ASGI - ASGI: More Headwinds Ahead

2023-10-10 04:04:43 ET

Summary

- abrdn Global Infrastructure Income Fund is a closed-end fund that focuses on global utilities and infrastructure equity investments.

- The fund has a high correlation to the utilities sector and is sensitive to interest rates.

- ASGI has a discount to NAV of -16% and a managed distribution plan, but a significant portion of its distribution comes from long-term gains.

- As rates stay higher for longer, we are going to witness a P/E de-rating of the utilities sector.

- The fund runs jurisdictional risk, as observed in the -30% price plunge for the Grupo Aeroportuario del Centro Norte holding.

Thesis

The abrdn Global Infrastructure Income Fund ( ASGI ) is a closed end fund. The vehicle seeks to provide a high level of total return with an emphasis on current income, via a portfolio of global infrastructure equity investments.

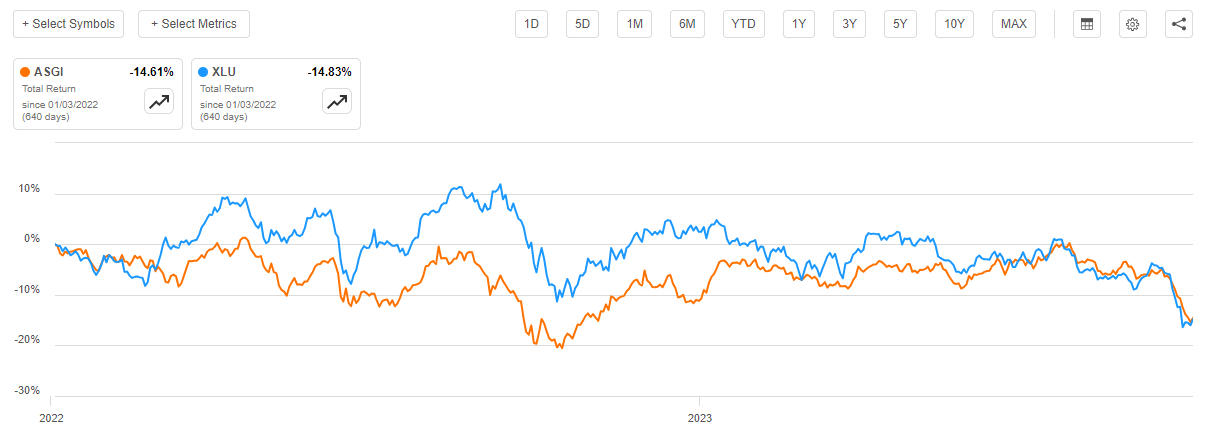

The CEF has two main sleeves - utilities and infrastructure investments (such as airports). What is nice about this fund is its global mandate, having only a 48% allocation to North American names. The vehicle however has a very high correlation to the utilities sector:

{kind=link}

Since January 2022, when the higher interest rate environment started, the fund's price moves have been very well correlated to the Utilities Select Sector SPDR Fund ETF ( XLU ).

ASGI's main risk factor is represented by interest rates, followed by jurisdictional risk as exposed by the recent price plunge in Mexican airport operators as a result of tariff changes . The article further discusses the relevant names and implications in the 'Holdings' section.

ASGI has a high discount to NAV of -16%, which opened up given the fund is fairly recent (2020 IPO) and the current high interest rate environment. We do not expect things to change here until the Fed starts lowering rates and the fund is able to post a more consistent and observable track record, especially in light of its merger with MGU.

A retail investor should focus more on the collateral risk factors in this instance rather than the fund discount. The underlying assets in the portfolio will be mainly driven by the risk factors pertaining to utilities, a sector which we are of the opinion that will de-rate during a cycle of 'higher for longer' interest rates.

Analytics

AUM: $0.38 billion

Sharpe Ratio: 0.31 (3Y)

Std. Deviation: 16.2 (3Y)

Yield: 9.3%

Leverage Ratio: 0%

Discount to NAV: -16.5%

Z-stat: -1.5

Composition: Global Utilities & Infrastructure Projects

Holdings

The fund contains a mix of utilities and infrastructure assets:

Sectors (Fund Fact Sheet)

The fund has an 'Industrials' sleeve which is in fact infrastructure assets. Let us have a closer look at some of the individual names in this vehicle:

Top Holdings (Fund Fact Sheet)

The top-10 names here make up over 25% of the fund, and we would not consider this CEF granular. NextEra Energy ( NEE ) for example, which accounts for 2.5% of the fund, is a large North American utility that has recently plummeted in price on the back of lower guidance:

Engie ( ENGIY ) is a European utility behemoth, with a large 10% dividend yield:

ENGIE SA engages in the power, natural gas, and energy services businesses. It operates through Renewables, Networks, Energy Solutions, Thermal, Supply, Nuclear, and Others segments. The Networks segment comprises the electricity and gas infrastructure activities and projects, including the management and development of gas and electricity transportation networks and natural gas distribution networks in and outside of Europe, natural gas underground storage in Europe, and regasification infrastructure in France and Chile.

The company's stock price has gone nowhere in the past year, but the utility passes investors a very large dividend yield. The company is very much akin a bond.

Many of the underlying holdings in this fund are very interest rate sensitive. Let us have a closer look at the 'Real Estate' sector:

{kind=link}

The fund contains 2 REITs, namely American Tower Corp ( AMT ) and Crown Castle ( CCI ). Both these names are fundamentally solid, but given that REIT structures act like pass-through entities, they have a high sensitivity to interest rates:

They both have been pummeled in the past year given the rise in rates, with AMT being down -18%, while CCI is down -32%.

Another interesting item to note when drilling in the collateral tape is the regional risk taken by the fund. The vehicle has a fairly sizable position in the Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. ( OMAB ):

{kind=link}

OMAB recently saw its price plummet by over -20% on the back of tariff changes:

Shares of Mexican airport operators plummeted on Thursday, after the country's civil aviation regulator announced changes to tariff regulations. Grupo Aeroportuario del Sureste (NYSE: ASR ), or Asur, was down 19.1% in afternoon trade, Grupo Aeroportuario del Pacífico (NYSE: PAC ) was lower by 23% and Grupo Aeroportuario del Centro Norte retreated 30.1%.

Investments in infrastructure assets outside of highly regulated markets like the U.S. or E.U come with significant political and regulatory risks. Political parties can dictate tariff changes rather than economic reality. ASGI has roughly 20% of its portfolio in EM jurisdictions:

Geographic Composition (Fund Fact Sheet)

Having investments in EM does not mean they cannot be profitable. It just means they are more volatile, and the risk/reward ratio is different.

Distribution

The fund has a managed distribution plan, which consists of a fixed monthly payment of $0.12/share. The plan was re-approved in 2023, but can be changed by the fund's Board of Trustees at any point in time.

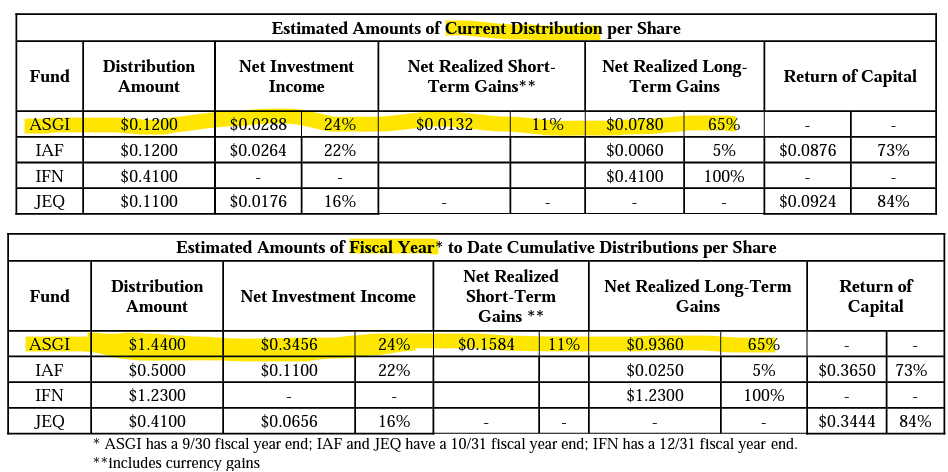

The CEF has a fully covered distribution as of its latest Section 19a, both on a payment date basis as well as a fiscal year basis:

{kind=link}

We can see from the above table that for the fiscal year ending 9/30, the fund's distribution came 24% from its net investment income, 11% from short term gains and 65% from long term gains. The story is good, but keep in mind that a large percentage of the distribution comes from long term realized gains. If the underlying equities do not perform going forward we will see the fund starting to use return of capital here.

The current distribution parsing is consistent with what we see in respect to long term NAV performance, which has been stable:

The fund's NAV in the past decade has oscillated around the $20/share mark, which is a positive feature for long term holders.

Discount to NAV

The CEF has been trading at a high discount to NAV since the advent of a higher rates regime:

We can see the fund moving in a tight -10% to -15% range in terms of discount to NAV in the past two years. Expect these levels to persist in a high interest rate environment and for a period of time after the MGU merger .

Conclusion

ASGI is a closed end fund that makes investments in global utilities and infrastructure equity names. The vehicle has a 9.3% yield which is fully supported currently, but 65% of its composition is capital gains. That means that a flat or negative performance in the underlying equities will result in the fund using ROC.

The CEF has a massive -16% discount that has opened up due to the high interest rate environment, the fund's merger with MGU and the fairly new nature of the CEF (the fund IPO-ed in 2020). Expect the discount to persist until the Fed starts cutting rates and the vehicle establishes more of a track record.

Since the start of 2022, ASGI's price performance has been very well correlated to the utilities sector (XLU as a ticker). Expect that correlation to continue, with the main risk factor for the CEF being rates, and the P/E de-rating of the utilities sector. We have already seen this move begin with NextEra, which is down -39% this year and a top holding in ASGI. We expect the current 'higher for longer' rates environment to be a significant headwind for many of the bond-like investments in ASGI, with more weakness ahead for the name. We are of the opinion that retail investors would do well to lighten up on this name now and revisit the fund once the Fed starts cutting rates.

For further details see:

ASGI: More Headwinds Ahead