ASMXF - ASM International: Q3 Impacted By China Restrictions

Summary

- ASM International NV reported strong Q3 results and achieved record high revenue.

- ASM International is being affected by China restrictions from the US and had to adjust its income expectations.

- The company has improved its balance sheet and ASM International financials remain strong.

- The long-term outlook remains unchanged for ASM International, but the recent increase in share price and economic uncertainties are a drag on the company.

Just 2 weeks back I wrote my initial thesis on ASM International NV ( ASMIY ) (which you may find here ), and I recommended buying the company because of strong growth prospects and the recent stock weakness opening up a great opportunity for strong returns. Now, two weeks later, the company just reported its 3Q22 earnings , and they did not disappoint. The stock price also did not disappoint over the last 2 weeks, since it increased by over 10% at the time of writing this article (after the big loss at the opening the day after the report).

In this article, I will review the quarterly earnings report just published and see whether I still think the stock is a buy.

Financial results

This is what I wrote about the outlook two weeks ago:

In a couple of weeks, ASM will report its 3Q22 earnings. During the last earnings call, management remained positive. They projected supply chain problems to remain challenging and expect revenue to come in at €570-600 million, which is a strong improvement YoY. The company expects backlog to remain high thanks to more new orders coming in, but also because supply constraints will limit shipments in H2. Management remains confident in their FY22 outlook of mid- to high-teens percentage growth, although they do expect it to come in at the lower end of the outlook, because of the supply chain disruptions. The problem here is not demand, but the number of shipments ASM can realize, which is a good sign. Supply chain problems should start to ease into 2023.

The long-term outlook for ASM also remains strong. Global wafer equipment spending is expected to keep growing, which is a strong industry tailwind for ASM.

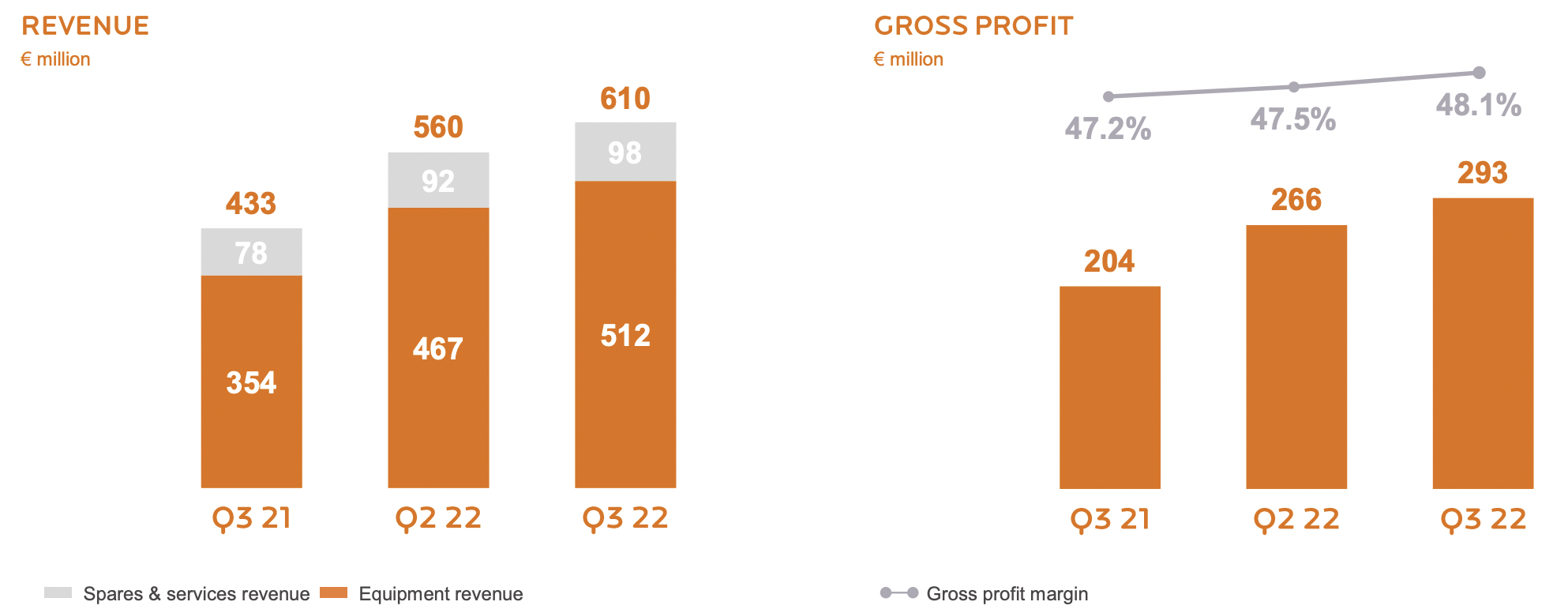

The company just reported its earnings and outperformed its own outlook. Remarkably, the company improved its margins QoQ, despite high inflation, from 47.5% in 2Q22 to 48.1% in 3Q22. The operating margin came in at 26.2%. The company reported revenue of €610 million and therefore outperformed its own outlook of €570-600 million. New orders came in at €676 million, a decrease compared to the record intake we saw during 2Q22. This might signal that demand is getting a little softer although order intake was still higher compared to 1Q22.

It is important to note that ASM adjusted its order intake to reflect the expected negative impact of the recent U.S. export restrictions on China. These restrictions will negatively impact the business and its revenues. 16% of total revenue so far this year is coming from China, and this is a fast-growing part as well. ASM right now expects these U.S. restrictions to affect 40% of sales to China. ASM has already factored in this loss of business into their order intake numbers and 4Q22 guidance.

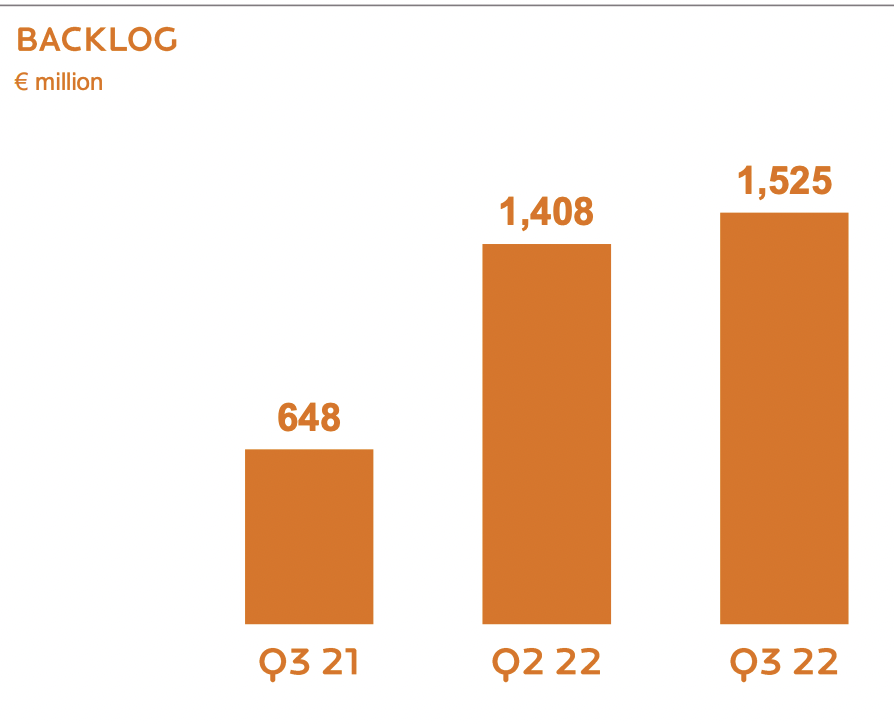

ASM still reported a strong quarter, despite China restrictions, high inflation, and recession fears. Free cash flow came in at a healthy €122 million. Total revenue increased by 41% YoY and net earnings increased by 32% YoY, both showing strong continued growth YoY. Despite solid revenue and delivery numbers, the backlog still managed to increase, despite some headwinds on order intake.

{kind=link}

And although the China problem might create a lot of headlines, we should not forget that, despite all headwinds, ASM still reported record revenue and still increased gross margins.

{kind=link}

For 4Q22, ASM expects another growing quarter and revenue of €600-630 million, which includes the negative impact of the China restrictions. This is what management added:

Taking into account the guidance for Q4, ASM is on track for strong growth in 2022, its sixth consecutive year of double-digit growth, and is expected to clearly outperform the wafer fab equipment ((WFE)) market in 2022. During the third quarter, the semiconductor end market further slowed down, with significant declines in the PC and smartphone segments. Combined with an expected deceleration in global economic growth WFE spending is forecasted to be down in 2023, in particular the memory segment. While it is too early to provide guidance for 2023, we believe our company is in good shape, on the back of an expected robust backlog by year-end, our strong position in the leading-edge logic/foundry segment, and solid traction with newly introduced products and applications.

ASM saw a strong improvement in its balance sheet compared to the last quarter. At the end of 2Q22, the company had €552 million in cash and no debt. Now, at the end of the third quarter, the company improved this to a cash position of €620 million and no debt. This also pushed the cash position above the target of achieving at least a cash position of above €600 million.

Conclusion

ASM presented another strong quarter by reporting record-high revenue and order intake remaining resilient. I am a bit worried by the comments made about the China restrictions, though. These restrictions might have a negative impact on just over 40% of sales in China, where China represents 16% of revenue so far this year. This is not a significant impact on the business, yet it is another headwind in a difficult economy. ASM noted that they expect economic growth to slow down during 2023 and WFE spending to come down. While it might be too early to look at 2023, I believe the current backlog of ASM is very strong and might provide a buffer during difficult times.

I believe the company still has a solid long-term outlook, despite the recent strong increase in share price and additional headwinds from China. The near-term outlook might have gotten a bit worse since their reporting of 2Q22, yet management stays positive and so will I. Global demand for the machines ASM builds will remain high as these will play an important role in the future of high-end semiconductors.

The company is a hold for me as I see no dramatic change in the investment thesis. The forward P/E is still only 18.55 and therefore not expensive. Yet, the economic outlook has become worse and the recent increase in share price makes the buying opportunity less appealing. I do still think the company is good value and the long-term outlook remains unchanged. I believe buying at current levels would still result in strong returns, and therefore slowly initiating a position would not be a bad choice. Still, I recommend waiting, for now, to see where the economy is headed and how China restrictions affect ASM.

I, therefore, rate ASM International a Hold for now.

For further details see:

ASM International: Q3 Impacted By China Restrictions