ASML - ASM International: Growth Outlook Is Uncertain Due To Macroeconomic And Political Challenges

2023-10-27 14:03:51 ET

Summary

- ASMIY's third quarter performance showed a decline in revenue compared to the previous quarter.

- The semiconductor sector is facing challenges due to global economic stagnation and uncertainties, including rising interest rates and export controls.

- ASMIY's long-term outlook remains promising, but the current market slowdown and external challenges warrant caution.

Summary

This post is to provide an update on my thoughts on ASM International ( ASMIY ) third quarter results. In a prior post , I had recommended a hold rating for ASMIY, and I continue to uphold that rating. My decision is influenced by ASMIY's underwhelming third quarter performance, marked by a revenue decline compared to the preceding quarter. Furthermore, the global economic landscape is currently characterized by stagnation in major economies, with the upcoming year's economic projections being overshadowed by uncertainties, notably rising interest rates. This presents significant challenges for the semiconductor sector at large. Moreover, external political factors, such as export controls, are adversely affecting ASMIY's growth prospects. It remains unclear when these challenges will abate or if they might intensify, further complicating the outlook.

Investment thesis

In the third quarter, ASMIY reported a revenue of EUR622 million , marking a 9% increase year-on-year and a 6% decrease from the previous quarter. This performance met the upper end of their guidance, which ranged from EUR580 million to EUR620 million. The spares and services segment experienced notable growth, with an 18% increase in constant currencies. Equipment revenue also saw a rise, with an 8% year-on-year increase. When breaking down revenue by customer segment, the foundry led the way, followed by logic, and then power/analog and memory. The company's gross margin for the third quarter stood at 48.9%, showing an improvement from 48.1% in the same quarter of the previous year. SG&A expenses witnessed a 6% year-on-year increase and a 4% rise from the second quarter. Net R&D expenses surged by 70% compared to the previous year. The operating profit margin for the third quarter was reported at 25.3%. For the entirety of 2023, the company now projects an operating margin of at least 26%.

Amidst the backdrop of economic uncertainty and softer end-market trends, ASMIY delivered a robust performance in the third quarter. Major economies are witnessing sluggish growth, and the economic forecast for the upcoming year remains clouded with uncertainties. Factors such as rising interest rates, concerns over consumer spending, and geopolitical tensions are contributing to this uncertain outlook. Some end markets seem to be nearing the bottom of their cycle, as indicated by stabilizing demand and gradual improvements in inventories. However, the exact timing and strength of a potential recovery remain elusive.

In response to these market conditions, many customers have opted to reduce their capital spending budgets and decelerate their capacity expansion initiatives. In the logic/foundry segment, leading-edge spending has shown resilience, albeit with reductions, especially when compared to more significant cuts in the memory segment. These reductions are partly due to delays in the readiness of new fabrication plants, and also because of the prevailing end market weakness. However, this has been counterbalanced by significant growth from a lower base in 2022 in the mature logic/foundry business, predominantly in China.

Post the U.S. export controls introduced in the previous year, several Chinese customers have shifted their investments towards more mature nodes. Even though ASMIY's stronghold in these nodes isn't as pronounced as in the advanced nodes, they still have some applications and exposure in the mature logic/foundry segment, which has seen a significant uptick this year. Despite the current market challenges, the silver lining is that leading logic/foundry customers continue to adhere to their technological roadmaps. The transition to the gate-all-around node is anticipated to commence in high-volume manufacturing by 2025, which is expected to further boost ASMIY's market share in both their ALD and Epi segments.

The power/analog wafer segment has been a primary growth driver for ASMIY this year. Sales in this segment have more than doubled year-to-date, with silicon carbide demand remaining robust. The memory market, on the other hand, continues to grapple with overcapacity, implying that a more substantial recovery in end markets is essential before customers commit to significant new capacity expansions. However, the demand for high-performance DRAM, especially related to AI and the transition to DDR5, offers a glimmer of hope.

For the fourth quarter, the company projects a revenue range of EUR600 million to EUR640 million. This implies stable sales when compared to the third quarter. For the entire year, ASMIY anticipates revenue growth close to 10%, inclusive of the consolidation of LPE. Despite the current market slowdown, the long-term outlook for ASMIY remains promising, with the company set on a trajectory of healthy double-digit growth over the next half-decade.

Valuation

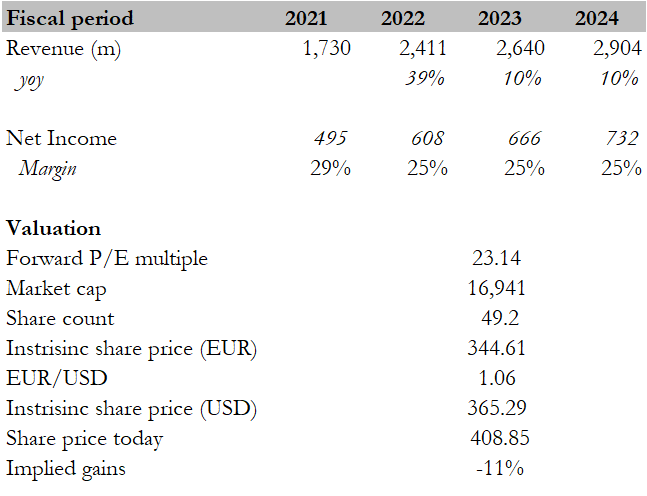

My target price for ASMIY based on my model is ~$365. My assumptions are grounded in several factors stemming from ASMIY's recent performance. The third quarter revealed a slight decline in revenue compared to the prior quarter, suggesting potential vulnerabilities. The spares and services segment showed growth, and the equipment revenue segment also trended upwards. However, a broader perspective reveals challenges, especially in the memory market, which is grappling with overcapacity. The global economic environment is marked by uncertainties, tepid growth in major economies, and geopolitical concerns, all of which could influence ASMIY's direction. Recent U.S. export controls have prompted a shift in investment strategies among Chinese customers. While ASMIY has a presence in the mature logic/foundry sector, their influence isn't as pronounced in the advanced nodes. ASMIY's revenue projection for the upcoming quarter indicates 10% growth, suggesting stability but not a significant rise compared to the previous year. The long-term outlook, while optimistic on the surface, is tempered by the current market slowdown and external challenges. The memory market continues to face hurdles, but there's potential in high-performance DRAM. The anticipated transition to new technological nodes in the near future offers growth opportunities, but these shifts come with their own set of uncertainties. Therefore, my assumptions for FY23 are derived from the guidance provided by the management during the earnings call, leaning towards the higher end of the range. Considering the prevailing uncertainties in the semiconductor sector, I've projected 10% growth for FY24 to maintain a conservative stance.

{kind=link}

Peers of ASMIY include ASML Holding , Aixtron , BE Semiconductor Industries , Siltronic , and X-Fab Silicon Foundries . The median forward P/E multiple among these peers stands at approximately 21x. Their median projected growth rate for the next twelve months [NTM] from 2024 over 2023 is 14%, and the median Debt to Equity ratio is 30.75x. In contrast, ASMIY's forward P/E is approximately 23x, with a growth rate of 15% and a Debt to Equity ratio of 0.68, essentially making it debt-free. ASMIY's higher forward P/E compared to its peers can be attributed to its higher growth rate and its exceptionally robust balance sheet, characterized by minimal debt. This strength is particularly commendable given the challenges in the semiconductor industry and macroeconomic factors like rising interest rates. Looking ahead, while the future of the semiconductor sector remains clouded in uncertainty, there's a clear assurance in ASMIY's balance sheet strength, positioning it well to weather potential interest rate shocks. Based on my target share price for ASMIY, I maintain my hold rating for the company.

Risk

A potential upside to my hold rating is an improving macroeconomic outlook. As inflation eases, interest rates are likely to decrease in tandem. This reduction in interest rates can stimulate economic growth by encouraging consumer spending. With a brighter economic landscape, businesses will be motivated to expand, leading to increased demand for semiconductors, given their integral role in the modern economy.

Conclusion

Based on my analysis of ASMIY's third quarter performance, considering ASMIY's recent performance weakness and the broader challenges in the semiconductor sector, while certain segments like spares and services have shown growth, the memory market's overcapacity and global economic uncertainties cast shadows on the company's trajectory. Additionally, geopolitical factors, such as U.S. export controls, have influenced investment behaviors, especially among Chinese customers. Although ASMIY's projected growth and robust balance sheet, characterized by minimal debt, stand out positively against its peers, the overall semiconductor industry's uncertain future and macroeconomic challenges warrant caution. Given these mixed indicators and with my target price below its current trading price, I maintain a hold rating for ASMIY.

For further details see:

ASM International: Growth Outlook Is Uncertain Due To Macroeconomic And Political Challenges