG. MEGI is worth exploring further in another future update.

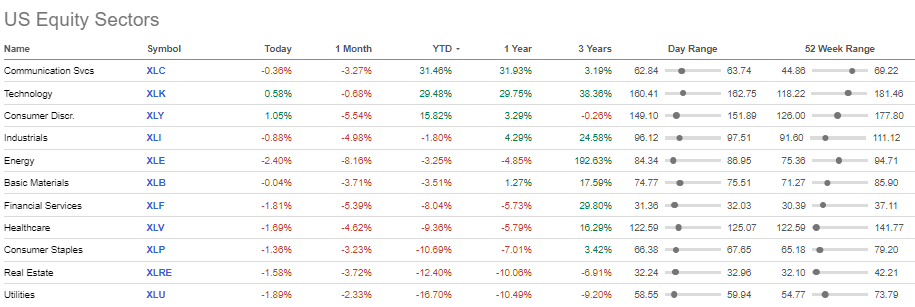

With that being said, the main fund we are discussing today is ASGI, and we can see that it has performed the best on a YTD basis. As utilities were slammed so far this year, being the worst performing sector by far, this is where the differentiated positioning and no leverage of the fund really shined through.

While industrials aren't necessarily blowing it away in terms of performance, coming in essentially flat on a YTD basis, they are still in the top half of sectors on a YTD basis. At this point, the utility sector is down almost 17% as higher interest rates have put significant pressure on that area of the market in more ways than one.

U.S. Sector Performance (Seeking Alpha)

{kind=link}

Another factor that investors could consider is the valuation of ASGI currently. The fund quickly went to a sharp discount, as most CEFs do after launching. While we aren't exactly at the new lows in terms of the fund discount, this still represents a time when the fund is trading at one of the deepest discounts since its launch a few years ago.

Ycharts

This could be something to continue to watch over the coming years, being a term fund. Though, in this case, the fund's anticipated liquidation date isn't until 2035, so we definitely have some time before that becomes a factor in applying any sway for the fund.

Appealing And Reasonable Distribution

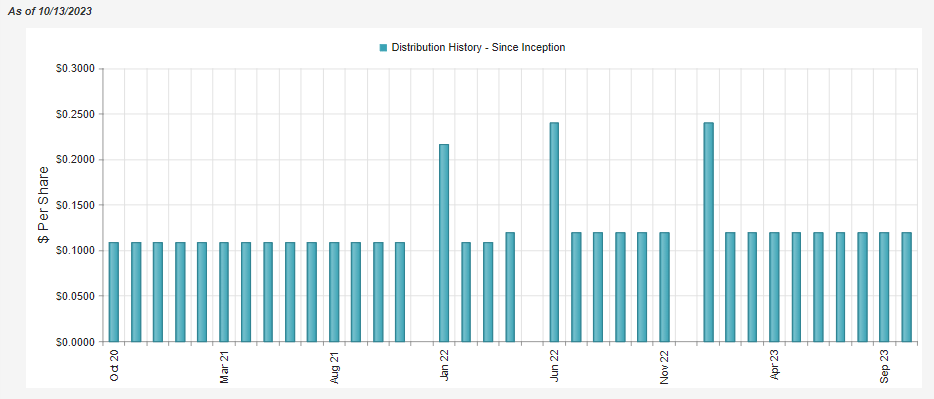

The fund launched with a $0.1083 monthly distribution and bumped it up to $0.12 in 2022.

ASGI Distribution History (CEFConnect)

{kind=link}

Besides buying assets at a deep discount with this fund, another characteristic of deeply discounted funds is the 'enhanced' distribution that investors receive. In this case, the fund's distribution yield comes to 9.30%, while the fund's NAV rate comes to a more modest 7.71%. At that NAV rate, I believe that's a reasonable payout level that they should be able to maintain for the foreseeable future.

At the very least, it is putting it in a much better position relative to its older peers UTF and UTG, where they are paying similar distribution rates currently but with shallow discounts means their portfolios have to generate just about the same return going forward for them to be covered. That leaves ASGI much more flexible with a low distribution rate.

On the other hand, all of these funds, being equity funds, will rely significantly on capital gains to fund their payouts. The underlying holdings they are invested in don't pay these 9%+ rates (or even 7.7%+ rates in the case of ASGI.) Therefore, they will require appreciation going forward at some point in order to justify paying these current rates. Either that, or the fund will erode away, and the NAV rates will just creep higher and higher until they are in a position where they need to cut the payouts.

ASGI's net investment income coverage comes in at just 6.25%. This is also a function of the fund's underlying holdings, but a higher operating expense ratio keeps NII lower.

ASGI Semi-Annual Report (abrdn)

{kind=link}

Here is a look at the distribution tax classifications that we discussed previously:

As is generally the case with equity funds, a large component of the distribution was classified as long-term capital gains. That's consistent with the earnings we saw above, but always a good reminder that it isn't always the case. Sometimes earnings and distribution classifications can differ wildly.

In 2022 this was reflected, but 2021 showed mostly ordinary income as the fund was getting started. Holding this fund in a taxable account could be appropriate as long-term capital gain distributions are tax-friendly compared to ordinary income.

ASGI Distribution Tax Classification (abrdn)

ASGI's Portfolio

On the subject of lower NII, some of the fund's positions don't pay any dividends at all. Several of the holdings outside the U.S. that also make up the largest holdings in the fund pay semi-annual dividends based on earnings. That's different from most U.S. corporations that often try to target quarterly dividends that grow over time.

ASGI Top Ten Holdings (abrdn)

The fund's top ten positions are mostly located outside the U.S. However, the fund still lists nearly 50% of the portfolio is invested in North American companies.

ASGI Geographic Exposure (abrdn)

The fund's weighting to industrials has frequently been the fund's largest sector allocation. In fact, from earlier this year , the fund has seen its industrial exposure increase, as well as the fund's utility weighting, has grown a touch, too.

ASGI Sector Allocation (abrdn)

The fund's largest holding, Aena S.M.E., S.A. ( OTCPK:ANYYY ), is an example of an industrial sector company that operates in the airport services industry. The company is headquartered in Spain and has operations in Spain, Brazil, the U.K., Mexico and Columbia. An example of a company that is an industrial stock but is oriented toward infrastructure as it provides a service for the public.

Ferrovial SE ( OTCPK:FRRVY ) is another position that shows up as a top ten position and is another Spanish company in the industrial sector. However, the industry here is labeled as "construction and engineering." The company defines several business lines that they are involved with: highways, airports, construction, energy infrastructure, mobility and "other business."

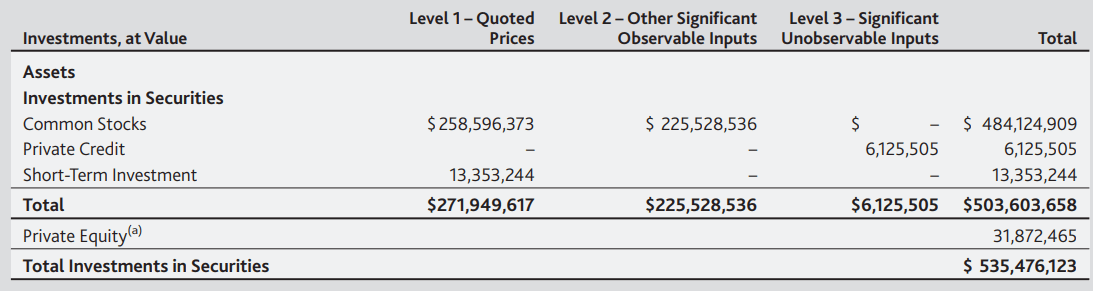

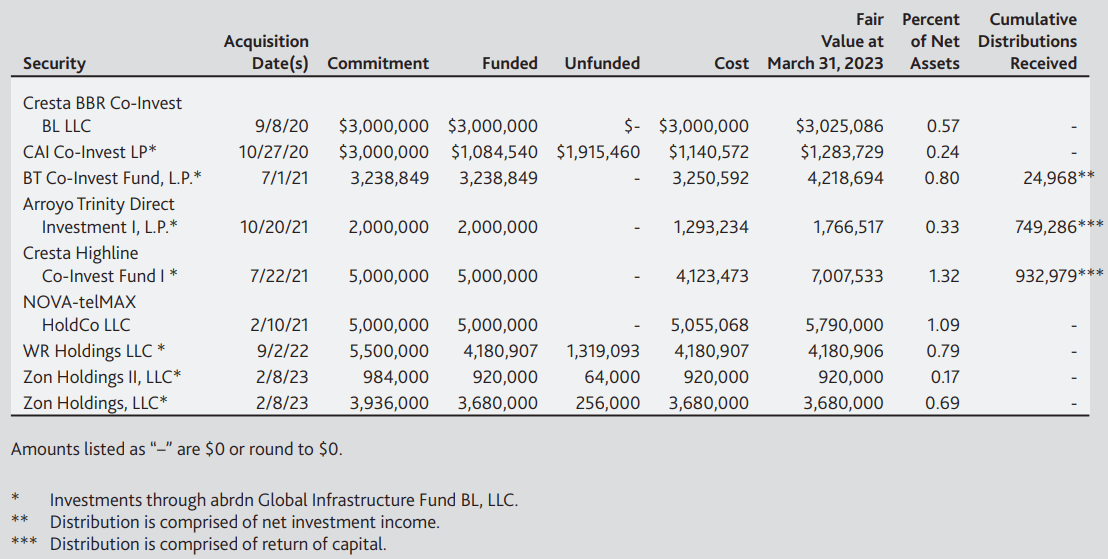

The fund's private holdings are one reason that some discount is likely warranted. Private investments add some uncertainty to the valuation. As of their last holdings list for the period ending June 30 , 2023 , private holdings were up to around 7.7%. That isn't necessarily the largest amount, and we had actually seen that not all of their private holdings are considered level 3 securities. Level 3 securities were only around 1.15% of the fund previously as of their last semi-annual report.

ASGI Level of Security (abrdn)

{kind=link}

Here are the private holdings listed with their costs and fair market value. Some of the holdings are newer investments that haven't seen their values change yet.

{kind=link}

Almost all of their private holdings are held through abrdn Global Infrastructure Fund BL, LLC. This vehicle is then owned by ASGI and is consolidated into the fund's operations.

However, this also highlights that months can go by without any changes at all to the valuations. The valuations aren't usually changed until a new round of funding goes through, and during conditions such as a tough market, some funding isn't done for a long while. These were the valuations as of their last semi-annual report.

Private investment exposure has ticked up since then, but it wouldn't have been enough to really make a meaningful difference from earlier this year. Therefore, I suspect the valuation of the portfolio is reasonably accurate for the most part, with the bulk of the portfolio in level 1 or 2 classifications outside of the 7.7% private holdings weight. Zon Holdings is the fund's third-largest position as of the last update, is an example of one of their private investment.

Conclusion

UTF and UTG are both solid funds, but they are certainly in a different situation at the moment compared to ASGI. While I wouldn't advocate for one over the other, I believe that ASGI is worth looking at for some infrastructure exposure. We already saw how the differentiated approach of the portfolio can result in different performance, which I believe helps justify holding a combination of the funds instead of having to choose one over another.

There are certainly short-term headwinds that could pressure this fund's underlying holdings going forward, such as a slowdown in the global economy. However, for long-term investors, I believe it still presents an attractive opportunity to invest in this fund while it is at a deep discount.

For further details see:

ASGI: A Differentiated Approach Relative To Peers Creates Opportunity