SVC - Ashford Hospitality Trust: Slow To Recover

- Ashford Hospitality Trust has been struggling for a couple of years now, with much of the pain caused by the pandemic.

- The firm is finally showing nice signs of a turnaround, and shares could end up looking quite cheap.

- But there are some issues the business is contending with, making the potential reward commensurate with the risk.

Few industries have been as negatively impacted by the COVID-19 pandemic as the hospitality industry. Due to the extreme social distancing that took place and the corresponding plunge in travel, the number of people staying at hotels plummeted, leading to significant pain for the companies that operate them. Since the pandemic has shown significant signs of winding down, a number of players in this space have shown improved fundamentals. But that doesn't mean that every prospect has recovered at the same pace. One of the laggards has, undoubtedly, been Ashford Hospitality Trust ( AHT ), an owner of hotel properties and other related assets.

Due to management's decision to sell off a number of properties over the past few years, as well as other factors like lackluster performance prior to the pandemic and a high amount of debt on its books, the enterprise turns out to be a rather complicated one to analyze. What we do know, however, is that the firm is finally showing some signs of recovery. On top of that, its stock looks rather cheap if we assume then it can eventually return back to pre-pandemic levels of activity. Although this is the case, I am also a firm believer in looking at the totality of the picture. And the data I see suggests a business that was never truly a high-quality operator even before the pandemic hit. So while shares of the firm may be cheap and may offer some nice upside potential if this current recovery continues, I am hesitant you rate it any higher than a 'hold' at this time.

A lot of issues to contend with

As I mentioned already, Ashford Hospitality Trust is a REIT that focuses largely on owning hotel properties. At present, the company has ownership interests in 100 consolidated hotel properties that have a combined 22,313 rooms in them. In addition, the business owns 82 hotel condominium units at WorldQuest Resort in Orlando, Florida. It owns a 16.7% interest in technology company OpenKey, which allows hotel guests to lock and unlock their hotel doors using their mobile app. Plus, it also has a 32.5% interest in 815 Commerce Managing Member LLC, which is the entity developing the Le Meridien Fort Worth hotel.

{kind=link}

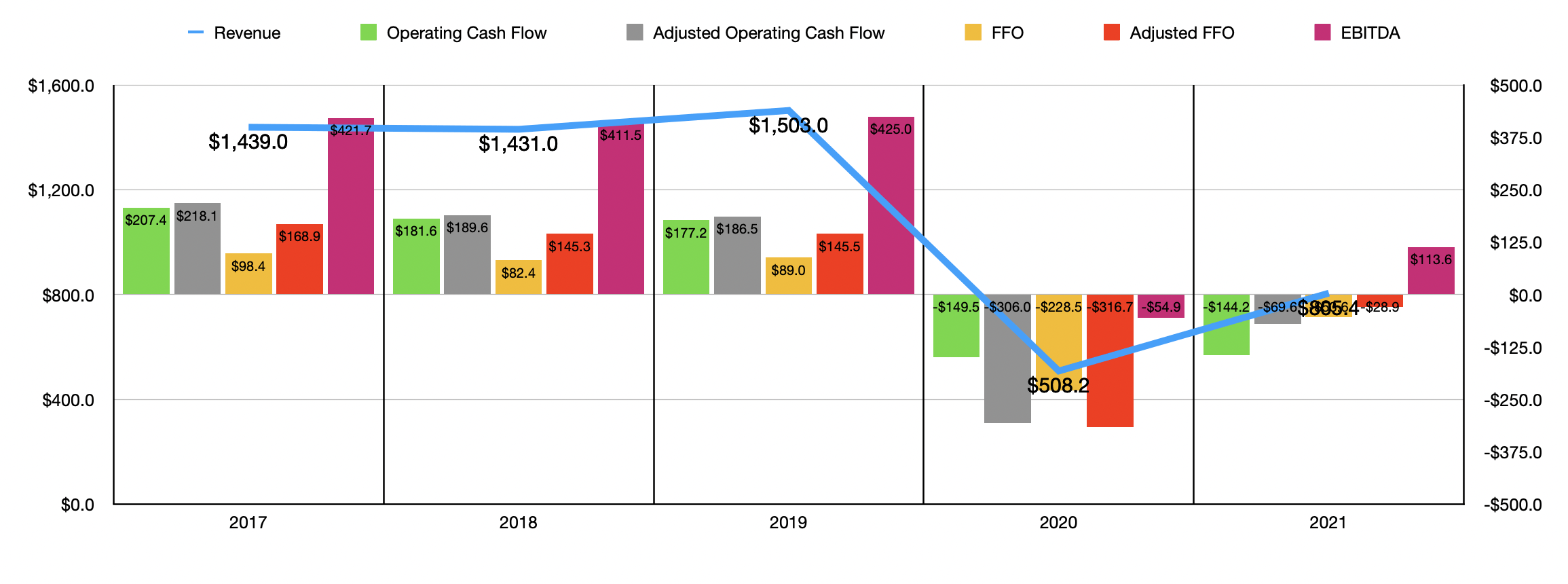

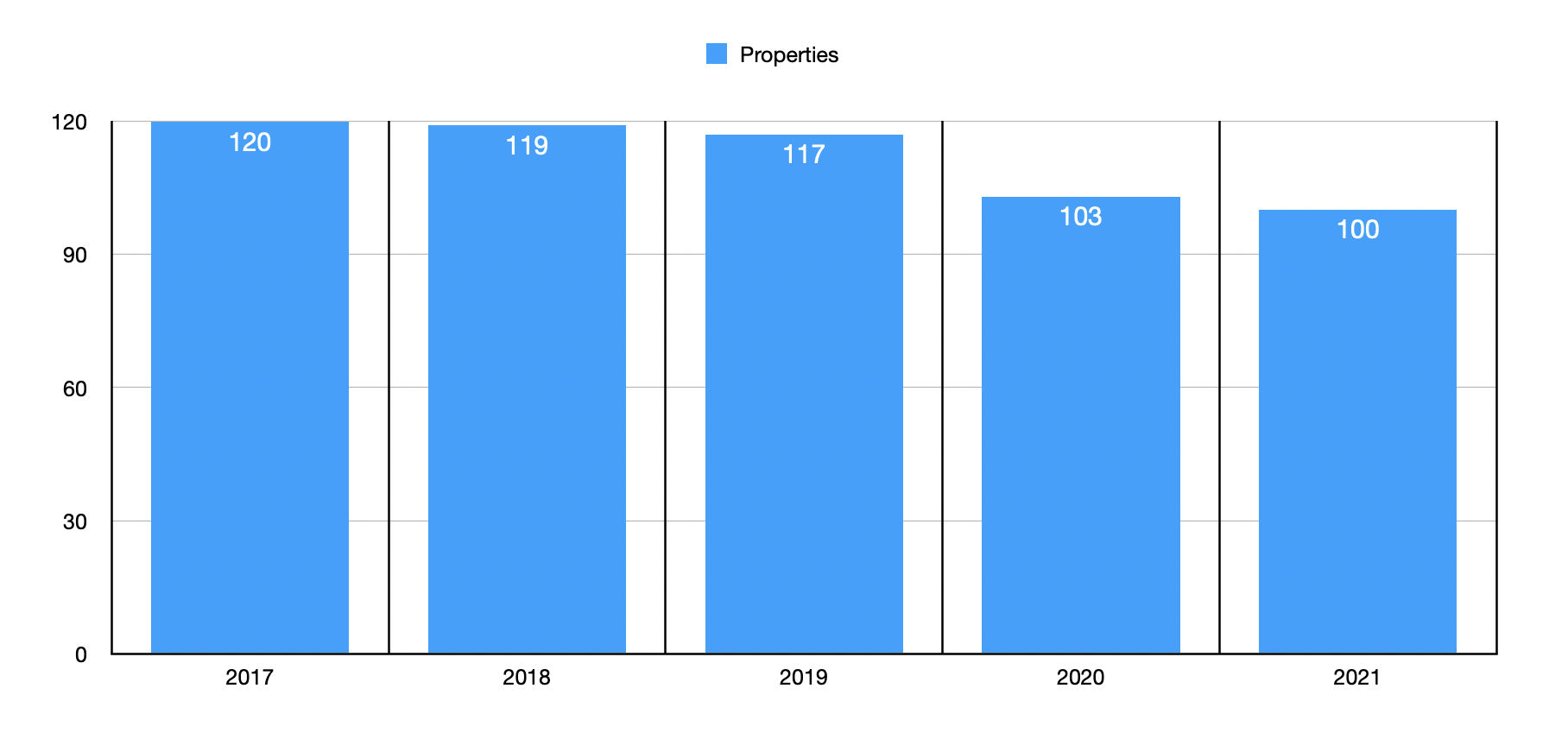

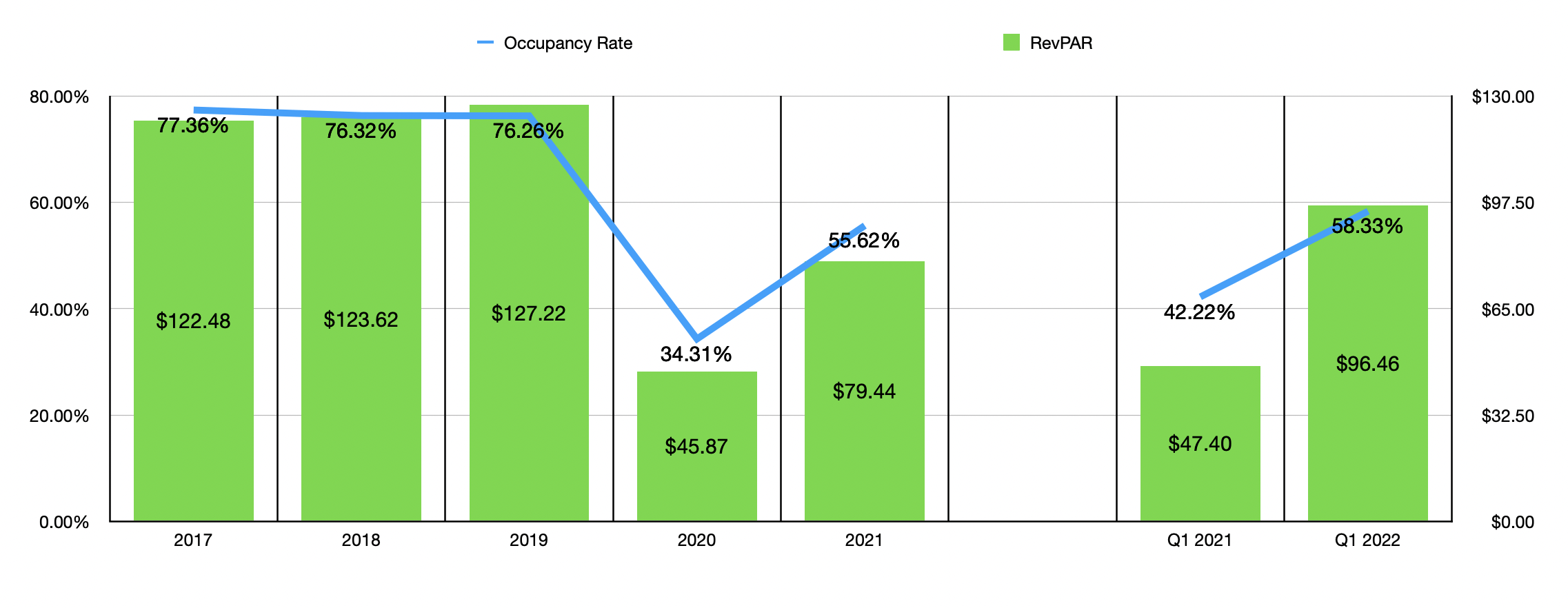

While all of these disparate assets cloud the fundamental picture of the company to some degree, there's no denying that the bulk of its activity relates to its consolidated hotel properties. And like pretty much every player in this space, the company was severely negatively impacted by the COVID-19 pandemic. Consider what happened between 2019 and 2020. In 2019, the company generated revenue of $1.50 billion. That plunged to just $508.2 million in 2020. This came in large part as a result of a plunge in occupancy at the company's hotels, with the occupancy rate falling from 76.3% in 2019 to just 34.3% in 2020. Another important metric to consider is RevPAR. This ultimately dropped from $127.22 to $45.87. Another key driver behind the difficult year was a decline in total assets the company owned. You see, at the end of 2019, the company had 117 hotel properties in its portfolio. After one year of the pandemic, this number had plunged to just 103.

{kind=link}

As revenue plunged between 2019 and 2020, we also saw profitability drop. The company's operating cash flow went from a positive $177.2 million to a negative $149.5 million. On an adjusted basis, the picture was even worse, with the metric falling from $186.5 million to negative $306 million. FFO, or funds from operations, went from $89 million to negative $228.5 million while the adjusted figure for this went from $145.5 million to negative $316.7 million. Even EBITDA for the company suffered, dropping from $425 million to negative $54.9 million.

{kind=link}

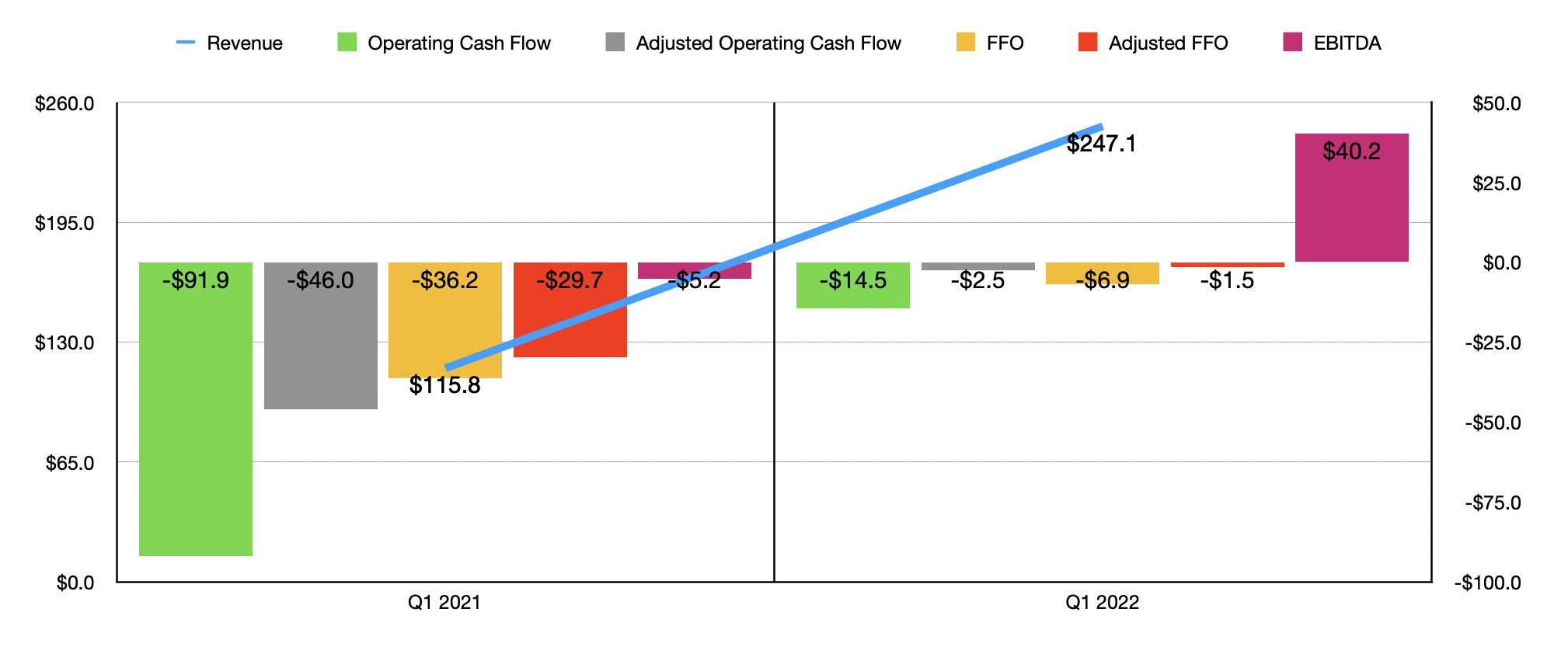

The good news for investors is that the company did start to see some sign of recovery in 2021. Although the number of hotel properties continued to drop, declining to 100 by the end of the year, occupancy rose to 55.6%, while RevPAR increased to $79.44. This was enough to bring the company's revenue up to $805.4 million for the year. Revenue has continued to improve into the 2022 fiscal year as well. For the first quarter of the year , revenue came in at $247.1 million. That's more than double the $115.8 million generated at the same time one year earlier. Although the number of properties for the company decreased during this time frame, its occupancy rate rose from 42.2% to 58.3% while its RevPAR increased from $47.40 to $96.46. We also know, thanks to some recent data provided by management, that the occupancy rate for its properties continues to improve. During the month of April, the occupancy rate at its properties increased to 74%. That brought the RevPAR of the firm up to $134. In May, the occupancy rate dropped a little bit to 72%. However, the RevPAR of the company remained relatively robust at $132.

{kind=link}

The recovery the company experienced on its topline over the past several months has also brought with it some recovery in the firm's bottom line. Operating cash flow moved to a negative $144.2 million in 2021 while the adjusted equivalent for this improved to a negative $69.6 million. FFO came in negative $53.6 million while adjusted FFO was negative to the tune of $28.9 million. The only profitability metric that turned positive was EBITDA. According to the data provided, this went from negative $54.9 million in 2020 to a positive $113.6 million last year. And the great thing is that this profitability picture has continued also into the current fiscal year. In the first quarter of the year, operating cash flow was negative by $14.5 million. That compares to the negative $91.9 million reported just one year earlier. On an adjusted basis, this metric went from a negative $46 million in the first quarter of 2021 to a negative $2.5 million this year. FFO went from negative $36.2 million to negative $6.9 million while the adjusted figure for this went from negative $29.7 million to negative $1.5 million. Over that same time frame, EBITDA turned from a negative $5.2 million to a positive $40.2 million.

At first glance, it may seem as though the recovery for the company is imminent. In truth, that's probably the case. But that doesn't make the firm a high-quality operation that's worth buying into. If you look at some of the graphs I provided throughout this article, you will also see performance for the firm prior to the pandemic. Profitability for the company has been rather mixed in the years leading up to that time frame, with the most common trend being a slight worsening of profitability and the company seeing occupancy rates at its properties drop while the number of properties in its portfolio also declined. If this were the only issue, then it could be overlooked. But there's also the fact that leverage for the business is quite high. Even if the company were to return back to the kind of performance it achieved in 2019, something that might be impossible because of its smaller asset base, the net leverage ratio for the firm would be 7.6. And that excludes the $163 million in preferred stock that the company has on its books as well.

{kind=link}

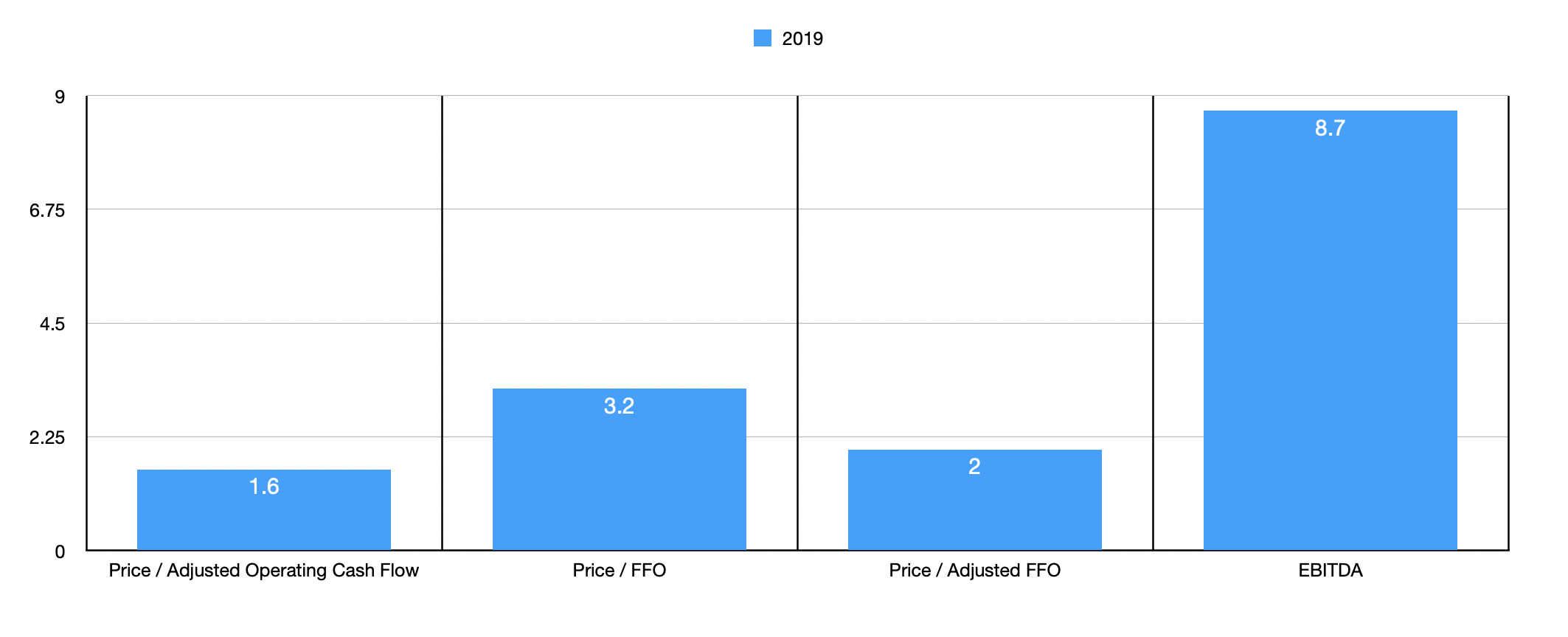

It seems to be this mixed operating history, combined with the firm's high leverage, that makes shares look cheap even if you assume a full recovery to the pre-pandemic times. For instance, using 2021 results, the firm is trading at a price to adjusted operating cash flow multiple of 1.6. The price to FFO multiple is 3.2 while the price to adjusted FFO multiple comes in at 2. The highest multiple for the company is the EV to EBITDA multiple, coming in at 7.6. This is not to say that the business is not trading on the cheap, though. As part of my analysis, I also compared it to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 4.4 to a high of 10. And using the EV to EBITDA approach, the range was from 10.4 to 14.7. In both cases, Ashford Hospitality Trust was the cheapest of the group. But given the company's mixed operating history, the very real probability that it cannot fully recover to what it achieved prior to the pandemic, and the high amount of leverage it has, this kind of discount relative to similar firms makes a lot of sense.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Ashford Hospitality Trust |

| 1.6 |

| 8.7 |

| Braemar Hotels & Resorts ( BHR ) |

| 4.4 |

| 11.1 |

| Hersha Hospitality Trust ( HT ) |

| 5.5 |

| 12.0 |

| Chatham Lodging Trust ( CLDT ) |

| 10.0 |

| 14.7 |

| Summit Hotel Properties ( INN ) |

| 8.6 |

| 10.4 |

| Service Properties Trust ( SVC ) |

| 6.5 |

| 11.0 |

Takeaway

At first glance, Ashford Hospitality Trust looks to be an interesting turnaround prospect that could serve as a deep value play for investors. I leave open the possibility that the firm could offer investors with significant upside potential if everything goes right. On the other hand, the company seems to have a lot of issues at this time and its risk profile is definitely greater than what you would expect of a high-quality operator. Normally, I am all for looking in the bargain bin when it comes to stocks. But in this case, I cannot bring myself to rate the enterprise any higher than a 'hold' at this time.

For further details see:

Ashford Hospitality Trust: Slow To Recover