FINGF - Ashtead Group: Upside Remains Attractive Despite Possible Near-Term Slowdown

2023-07-13 12:48:55 ET

Summary

- I reiterate a buy rating for ASHTY as I expect earnings to remain healthy and strong, despite a near-term slowdown.

- Despite near-term macro volatility, ASHTY should benefit from large mega projects in the U.S., as construction companies prefer to rent rather than buy during uncertain periods.

- While ASHTY's net debt position poses some risk, expected EBITDA growth should help lower the debt ratio.

Summary

Following my coverage on Ashtead Group ( ASHTY ), where I recommended a buy rating due to my expectation that ASHTY can sustain its growth in the current market while keeping its margins and returns healthy and expanding its free cash flow, this post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating on ASHTY with a price target of $90.34.

Business description

ASHTY is a provider of rental machinery and tools. The business' primary activity is the leasing of heavy machinery for building and manufacturing projects. Ashtead Group primary serves customers in the United Kingdom, the United States, and Canada.

Competitive environment

Grand View Research estimates that the global construction equipment rental market will grow from its 2022 size of $187.46 billion at a CAGR of 6.12% between 2023 and 2030. Spending increases on public infrastructure development and improvement, in my opinion, will provide a solid foundation for growth. Because of this, the construction equipment industry is booming. Companies and contractors in the construction industry are beginning to shift their focus from purchasing to renting construction equipment as a result of the rising cost of new machines due to inflation and supply chain issues. Renting construction machinery is a good alternative to buying new, maintaining, and stockpiling lots of tools.

Key rivals of ASHTY include Caterpillar ( CAT ), United Rentals ( URI ), Ahern Rentals, Cramo, Finning International ( FINGF ), and Liebherr-International.

Investment thesis

The fourth quarter of FY23 saw a constant currency increase in rental revenue of 15% for ASHTY, and an annual increase of 22%. Despite the fact that the macro environment will likely remain volatile in the near future, I think ASHTY will continue to profit from secular trends surrounding the acceleration of large mega projects in the United States, which are being driven by US legislation like the IRA, CHIPS Act, and Infrastructure Investment and Jobs Act. Increased rental market share, especially in the Specialties sector, should be good for ASHTY as well.

Since mega projects in the United States have a much longer average timeline of three years, I believe they will provide some resilience to growth in the near term, and management continues to place a strong emphasis on capturing a share of these opportunities.

Ashtead remains a secular growth story in my view and has the potential to continue growing at 20% over the near-term, similar to how it has performed in the past. This, combined with M&A and capital returns, should support a very positive equity narrative and propel share-price outperformance.

P&L/Balance sheet

{kind=link}

{kind=link}

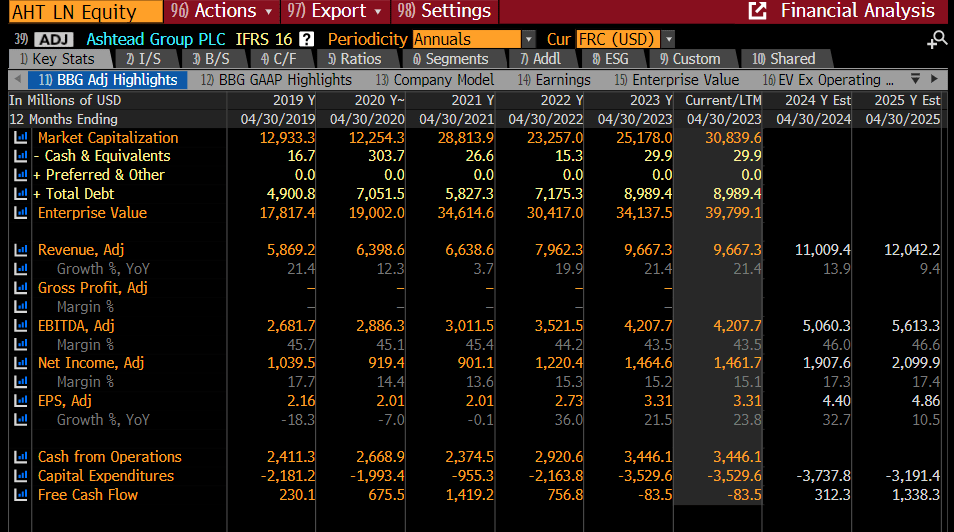

If we exclude the FY20/21 period, which was impacted by COVID and lockdowns, the ASHTY revenue trend has been strong. Excluding those, ASHTY has grown at a 20% annual rate for the other years, indicating a strong demand for rental equipment, which I interpret as a clear indicator of strong demand. As ASHTY is not immune to the macro situation, I expect moderate growth to slow for the rest of the year. However, I believe growth will remain healthy in the high teens as construction companies prefer to rent rather than buy during this uncertain period.

Given the fixed cost nature of the business, as growth slows this year, margins should suffer as well. Because ASHTY must maintain its fleet of vehicles regardless of utilization, lower volume results in lower margin. In absolute terms, I anticipate flat earnings in FY24, as management is likely to cut some expenses to protect margins. Earnings and margins should improve once growth returns to 20% or higher.

{kind=link}

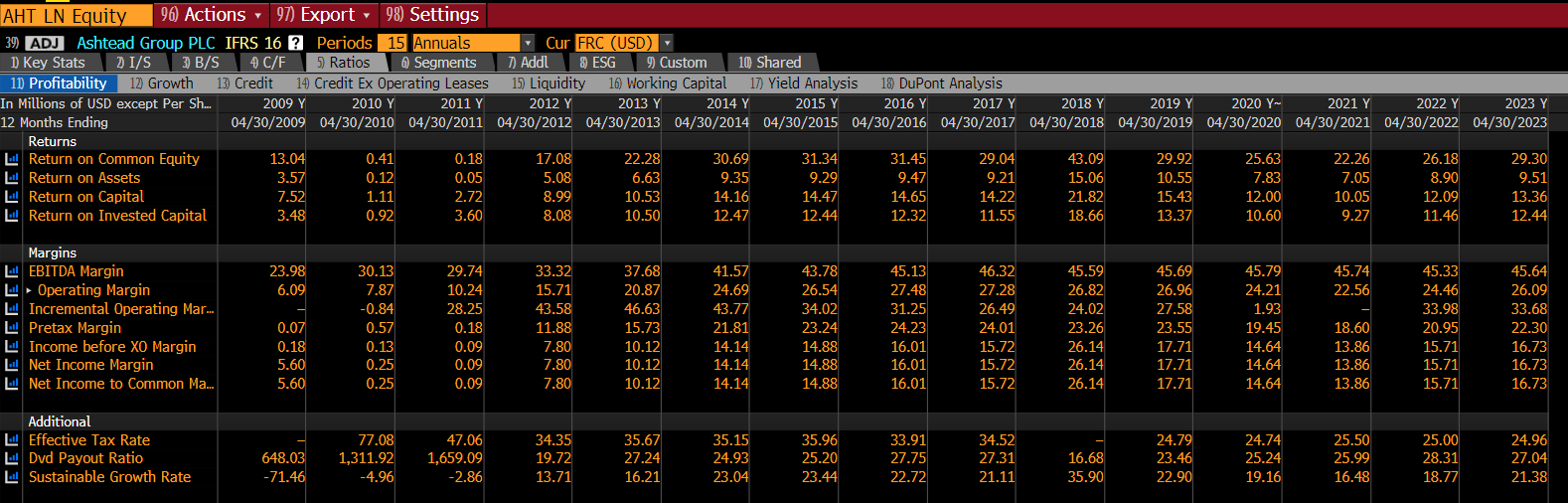

Given its net debt position of nearly $9 billion, ASHTY's balance sheet is not of the highest quality, exposing it to interest rate risk. The business net debt to EBITDA ratio has gradually increased up to 2x over the years, which is a mini red flag in terms of capital management.

Valuation

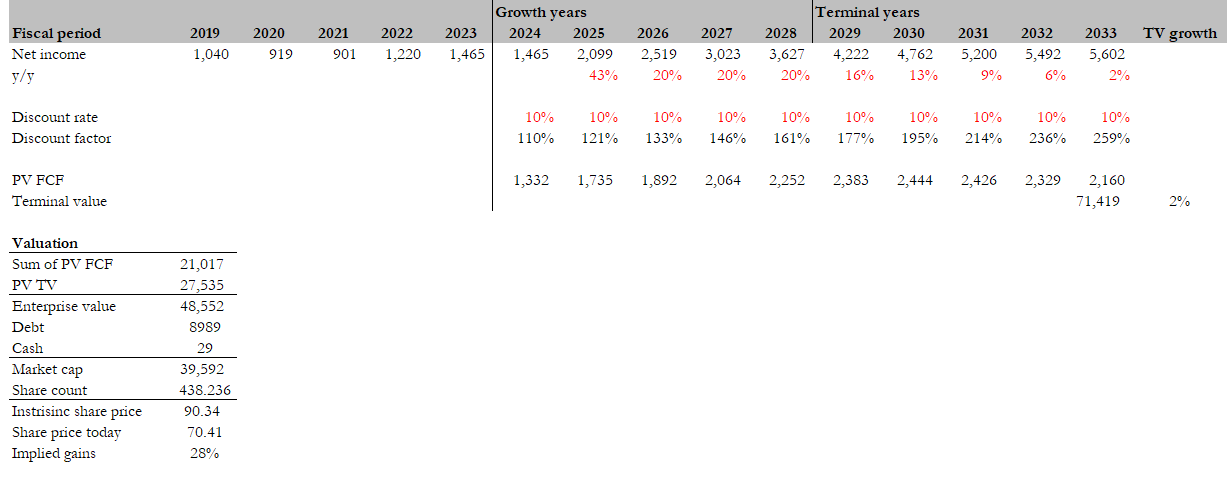

I believe the fair value for ASHTY based on my DCF model is $91. My model assumptions are that:

- Earnings to inflect in FY25 when growth normalizes

- Earnings to grow 20% as topline growth reverts to historical range

- Earnings growth to taper down to inflation rate over the long-term

{kind=link}

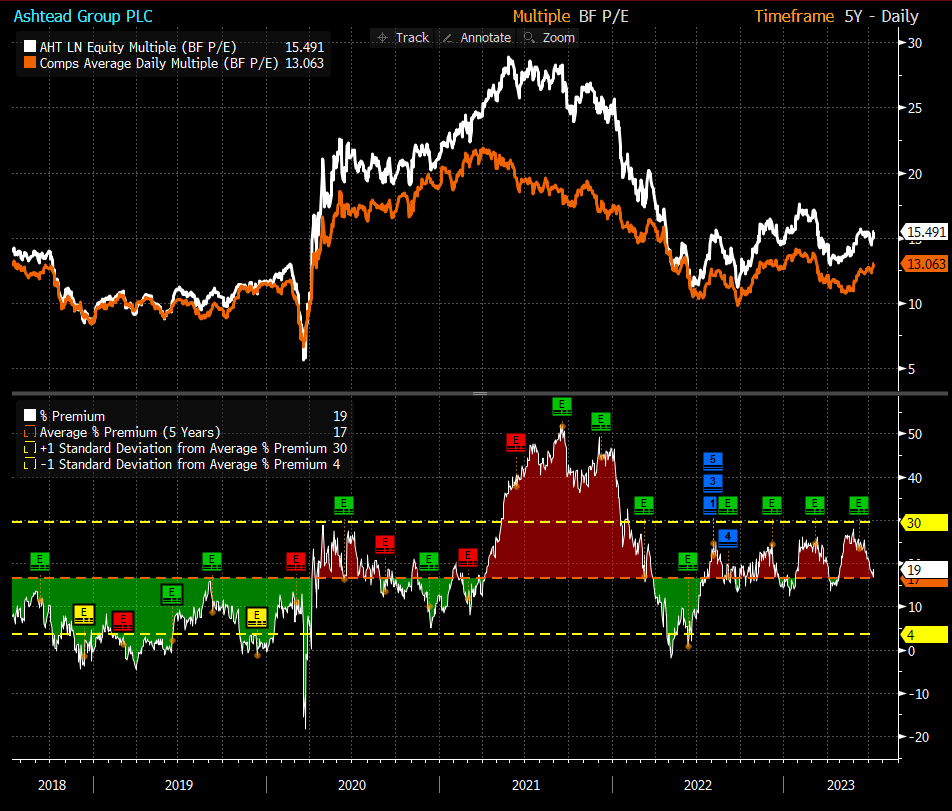

ASHTY is trading at 15.6x forward PE, and it is trading at a premium of around 3x to peers. This premium, I believe, is justified because ASHTY is growing faster than its peers (CAT, URI, FINGF) on average and has higher profit margins.

- CAT trades at 13x forward PE and is expected to grow at 4% next year with 17% EBITDA margin

- URI trades at 11x forward PE and is expected to grow at 16% with 49% EBITDA margin

- FINGF trades at 11x forward PE is expected to see revenue decline 6% with 12% EBITDA margin.

While the debt ratio is higher, I believe it is not a risk given the expected EBITDA growth, which should lower the ratio.

{kind=link}

Risk

Despite the very significant shifts that have occurred in both the business model and the rental market, ASHTY still has elements of cyclicality, given the nature of the industry. My expectation is that the company will be able to weather a recession much more successfully than in the past; however, short-term impact on earnings and sentiment might still exist.

Conclusion

In conclusion, I reiterate my buy rating for ASHTY with a price target of $90.34. ASHTY has demonstrated strong growth in rental revenue, and I expect it to be well-positioned to benefit from the acceleration of large mega projects in the United States. Despite the near-term macro volatility, ASHTY's focus on capturing market share and its resilience in the face of economic downturns provide an attractive upside. While growth may moderate in the short term, demand for rental equipment remains healthy, in my opinion. Margin compression is expected as growth slows, but earnings and margins should improve as growth returns. The net debt position poses some risk, but expected EBITDA growth should help lower the debt ratio.

For further details see:

Ashtead Group: Upside Remains Attractive Despite Possible Near-Term Slowdown