ASHR - ASHR: Too Early To Be A Mainland China Contrarian

2024-01-12 12:27:52 ET

Summary

- Chinese mainland blue chips had another torrid year in 2023.

- Yields are up, but valuations are not that cheap; nor has the macro backdrop improved.

- A-share vehicles like ASHR might still have more room to correct before we hit bottom.

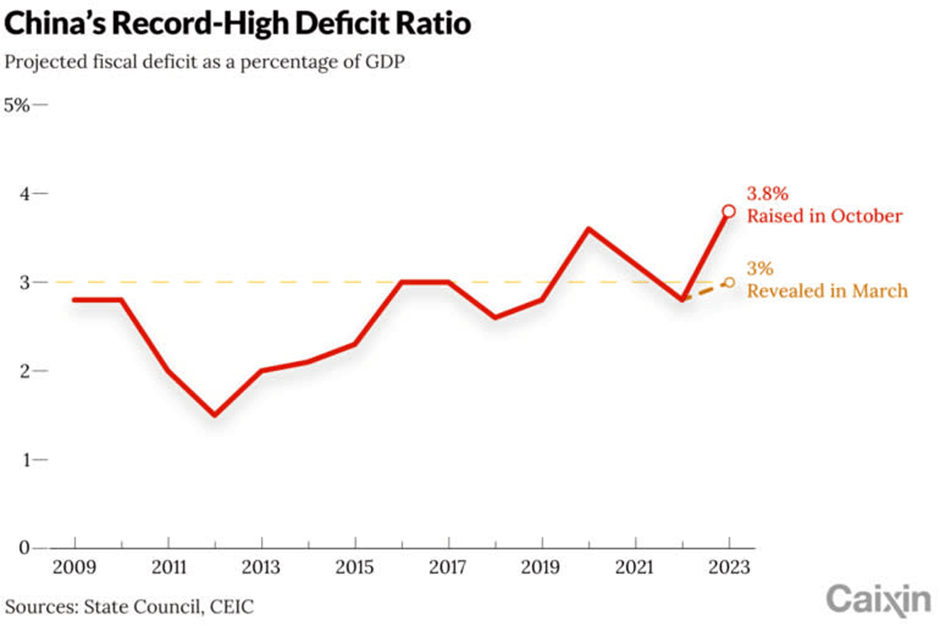

News flow out of China has shown some promise in recent weeks. Since the positive 'Central Economic Work Conference' (a year-ahead meeting for policymakers with regard to economic targets) in December, policy rhetoric has been very much one of growth. Of note, the post-meeting commitment to "effective improvement" came on the heels of a new willingness to push the deficit 'red-line' above 3% - positive signs in light of the ongoing property downturn. From here, all eyes will be on where this year's growth target lands (recall the 2023 target was +5% off a COVID-impacted base). Anything above 5% would indicate significant policy easing in the near future - both from the central bank (rate cuts) and central government (more bond issuances).

{kind=link}

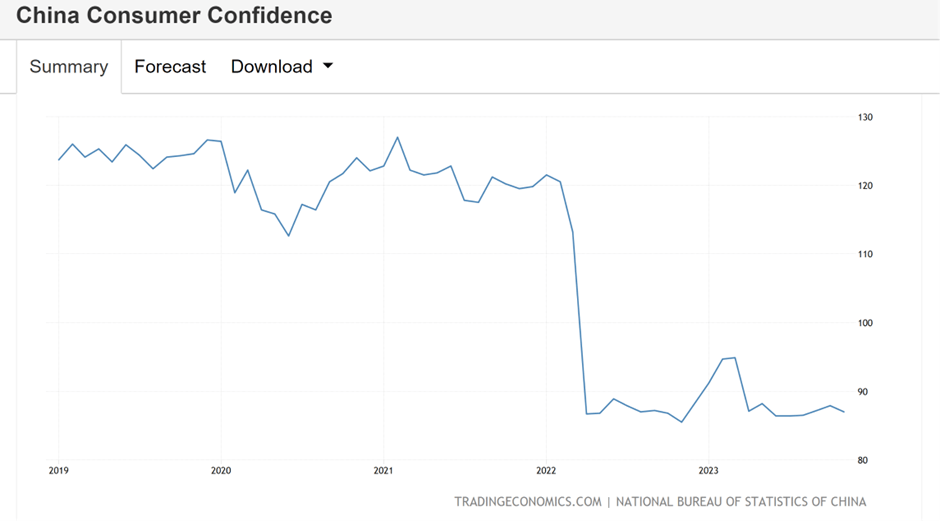

The prospect of more easing would, of course, be bullish for free-falling mainland Chinese equities. But this needs to be balanced against sluggish near-term economic activity and deflationary pressures, as well as a big demographic headwind long-term. Key to a reversal, in my view, is a psychologically impacted consumer - thus far, they continue to sit on record bank deposits post-COVID and remain largely unresponsive to incremental interest rate cuts.

{kind=link}

Efforts to reduce urban unemployment should help, as will more policy support for the property market. Ultimately, though, a lot more is needed for confidence to return, and thus, it might still be too early to underwrite a contrarian buy on Chinese equities.

Optimists will point to de-rated mainland equity prices - per the CSI 300 index tracked by the Xtrackers Harvest CSI 300 China A-Shares ETF (ASHR), mainland blue chips are now on offer at a seemingly undemanding ~10x trailing earnings and ~1.2x book . But this de-rate is more a reflection of the negative regime shift in economic, regulatory, and geopolitical direction than genuine value emerging, in my view; hence, in line with my prior coverage of ASHR, I continue to err on the side of caution here.

Xtrackers Harvest CSI 300 China A-Shares ETF Overview - One of the Better Mainland China Trackers

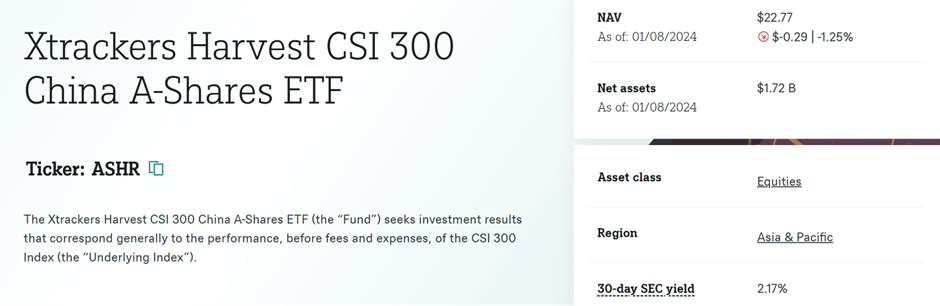

The DWS Group-managed Xtrackers Harvest CSI 300 China A-Shares ETF tracks, pre-expenses, China's market cap-weighted CSI 300 Index, a basket of 300 blue-chip mainland listings. While net assets further declined to ~$1.7bn after another drawdown in Q4 last year, the ASHR net expense ratio remains at a relatively competitive ~0.7% net (entirely from management fees).

By comparison, its closest US-listed A-share ETF comparable, iShares MSCI China A ETF (CNYA), charges a lower ~0.6% net but is also smaller and less liquid. After accounting for ASHR's narrower median bid/ask spread, the cost gap between both funds is quite marginal.

{kind=link}

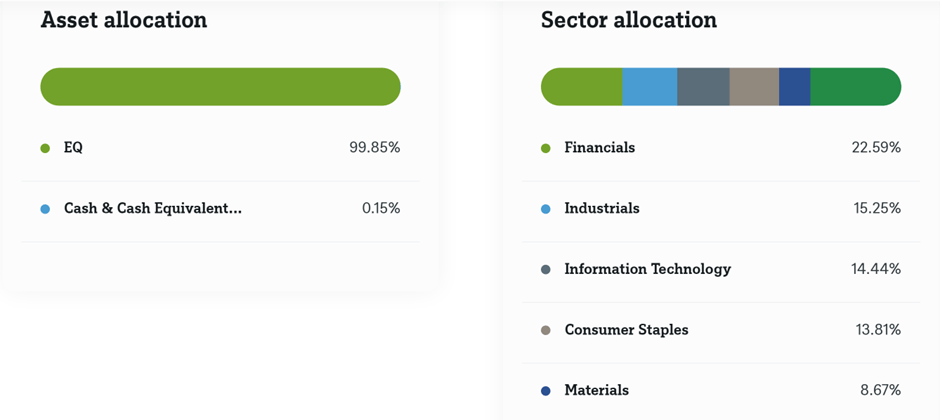

The fund's sector breakdown continues to lean toward China's Financials sector, albeit at a slightly lower 22.6%. Industrials and Information Technology also remain meaningful portfolio exposures at 15.3% and 14.4%, respectively, with Consumer Staples (13.8%) the only other sector over the 10% threshold. Together with Materials (8.7%), ASHR's top-five contribution runs at ~75%, so it's worth being mindful of the sector concentration.

{kind=link}

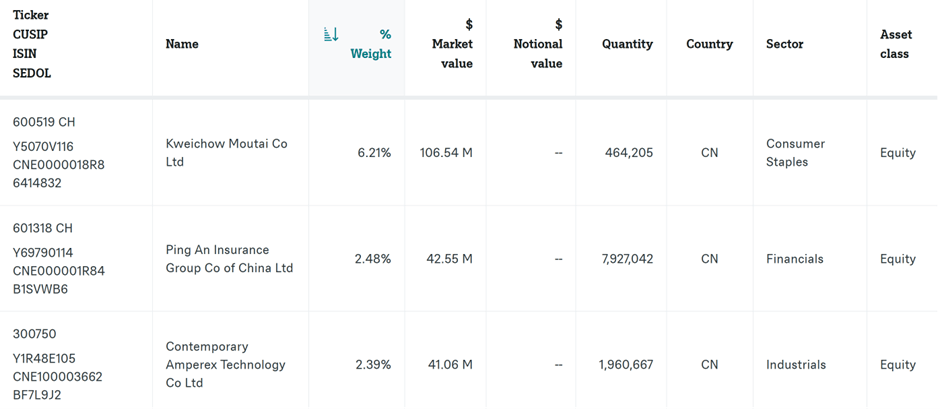

The fund's 300-stock portfolio composition hasn't seen too many notable shifts. Spirits franchise Kweichow Moutai is now an even larger holding at 6.2%. Outside of Moutai, most other holdings have a 2% or lower slice of the portfolio - insurer Ping An Insurance (Group) Company of China, Ltd. ( PNGAY ) and battery manufacturer CATL, the second and third-largest stock allocations, are slightly reduced to 2.5% and 2.4%, respectively. Beyond major banks like China Merchants Bank Co., Ltd. ( CIHKY ) and Industrial and Commercial Bank of China Limited (IDCBY), both of which have been relatively resilient through the broader market turbulence, consumer blue-chips Midea Group and Wuliangye Yibin also hold firm in the ASHR portfolio.

{kind=link}

Xtrackers Harvest CSI 300 China A-Shares ETF Performance - Another Down Year in 2023

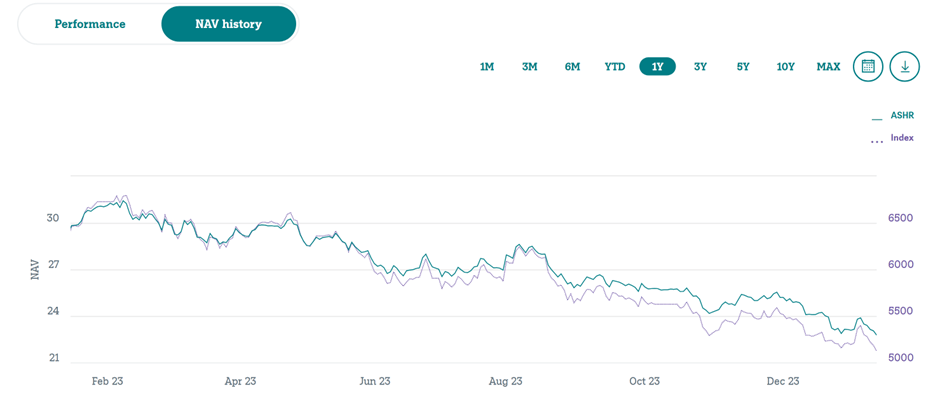

Following a disappointing Q4, ASHR's 2023 performance has worsened to -12.5% in market price terms and -13.1% in NAV terms - a wider than usual gap vs. the -11.1% returned by its underlying CSI 300 Index benchmark. In turn, the fund's overall compounding rate since inception is also down to +3.1% per annum in market price and NAV terms, with a poor three-year run (-14.7% annualized NAV return) further eating into the fund's prior gains. While ASHR is slightly ahead of key peer CNYA (-13.5% in 2023), it has far underperformed consumer/tech-focused Invesco Golden Dragon China ETF (PGJ), which only posted a -2.5% loss for the year.

{kind=link}

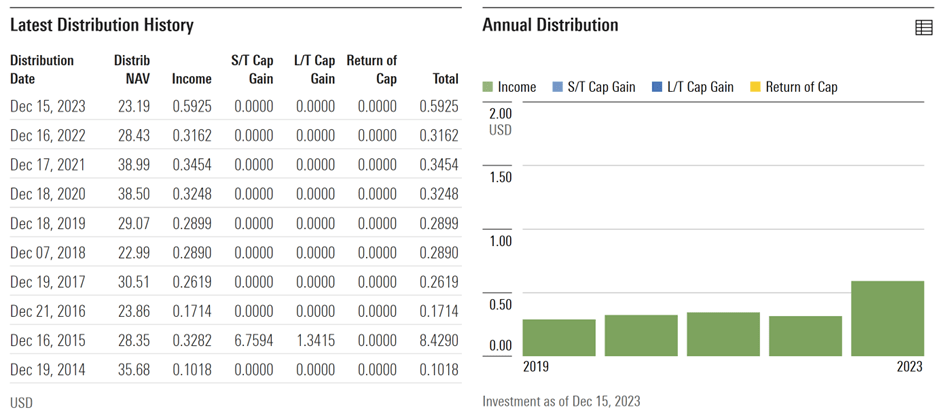

The only real positive for 2023 was ASHR's higher $0.59/share year-end distribution. In total, this moves the yield up to a solid ~2.6% - slightly below CNYA's ~3.1% trailing twelve-month yield but well ahead of Chinese ADR-focused funds like PGJ. Given most of the payout is funded by income from ASHR's cash-generative portfolio rather than one-off capital gains, the current pace is likely sustainable. Valuations, on the other hand, are still not as cheap as I'd like - the ASHR portfolio is currently priced at a premium to book and a ~10x P/E multiple.

{kind=link}

Too Early to be a Mainland China Contrarian

In contrast with the China optimism at the start of 2023, things are a lot more bleak in the early innings of 2024. While there have been some bright spots in the macro data, including the urban unemployment rate and leading Caixin PMI indicators (manufacturing and services), the underlying issues that plagued Chinese equities last year remain unresolved.

Yes, there is growing recognition among policymakers that support is needed, particularly for the deteriorating property market. The issue, though, is the very limited capacity to recover consumer confidence - a result of overly high local government debt levels accumulated over the years. More incremental, rather than large-scale fiscal and monetary easing means any turnaround is likely to be a very gradual one. Net-net, even with mainland equity listings priced multiple turns below where they were a few months ago, I am still quite cautious.

For further details see:

ASHR: Too Early To Be A Mainland China Contrarian