TAK - ASKA Pharmaceutical: EV Compressed By Ignored Non-Operating Assets

2023-07-31 09:00:00 ET

Summary

- ASKA Pharmaceuticals' market cap is covered 30% by net non-operating assets that render its EV/EBITDA multiple too low for a growing generics business in Japan.

- It has a growing exposure to gynecological drugs, which in some cases are receiving beneficial copayment terms from the NHI in order to support women's health and fertility in Japan.

- The NHI price cuts that can happen after annual reviews in drug prices are secularly going to target fewer and fewer drugs, with more being left relatively alone.

- As a Japanese generics company with meaningful capital reserves, they have a lot of reinvestment opportunities in manufacturing facilities, biosimilars and international expansion.

- While there could be some softness in the feed additives business, we think their gynecological portfolio will manage to offset any negative effects and drive growth from a <4x EV/EBITDA multiple. Clear buy.

ASKA Pharmaceutical (TYO:4886) is another unreasonably cheap Japanese idea in a similar vertical to other generics stocks from Japan we've written about on SA, with ASKA being larger among them.

It is listed on the Prime Market of the Tokyo Stock Exchange and can be purchased directly on Japanese exchanges through leading platforms like IBKR with plentiful daily liquidity averaging over $500k over meaningful historical stretches. There may be better options for how to buy the stock for US investors. We are not US investors, and only mention availability on IBKR because we personally use IBKR and know Americans who use it and have access to this stock through the platform. Needless to say, investigate for yourself and do your own due diligence to find access to this business' stock and on liquidity conditions for the stock.

Trading at a compressed PE and an even more compressed EV/EBITDA, its pricing doesn't reflect pretty solid business conditions, where being substantially a generics company in Japan actually comes with meaningful advantages and much less business volatility than generics in other countries. Moreover, they have new medicines in the pipeline that are very likely to offset declines in some areas due to pricing pressure from the NHI, and these medicines are focused in gynecology, which is probably the best place to be in Japanese drug markets since the NHI has begun with infertility treatments to subsidise women's health products by increasing national insurance coverage to attack the Japanese fertility problem. The other business they're in which is veterinary pharmaceuticals and feed additives should benefit from food security concerns that are arising just now. With about 30% of the market cap covered by non-operating assets and various options for how that needle-moving cash balance can be put to work, we think ASKA is a clear buy at less than 10x PE and an EV/EBITDA at around 3.7x.

Quick Note on the Generics Business in Japan

It's worth discussing how pricing works in the Japanese healthcare system. Essentially, manufacturers are able to sell to institutions on a relatively free market basis, but every year the NHI (which is the national health insurance institution in Japan) surveys what the prices end up being at pharmacies in hospitals and compare that to the mandated NHI price. If it's too different, then the NHI intervenes and forces price decreases by manufacturers which cuts into the profits on the product.

The NHI mandated price is determined by a host of factors. For new and innovative products, premiums are given and pricing is made so that it is in line with prices in other comparable markets like Europe if there are direct comps for the drugs. Once a drug goes off the equivalent in Japan of the 'patent period', the NHI starts reducing the insured price to enact what usually ends up looking like a generics cliff that you'd get in the US but smoothed out over several years.

Because the market isn't that competitive in Japan, it is often the case that off patent branded drugs don't become attacked by generics competition even years after patent expiration and can sell for prolonged periods of time at prices comparable to where they sold when they were on patent. With annual surveys (used to be every two years only until a couple of years ago) and downward revisions of the price, these drugs have been hit hard and have been priced down more consistently with no space to have their price float back up according to market forces. If there isn't a lot of generics competition around a particular drug, some exceptional price cuts become applied to the NHI price. A healthy decline in a generic's price will be annual declines in price of around 6% or so. Definitely not the sort of 80% declines you see in the US the moment a patent is over.

Again, the NHI price is a standard that ends up anchoring prices of drugs, but during the year the price can float away from the NHI price depending on free market factors and what products medical institutions might demand. Also being a new generic product on the market is not a bad thing. Since the markets aren't that competitive and government stakeholders want more generics competition, there is usually the setup for your generic product to take substantial share.

In Japanese generics markets you have generics drugs, branded patented drugs, off patent branded drugs and authorised generics or AG, which is a drug that is produced by the same company that produces the branded version (with the exact same formulation) but under a generic name in order to pre-empt generic competition and defend market share before the patent on the branded version is expired.

The situation for most generics is pretty non-volatile. Prices fall by an average of a few percent, like 5%, every year. Only really ensconced branded but off patent drugs have been at risk lately, with Pfizer's ( PFE ) Vyndaqel having seen more than a 70% decrease in price, an example of what happens to a drug if it's been benefiting from an extraordinary period of lacking competition despite being off patent. The reality is that as time passes and as the annual price reviews set into the markets, the proportion of products that get hit by price decreases will fall, even as discrepancy rates from the NHI mandated prices become stricter. Discrepancy rates went from 8% to 7% from 2021 to 2023 and the proportion of drugs facing cuts fell from 69% to 48%. With the annual reviews now in place, things will likely fall further as drug prices will be unable to float away from NHI mandates as meaningfully as before. Companies like ASKA that already have demonstrated limited NHI declines will likely continue to demonstrate limited instances of running afoul the NHI mandated price on the free market. The big hits to price will be increasingly reserved for the cases like Vyndaqel, which will also become more infrequent.

A thing to note about Japan is the strategy to find new indications. Finding new indications helps to extend the exclusivity period on top of being able to find new markets. It is a very important consideration for the ROI on drug development, comparatively more important in Japan than in other markets.

The final thing to note about Japan is that drugs are paid for on a co-payment basis with the NHI which insures the drug. The split is standardised, but if the Japanese government and NHI system want to promote a certain drug or class of drugs, it can change the ratios to subsidise consumption. This is what is happening with infertility medicines as Japan hopes fewer barriers to access these treatments will improve fertility outcomes for Japan. ASKA has meaningful exposure to gynecological medicines, which might be favourably covered by the insurance scheme or are at low penetration compared to Western countries, and the drugs in the pipeline are focused on this market.

ASKA Pharmaceutical Products

Here are the main products in the non-veterinary businesses.

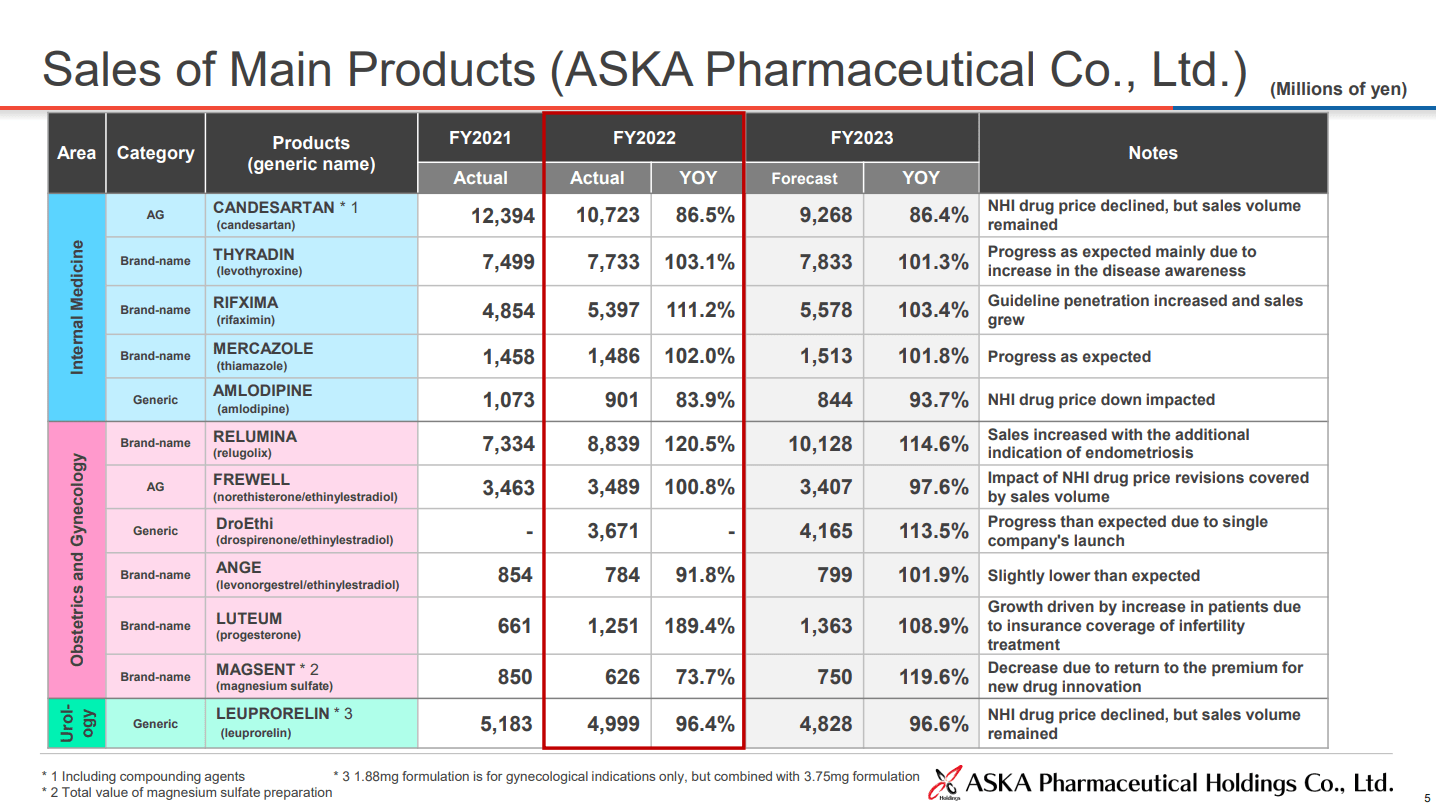

Non-veterinary Products (FY 2022 Pres)

{kind=link}

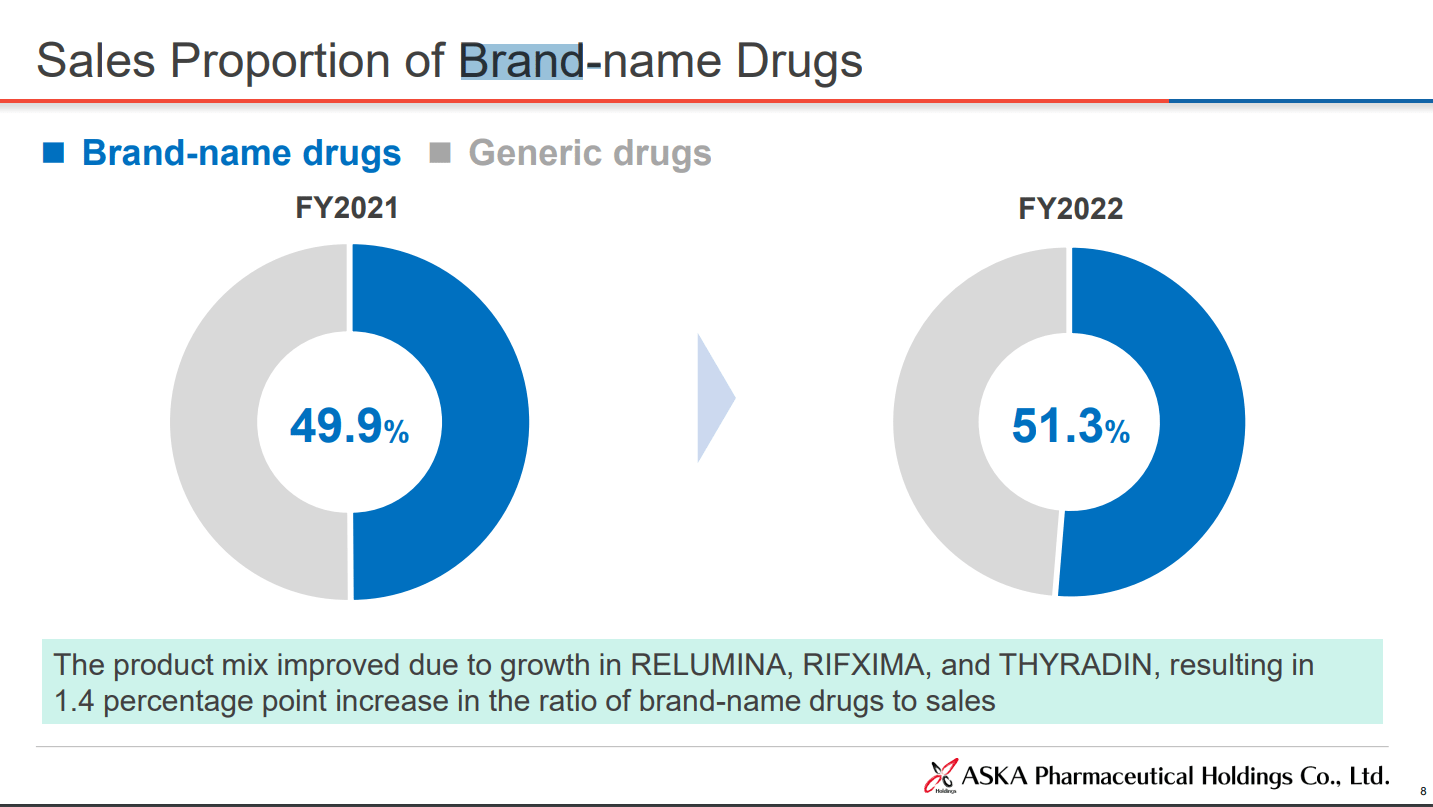

The designations show that the majority of products are actually brand name and/or not under current NHI pricing pressure. THYRADIN is a really old drug that has plateaued out, even though it is still sold under its brand name, and is not exclusive. RELUMINA, which is a major force in the gynecological portfolio being developed between Takeda ( TAK ) and ASKA, is exclusive.

Brand Name vs AG and Generics (FY 2022 Pres)

{kind=link}

As far as we understood, given the launch times of the brand name drugs, it should be more than 10 years before more of the major products go off patent. So for now the pressure is relatively predictable and isolated to FREWELL (5% of sales) and CANDESARTAN (over 10% of sales) which are receiving pressure in the form of lower prices and unit economics from the NHI pricing initiatives. However, FREWELL is benefiting from copayment subsidies as are other drugs in the gynecological portfolio. So really, it's only CANDESARTAN that needs to be tracked for notable declines.

The internal medicines are less exciting. Two are eroding due to NHI pricing pressure, but the rest are forecast to be pretty stable and are in pretty typical thyroid treatment medication, where THYRADIN is being given a marketing push as thyroid conditions are apparently under-diagnosed in Japan, and CANDESARTAN is a high blood pressure treatment. RIFXIMA was in-licensed from an Italian company and launched in 2016 as a broad spectrum antibiotic. It is unremarkable but growing slightly.

LEUPRORELIN (8% of sales) is used for several things in gynecology, including treating uterine fibroids, but it is labeled as a urological treatment because it's used in various other things as well including the treatment of prostate cancer.

The interesting products are all in the gynecological portfolio. While the other treatment areas covered by ASKA are pretty stable, the gynecological portfolio is experiencing a major push since purchase of some products by retail customers is being subsidised by the co-payment system. Better and arguably fairer access to women's health products might help with Japan's fertility crisis, and LUTEUM (2.5% of sales) revenues almost doubled becoming a more major component of ASKA's sales thanks to NHI copayment support to infertility treatments. FREWELL for dysmenorrhea, otherwise under NHI pricing pressure, benefits from an attractive reimbursement rate as well in Japan. In Phase III is a contraceptive which will be released more or less at the same time as competitor Fuji Pharma's contraceptive treatment, and is still an underpenetrated and small market in Japan, about a quarter of the size of the dysmenorrhea market.

RELUMINA (just under 10% of sales and growing) is the most important gynecological drug for uterine fibroids as the first indication also recently indicated for endometriosis. The new indication for endometriosis adds about 50% to the TAM of the drug, and is the area where volumes are increasing the most. RELUMINA's large share in gynecology should be able to offset declines in CANDESARTAN. NHI supported LUTEUM and the new DroEthi (already 5% of sales) launch will offset the rest and then some. ASKA is very likely to achieve net sales and operating profit growth before even the launch of their contraceptive medicine which is nearing the end of trials, as well as the adhesion barrier product in Phase III which will have a nice surgical process market, beginning in gynecology and gastroenterology.

The last thing to mention are the veterinary products. 72% of this segment, which in turn represents about 10% of ASKA's overall sales, is in feed additives and mixed feed. The rest is in livestock pharmaceuticals. Feed is an important and strategic market, and in our coverage we see that feed prices remain elevated . ASKA has foreseen some softening in this market because capacity has come online in other countries who export to Japan. However, we think that there is a high probability that this division overperforms forecasts, as these products are necessities are supplies have been hit again as Russia targets grain siloes and abandons the grain deal to put pressure again on grain-based feed supply. Scarcity should enable ASKA to wedge in higher prices and get more value out of its additives. We don't think incremental pressure on this segment will materialise that much, and the animal health business won't drag on results as food and food supply create price uplift.

Non-operating Assets and Valuation

ASKA has everything in place to transition away from some of the declining products to those with more potential in gynecology, which has scope to receive further attention from the NHI in the form of greater insurance coverage, as the issue of better access to female health products may become central in eliminating factors that might be dissuading childbearing in Japan. New products on the horizon also help to keep sales and profit growth coming. Furthermore, the end of inflation should take the pressure of generics companies in the form of lower costs in active pharmaceutical ingredients, which have joined a host of products in experiencing quite severe inflation.

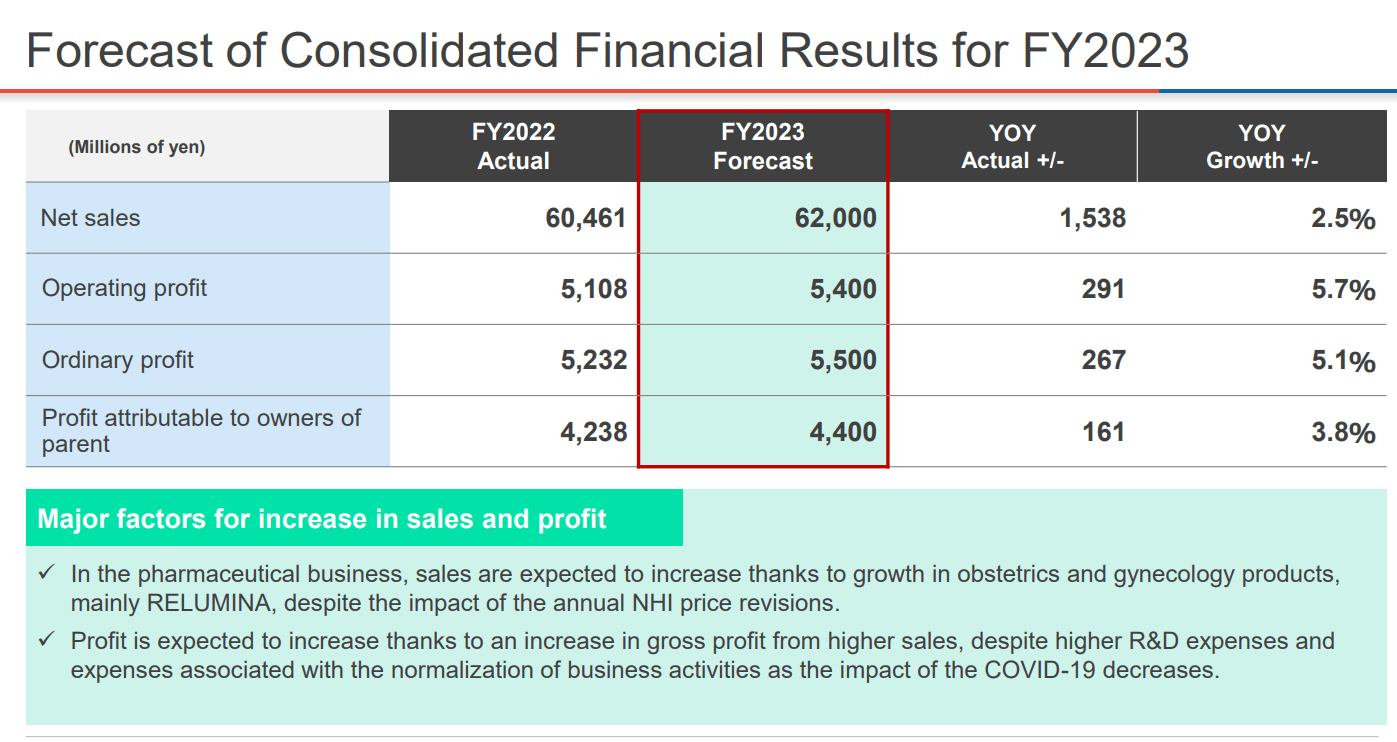

Financial Forecasts (FY 2022 Pres)

{kind=link}

But the greatest sign of continued earnings growth to trounce markets who've priced ASKA at less than 10x PE and less than 4x EV/EBITDA is that massive optionality afforded by a currently unused balance of non-operating assets. While these non-operating asset balances are often cordoned away from shareholders due to overly conservative Japanese managers, in this case there is plenty of precedent in similar companies putting this cash to a use that is highly likely to generate incremental profit growth that warrants repricing.

Fuji Pharma , a relatively close competitor to ASKA, used to have a large non-operating balance until it spent it on an important intangible asset, a distributorship, in order to reap the full upside of an undisclosed biosimilar that they plan to release to the Japanese market sometime in the next couple of years. Fuji Pharma also used some cash to expand facilities in order to have the capacity to handle more contract manufacturing engagements that it might get from companies wanting to get in on expanding parts of the Japanese pharmaceutical markets, like women's health.

ASKA already has paid for distributorships in the past, but a couple of very valuable distributorships could be bought from other drug developers with the 14 billion Yen they have lying around. Considering the ROIs on something like a biosimilar distributorship, something like 2 billion in annual profits could be added to the bottom line, if we're using biologics as a baseline which is what Fuji invested in. That could mean something like a 50% boost to current profits, which is very needle-moving. If you just assume returns equivalent to the company's current earnings yield from the 10x PE of 10%, then we're looking at a potential 28% increase in profits.

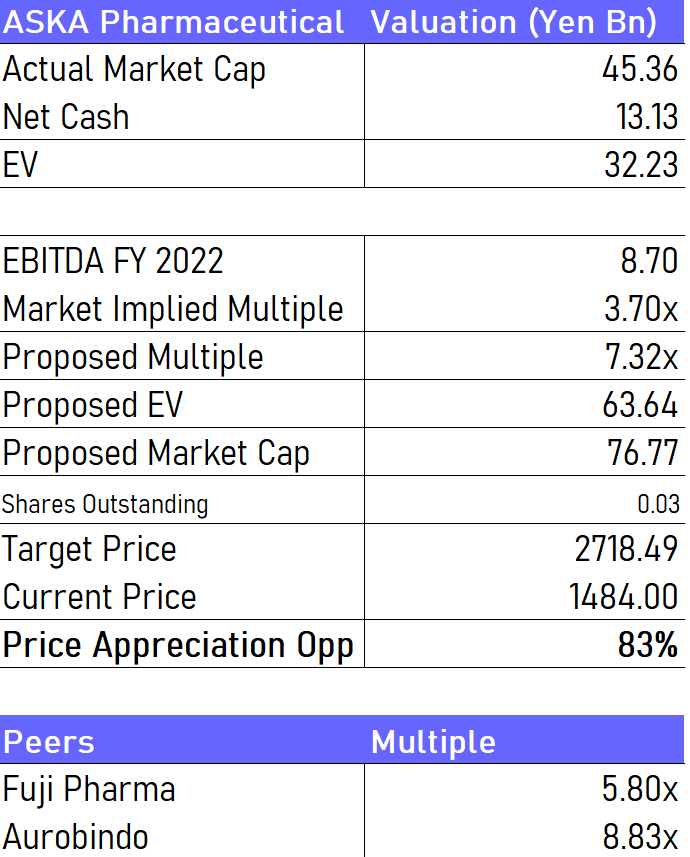

Taking the net cash equivalent value of the non-operating assets invested in some non-strategic securities, we get the following for the valuation. The peers are Fuji Pharma, which is the closest peer, as well as Aurobindo which is another consistently growing generics company with a higher valuation.

{kind=link}

This passes the sanity test. Assuming, as is often the case, that markets are currently ignoring the non-operating balance, if it were to be invested to produce 30% profit growth and then the current PE would be applied to ASKA again at that higher earnings figure, the upside would be at least 30%. Considering that growth usually conditions markets into applying a more reasonable, higher multiple, that upside only grows. At any rate, the valuation above is already very conservative, since we are ultimately dealing with pure, cash-equivalent value on the balance sheet that is compressing EV figures.

Bottom Line

Ultimately, value is determined by reinvestment opportunities. ASKA is already cash generative, with about 50% FCF conversion from EBIT and decent margins a little below 10%. Most importantly, it has a massive, easy to liquidate non-operating balance with precedents from close peers doing so in order to expand their businesses. These reinvestments in markets like gynecology (which is low penetration in Japan) or other markets that have good prospects in ASKA's domestic market could quite easily generate earnings growth. With a substantial cash balance that covers 30% of market cap, even a relatively weak ROI outcome will still meaningfully move the needle in terms of profits, on top of the growth already being achieved by ASKA's products in the pipeline and their current running portfolio.

With generics markets in Japan being relatively stable and with Japanese healthcare costs already being in the lower quartiles by country, there isn't much scope for further or dramatic 'stroke of the pen' risks. In fact, ASKA is probably more likely to benefit from unexpected regulatory change since fertility is a strategic Japanese concern, and almost half of ASKA's business is exposed to women's health products. A growing, solid company with good prospects in a recession resistant industry like healthcare is a clear buy at a multiple below 4x EV/EBITDA.

For further details see:

ASKA Pharmaceutical: EV Compressed By Ignored Non-Operating Assets