ASHTF - Ashtead Group: Cautious After The Big Half-Year Revision

2023-12-06 10:34:49 ET

Summary

- Ashtead has reset its near-term guidance bar lower.

- While the resulting stock price sell-off has been significant, not enough optimism has been cleared out.

- The stock remains pricey (for a cyclical) and pays investors a low dividend; I see no reason to buy this dip.

Ashtead Group ( OTCPK:ASHTF ), a construction and industrial equipment rental company operating global networks under the 'Sunbelt' brand in the US and the UK (formerly A-Plant), has seen its stock hammered in recent weeks following a big FY24 revision in its pre-released trading update . The extent of the sell-off might seem excessive for a fiscal Q2/Q3 event (near-term emergency response headwinds (e.g., hurricanes)), though the spillover impact into FY25 via higher depreciation and interest charges is material as well.

More broadly, investors may also be pricing in a protracted period of GDP weakness or perhaps even a recession next year – in line with the many rate cuts currently priced into the US/UK sovereign bond curves. Even after the recent de-rate, Ashtead isn’t cheap at the current mid to high-teens earnings multiple, likely already embedding expectations of a more resilient through-cycle earnings profile. With more capex outlays also likely to hinder free cash flow generation and the relatively low 1-2% dividend yield offering little incentive to hold the stock, I would steer clear.

A Big Letdown at the H1 Update

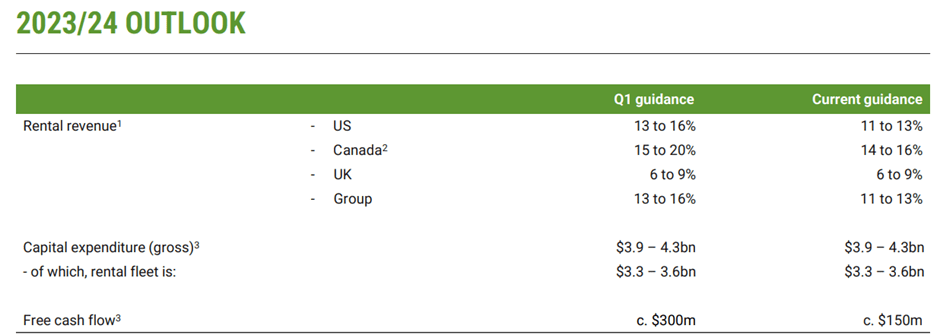

Ashtead has been riding a strong wave of earnings momentum through the pandemic, so the market had perhaps been expecting a benign outcome ahead of its interim trading update. Yet, the pre-release last month and this week’s detailed H1 2024 release offered more negatives than positives. The company did start on a high, noting “record results for the half year and the second quarter with Group rental revenue growth for the half year of 13%, EBITDA growth of 15%.” But accompanying the headline numbers was an acknowledgment of “lower levels of emergency response activity with a significantly quieter hurricane season than seen in recent years and fewer naturally occurring events, such as wildfires, with this effect continuing into the third quarter.”

At first blush, the Q2/Q3 “emergency response” headwind might seem like a temporary phenomenon, though the larger-than-expected guidance revision is nonetheless concerning. Specifically, US rental revenue growth is now set to run at 11-13% (down from 13-16% previously), with EBITDA also running two to three percentage points lower. Also weighing on the P&L is a hefty ~$2.1bn depreciation charge for the full year.

{kind=link}

Ashtead Group

Post-release, the stock suffered a steep sell-off and has yet to recover (note that the FTSE has closed higher over the same period). While Ashtead has delivered immense value over the years, largely on the back of operating leverage gains and accretion from bolt-on acquisitions, the market may finally be coming to terms with more challenging trading conditions going forward. It’s also worth keeping in mind that Ashtead was trading at some fairly pricey multiples (for a cyclical name) heading into the print. With all this in mind, I don’t view the sell-off as excessive - even with the company offering some mitigating positives, such as higher YoY second-hand equipment sales for the year.

Looking Ahead to a More Challenging 2024

Even with the bar reset lower post-H1, there are still plenty of ways investors can lose out here. After all, we are heading into a higher rate backdrop, an environment where cyclical, capex-heavy companies like Ashtead don’t typically thrive. So, while management successfully capitalized on the low to near zero interest rate environment post-financial crisis, I would be cautious about underwriting similar success in the near term.

Plus, I’m not convinced the company has completely normalized earnings from its pandemic years, when utilization was running at unsustainably high levels. Depending on how many of the customers that left during the pandemic years return (note Ashtead suffered some churn due to the lack of capacity), utilization rates could normalize lower than many expect. Given management has also committed to an elevated capex run rate, necessary to refresh its fleet and keep maintenance costs down, this could hit its free cash generation going forward.

{kind=link}

Ashtead Group

Following H1, the next catalyst will be Ashtead’s strategic mid-term update, due on its capital markets day in Q2 next year. The event could go both ways – my base case is that management will push a strongly positive message, particularly around the upside from a post-lockdown infrastructure recovery in the US, though a more prudent move to reset mid to long-term expectations may also be on the cards. In any case, I suspect the event will offer support to Ashtead bulls heading into its fiscal year-end, potentially a reason for the stock still sustaining a mid to high-teens earnings multiple.

For now, I don’t see a compelling reason for current valuation levels - this remains a cyclical business heading into a potential economic downcycle next year when the lagged impact of higher rates starts to bite. Investors aren’t getting paid a high enough dividend either at the current sub-2% yield (vs 4-5% for longer duration Gilts). At the same time, they'll have to take on the risk of dilutive capital raises (debt or equity) to fund more bolt-ons or future legs of its capex cycle. Pending clear signs of earnings resilience through a lower GDP environment with higher funding rates, I think there may still be more downside ahead.

{kind=link}

Ashtead Group

Cautious After the Big Half-Year Revision

Ashtead has been rightfully punished in recent weeks as markets price in its lowered FY24 guidance. While management has caveated that this was driven by transitory factors rather than anything structural, there will be some post-FY24 P&L impact, particularly on the depreciation and interest lines. Longer-term, I suspect too much optimism has been priced into Ashtead stock at the current mid to high-teens earnings (high-single-digits EV/EBITDA) - a multiple more characteristic of secular growth than cyclical. So, in the likely scenario that the earnings trajectory comes under pressure from the double whammy of a GDP downturn next year and ‘higher for longer’ rates, the stock could still de-rate from here. Net, I see no reason to chase the shares after the recent dip and remain firmly on hold.

For further details see:

Ashtead Group: Cautious After The Big Half-Year Revision