MEGI - ASGI And MEGI: Deeply Discounted Infrastructure Funds

2023-08-10 14:56:25 ET

Summary

- The utility sector has been underperforming in 2023 due to the rising interest rate environment, but that doesn't mean they aren't attractive or can't perform well going forward.

- The abrdn Global Infrastructure Income Fund and MainStay CBRE Global Infrastructure Megatrends Term Fund are trading at deep discounts, making them potential opportunities.

- ASGI operates without leverage and may be a safer choice, while MEGI utilizes leverage; both funds pay reasonable distribution rates currently.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Infrastructure/utility companies often present attractive features for income investors as they can provide steady and reliable dividends to investors. That can make them work well in closed-end funds that provide a basket of exposure to this space. However, utilities have been hit with the rising interest rate environment and are one of the weaker performing sectors so far into 2023.

In fact, at the time of writing, utilities are now the worst-performing sector for the year, admittedly though the decline hasn't been too significant.

{kind=link}

Today, I wanted to give a look at two infrastructure CEFs that are trading at some deep discounts. That would be the abrdn Global Infrastructure Income Fund ( ASGI ) and MainStay CBRE Global Infrastructure Megatrends Term Fund ( MEGI ). They are the newest funds in the space, and they are trading near the widest discounts for the space.

| Utility/Infrastructure CEFs |

| Ticker |

| Notes |

| Yield |

| P/D |

| Z |

| Leverage |

| AUM / |

| UTG |

| Domestic, >95% equity |

| 8.44% |

| 0.75% |

| 0.5 |

| 21% |

| $2,003 |

| DNP |

| Domestic, 80-95% equity |

| 7.72% |

| 23.74% |

| 0.2 |

| 27% |

| $2,928 |

| GUT |

| Domestic, 80-95% equity |

| 8.64% |

| 117.59% |

| 2.1 |

| 23% |

| $236 |

| HTD |

| Domestic, hybrid |

| 8.20% |

| -4.17% |

| -0.6 |

| 36% |

| $747 |

| BUI |

| Mostly domestic (>50% US), >95% equity |

| 6.55% |

| -1.16% |

| 0.2 |

| 0% |

| $500 |

| DPG |

| Mostly domestic (>50% US), >95% equity |

| 8.50% |

| -10.51% |

| -2.0 |

| 29% |

| $422 |

| UTF |

| Mostly domestic (>50% US), 80-95% equity |

| 8.14% |

| 0.53% |

| 0.6 |

| 30% |

| $2,179 |

| GLU |

| Mostly domestic (>50% US), 80-95% equity |

| 8.20% |

| -4.50% |

| 0.9 |

| 40% |

| $92 |

| ASGI |

| Global (<50% US), >95% equity |

| 8.12% |

| -14.79% |

| 0.1 |

| 0% |

| $525 |

| MEGI |

| Global (<50% US), 80-95% equity |

| 9.53% |

| -12.80% |

| 1.8 |

| 30% |

| $814 |

| MFD |

| Global (<50% US), hybrid |

| 10.24% |

| -11.65% |

| -0.4 |

| 27% |

| $76 |

| ERH |

| Global (<50% US), hybrid |

| 8.17% |

| -6.16% |

| 0.3 |

| 23% |

| $101 |

| JRI |

| Global (<50% US), hybrid |

| 9.16% |

| -14.35% |

| -0.3 |

| 30% |

| $365 |

| PDT |

| Global (<50% US), hybrid |

| 9.18% |

| -6.70% |

| -2.0 |

| 39% |

| $573 |

| 8.49% |

| 3.99% |

| 0.1 |

| 25% |

| $826 |

Data as of August 9th, 2023, closing.

abrdn Global Infrastructure Income Fund

- 1-Year Z-score: 0.06

- Discount: -14.79%

- Distribution Yield: 7.88%

- Expense Ratio: 1.75%

- Leverage: N/A

- Managed Assets: $544 million

- Structure: Term (anticipated liquidation date around July 28th, 2035)

ASGI's investment objective is "to seek to provide a high level of total return with an emphasis on current income."

To achieve this objective, the investment strategy is quite simple. They will "invest in a portfolio of income-producing public and private infrastructure equity investments from around the world." Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

ASGI has been a particularly attractive fund in this rising rate environment due to not operating with leverage. Besides higher expenses for borrowing costs, that can also make it relatively less volatile.

As the fund acquired Macquarie Global Infrastructure Total Return Fund (MGU) earlier this year, the fund's expense ratio is supposed to go down for the following year with a limit of 1.65%. However, the 1.75% was what was provided in their last semi-annual report . This still makes it one of the more expensive CEFs, even as it doesn't include leverage costs. As an example, MEGI's expense ratio is 2.8%, but 1.33% of that is from leverage to bring the operating expenses to 1.47%.

The fund also doesn't utilize an options strategy to enhance its potential returns. Leverage and an options strategy are generally the go-to strategies for CEF management to employ. While we are in a higher interest rate environment, not employing leverage could be seen as beneficial due to rising borrowing costs that can be 6% or even higher now.

Going back to MEGI again, their borrowings are based on OBFR plus 0.75% . OBFR was last 5.06% , putting their borrowing costs at around 5.8%. However, we also just received another 25 basis point hike from the Fed. Leverage can still be a benefit if the fund can generate higher returns through appreciation, but at this level, the fund isn't likely to be investing in many securities that pay dividend yields above and beyond the costs of borrowings.

Just the same as any other equity-focused CEF, ASGI will require significant capital gains to fund its distribution. They don't employ any options or leverage strategies that can potentially help them achieve that goal. Instead, the fund has targeted private investments as its bit of a unique characteristic. As of March 31, 2023, private investments accounted for only 6.1% of the net assets. In terms of its distribution, the fund has one raise in its history.

{kind=link}

The NAV is higher now than the $20 it was at inception, indicating that the fund has not only covered its payout so far but it's also had a bit of appreciation. At a NAV distribution rate of 6.67%, I believe that ASGI is far from any danger zone of cutting.

Despite this positive performance, the fund is still relatively newer, and investors have pushed it to a large discount. As we noted above, it's one of the largest discounts in the whole CEF infrastructure space, with only MEGI at a large discount as of the latest closing.

MainStay CBRE Global Infrastructure Megatrends Fund

- 1-Year Z-score: 1.76

- Discount: -12.80%

- Distribution Yield: 9.17%

- Expense Ratio: 1.47%

- Leverage: 28.46%

- Managed Assets: $1.214 billion

- Structure: Term (anticipated liquidation date, December 15, 2033)

MEGI is your fairly standard closed-end fund , with the fund "seeking a high level of total return with an emphasis on current income."

To set this fund apart, the fund's twist compared to other infrastructure or utility funds is a "thematic theme." They are "focused on the investment megatrends of decarbonization, digital transformation, and asset modernization, which are reshaping the demand for infrastructure assets and driving income and growth potential."

MEGI is newer than ASGI, as it was launched in October 2021 compared to ASGI's launch in July 2020.

We already touched on a couple of items related to MEGI when discussing ASGI above. In particular, the leverage. While leverage costs are rising and add volatility, the idea is that it could also help enhance performance when things are going right. Unfortunately, due to its launch timing, it was hit with a volatile market almost immediately. They launched with a NAV of $20, and it is now down to $16.69.

That doesn't make it a bad long-term fund going forward, but it can be discouraging for investors when they see losses mount shortly after launch.

Newer CEFs often drop to discounts after launching anyway - despite their transition to being term structure funds. However, discounts in the CEF space have widened out across the board, which could have also contributed to the deep discount being present.

MainStay also isn't the biggest name in the CEF space, which might also turn investors off. That said, they actually have a traditional mutual fund, the MainStay CBRE Global Infrastructure Fund ( VCRAX ), that is older. It could also be seen as an alternative to MEGI if investors don't want to deal with leverage in this current environment. Both funds are managed by the exact same four managers from CBRE Investment Management.

Though it should be noted that it doesn't have the "megatrends" theme involved in it either. Despite that, there is still some overlap in their portfolios as the traditional and renewable infrastructure space lines now blur together. Utility companies have all been transitioning to include more renewable power generation, so any traditional utility or infrastructure can essentially be labeled as a "decarbonization" or "asset modernization" play.

MEGI launched with a monthly distribution of $0.1083, but they most recently increased this with a 15% increase to $0.125 per month. It's at a higher NAV distribution rate of 9.6% now compared to ASGI of 6.92%. The move seems unusual as the fund hasn't performed well since its launch, but it could be in an attempt to close the discount further. The discount has recently narrowed, so it appears it could be having some success. Additionally, as it was just raised, there is a fairly high unlikelihood that it would be cut for the foreseeable future.

Performance and Portfolio Comparison

When looking at the results of the funds since MEGI's launch, ASGI has been able to pull away despite not having leverage. In fact, it would appear that since MEGI has declined in this time period, leverage would have only had a further negative impact on the fund.

Ycharts

Including the rising rate environment, MEGI could also have a more difficult time providing positive returns in the future.

However, this wasn't all to the detriment that has been coming from leverage. Instead, portfolio positioning is likely playing a strong role here. ASGI has favored higher exposure to industrial stocks as opposed to going more of the utility route.

{kind=link}

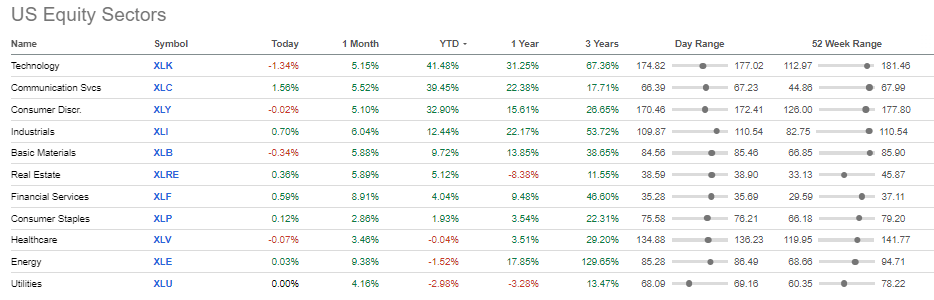

Industrials, unlike utilities, are not having negative performance in 2023 and are up based on the tracking ETF ( XLI ) by 12.5%.

Trying to compare ASGI and MEGI directly is a bit difficult as they don't list sectors in terms of their traditional categories. Instead, they use the megatrend theme terminology.

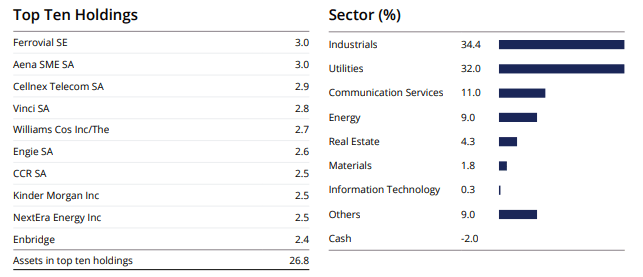

MEGI Megatrend Theme Exposure (MainStay)

In looking at the top holdings, we can get a bit better sense of their portfolio exposure. In the top ten, we see one overlapping position between the funds, Enbridge ( ENB ).

MEGI Top Ten Holdings (MainStay)

It can also be marked down that MEGI is more unusual as it doesn't include NextEra Energy ( NEE ) exposure in a top spot. They're included in the portfolio - as well as NextEra Energy Partners ( NEP ) - but just outside the top ten as positions #12 and #13. A bit ironic as NEE and NEP would probably fit well into the "megatrends" theme.

Conclusion

ASGI and MEGI are two deeply discounted closed-end funds in the infrastructure space. Despite sharing the infrastructure and global focus, the funds are operated quite differently, with different holdings and sector focus, and that can make both worth considering.

On the other hand, for investors looking to avoid leverage due to higher potential volatility and higher borrowing cost headwinds, ASGI is a clear choice. For those that believe leverage in the current environment can overcome the drawbacks of higher borrowing costs and volatility, then MEGI could be a clear choice.

For further details see:

ASGI And MEGI: Deeply Discounted Infrastructure Funds