ASMIY - ASM International: Valuation Has Already Priced In Potential Growth Acceleration

2023-08-07 04:07:26 ET

Summary

- ASM International's recent results show 2Q23 revenues slightly below consensus, but positive aspects include improved product mix and increased sales from China.

- Weakening demand in certain segments and push-outs in cutting-edge Logic/Foundry contribute to lower order intake, but this should return to normalcy.

- Valuation has already priced in potential growth acceleration and margin expansion.

Summary

This post is to provide my thoughts on ASM International ( ASMIY ) recent results. I am recommending a hold rating as the valuation seems to have priced in the potential acceleration in growth and margin improvement. In order to make the risk-reward situation more appealing, ASMIY would need to grow faster than I expect, as its valuation is already at a premium to peers. While it is possible for ASMIY to grow faster, I would prefer to invest when the valuation is cheaper.

Investment thesis

ASMIY’s 2Q23 revenues were €669.1 million, 1% below consensus, and total orders came in at €485.8 million. Positive product mix and a larger proportion of sales coming from China also helped drive total EBIT to $170.7 million.

Management attributed weakening demand, prompted by push-outs in cutting-edge Logic/Foundry, for the quarter's lower order intake of €486 million, down 48% y/y in constant currency terms. In my opinion, this is a result of slower readiness for new customer fabs and weaker end-market conditions. This is not good, but I don't think the market will be too shocked by it, especially since ASML's recent earnings call has already talked about it. While this may seem like bad news at first glance, I'm actually in the camp that sees this as evidence of the backlog returning to its more typical levels after having been artificially inflated in 2022 due to the positive effects of the improved supply chain. This bodes well for a quicker return to normalcy in growth in the coming quarters.

Looking ahead, management expects that in 2023, the overall WFE market will decline by mid to high single digits % due to the negative effects of weak Memory dynamics and leading-edge Logic/Foundry pushouts. Nonetheless, I think it's encouraging that the company has reiterated its forecast for single-digit constant currency revenue growth in 2023, especially when compared to the wider WFE market, which is predicted to decline by 10% in CY2023 . I believe the delays in cutting-edge Logic/Foundry, which reflect weaker end-market conditions, are more of a matter of timing than a structural change. As a result, the company's intrinsic value shouldn't take much of a hit, as revenues will resume normally over time.

It's worth noting that ASMIY's top customers are moving forward with their technology roadmaps, and the company has also confirmed its plans for the upcoming Gate-All-Around [GAA] node, with pilot-line production of GAA beginning in 2024 and high-volume production beginning in 2025. For this reason, I anticipate that orders growth will accelerate and exhibit very healthy performance in the upcoming quarters, serving as a key potential upside catalyst. In the coming quarters, I anticipate this shift to GAA to serve as a reliable and sustainable growth driver for ASMI.

Other than that, 2Q saw stable demand in mature node markets and Silicon Carbide Epitaxy, and management is anticipating healthy growth this year. To some extent, I think the stronger dynamics in investments in ASM's mature nodes—particularly strong China—could compensate for the general weakness in other end-markets. ASM also reported that LPE is on track to surpass its €130 million revenue goal for the year thanks to the expansion of its customer base and its increased demand for Silicon Carbide. Last but not least, this quarter saw LPE receive its first order from a major European SiC player, which I believe to be an omen of more to come.

Valuation

Own calculation

I believe the fair value for ASMIY based on my model is €596.85. My model assumptions are that: ASMIY will see growth acceleration in the coming years as the business gets past the normalization of order backlog, recovers in leading-edge logic/foundry, and GAA orders flow into the P&L. Consequently, we should see a net margin recovery back to historical levels.

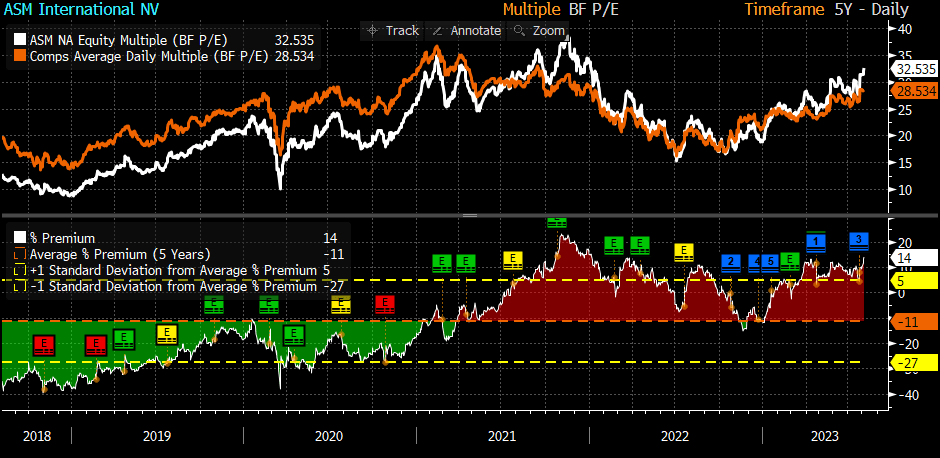

Peers include: AMSL Holding, BE Semiconductor Industries, Inficon Holding, Technoprobe, Aixtron, X-Fab Silicon Foundries, and Siltronic. The median forward PE multiple peers are trading at is 28.5, and the expected 1Y growth rate is 19%. Historically, ASMIY has traded pretty in line with peers, with a modest discount of 11% through the years. While I see ASMIY's 1 year forward growth to be lower than peers, I think the potential acceleration in growth should continue to support the current multiple.

The issue is that, at 32x forward PE, ASMIY seems to be fairly valued based on my model. I do not expect valuation to re-rate further as it is already breaking the historical trend. Hence, ASMIY would need to grow a lot faster than I expected to make the risk-reward situation appealing.

At the current share price, I recommend staying neutral until the valuation becomes cheaper.

{kind=link}

Conclusion

I recommend a hold rating as valuation has already factored in potential growth acceleration and margin improvement. While recent results show positive aspects, such as improved product mix and increased sales from China, challenges stemming from weaker demand in certain segments raise caution. The company's resilience and strategic moves, including transitioning to the GAA node and stable performance in mature markets, indicate future potential. However, the current valuation at 32x forward PE suggests limited room for further re-rating, necessitating a significant growth surge to improve the risk-reward balance.

For further details see:

ASM International: Valuation Has Already Priced In Potential Growth Acceleration