TNET - ASGN Incorporated: Not A Great Play But Not A Bad One Either As We Near Fourth Quarter Earnings

Summary

- ASGN Inc. has generally fared well in recent years, but cash flows have been lumpy.

- The first nine months of 2022 demonstrated a similar degree of volatility, but the overall picture for the business tilts positive.

- Shares aren't the cheapest, but they are affordable and likely do have a bit of upside potential to them.

Companies, particularly large ones, often require a lot of support from other firms in order to function efficiently. This often takes the form of outsourcing certain activities such as information technology services and professional solutions. There are multiple companies that base their entire existence on providing these types of services for their clients. And one such example that investors should pay attention to is ASGN Inc. ( ASGN ). In recent years, the financial trajectory seen by the company has been quite lumpy. When you factor in this lumpiness with how shares are priced compared to similar firms, I would say that it's not a bad prospect, but it's not a great one either. All things considered, I would say that shares will likely generate performance that comes in slightly better than the broader market moving forward. And as such, I've decided to rate it a soft ‘buy’ at this time.

A decent firm, but nothing special

The management team at ASGN describes the company as a leading provider of information technology services and professional solutions. Examples here include technology, creative, and digital offerings, all spread across both the commercial and government sectors. To truly understand the company though, we should dig into each of its segments individually. The first of these is the Commercial segment, which provides IT services and solutions, as well as creative digital marketing services, to its customers. These largely consist of Fortune 1000 companies and mid-market clients. Specific activities here center around assignment and consulting. On the assignment side, the company provides clients with the aforementioned services on a temporary basis and/or for specific projects. Under the consulting side, the company provides workforce mobilization, modern enterprise, and digital innovation IT consulting services that span a wide variety of fields such as data and analytics, cloud, and digital transformation solutions. Altogether, this is the largest segment of the company, accounting for 73% of its revenue during its 2021 fiscal year.

Next in line, we have the Federal Government segment. This is considerably smaller, accounting for only 27% of the firm's revenue during its 2021 fiscal year. Through this unit, the company delivers advanced solutions in cloud, cybersecurity, artificial intelligence, machine learning, application and IT modernization, and science and engineering services to its clients, both in the public and private sectors. Some of this work also involves the US defense and intelligence communities. Often, these are contracts that range between three and five years in length, providing the company some degree of stability, irrespective of general market conditions.

{kind=link}

Author - SEC EDGAR Data

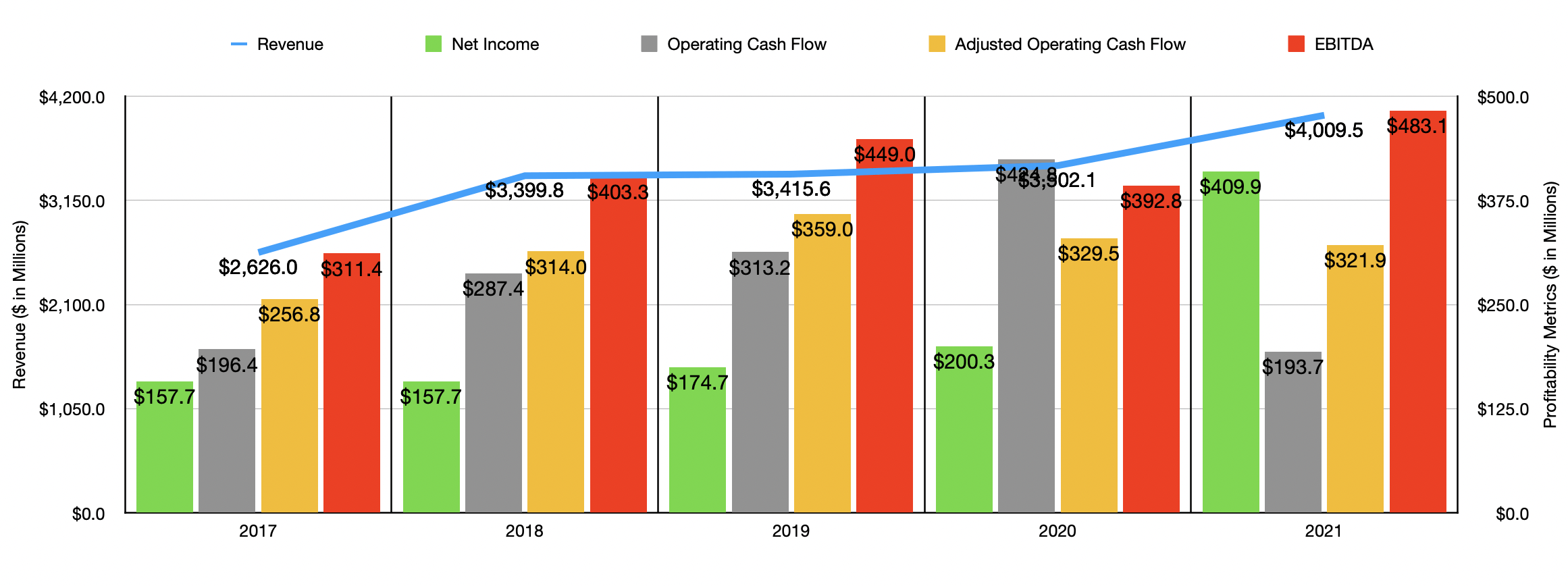

Over the past five years, the sales trajectory seen by ASGN was quite positive. Revenue increased in each of the past five years, jumping from $2.63 billion to $4.01 billion. The greatest growth for the company from 2020 to 2021 came from its Commercial segment, with revenue spiking 17.2% from $2.50 billion to $2.93 billion. The primary driver on this front was the consulting side of the equation, with revenue skyrocketing 68.3% from $380.9 million to $641.2 million. Management attributed this to robust growth in high-margin commercial consulting, creative digital marketing, and permanent placement services. Mid-single-digit growth in IT assignment services also contributed. This all, in turn, was largely the result of broad-based industry demand, an increase in the company's own technical capabilities, the expansion of its nearshore delivery center in Mexico, and the contribution from acquired businesses that added $40.5 million to the company's top line.

Also on the rise over the past five years was net income. This jumped from $157.7 million in 2017 to $200.3 million in 2020. Then, because of robust market conditions, the numbers spiked to $409.9 million in 2021. Other profitability metrics, however, did not exactly follow suit. After seeing operating cash flow climb from $196.4 million in 2017 to $424.8 million in 2020, it then declined to $193.7 million in 2021. If we adjust for changes in working capital, operating cash flow would have peaked at $359 million in 2019. In each of the two years since then, it declined year over year, eventually hitting $321.9 million. Volatility was also seen when looking at EBITDA. After hitting $449 million in 2019, up from $311.4 million two years earlier, the metric dipped to $392.8 million in 2020. In 2021, however, it made a fresh high of $483.1 million.

{kind=link}

Author - SEC EDGAR Data

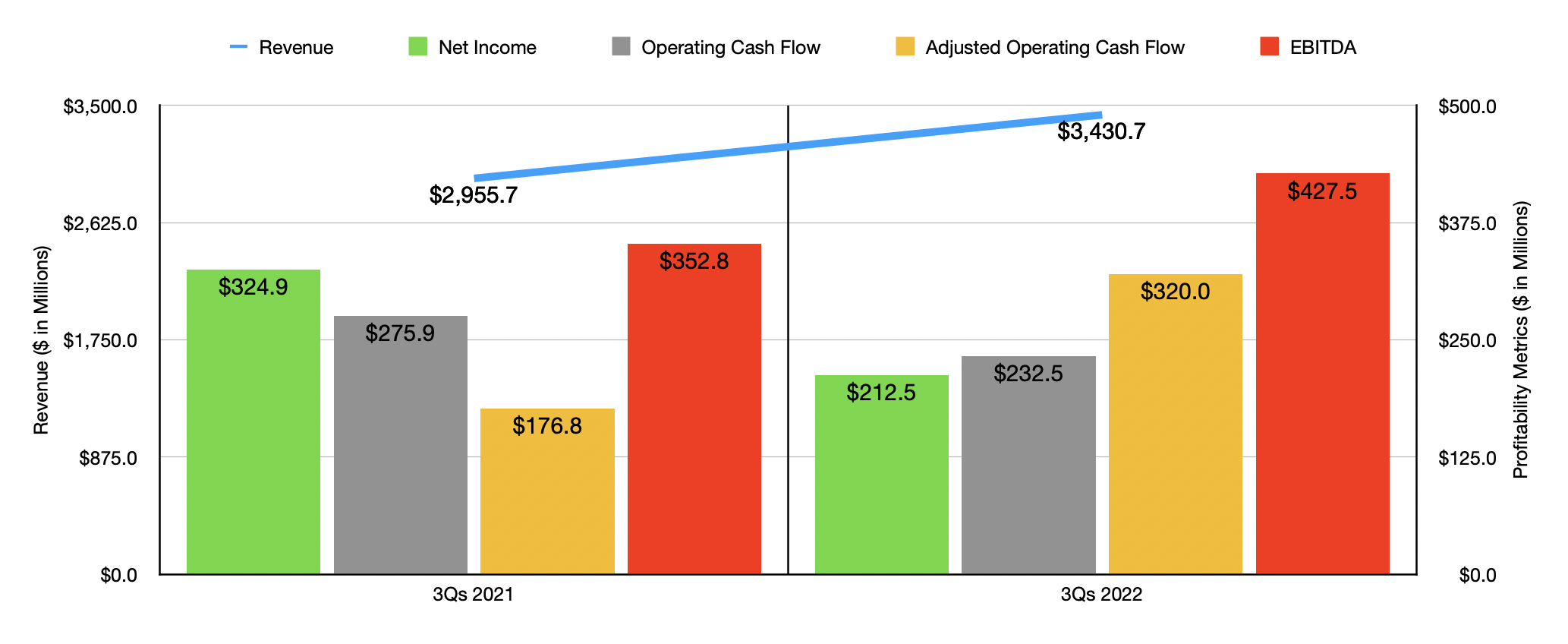

When it comes to the 2022 fiscal year, the picture for the company remained mixed. Revenue, for instance, came in strong during the first nine months at $3.43 billion. That translates to a 16.1% rise over the $2.96 billion reported one year earlier. At the same time, however, net profits dropped from $324.9 million to $212.5 million. Operating cash flow fell from $275.9 million to $232.5 million. But on an adjusted basis, it rose from $176.8 million to $320 million. Also on the rise was EBITDA, jumping from $352.8 million to $427.5 million.

After the market closes on February 8th, the management team at ASGN plans to announce financial results covering the final quarter of the company's 2022 fiscal year. For that quarter, they anticipate revenue coming in at between $1.12 billion and $1.14 billion. This would stack up nicely against the $1.05 billion reported one year earlier. For context, analysts are currently anticipating sales of roughly $1.14 billion. This suggests that they are more bullish than management was when they announced guidance back during their third quarter earnings release. On the bottom line, management said that net income would be between $54.2 million and $57.8 million. On a per-share basis, we are looking at between $1.07 and $1.14. This would be down from the $1.60 per share that management reported during the final quarter of 2021. Analysts, meanwhile, are forecasting profits of between $1.10 and $1.50 per share. This would mean net income of between $55.8 million and $76.1 million. Although analysts did not give any other real guidance, management did say that EBITDA should be between $128.5 million and $133.5 million for the quarter. For context, during the same time one year earlier, that metric was $130.3 million.

{kind=link}

Author - SEC EDGAR Data

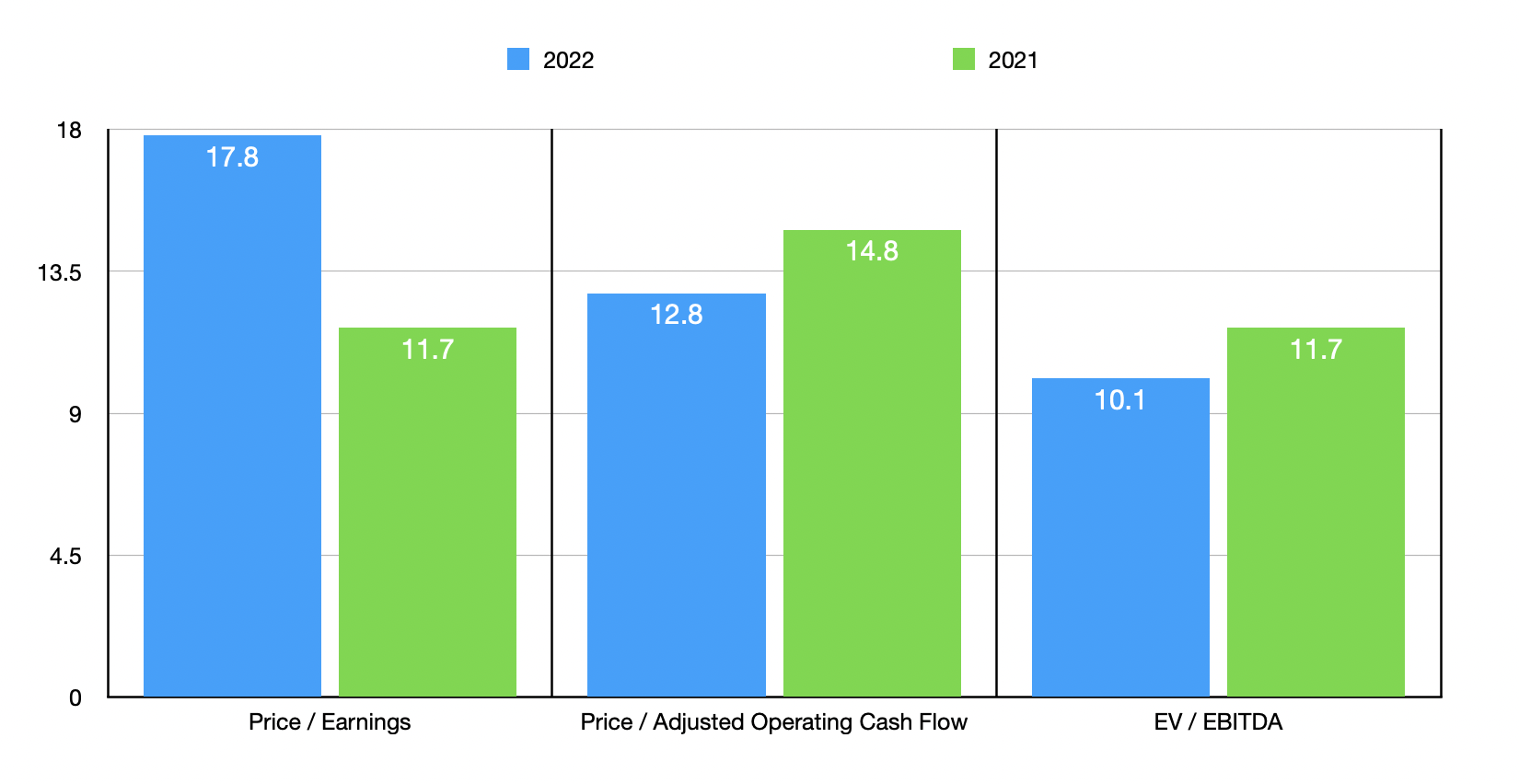

Based on the data provided, I estimated that the company should have generated net profits in 2022 of $268.5 million. Adjusted operating cash flow should come in at $372.1 million, while EBITDA should have been around $558.5 million. Using these figures, I calculated that the company is trading at a price-to-earnings multiple of 17.8. The price to adjusted operating cash flow multiple should be 12.8, while the EV to EBITDA multiple should be 10.1. As you can see in the chart above, this pricing is better, using two of the three metrics, than if we were to use data from 2021. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies range from a low of 9.4 to a high of 29. In this case, four of the five businesses are cheaper than ASGN. Using the price to operating cash flow approach, the range was from 6.8 to 16.3. In this case, one of the five companies was cheaper than our target. And finally, using the EV to EBITDA approach, the range was from 5.2 to 15.7. In this case, three of the five companies were cheaper than ASGN.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| ASGN Inc. |

| 17.8 |

| 12.8 |

| 10.1 |

| Insperity ( NSP ) |

| 29.0 |

| 13.4 |

| 15.7 |

| ManpowerGroup ( MAN ) |

| 12.9 |

| 11.3 |

| 7.2 |

| TriNet ( TNET ) |

| 13.5 |

| 16.3 |

| 7.4 |

| Kforce ( KFRC ) |

| 13.4 |

| 8.6 |

| 7.8 |

| Korn Ferry ( KFY ) |

| 9.4 |

| 6.8 |

| 9.1 |

Takeaway

From the data I see available, I must say that ASGN is an interesting company, but not one that I find myself particularly drawn to. I like the space in which it operates, but I also acknowledge that we will eventually see some weakness there. That could make shares a bit pricier moving forward. For now, the stock looks reasonably attractive, but it's also not anything special. Because of this and in spite of the fundamental lumpiness, particularly related to cash flows, that the company has demonstrated over the prior few years, I believe that a soft ‘buy’ rating is the best I can give it at this time.

For further details see:

ASGN Incorporated: Not A Great Play, But Not A Bad One Either As We Near Fourth Quarter Earnings