PEB - Ashford Hospitality's 12% Preferreds: You Can Check Out Any Time You Like

2023-06-30 15:42:16 ET

Summary

- Ashford common shares have recently scraped all-time lows.

- The preferred shares now yield over 12%.

- The bull argument can be summed up in four words, i.e. "mainly property level debt".

- Does that save the day for the preferred shares?

In our last article on Ashford Hospitality Trust ( AHT ) we highlighted our disagreement with analyst estimates. We also wanted investors to focus on the enterprise value rather than the market capitalization. Specifically we said,

Analysts are slowly coming around to our view and the consensus now believes that funds from operations (FFO) will drop by about 50% in 2023.

We are going out on a limb here to say that they are all still wrong and at least in the back half of the year, FFO will be negative. But assuming they are right and AHT churns out $1.00 of FFO per share, that is about $32 million. Does that $32 million of FFO on a $3.6 billion enterprise value excite you? Consider yourself alone then.

Source: Leverage Likely To Bite In 2023

The recent bump in share price notwithstanding, the stock has generally continued its downward trajectory.

Seeking Alpha

While the common shares have not paid a dividend in a long, long, time, investors have gravitated towards Ashford's preferred shares. Today, we look at what should be key considerations for anyone diving into those.

The Preferred Shares.

Ashford has five classes of preferred shares.

1) Ashford Hospitality Trust, Inc. PFD Series D ( AHT.PD ), coupon 8.45%, current yield 12.05%.

2) Ashford Hospitality Trust, Inc. PFD Series F (AHT.PF), coupon 7.375%, current yield 12.35%.

3) Ashford Hospitality Trust, Inc. PFD Series G (AHT.PG), coupon 7.375%, current yield 11.67%.

4) Ashford Hospitality Trust, Inc. PFD Series H (AHT.PH), coupon 7.5%, current yield 12.20%.

5) Ashford Hospitality Trust, Inc. PFD Series I ( AHT.PI ), coupon 7.5%, current yield 12.03%.

Obviously, these are some really high yields. Even considering the hotel REIT sector, these stand out. We briefly state three comparatives with coupons and yields.

1) Hersha Hospitality Trust RED PFD SER D ( HT.PD ) has a coupon of 6.5% and a current yield of 8.55%.

2) Braemar Hotels & Resorts Inc. Pfd Ser D ( BHR.PD ) has a coupon of 8.25% and a current yield of 8.58%.

3) Pebblebrook Hotel Trust 5.70% CUM PFD H ( PEB.PH ) has a coupon of 5.7% and a current yield of 8.2%.

So you are getting paid some abnormally high dough to get involved with Ashford. What are the risks?

Q1-2023

A look at the Q1-2023 results shows the strains facing the REIT. The company's own measure which include funds from operations (FFO), was negative to the tune of $17.2 million. We have also highlighted the preferred dividends in the picture below.

Ashford 10-Q

Adjusted FFO (AFFO) was positive but that includes three addbacks that we personally believe should not be added. These include the stock based compensation, amortization of the credit facility exit fee and amortization of loan costs. These are not one time items and considering the huge swath of refinancings that Ashford will have to engage in, you can expect them every quarter in some form or another. Without the help of these, AFFO would have been negative.

Why are FFO and AFFO so weak when the company has pretty much rebounded in terms of revenues from COVID-19?

The answer lies in Ashford's all-in bet on floating/variable rate debt. The vast majority of its debt is at the property level, which we agree is great. But the vast majority is also floating rate as can be seen below. These have all been resetting higher and by end of Q1-2023, their costs were eating Ashford's bottom line.

Ashford 10-Q

We have highlighted the one non-mortgage liability above as that will become crucial to negate the "buffer" argument.

Outlook

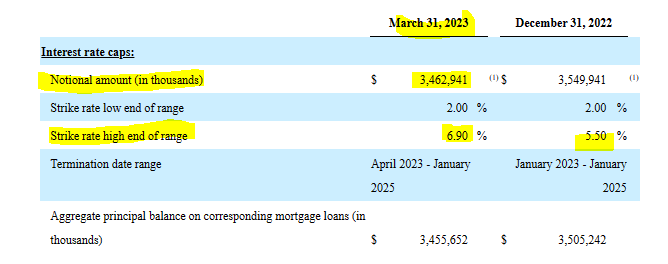

Interest expense was $81.5 million in the last quarter, almost double what we saw in Q1-2022. There are some caps and hedges in place that blunt the impact of more potential rate hikes by an overly enthusiastic Federal Reserve.

{kind=link}

Ashford 10-Q

We will note that this covers all the non-term loan mortgage debt that is variable rate. But the strikes, which refer to LIBOR rate, are still a bit higher than market in some cases. We would expect interest expense to rise again Q2-2023 and potentially peak out near the $85 million a quarter mark. $85 million in interest expense on a quarterly basis ($340 million annually), must be put in context of AHT's market capitalization.

We also think this will be higher than its adjusted EBITDA for the year. In other words, adjusted EBITDA minus interest will be a negative number. Needless to say FFO will be negative for the full year just as we saw for Q1-2023. That gets into just how poor the preferred share coverage is. But it gets worse as at the adjusted EBITDA and FFO level we are not even discussing capex. Ashford spent $29 million last quarter.

Ashford 10-Q

A normalized run-rate for us would be about $160-$200 million annually. So we think this capex has room to move up substantially.

Verdict

Ashford likely has a negative cash flow of about $150-$200 million annually when you consider the capex. Between 2016-2019, Ashford spent more than $200 million annually . While in theory preferred share dividends are paid before capex, Ashford does have to maintain its hotels for the long haul. The bull contention has been that Ashford has the cash to keep paying the preferred dividends. The balance sheet does support that for now. We are looking at $540 million of current assets that are relatively liquid versus $140 million of relevant current liabilities.

Ashford 10-Q

Before we go counting that $400 million though, we should offset against that term loan which we had highlighted earlier of $195 million. So that leaves us with $200 million or so and we should keep in mind that Ashford really cannot spend this down to the last cent, especially the restricted cash. At present, it has enough liquidity to keep paying the preferred dividends but we are betting that that will change between 9-15 months. The company has shown zero reservations in diluting common shareholders so if they do one massive round of share issuance again, it might buy the preferred shares some time.

We would stay out of this 12% yielder as you might get "Hotel Californiaed" here chasing yield. Once the dividends are cut, the preferred share prices could drop another 50% from here.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Ashford Hospitality's 12% Preferreds: You Can Check Out Any Time You Like