ASHTF - Ashtead: Strong Performance But Risks Ahead

2023-05-26 06:13:52 ET

Summary

- Industrial equipment supplier, Ashtead, has seen an expected drop in share price. But does it mean a bigger drop ahead?

- There's no denying the company's robust fundamentals, but the US construction sector is facing uncertainties with a drop in leading indicators, tighter lending standards, and the US debt ceiling situation.

- ASHTF's long-term returns are strong, but I'd wait until the current uncertainties blow over before buying it. If for no reason other, a chance of buying it at lower price.

Since I last wrote about the industrial equipment supplier Ashtead (ASHTF) in February, it was and remains a fundamentally solid company. However, I had anticipated a near-term dip in price, which has happened. Since that time, its price has dropped by 6.6% as I write and as a result, it is back to where it started this year. The question now is whether it will continue to drop further or if we can expect better times ahead for the stock or its ADRs.

There are two reasons why I expected a short-term dip in its price:

- First, analysts had expected revenue growth at 8.4% in FY24 (May 1, 2023-April 30, 2024), a dramatic drop from the 24.1% growth they expect for FY23 and the 25% revenue rise seen for the first nine months of FY23. This indicated the potential for more tempered investor expectations going forward.

- Second, its trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio was at 20.3x at the time, which was higher than its 10-year average P/E of 17.2x. This indicated the possibility of a 15% drop in price.

Since then, however, there are updates on both counts, which can give more insight into what's next for Ashtead.

Growth can slow down

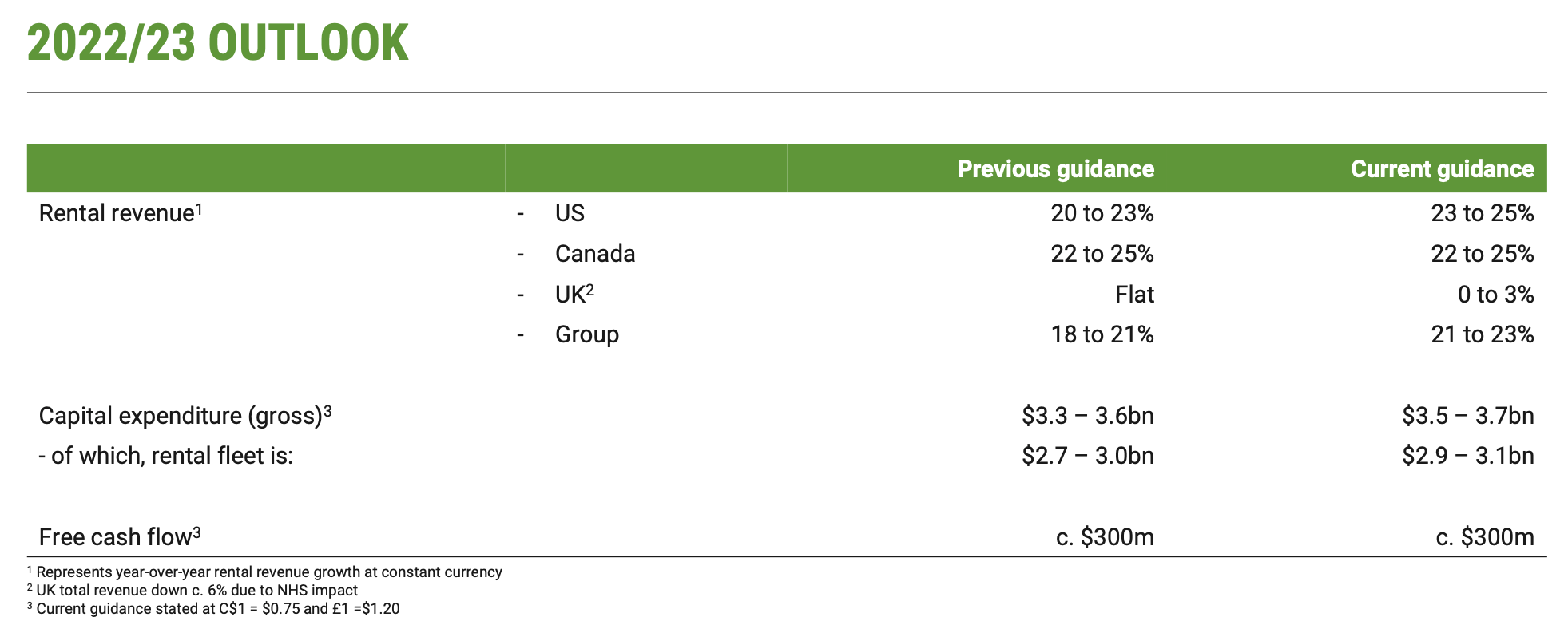

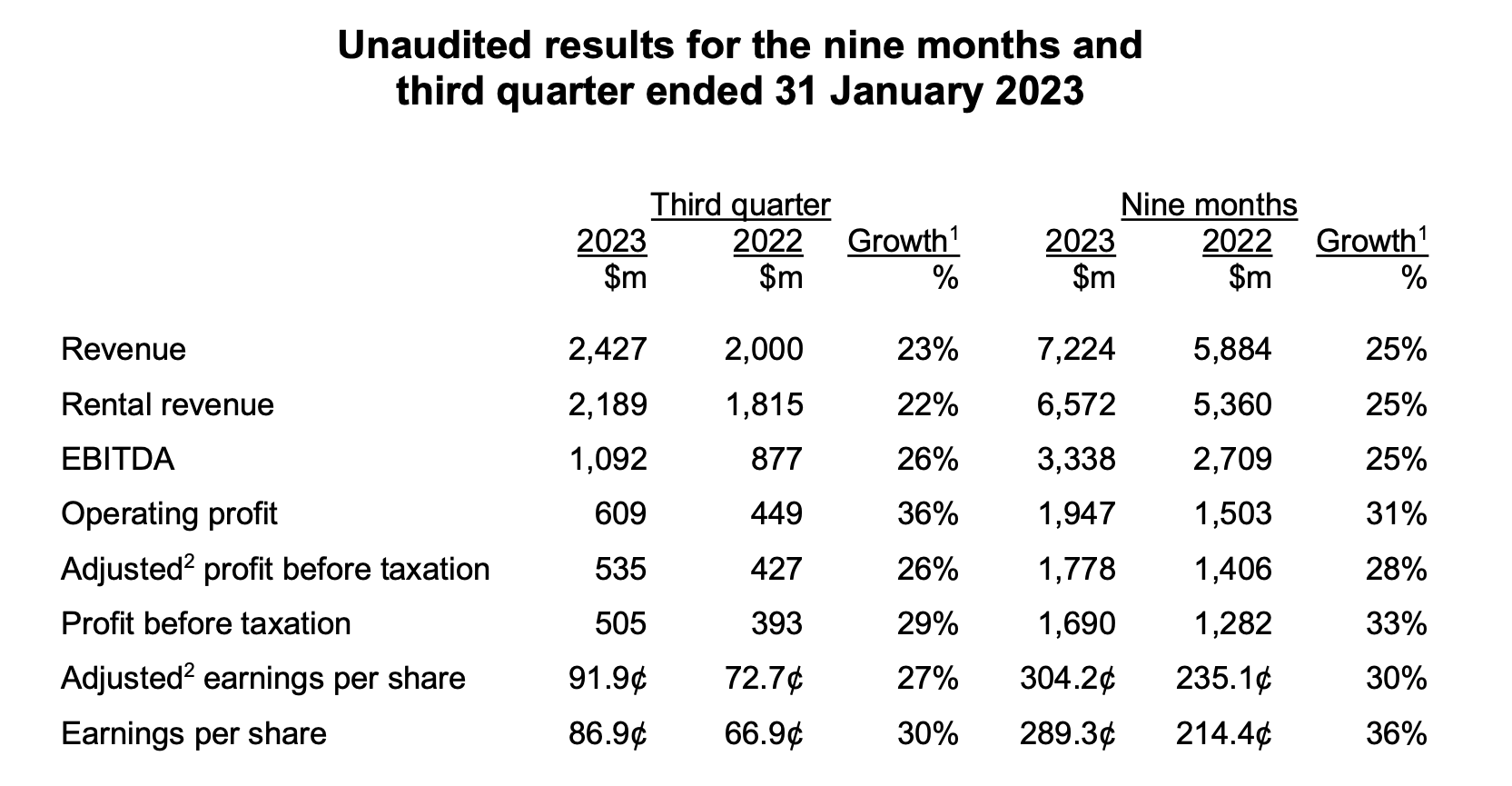

The first is its nine month update for FY23 (9M FY23), which showed robust growth. The company's revenues grew by 25% year-on-year (YoY), barely slowing down in the third quarter of the year (Q3 FY23). At 23%, Q3 FY23 revenue growth has more than met my forecast of at least 20% growth (see article linked above). Even at the time, it was obvious that the company could exceed expectations, and this point has been underlined by the fact that it has raised its guidance for FY23.

It now expects rental revenue, which accounts for most of the total revenues, to grow by 21% to 23% during the year, up from 18% to 21% earlier. Let me give some more context here. At the start of the financial year, Ashtead had pencilled in growth of 12% to 14% in the figure. It has come a long way since.

{kind=link}

Here's the rub, however. Even with the latest upgraded guidance, Q4 FY23 growth could slow down. If full year growth comes in at 22%, the midpoint of the guidance range, we get a Q4 growth rate of around 20%, which could be a sign of the start of slowing down in the company's strong growth. Further, FY24 growth is expected to be even more subdued. Likely because of the sustained strong numbers and improved guidance, analysts have increased their growth expectations, to be sure. They are now at 12.2% from the 8.4% when I last checked. At the same time, it is still a significant slowing down from FY23.

Further, the company's trailing twelve months [TTM] price-to-sales (P/S) ratio at 2.9x is higher than the historical level of 2.6x , indicating more correction in price in the short term.

Earnings indicate upside

Next, let's consider Ashtead from the earnings perspective. The company's earnings per share [EPS] were by a strong 36% for 9M FY23 and 30% for Q3 FY23. Its operating margin for 9M FY23 was also up to 27% compared to 25.5% for the same period in FY22, despite, as it points out "supply chain constraints, inflation and labour scarcity".

{kind=link}

Interestingly though, the company's trailing twelve months [TTM] reported or GAAP price-to-earnings (P/E) ratio is down to 17.3x from 20.3x at the last check. It is now trading below its 10-year median P/E of 17.6x. Further, it continues to trade at a lower ratio than the industrial sector, which is now at 18.3x. Contrary to the implication from the P/S, this indicates a small upside.

Consider the US construction sector

Finally, let's look at the outlook for the US construction sector since the last update. Recall that it has been a big reason for the optimism around companies like Ashtead, given the big policy push to infrastructure creation in the US. As the company mentions in its latest earnings presentation "Construction projects from the Infrastructure, CHIPS and Inflation Reduction Acts favour rental and the larger rental companies in particular".

However, the Dodge Momentum Index [DMI], a leading indicator for the US construction industry that Ashtead likes to reference in its earnings presentations, is showing signs of weakness. It declined by 5.1% month-on-month in April, the third monthly decline in the first four months of 2023. It does need to be noted that the DMI is coming off an all-time high in November 2022, and is down by 16% since. The index is still up by 11% YoY in April, which makes the Dodge Construction Network hopeful of a return to growth in 2024.

Source: Dodge Construction Network

Still, this is a need for caution here, particularly as the recent banking crisis has resulted in a tightening of lending standards. Further, there is a new concern around the US debt ceiling breach. The debt ceiling is the maximum permissible amount that the government can borrow before Congress takes a vote increasing it or not. The deadline is fast approaching in June, and if no decision is reached there could be adverse economic consequences, and of course, it has implications for the construction sector too.

In total, this means that from a sectoral perspective, the odds which were heavily in favour at the start of the year have swung against it now.

What next?

In sum, it looks like Ashtead is fairly valued for now according to me. It is indeed trading at a lower P/E compared to the industrials sector, but I believe that is for good reasons of risks to the construction sector. It is still a good long-term buy, going by its robust price performance, supported by sustained improvement in fundamentals over time, but for now there are definitely potential challenges ahead. These could reflect on its price, and for that reason I am going with a Hold rating on it, until the situation around the US construction sector becomes clearer.

For further details see:

Ashtead: Strong Performance But Risks Ahead