MEGI - ASGI: Attractive Discount For This Unique Infrastructure Fund

Summary

- ASGI is a closed-end fund focused on global infrastructure investments, including private investments.

- MGU is set to be merged into ASGI, making it a significantly larger fund early in March.

- The fund's discount is attractive for this interesting infrastructure fund with significant exposure to both industrials and utilities.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 7th, 2023.

abrdn Global Infrastructure Income Fund ( ASGI ) has been providing investors with a steady distribution since its launch. The fund has also been providing investors an opportunity to get in at a large discount for this fairly unique fund. Newer closed-end funds often go to some wide discounts, but now ASGI has been around since 2020, so it could be considered starting to mature.

It is unique and interesting in terms of being an infrastructure fund because of its overweight exposure to industrial stocks - not what we'd traditionally always expect in an infrastructure closed-end fund. They also have some of their capital invested in private infrastructure positions, helping to offset them from the rest of their peers further. However, it still contains exposure to the typical infrastructure plays as well, including utilities, communication services and some energy and real estate.

Since our last update , the fund's performance has been relatively strong. That was after 2022 proved to be a relatively good year for utilities and industrials as compared to the broader market.

ASGI Performance Since Prior Update (Seeking Alpha)

Additionally, the merger with Macquarie Global Infrastructure Total Return Fund ( MGU ) has been approved and is official, with a date expected for closing. We also have a new annual report available for ASGI.

The Basics

- 1-Year Z-score: -0.40

- Discount: -14.30%

- Distribution Yield: 7.96%

- Expense Ratio: 1.79%

- Leverage: N/A

- Managed Assets: $187 million

- Structure: Term (anticipated liquidation date around July 28th, 2035)

ASGI's investment objective is "to seek to provide a high level of total return with an emphasis on current income."

To achieve this objective, the investment strategy is quite simple. They will "invest in a portfolio of income-producing public and private infrastructure equity investments from around the world." Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

ASGI is set to get much larger in early March as they absorb MGU. That's anticipated to be completed by the market open on March 13th, 2023 . We covered more of the in-depth details of that merger previously.

MGU isn't necessarily the largest fund, but with its roughly $350 million in net assets, it should combine with ASGI to be around $537 million in total managed assets. That should help with liquidity as daily trading volume should increase. At the moment, the daily trading volume for ASGI comes in at around 20k shares. That should benefit shareholders overall, as it will be easier to enter or exit a position in this name.

Another benefit of these sorts of combinations is the expectation for a reduction in expenses. It's always touted in the marketing material. They actually suggest that the expense ratio should go from the current level to around 1.56%. They actually put in a contractual agreement to "limit the total ordinary operating expenses of the combined fund following the consumption of the reorganization from exceeding 1.65%." So while these sorts of mergers often see negligible expense reductions, at least there should be something with this one.

ASGI isn't leveraged, but MGU is leveraged. It is anticipated that MGU will deleverage prior to the closing date. I believe that is a positive for the fund, as having the option of a non-leveraged infrastructure fund such as ASGI benefits investors.

Performance - Attractive Discount

Since the fund's launch, it started trading almost immediately at a large discount. This tends to be the case with new CEFs. However, despite being a new fund, they did participate in some of the historical CEF discount narrowing we saw in 2021.

That quickly widened back out with the volatility we experienced in 2022. That also tends to be a fairly common trend with CEF discounts. As soon as volatility picks up, the discounts start widening out to create opportunities. An opportunity is precisely what I see with ASGI, as its trading near the bottom of its discount range.

Ycharts

Although it's a short discount range, I believe the fund can start to gain interest from investors who don't pick up CEFs in the first year or two. As a term fund, the discount can be realized eventually. That being said, we have quite a few years before that becomes a meaningful part of the discussion.

Since its launch, its performance has been similar to other infrastructure funds. The most popular infrastructure CEFs tend to be Reaves Utility Income Fund ( UTG ) and Cohen & Steers Infrastructure Fund ( UTF ). I've also included BlackRock Utility, Infrastructure & Power Opportunities ( BUI ) for comparison. UTG and UTF are leveraged, and BUI, similar to ASGI, is not leveraged.

Ycharts

While this chart can give us some performance context since the fund's launch, I think it shouldn't be given too much weight beyond a general comparison.

For one, it's only past performance. Perhaps more importantly, these are fairly different funds. Despite the tendency to want to compare all infrastructure together, CEFs get rather niche in their categories. That can make it difficult to find actual proper comparisons between funds.

On top of that, ASGI's discount puts it at a much better valuation than any of the other infrastructure peers except for MainStay CBRE Global Infrastructure Megatrends Fund ( MEGI ), which is another new CEF name that came to market in 2021.

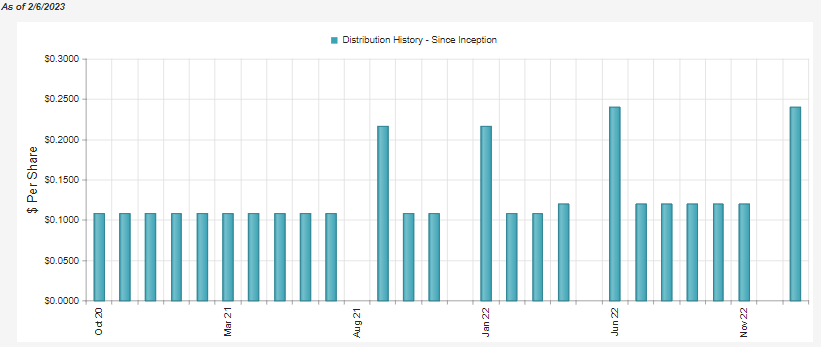

Distribution - Steady

This fund currently offers investors a distribution yield of 7.96%, with a NAV rate of 6.82%. Since the fund's launch, they've had quite a bit of success, and the initial distribution was bumped from $0.1083 to $0.12 early in 2022.

{kind=link}

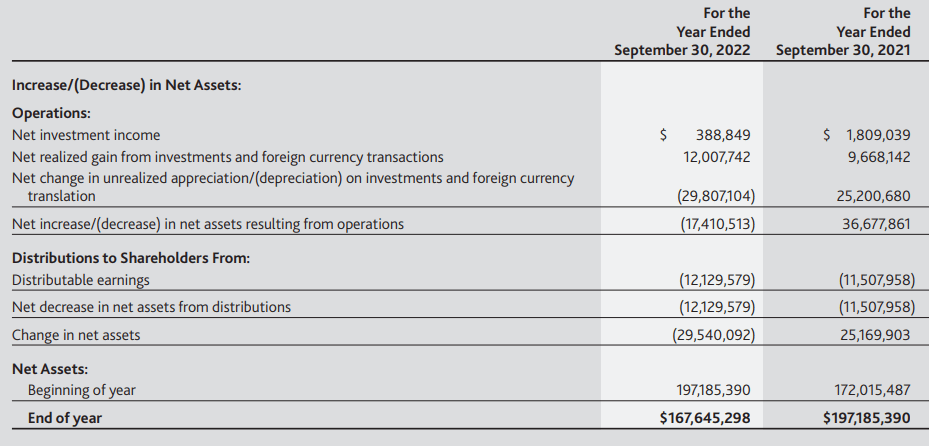

However, the fund isn't leveraged, and they rely significantly on capital gains to fund their distribution. They invest in quite a few dividend-paying companies. Still, the fund's high expense ratio reduces most of the total investment income that would be left over for shareholders in the form of net investment income. In fact, the NII in the latest fiscal year was better than the loss they showed in their semi-annual report. At around NII coverage of 3.2%, it certainly isn't anything to brag about.

2020 was a down year for the fund, but that didn't mean they didn't have capital gains embedded in the portfolio to rely on from the previous year. With that being the case, they were able to realize capital gains to fund their distribution shortfall.

{kind=link}

On the other hand, we see that unrealized gains were material for the fund. It was a better relative year for the fund but not a great one. Those declines still meant the fund saw a reduction in net assets. Going forward, that could be a potential problem if it happens for several years. At a distribution rate on NAV of under 7%, I think we are far from the danger zone.

This also doesn't factor in when the fund becomes much larger. That will change the fund's figures materially. Looking at MGU's latest coverage isn't even too helpful because they are anticipated to reduce their leverage. Once the combination of these two funds is in place, this will be something to watch closely in the upcoming reports.

As is generally the case with equity funds, a large component of the distribution was classified as long-term capital gains. That's consistent with the earnings we saw above, but always a good reminder that it isn't always the case. Sometimes earnings and distribution classifications can differ wildly.

In 2022 this was reflected, but 2021 showed mostly ordinary income as the fund was getting started. Holding this fund in a taxable account could be appropriate as long-term capital gain distributions are tax-friendly compared to ordinary income.

{kind=link}

ASGI's Portfolio

This is another way that MGU will significantly impact ASGI in the future. While they anticipate liquidating enough for the borrowings to be paid off prior to the merger, the fund will look quite different on the merger date.

They also expect to sell approximately 43% of MGU's assets following the closing. That still leaves a healthy amount of AUM left over to be invested in infrastructure that they believe is still worth holding on to. Some of this overlaps with what they already hold and is consistent with the fund's investment policy and objectives.

With this transition, they look to include more private opportunities as they have been, which they expect could take 12 to 24 months to accomplish.

With all that being said, watching for new fact sheets and other material in the future will be imperative to see how this fund transitions. ASGI will sometimes provide fund update calls, which talk about their funds and the outlook of what they're invested in.

At this time, the fund still is overweight industrial exposure, but it has come down some since. They are now almost nearly equal in position sizing with utilities in the fund.

ASGI Top Sector Weighting (abrdn)

This is where MGU being absorbed could shift the weightings more heavily into utilities . That isn't necessarily a bad thing, but it is a shift that is worth noting.

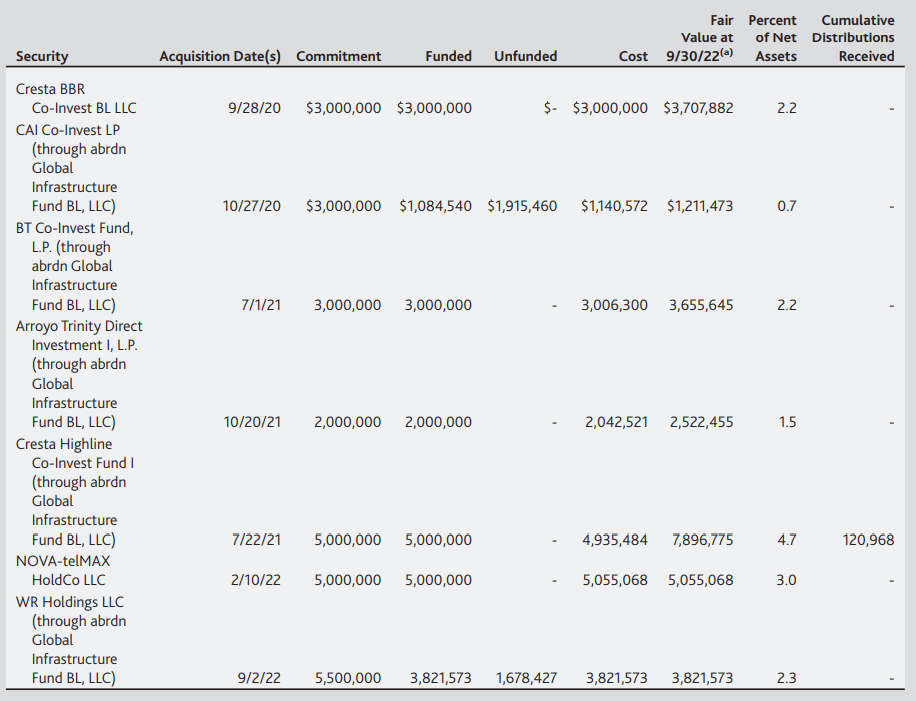

As touched on, ASGI will also include private exposure. We often rely more on management to make the right call in these types of positions. They have limited or no public information available, which can make them pretty opaque.

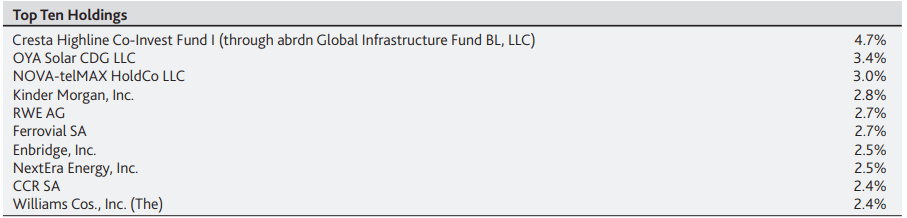

These represent some of their top positions. The private investments make up around 20% of their invested assets at the end of fiscal 2022. We can also see that the top ten holdings represent a fairly large weighting of the overall fund.

ASGI Top Ten Holdings (abrdn)

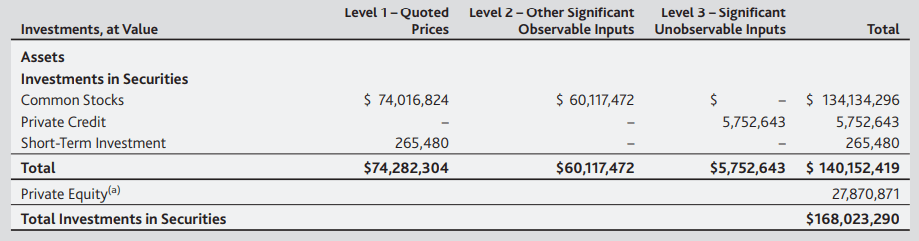

The level three securities will be level 2 or level 3 investments. These can be harder to value, particularly the level 3 investments, and that's why we tend to see discounts open up on these types of funds. Whenever there is some uncertainty, it often results in shareholders being skeptical.

However, for ASGI, the level 3 securities aren't an overly large portion of the fund - despite the fund's net assets being around 20% in private investments. The private equity they list as being incorporated in level 2 securities. That should mean investors can be a bit more comfortable.

{kind=link}

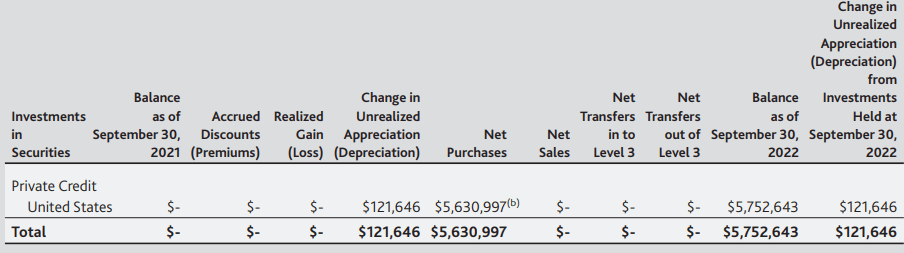

Their level 3 security is represented by only one position: OYA Solar CDG LLC. It's also encouraging that the valuation of this position has changed. We've seen other CEFs list their level 3 private holdings without any change despite holding them over the last year or two in a volatile market.

{kind=link}

Though a level 2 security doesn't mean it isn't restricted. Here's a list of restricted private investments.

{kind=link}

Interestingly, they list their private holdings simply as "private infrastructure holding" in the fact sheet. However, they then share this in the annual report when referencing the top ten. The Cresta Highline Co-Invest Fund is their largest holding. OYA Solar investment would then be the fund's second-largest holding.

I suspect that these continue to be the first and second largest holdings. However, NOVA-telMAX HoldCo LLC would have slipped with the latest fact sheet to the number 5 spot. At the time of their annual report, it was the third largest position.

{kind=link}

Conclusion

ASGI is an interesting infrastructure fund that's trading at a deep discount. With private investments, we tend to see a larger discount than usual. That certainly appears to be the case with ASGI, but most of their private investments are in the level 2 security camp. That should make them relatively more certain of the valuation based on "other significant observable inputs." At the same time, we still rely on the management to make the right calls in these investments with limited information. On top of this, ASGI is set to change drastically as it absorbs MGU. I believe that watching positioning will be something to keep a close watch on after the March closing date.

For further details see:

ASGI: Attractive Discount For This Unique Infrastructure Fund