ASGI - ASGI And BUI: 2 Conservative Utility Plays For 2024

2023-12-23 23:56:58 ET

Summary

- Utilities remain attractive as long-term investments, and the headwind of higher rates is quickly turning into a tailwind for the sector that could continue through 2024.

- BlackRock Utilities, Infrastructure & Power Opportunities Trust and abrdn Global Infrastructure Income Fund are two conservative utility-oriented funds that do not employ leverage.

- Outside of each fund's material utility sleeve, they also carry some broader diversification through additional infrastructure exposure primarily related to the industrial sector.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Utilities have been struggling for over the last year due to the higher interest rate environment. However, we've already seen what can happen when risk-free rates start to ease up, which has seen a significant rebound from the October lows when Treasury rates were surging to highs not seen since prior to the Global Financial Crisis. That being said, utilities are still a conservative place to put capital to work and remain rather attractive. The higher rate headwind could turn into a continuing tailwind of momentum as we head through 2024, with rate cuts expected.

Many closed-end funds utilize leverage in the form of borrowings to help potentially enhance returns. This comes with greater volatility, and that means a higher risk of potential gains but also losses. Two conservative utility-oriented funds that don't employ borrowings are BlackRock Utilities, Infrastructure & Power Opportunities Trust ( BUI ) and abrdn Global Infrastructure Income Fund ( ASGI ).

While rates are expected to be cut next year and that could help drive these funds higher, their more conservative approach can still be appropriate for investors who still want to avoid leveraged funds. After all, rates are still higher, and they aren't anticipated to go back to zero. Some investors simply don't want to add additional leverage to their portfolio as underlying companies employ leverage through debt themselves.

With all that being said, I view BUI and ASGI as both strong candidates for next year to grow an investor's passive income. They also provide exposure to global investments, which look relatively cheaper than their U.S. counterparts. Additionally, both are trading at attractive discounts for each fund, making that a potential catalyst for additional upside potential if they can see those narrow.

abrdn Global Infrastructure Income Fund

- 1-Year Z-score: 0.43

- Discount: -15.82%

- Distribution Yield: 8.04%

- Expense Ratio: 1.65%

- Leverage: N/A

- Managed Assets: $508 million

- Structure: Term (anticipated liquidation date around July 28, 2035)

ASGI's investment objective is "to seek to provide a high level of total return with an emphasis on current income."

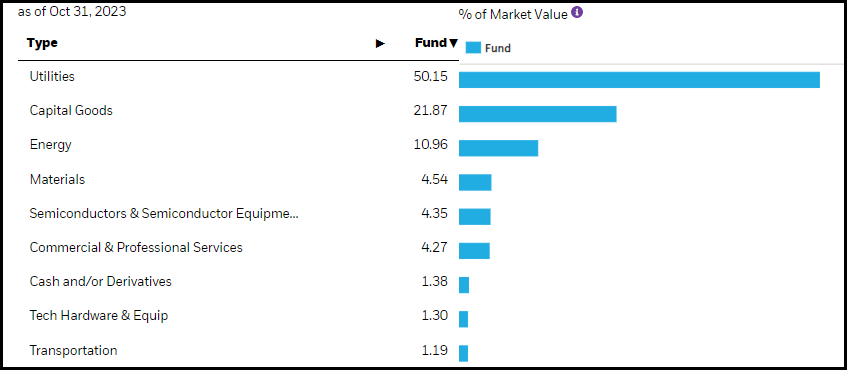

To achieve this objective, the investment strategy is quite simple. They will "invest in a portfolio of income-producing public and private infrastructure equity investments from around the world." Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

ASGI would be the more aggressive of the two because it doesn't utilize a covered call-writing strategy that BUI does. Covered calls can bring in premiums for the funds, and that means a stable source of distributable earnings for a fund, but in a rapidly rising market, it can actually cap out some of the performance when the underlying positions get called away. Therefore, with no options being part of their strategy, they are less constrained.

Where ASGI is also different from BUI and the overall infrastructure fund peers is that the fund also puts a heavy emphasis on industrial sector exposure. Utilities are the largest exposure, but the industrial sleeve isn't too far behind in its weighting. The fund is invested 54% in U.S. holdings with the second largest exposure to Europe and then Latin America and Asia.

ASGI Sector Allocation (abrdn)

The fund's expense ratio is higher compared to most unleveraged peers, and in fact, it would be even higher than the 1.65% - but from a merger earlier this year, they capped it at 1.65%. Speaking of mergers, the fund is set to absorb another fund early next year, which we touched on in our prior update .

After becoming a larger fund earlier this year, the fund is set to become even larger again. Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund ( MFD ) is set to be merged with ASGI. This is expected to take place in February 2024. Of course, subject to the approval of MFD shareholders.

MFD is a much smaller fund than Macquarie Global Infrastructure Total Return Fund ( MGU ). MGU had nearly double the net assets that ASGI did, which made ASGI significantly larger on a relative basis. Still, even the ~$70 million in net assets that MFD would bring would make ASGI a larger fund. And a larger fund means potentially more liquidity for shareholders.

Speaking of our prior update, that was some fortunate timing as we caught the almost absolute low of the fund when it was published. I've been bullish on ASGI for a while, so that certainly should be considered as well, but the prior update came at a great time.

ASGI Performance Since Prior Update (Seeking Alpha)

Since this time, though, the fund's discount has narrowed, but it continues to trade at a deep and attractive discount, nonetheless. Overall, the fund isn't that old, so a 'normal' range at this point can be more difficult to come up with.

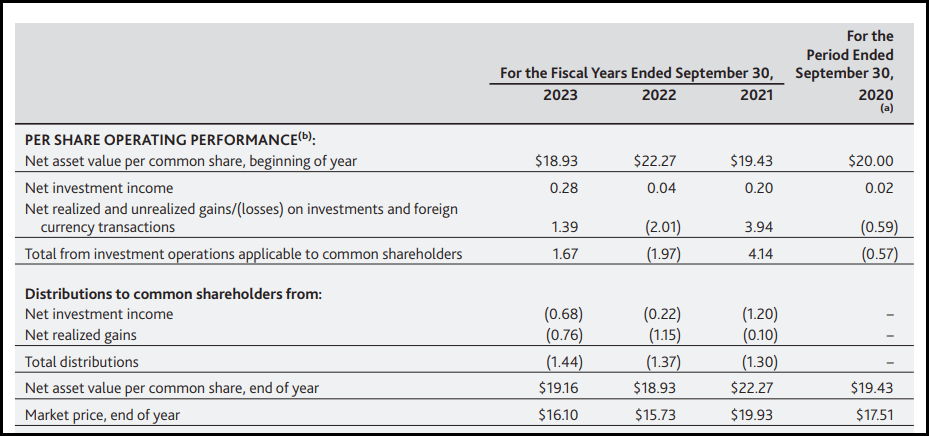

With the fund's latest annual report , there was a very encouraging uptick in the fund's net investment income. Previously, this fund earned a relatively shallow NII through 2022. Given the significantly larger size of the fund, that would have naturally helped NII on an overall basis, but this also translated into a per-share basis, which is more relevant given the transformation of the fund over the last year.

The more NII a fund can produce, the more stable its distribution could potentially be, as this should be a fairly regular source of cash flow for the fund's distribution.

{kind=link}

The fund has continued to maintain its $0.12 monthly distribution since it was raised in early 2022. However, they recently made an announcement that they are c hanging the distribution policy .

Starting with the January 2024 distribution, the fund's distribution will "be 9% of the average daily NAV for the previous month as of the month-end prior to declaration." This will see the distribution change annually going forward based on this new policy. This change has also resulted in an increase in the distribution to $0.15 for 2024. That's a sizeable increase and was because the fund's NAV distribution rate previously was closer to around a 7% rate.

Going forward, I think this was an overall good move. It means a fairly predictable distribution because if NAV is rising in the last month, we know it'll be increased. Alternatively, if the NAV is declining, then we know to expect a decrease. There are many funds out there that operate with a similar distribution policy. However, a 9% hurdle plus the expenses of operating the fund are likely to be unachievable every year. Therefore, I suspect the NAV will slowly decline over time, and that would also mean the distribution will slowly decline over time. At least until the fund's anticipated termination date, at which time the entire NAV would be liquidated and paid out to investors - barring the usual term fund caveats.

That doesn't mean that returns can't be respectable; it just wouldn't seem logical to expect a 10%+ return to be capable over every year. The S&P 500 Index itself can only just barely do that over the long term.

BlackRock Utilities, Infrastructure & Power Opportunities Trust

- 1-Year Z-score: -1.41

- Discount: -5.85%

- Distribution Yield: 7.05%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $492 million

- Structure: Perpetual

BUI's investment objective is to "provide total return through a combination of current income, current gains and long-term capital appreciation."

To achieve this objective, they have quite a bit of flexibility. They will invest "primarily in equity securities issued by companies that are engaged in the Utilities, Infrastructure, and Power Opportunities business segments anywhere in the world and by utilizing an option writing (selling) strategy in an effort to enhance current gains."

For their options selling strategy, one thing that can help is that they aren't writing over their entire portfolio. The latest overwritten percentage came in at 31.23%. That means that only a minority of their portfolio could see that capped upside that we touched on above. Additionally, they write against individual positions so they can generate option premiums from some positions that could potentially only be moving sideways. That results in being able to have some distribution coverage even if the market isn't doing anything.

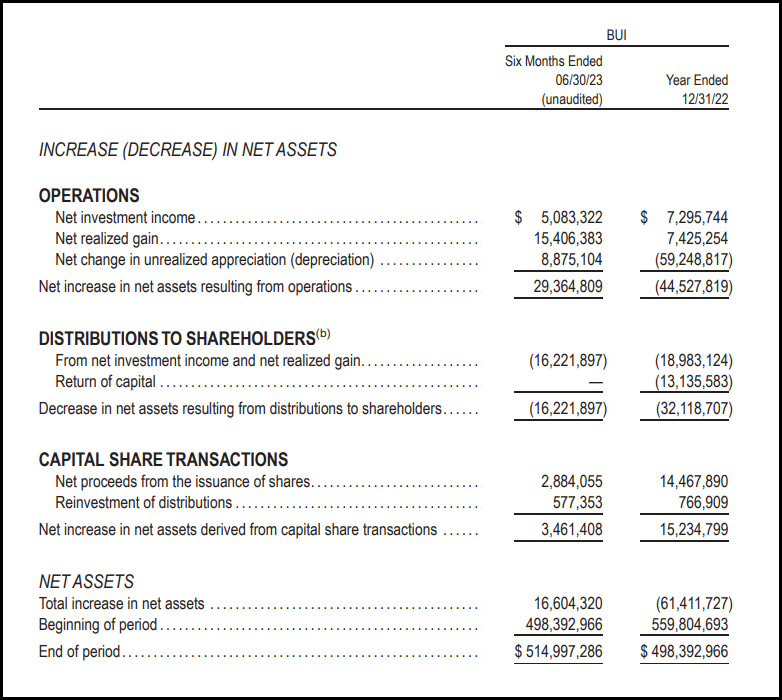

Based on the fund's last semi-annual report ending June 30, 2023, during that six-month period, the fund took in gains of $7.356 million from their options written. Against the shares outstanding at the time of that report, it would have worked out to nearly $0.33 per share in gains. That would be on top of the NII generated of $5.083 million in the six-month period or $0.23 NII per share. From these two sources alone, that would account for $0.56 in total earnings being generated against $0.726 in distributions to shareholders. The remainder was easily covered through realized gains in the first half.

{kind=link}

At an NAV distribution rate currently at 6.63%, we seem to be far away from any danger of distribution cuts as this isn't stretched at all. In fact, if it wasn't for the sell-off in utilities pressuring the space lower, we would be looking at a rather shallow distribution rate where we could be discussing potential increases to the payout.

In our previous update for BUI , I had rated it as a 'Hold' primarily due to a shallow discount.

BUI Performance Since Prior Update (Seeking Alpha)

During this time, the shares have turned lower, but some of this was from the discount widening, which helps to flip me back to a 'Buy' rating for this fund now. That would be combined with utilities that also overall sunk a bit lower in this period. However, the largest driving factor in weaker performance was the fund's discount opening up.

At one point, the fund had traded at a deep discount fairly regularly, and a 10%+ discount wasn't that rare since around 2016, that began to change. The consistency of the fund's distribution and the expectation that it looks set to continue, I believe, is what merits a better overall valuation now relative to then.

YCharts

Similar to ASGI, BUI isn't necessarily a pure utility play. This fund also has a fairly sizeable sleeve to "capital goods" (AKA industrials.) Additionally, BUI is similar to ASGI in that they have a 58% weight to U.S. companies, but then European exposure comes in as the second largest weight.

{kind=link}

Conclusion

I believe that the utility sector is attractive and looks set to rebound in 2024 from a relatively lackluster couple of years. As risk-free rates declined more recently, we already got just a taste of the potential rebound the space could do.

ASGI and BUI are two conservative ways to play that potential rebound, where they are overall attractive long-term considerations even without this potential catalyst. Additionally, they can add even more diversification by taking more of a broader infrastructure approach through investments outside of only utilities specifically. With both funds, they seem to place a strong emphasis on industrial names outside of their heavy utility sleeves.

These funds aren't leveraged in the form of borrowings, which, if one feels incredibly strongly about the direction of rates going more aggressively, could make sense in leveraged funds. Still, for investors who are risk-averse or want to take a more balanced approach to moderate their more aggressive sleeve of investments, these two could be great additions to grow one's passive income.

For further details see:

ASGI And BUI: 2 Conservative Utility Plays For 2024