ASMXF - ASM International: A Solid Backlog And Growth Potential

2023-07-27 22:16:14 ET

Summary

- ASM International reported a solid Q2 performance with resilient growth and a strong backlog in a challenging semiconductor industry. Yet, order intake continued to slow down significantly.

- The company is well-positioned for impressive growth opportunities in fast-growing semiconductor technologies like silicon carbide (SiC) and Epitaxy.

- The impact of Chinese export restrictions by the US has had a lesser impact than anticipated, decreasing a significant risk in the longer term.

- Despite declining order intake and lower revenue growth expected in the second half of the year, ASMI's sound financial position and market positioning support steady growth in the long term.

Investment thesis

I maintain my Hold rating on ASM International NV ( ASMIY ) and update my revenue and EPS estimates following the company’s Q2 results, which showed another resilient performance but a decreasing order intake. In addition, ASMI is guiding for a significant revenue growth decline in the second half of the year as the weakness for foundry/logic and memory customers remains.

Recent financial results for Q2 have shown that the impact of Chinese export restrictions was not as severe as expected, and ASMI continues to enjoy solid demand for its products. While revenue growth has slowed down from previous quarters, the company's backlog remains respectable, providing a buffer against the current industry weakness.

ASMI's exposure to fast-growing semiconductor technologies like silicon carbide (SiC) and Epitaxy positions the company for impressive growth opportunities. With a significant market share in the SiC equipment market, ASMI is well-positioned to benefit from the expected 23.8% CAGR in the SiC industry through 2030. Additionally, its foothold in the Epitaxy market, projected to grow at a 20% CAGR through 2028, further bolsters its growth prospects. ASMI's diverse customer segments, particularly in Power/Analog and silicon carbide (SiC) technologies, should drive revenue growth, while its market position in atomic layer deposition ((ALD)) equipment remains a steady income source.

The company's sound financial position, minimal debt, and investments in future growth underscore its ability to weather industry challenges. Furthermore, based on the company's excellent Q2 results and the management's outlook, ASMI is expected to outperform the wafer fab equipment (WFE) market in 2023 and deliver steady revenue growth over the next few years. With a favorable market share expansion and technological advancements, ASMI is well-positioned for impressive growth throughout the decade.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

ASM International simply keeps on performing, protected by a strong backlog

I last covered ASM International in November when I rated the shares a hold due to the uncertainty surrounding the impact of Chinese export regulations and the already high valuation. Still, I concluded that ASMI was brilliantly positioned for extremely strong growth over the remainder of the decade.

Meanwhile, the last couple of months and last two financial releases from the company have shown that the impact of Chinese export restrictions was less than anticipated by me, analysts, and management itself. As a result, and due to solid continued demand for the company’s products, growth has remained impressive in a very challenging environment, including a cyclical downturn for the semiconductor industry. The company has consistently managed to keep growing at a rapid pace, and while growth may have been slowing down, it has held its backlog at a respectable level. It is, therefore, no surprise that the share price is up by over 70% since my last article, which is why it is about time to take a look at the company’s recent financial performance in order to find out whether shares are attractive following a massive share price jump yet combined with easing headwinds.

ASMI reported Q1 results earlier this week and the 7% jump in share price the following trading day might say it all. The company remains in excellent shape, outperforming most of its peers while investing in future growth. Yet, the first cracks as a result of a lower semiconductor demand are starting to appear.

Q1 revenue came in within the guided range by management but was below the expectations from Wall Street analysts. ASMI reported revenue of €669 million, below the €677 million consensus but still up 21% YoY. Reporting 21% top-line growth is, of course, nothing to complain about, yet it is essential to point out that growth has been slowing down significantly from the 42% growth reported in 4Q22 and 40% growth in Q1. At the same time, the company lapped a strong 2Q22 with 30% growth and still managed to report impressive growth, which is a testimony to the strong demand for its products, even as the semiconductor industry has been experiencing a significant slowdown over the last 12 months.

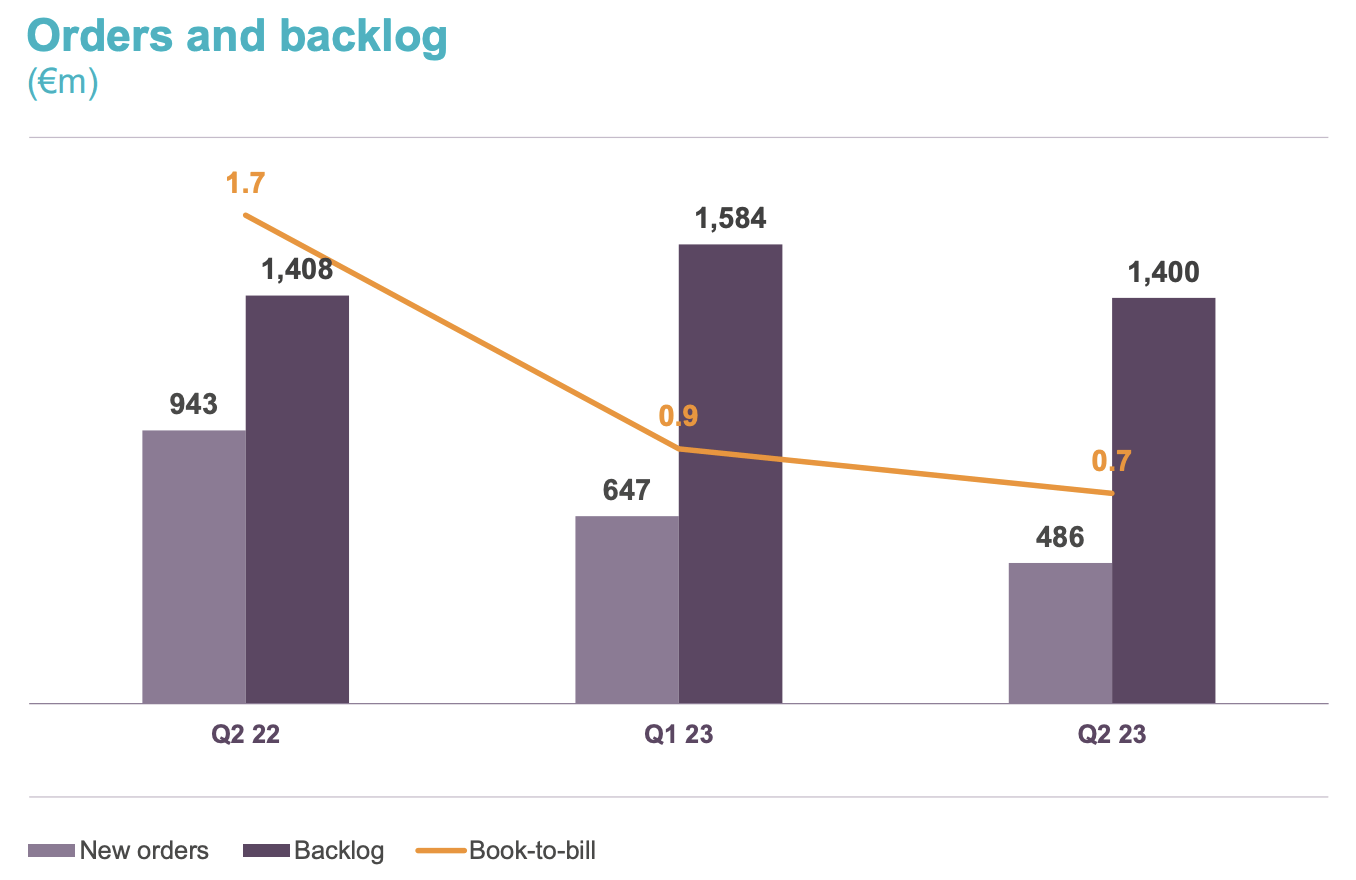

Even more important, the order intake has also been showing a substantial decline. In Q2, ASMI reported an order intake of €486 million, down a staggering 48% YoY and 24% sequentially. This is purely the result of more challenging market conditions, lower capex spending by customers, and orders being pushed out. The decline was driven by all customer segments and, crucially, does not come as a surprise. This downturn in order intake was long predicted as the lower demand for semiconductors after the COVID-19 boom would always result in decreased demand for capacity expansion. Luckily for ASMI, its order intake over recent years has been far above its capacity, resulting in a strong backlog that it can use to fuel its growth. In 2Q22, the book-to-bill stood at 1.7 and this has now fallen to 0.7 in Q2, which is still far from bad. In addition, the backlog still stands at a very solid €1.4 billion, only down a little under €200 million from last quarter. And with the semiconductor industry expected to gradually improve again in the second half of this year and into FY24, I don’t think ASMI investors have much to worry about as the continued “solid” (as opposed to stellar) order intake and impressive backlog should be enough to offset current industry weakness.

{kind=link}

Looking at the different customer segments, foundry continued to account for the largest share of revenue, and while this was down on a sequential basis due to a further slowdown in this industry, and a recovery staying out until later this year as guided for by TSMC ( TSM ), ASMI was still able to report a YoY increase in foundry revenues. The second-largest segment for ASMI last quarter was Power/Analog, which continued to see strong momentum as the Power semiconductor market remained incredibly strong, as highlighted by the strong results reported by Infineon ( IFNNY ). As demand in these sectors remains strong, this boosts demand for ASMI’s equipment to increase capacity. As a result, revenue from the power/analog segment, in combination with the wafer manufacturing business, more than doubled over the last 6 months and overtook revenue derived from memory, which continued to struggle. While revenue from memory did see a slight sequential increase, this remained down substantially YoY.

Overall, I believe we should see continued strength in Power semiconductor revenues for ASMI and a further slowdown in foundry in the second half of the year. Weakness in Memory and analog could persist a little longer, with a more powerful recovery by the start of 2024. This should mean business fundamentals for ASMI should also start improving by the start of FY24, with a higher order intake and accelerating top-line growth.

Moving to the bottom-line performance in Q1, the gross margin was 49%, down from 51.1% in Q1 but up from 47.5% in the same quarter last year. Overall, ASMI is able to maintain its strong margin profile and continues to report solid profits despite the cyclical downturn in the industry and the high levels of inflation witnessed over the last year. In Q2, the company reported an operating profit of €180 million, up 23% as the operating margin increased from 26.5% in 2Q22 to 26.9% in the latest quarter.

ASMI has a very healthy balance sheet with practically no debt and a solid cash position of €490 million, although this is down from €573 million at the end of Q1 due to increased investments and free cash flow. Also, the company returned a total of €183 million to shareholders through both dividends and share repurchases, which was not fully covered by the FCF of €86 million, down from €121 million one year ago.

The near-term headwinds driving a declining order intake should be seen as an opportunity instead of a negative

Despite the short-term headwinds impacting the business and causing a lower order intake, primarily driven by a decline in the logic/foundry and memory businesses, ASMI management continues to see relatively strong demand from these customers, especially in logic/foundry, as these remain committed to their technology roadmaps, keeping Capex plans fairly steady. In fact, a big cause for the decline in new orders is the delays in fab readiness due to a shortage of specialized personnel to get these new fabs operational. As manufacturers are unable to get these operational, these push-out equipment orders at the likes of ASMI. So, crucially, a large part of these orders is not lost but postponed, and these should nevertheless be realized over the next several years, boosting the longer-term outlook for ASMI. This is also why management remains committed to these industries despite the near-term cyclical impact.

Moreover, management believes it is well-positioned to take more market share once these industries recover. This is what management stated regarding the memory market rebound:

Nevertheless, we believe that we are well positioned for increased sales once the memory market recovers. We have strengthened our positions with High-K Metal Gate in DRAM as mentioned and with ALD gap fill in 3D NAND. We continue to work on additional new applications with the potential for further share of wallet gains in memory in the coming

Financially, the company remains in terrific shape, and although the order intake is now really dropping due to lower demand for semiconductors, the longer-term positioning of the company remains incredibly promising, and management seems to be able to look through the near-term decline and position itself favorably for market share gains once the market recovers.

ASMI is well-positioned for impressive growth

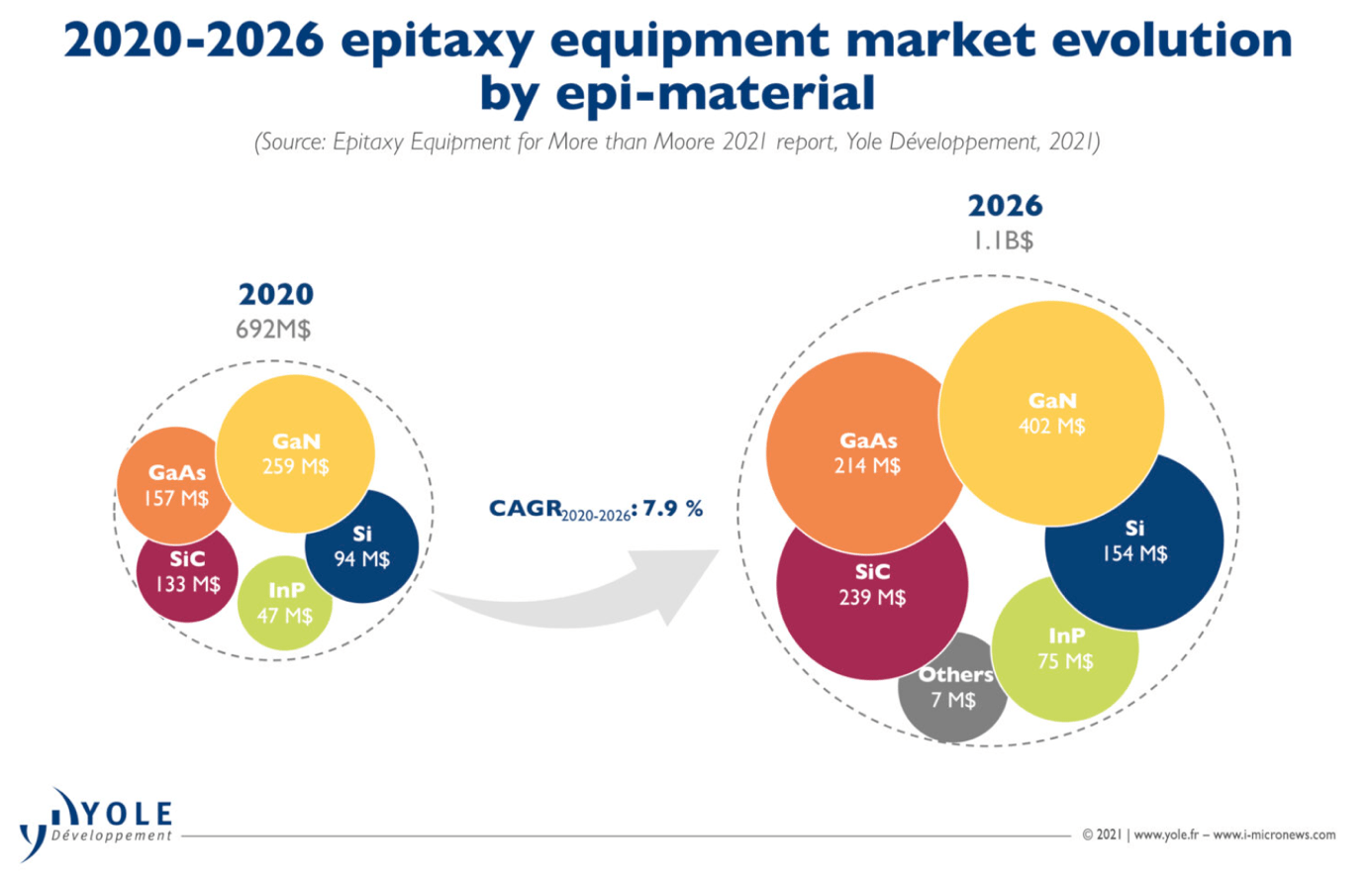

As mentioned before, management believes it should be well-positioned to benefit from a rebound in demand. Contributing to this is the company’s excellent exposure to fast-growing semiconductor technologies like silicon carbide (SiC) and Epitaxy. The company already holds a significant position in the SiC equipment market as, after the acquisition of LPE last year, its market share has grown to over 24% . And this is quite crucial for ASMI’s growth outlook as the SiC industry is expected to grow at a 23.8% CAGR through 2030, posing a massive growth opportunity for ASMI as one of the leading manufacturers of equipment for this technology. This is what management stated during the Q2 earnings call about increasing its SiC market share:

With a further increase expected in the second half, we are confident that our silicon carbide sales will increase to more than €130 million, as earlier communicated. We believe the film quality and cost of ownership offered by our silicon carbide Epi tools are among the best, if not the best, in the industry. The transition from 150-millimeters to 200-millimeter wafer size offers opportunities to step up our market share.

The acquisition of LPE last year also increased the company’s foothold in the Epitaxy market, a technology closely related and much used in SiC technology. Now, without getting too much into the technologies itself, it basically allows faster transistor switching at lower power, making it extremely useful for power semiconductors. This is why the technology is increasingly getting adopted across industries, driving an expected 20% CAGR through 2028.

{kind=link}

Meanwhile, the company also remains a leader in atomic layer deposition (ALD) equipment, a market expected to grow at a solid 8.2% CAGR through 2027. ALD equipment accounts for over half of ASMI’s sales, providing it with a solid and reliable income basis, in addition to the several higher growth opportunities discussed above.

While ASMI already has a strong foothold in all these industries, it plans to increase its market share over the next several years by leveraging the transition to gate-all-around, a new technology used to allow for faster and more power-efficient semiconductors. This new technology is key to realizing next-generation applications such as high-performance computing. Therefore, the adoption of this technology is expected to be huge, driving a 32.5% growth CAGR through 2029. This is what management said during the Q2 earnings call regarding its confidence in this transition:

We are confident that the transition to gate-all-around nanosheet technology will result in a meaningful double-digit increase in our served available market as ALD will be required for a growing number of critical deposition steps.

The impact of Chinese export restrictions should remain minimal

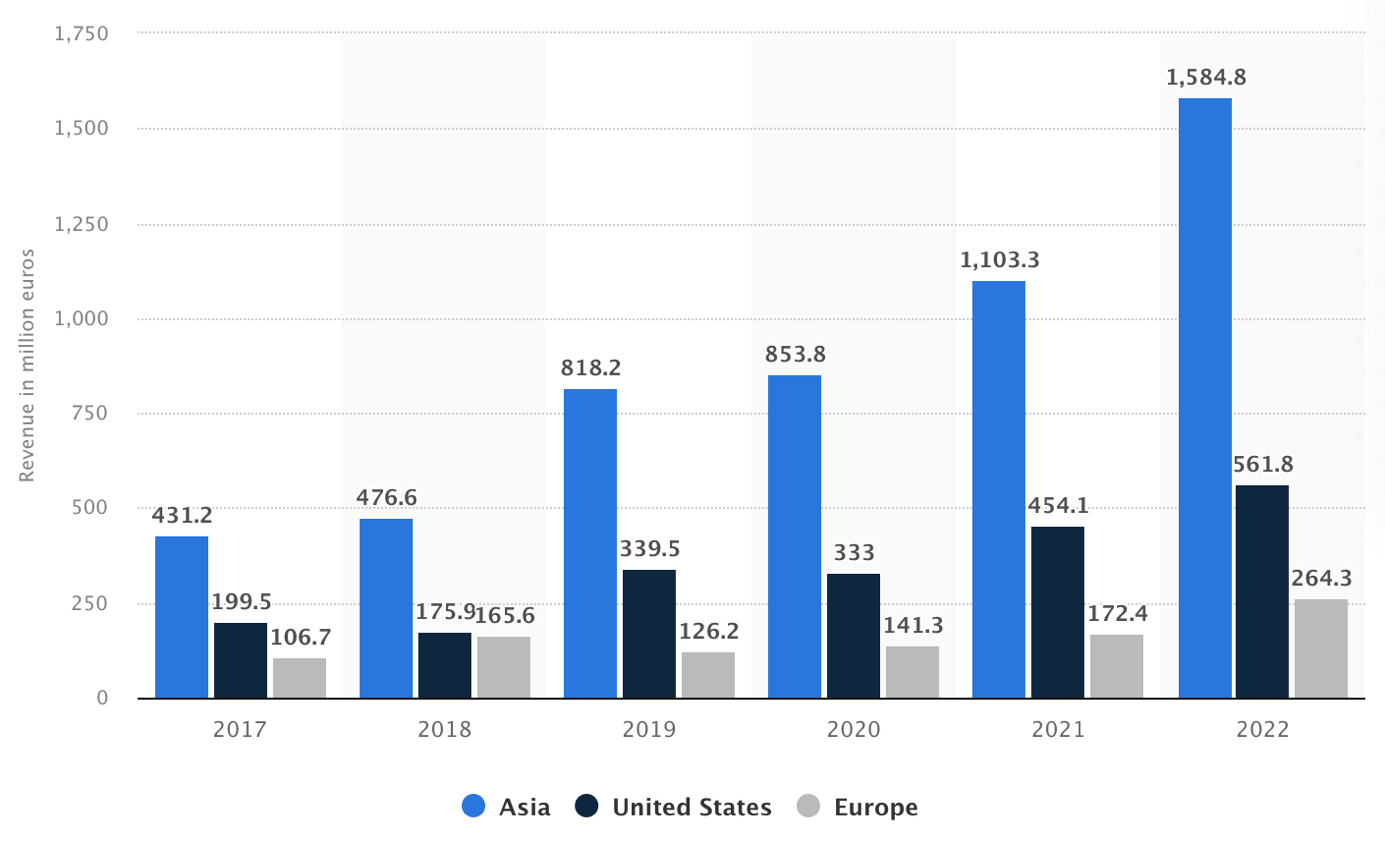

Like many of its semiconductor equipment peers, ASMI is heavily exposed to the Asia Pacific region in terms of revenue. In FY22, nearly 70% of its revenues were derived from Asia, with the US and Europe accounting for only slightly over 30%. Considering the tensions between China and the US, the possibility of a Chinese invasion of Taiwan, and the unpredictability of Asian governments, I view this exposure as somewhat of a risk.

ASMI's revenue by region (Statista)

{kind=link}

Positively, we should see the number of fabs in Europe and the US increase over the next several years, which should also mean that the revenue mix for ASMI should improve as more of its machines will need to be shipped to these new (Western) fabs.

Also, the impact of the Chinese export restrictions imposed by the US in October last year and the recently introduced restrictions from the Dutch and Japanese governments only had a minimal impact on growth for ASMI. As communicated late last year, the export restrictions will have an impact of 15% to 25% of China sales, or around 13% of total revenue at the midpoint of the range. So far, the impact has come in at the low end of the range due to Chinese customers redirecting their strategic investments towards less advanced nodes, which has allowed ASMI to largely fill in this loss. Overall, the result seems to sit below 10% of total revenue, which does not have to be viewed as a major issue. Clearly, the impact of these restrictions is lesser than anticipated, which allows for a higher valuation multiple due to decreased risks.

Outlook

For Q3, management has guided for revenue to come in between €580 million to €620 million, down 1.6% YoY and showing a significant growth slowdown compared to the 21% positive growth recorded in Q2. Furthermore, management expects revenue to be down 10% in the second half of the year compared to the first half due to weakness in memory, softening in logic/foundry, and a continued solid trend in power/analog. This lower revenue base should also negatively impact margins for ASMI as its investments remain high. Eventually, this should be closer to 26% for the full year. Meanwhile, the order intake is expected to remain weak in Q3 but the drop in orders is expected to be less pronounced compared to Q2 as Capex levels of manufacturers remain stable, but pushed-out orders remain a problem.

For FY23, management still expects to grow revenue by a single-digit percentage as growth is expected to slow down significantly in the second half of the year. According to Gartner , this would still mean that the company outperforms the wafer fab equipment (WFE) market as this is projected to decline by 14% in 2023.

ASMI also maintained its long-term outlook and still expects FY25 revenue of between €2.8 billion and €3.4 billion and a slightly higher gross margin of between 46% and 50%.

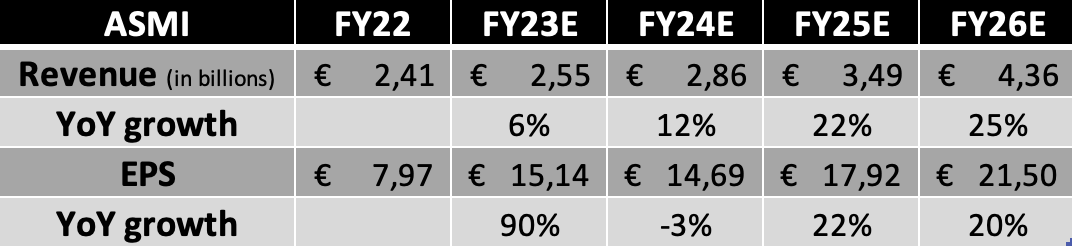

Following this outlook from management, the excellent Q2 results, and the lesser-than-expected impact of Chinese export restrictions, I now expect the following financial results until 2026.

Financial projections (Author)

{kind=link}

Shortly explaining these estimates, I expect ASMI to report FY23 revenue growth of 6% as I am predicting the second half of the year to be slightly more challenging than anticipated by management. As uncertainty is high, I choose to remain somewhat more conservative. Also, I am not expecting a massive acceleration in FY24 as the semiconductor industry is projected to gradually recover. With this recovery probably going relatively slow due to lasting economic headwinds and ASMI being slightly late cyclical, I expect ASMI to show a gradual recovery in FY24, with a more significant growth acceleration in FY25 and FY26. As the company remains very well positioned in its respective industries, it should see solid growth over the remainder of the decade. I even predict FY25 revenue to come in at the very high end of management’s guidance as I see meaningful market share expansion ahead for ASMI.

Meanwhile, EPS will fluctuate a lot due to inconsistent operating costs, in part due to changing investments from management. Therefore, these EPS estimates are susceptible to later changes as the trajectory and strategy from management becomes clearer.

Conclusion

ASM International continues to demonstrate its resilience and strong performance in the semiconductor industry. Despite facing challenges like Chinese export regulations and a cyclical downturn, ASMI has managed to maintain impressive growth and a solid backlog, which allows it to somewhat offset the expected weakness in the second half of the year.

The impact of Chinese export restrictions turned out to be less severe than anticipated, allowing the company to navigate through the challenges successfully. And although there have been recent declines in order intake due to market conditions and lower semiconductor demand, the company's strong backlog and strategic positioning bode well for future and near-term growth.

Overall, ASMI remains an excellent investment with the potential for significant returns. Its strong fundamentals, strategic positioning, and growth prospects in the semiconductor industry are plenty to be enthusiastic about. Yet, shares have become quite a bit more expensive than when I last covered the company in November. Back then, these were valued at 18.5x forward earnings, but this has now increased to 28.5x. Even when considering the company’s growth prospects, I believe shares are very richly priced right now. I believe a share price below €340 would offer a better margin of safety and better long-term returns. Therefore, I rate ASMI shares a Hold .

For further details see:

ASM International: A Solid Backlog And Growth Potential