ASH - Ashland: Poor Results And High Valuation

2023-12-04 00:57:34 ET

Summary

- Ashland struggled in FY23 due to a destocking issue, which is expected to continue affecting them in FY24.

- The company's Q4 FY23 sales declined by 18% compared to the previous year, with all segments experiencing a decline.

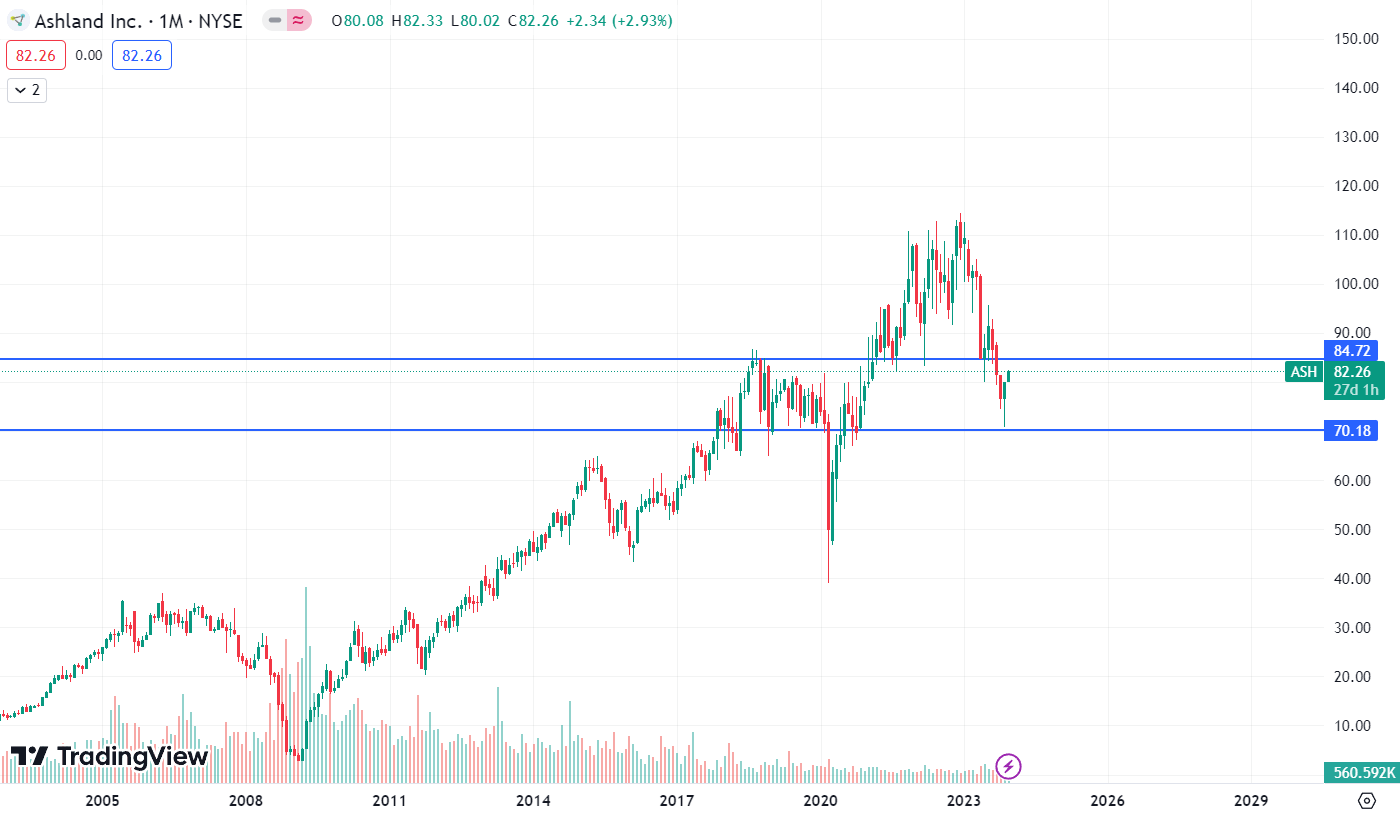

- ASH's stock price chart indicates a bearish trend, and there is a high chance it may reach $70 in the future.

Ashland (ASH) offers specialty ingredients and additives worldwide. ASH recently announced Q4 FY23 and FY23 results. They struggled in FY23 due to a destocking issue, which is expected to affect them in FY24. So, the outlook for FY24 isn’t that positive, and its valuation seems high. So, I think ASH might be unable to provide their investors any value. So, considering the risk, I assign a sell rating on ASH.

Financial Analysis

ASH recently posted Q4 FY23 and FY23 results . The sales for Q4 FY23 were $518 million, a decline of 18% compared to Q4 FY22. The sales from its life sciences, specialty additives, personal care, and intermediates segments saw a decline, which led to the poor performance of the company in terms of sales. The sales from the life sciences, specialty additives, personal care, and intermediates segments declined by 5%, 23%, 22%, and 42% in Q4 FY23 compared to Q4 FY22. All the segments were affected by customer inventory destocking, which led to a decline in sales. The gross margin also declined, and the decline was due to the inventory actions taken by the company due to low demand. The net loss for Q4 FY23 was $4 million compared to a net income of $57 million in Q4 FY22.

The annual numbers were also weak. The FY23 sales were down 8% compared to FY22, and the income from continued operations also declined 7.1%. The quarterly and annual results were disappointing, and the destocking issue affected them more in the second half. The destocking issue didn’t affect them much in the first half, but it was aggravated in the second half. The company is experiencing softness in demand, especially in Europe and China. The company expects the destocking issue to last until Q2 FY24, but that would be the best-case scenario. It can also extend further than that. One thing that somewhat offset the destocking issue was the high pricing. The company enjoyed high pricing in Q4 FY23, which I believe can be a matter of concern for FY24. Currently, the demand across markets is low, and no one can guarantee that the company will continue to enjoy high pricing. So, if they are not able to enjoy high pricing, then it can be worse for them. So, the future of ASH in FY24 looks uncertain.

Technical Analysis

{kind=link}

ASH is trading at $82.2. ASH's price chart doesn't look good. In September, the price broke down below the $85 level, which was an important support zone for the stock. After giving the breakdown, the stock is returning to retest the $85 level. So, the setup made here is bearish, and after the retest is done, there is a high chance that the stock might continue its downward trajectory. The next support zone for the stock is at $70. So there is a high chance that it might reach $70 in the coming times. Hence, considering the bearish price action, I would advise to avoid investing in ASH.

Should One Invest In ASH?

After three years of positive sales growth, they struggled to grow their sales in FY23, and with the guidance provided by the management and looking at the headwinds, I think they might continue to struggle in FY24 in terms of growth. The expected sales for Q1 FY24 are around $480 million, which is 8.5% lower than Q1 FY23. So, the expected weakness in FY24 can adversely affect ASH's share price. Additionally, the current valuation of ASH looks expensive. ASH is trading at a P/E [FWD] ratio of 26.86x compared to the sector median of 16.87x, and considering its performance, I think ASH is overvalued. Its EPS [FWD] is $3.83, and considering its outlook for FY24, I think it can trade around a P/E of 19x. So, it gives us a price target of $72.7, which is around 11% lower than the current share price. So, considering the poor results, overvaluation, and not-so-positive outlook for FY24, I assigned a sell rating on ASH.

Risk

Growing and unstable prices for raw materials, particularly for wood pulp, cotton linters, and hydrocarbon derivatives, could harm Ashland's operating expenses, operational performance, and inventory valuation. Similarly, energy expenses play a big role in several of Ashland's product costs. Ashland's capacity to pass on the costs of price rises is reliant on market conditions, and it is not always able to raise prices in response to such rising costs. Similarly, decreases in Ashland's inventory valuation brought on by market volatility might not be made up for and might even cause losses.

Ashland purchases specific goods and raw materials from vendors, frequently in accordance with formal supply agreements. Ashland might be unable to make alternate supply arrangements if those suppliers decide to cancel or fail to fulfill contractual obligations or if they cannot fulfill Ashland's orders in a timely manner. Additionally, Ashland may find it difficult to acquire some raw materials on commercially acceptable conditions due to national and international government rules pertaining to the production, shipping, or import of particular raw materials. Clary sage, aloe, guar, and cotton linters are agricultural products that are vital to several Ashland industries. Crop yields, meteorological conditions, and other factors can significantly influence the availability of these resources.

Bottom Line

ASH posted poor Q4 FY23 and FY23 results. The sales were down significantly, and the outlook for FY24 is weak. It might struggle financially in FY24, and its valuation looks expensive. Considering these factors, I think ASH might not be able to provide any value to its investors in the coming quarters. So I assign a sell rating on ASH.

For further details see:

Ashland: Poor Results And High Valuation