ASGI - ASGI: Non-Leveraged Infrastructure Fund At A Deep Discount

2023-06-16 12:03:32 ET

Summary

- ASGI, a non-leveraged infrastructure CEF, benefits from a heavy weighting towards industrials.

- The fund's large discount and attractive distribution yield of 8.44% make it an appealing option for income investors.

- Despite declines in utilities and energy sectors, ASGI has provided positive returns and outperformed other popular leveraged funds.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 2nd, 2023.

One of the main benefits of abrdn Global Infrastructure Income Fund (ASGI), besides its attractive discount, is that the fund doesn't employ any leverage. This can be beneficial when interest rates are rising, and volatility in the market is higher. ASGI isn't exposed to higher interest rates on any borrowings, and it can limit the volatility of the fund by not having the added risk of leverage.

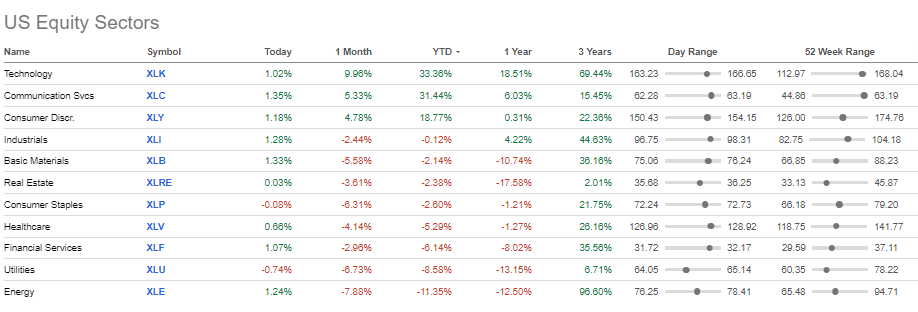

Utilities and energy, which are included in most infrastructure funds, haven't necessarily been having the best year. So the fact that this fund hasn't employed leverage has seemingly been to its benefit compared to some of its leveraged peers.

These declines in utilities and energy are despite what the S&P 500 Index would be projecting. The broader market is being propped up by a select handful of mega-cap growth/tech names that have really kind of masked that everything else is flat or even quite negative through 2023. The energy sector has been the worst, and utilities are right behind it to the downside.

U.S. Equity Sector Performance (Seeking Alpha (performance as of June 1st, 2023.))

{kind=link}

Fortunately, ASGI has still been able to provide positive returns. The fund is invested globally and has a significant allocation to industrial stocks that's actually at a higher allocation than utilities.

The Basics

- 1-Year Z-score: -1.45

- Discount: -16.62%

- Distribution Yield: 8.44%

- Expense Ratio: 1.75%

- Leverage: N/A

- Managed Assets: $540.4 million

- Structure: Term (anticipated liquidation date around July 28th, 2035)

ASGI's investment objective is "to seek to provide a high level of total return with an emphasis on current income."

To achieve this objective, the investment strategy is quite simple. They will "invest in a portfolio of income-producing public and private infrastructure equity investments from around the world." Interestingly, the most significant exposure in ASGI is to industrial stocks, making this fund a bit unique in the infrastructure space. However, utilities are right up there in terms of exposure.

The fund's expense ratio comes to 1.75%, which is high and is something I note in every update. However, that was for the six months ended March 31st, 2023 . The fund has since merged with Macquarie Global Infrastructure Total Return Fund (MGU) on March 10th, 2023. At that time, there was an expense ratio limit put into place of 1.65%. That's still high, and it's only for the following year, but any decline is welcomed.

abrdn Inc., the investment adviser of the Fund, has contractually agreed to limit the total ordinary operating expenses of the Combined Fund following the consummation of the Reorganization (excluding leverage costs, interest, taxes, brokerage commissions, acquired fund fees and expenses and any non-routine expenses) from exceeding 1.65% of the average daily net assets of the Combined Fund on an annualized basis for twelve months following the closing of the Reorganization.

This merger also made it a significantly larger fund that provides more liquidity when buying and selling shares through a higher daily trading volume. The fund had previously been under $200 million in net assets. The average trading volume in our previous update was around 20k per day. According to Yahoo Finance, this has now climbed to an average of over 49k.

Performance - Beating 'Peers' And Attractively Discounted

On a YTD basis, ASGI has been one of the better performers on a total NAV return basis. It has only been eclipsed by BlackRock Utility Infrastructure & Power Opportunities Trust ( BUI ) on a total share price basis. However, BUI is also a non-leveraged fund, so it has seemingly benefited by not being dragged down by poor results in the utility and energy sectors. ASGI and BUI have both outperformed the other popular leveraged funds, Cohen & Steers Infrastructure Fund ( UTF ) and Reaves Utility Income Fund ( UTG ).

Ycharts

However, I would note that using these as 'peers' probably isn't appropriate. Not only are the underlying strategies different of non-leveraged vs. leveraged, but the fund's allocations are fairly different too. ASGI has been benefiting from a material tilt towards industrials and a smaller allocation to utilities compared to these funds. Each is appropriate and worth holding for different reasons, in my opinion. What this does is give us some context of why its differences can make it attractive.

Since the fund's inception in mid-2020, it has been a strong performer, too. So this isn't necessarily just a YTD thing, but it has been a big driver of where we are today. During 2021 and early 2022, we can see that UTF was a really strong outperformer in this basket of infrastructure funds. Since ASGI's inception, BUI has been able to outperform as well.

Ycharts

As is the case when most new CEFs launch, they go to some deep discounts. ASGI is no exception, and we remain at an attractively discounted price in a period that seems to be favoring ASGI's strategy. Excluding the massive drop shortly after launch, we are near the widest discount level.

Ycharts

Distribution - Deep Discount Leads To Attractive Rate

Besides buying assets at a sale price, there is another big benefit of a fund trading at a discount. That comes in the form of the distribution yield of the fund coming in at 8.44%. That's what investors would collect going forward should they maintain the current monthly distribution rate. However, the actual NAV distribution rate is only 7.04%. That's the amount the underlying portfolio has to generate to sustain the current rate.

For an extreme example of where this works against investors, we can check out Gabelli Utility Trust (GUT). That fund trades at over a 110% premium. Investors collect an 8.88% distribution rate, while the underlying portfolio has to generate an unsustainable 18.69% rate.

To generate a higher distribution rate for ASGI compared to its underlying holdings' dividend yields, they will rely on capital gains to fund it. For an equity CEF and even an infrastructure fund, this isn't anything new at all.

The latest semi-annual report showed us a net investment income per share of $0.05. This is likely to change as we move forward due to the MGU merger, but we did see a small uptick compared to the prior year, where it was $0.04 for the full fiscal year. So we've seen a shift to producing more NII, which can be more predictable than capital gains.

{kind=link}

Still, they pay $1.44 annually currently, so even an annualized $0.10 would provide for NII coverage of only 7%. Working against NII is the fund's higher expense ratio and holdings that pay relatively lower dividend yields compared to some of those peers we touched on above. The lower expense ratio for the next twelve months should give us some better coverage, but we could see it sink again in the following year.

Overall, they've been successful in finding capital gains to fund the distribution, but this is something that will be required going forward on a regular basis. If we get back-to-back weak years of gains, I would fully expect a distribution cut. However, that doesn't appear to be a problem at this time.

ASGI's Portfolio

With the merger of MGU into ASGI, we saw turnover for the fund in their latest portfolio explode to 107%. That was up from 25% and 28% in fiscal 2022 and 2021, respectively. While there was some significant overlap from the funds, this was something I was looking at to see how the portfolio may shift. MGU was nearly double the size in terms of net assets compared to ASGI. MGU deleveraged prior to the merger. Otherwise, it would have had an even larger impact.

For the most part, we see that sector allocations did not materially change. The fund had previously listed 28.9% in industrials, 27.6% in utilities and 10.2% allocated to communication services, with 7.8% in the energy sector. This is now the sector weightings as of the end of March 31, 2023 . The sector weightings shifted slightly, but the allocations are all pretty much in line with where they were previously.

ASGI Sector Weighting (abrdn)

Similarly, the geographic allocations for the fund haven't moved too substantially, either. The fund generally runs around 40% of its portfolio in U.S. names. France did see its weighting increase a touch to grow a touch larger than the exposure to Spain. However, for the most part, this doesn't appear to be a material change.

ASGI Geographic Allocation (abrdn)

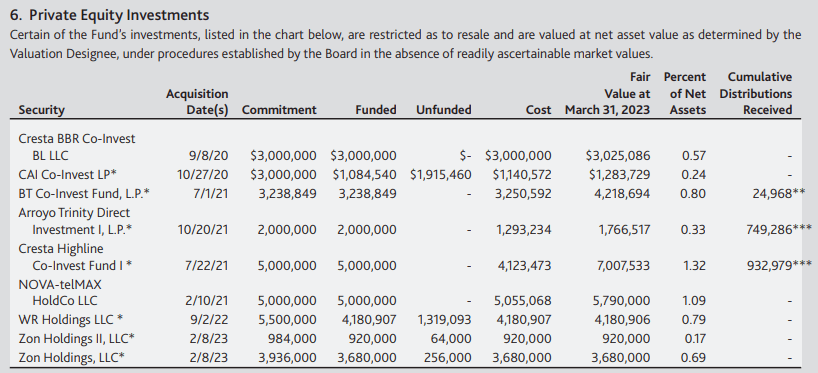

For the fund's top ten holdings, we actually have changes to discuss. The fund previously had its largest holdings allocated to "private infrastructure holding." That was the largest, second largest and fifth largest holding in our prior update.

ASGI Top Ten Holdings (abrdn)

These are still holdings for the fund, but due to a sizeable shift in the fund's total assets with acquiring MGU, the weightings just aren't as large anymore. Since the end of September 30, 2022, we've seen the weightings as a percent of net assets drop quite materially to reflect this.

For example, the Cresta BBR not only saw its fair value drop from $3.708 million to now $3.025 million but due to the increase in assets, the percentage of net assets went from 2.2% to 0.57%. Cresta Highline saw its fair market value also decline from $7.897 million to now $7.008 million. The percentage of net assets value was 4.7% but has now come down to 1.32%. Thus, why we aren't seeing these private holdings in the top ten list.

{kind=link}

Conclusion

ASGI is a non-leveraged CEF in the infrastructure space. The fund has a heavy weighting towards industrials, which has benefited the fund relative to other infrastructure funds this year. The fund, also not incorporating leverage, should see relatively lower volatility than its infrastructure peers as well. With the fund's large discount, it is currently looking quite attractive to consider for an income investor.

For further details see:

ASGI: Non-Leveraged Infrastructure Fund At A Deep Discount