TSM - ASML: Priced For Perfection Market Ignoring China Geopolitical Risks

2023-04-16 22:32:56 ET

Summary

- After the valuation reset in the tech sector, ASML is one of the strongest-performing stocks among peers.

- The company has paired secular revenue growth with attractive profit margins.

- The valuation of the stock is a multiple higher than that of its largest customer Taiwan Semiconductor, which makes up a disproportionate amount of its business.

- ASML is a very dangerous stock, especially for long-term investors.

ASML ( ASML ) is one of the few stocks in the tech sector that is still trading over 100% higher than pre-pandemic levels. The company has an arguably monopolistic position in advanced semiconductor equipment systems and has been able to pair high secular revenue growth with unusually attractive profit margins. While the fundamental picture remains very strong, I make the argument that the stock is exhibiting many of the same traits of other tech stocks from the recent tech bubble. Furthermore, the price of the stock is puzzling considering that the valuation is a multiple higher than that of its largest customer, which makes up a disproportionate amount of its business. While the chances of downside do not appear large or imminent, the risk-reward does not favor surprises to the upside. ASML looks like a very dangerous stock as valuation will eventually matter.

Problem 1: ASML Stock Is Overvalued

I am not going to rehash the business model or bullish thesis as that is well documented by this point. For those not yet familiar with this story, I can recommend both this typically excellent article by Dividend Sensei as well as an CNBC documentary video.

I have made that choice deliberately because ASML has many of the traits that I saw prior to the bursting of the recent tech bubble. The most notorious of these traits is the idea that one can buy a stock at any valuation if the quality of the business model is high enough.

Consider that ASML trades at an astonishing premium to its competitors. Canon ( OTCPK:CAJPY ) trades at 12x earnings and 0.7x sales. Nikon ( OTCPK:NINOY ) trades at 10x earnings and 0.71 sales. Applied Materials ( AMAT ) trades at 16x earnings and 3.9x sales. ASML is trading at 32x earnings and 11x 2030 consensus estimates.

{kind=link}

On the basis of revenue, ASML is trading at 9x sales - an astonishing multiple for a company projected to see revenue growth to decelerate to the low teens in coming years.

{kind=link}

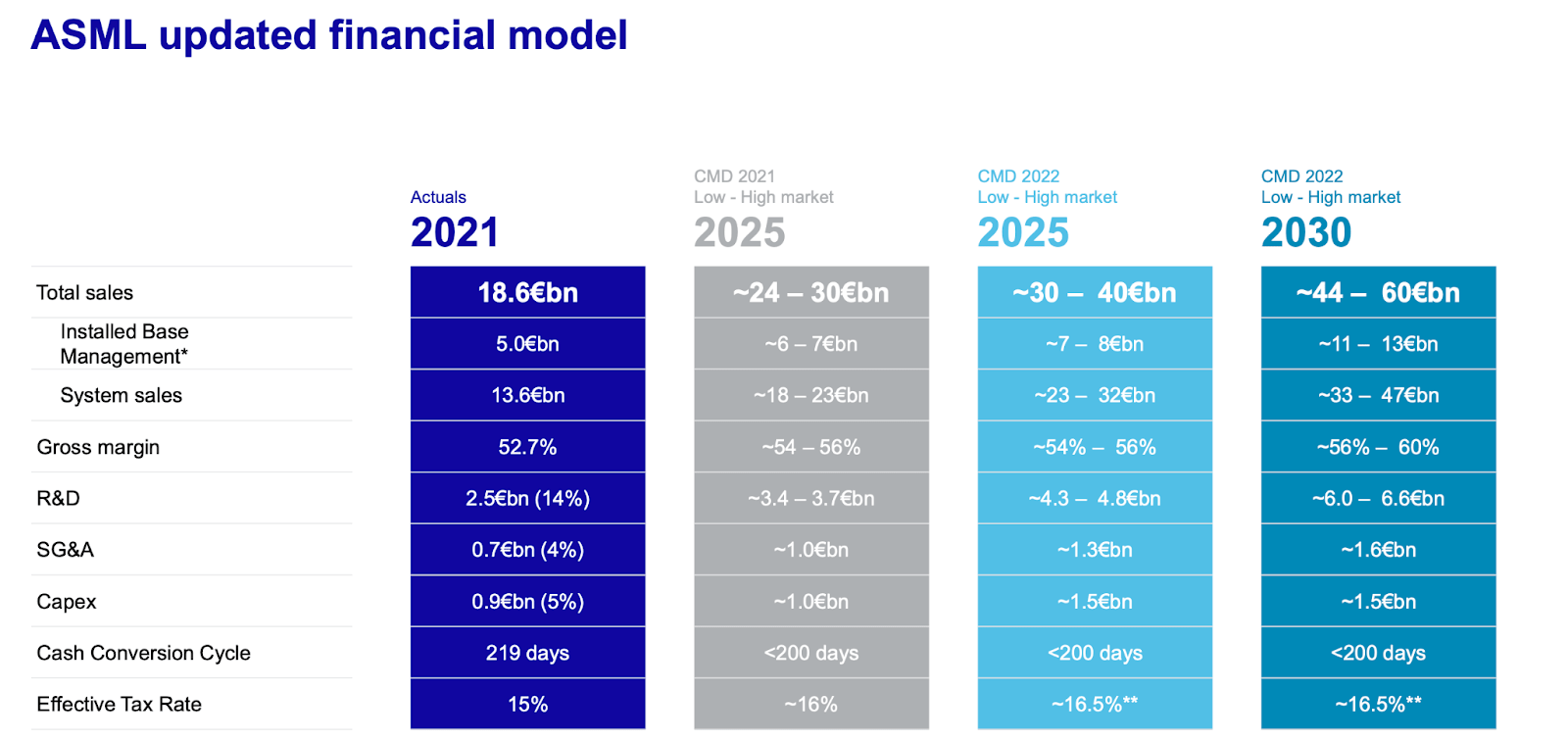

ASML has given long term guidance at their 2022 Investor Day, projecting up to $40 billion in 2025 revenues and $60 billion in 2030 revenues.

{kind=link}

Based on the guidance for gross margins and operating expenses above, this implies up to $14 billion in net income in 2025 and $23.7 billion in net income in 2030. I note that while ASML has a strong balance sheet position with $7.3 billion of cash versus $4.2 billion of debt, the interest income earned on the excess cash is unlikely to materially alter the above estimates. One can verify in the consensus estimate diagrams shared above that analysts are already betting on ASML achieving the upper end of both revenue and earnings guidance. Yet even based on those optimistic projections, ASML stock is already trading at 4.5x 2030e sales and 11x 2030e earnings. With consensus estimates calling for mid-single-digit revenue growth in 2031 and onwards, I find current 2030 valuations to be already very full (relative to where the rest of the tech sector trades today) - implying that the stock can move nowhere over the next 8.5 years and still appear richly valued.

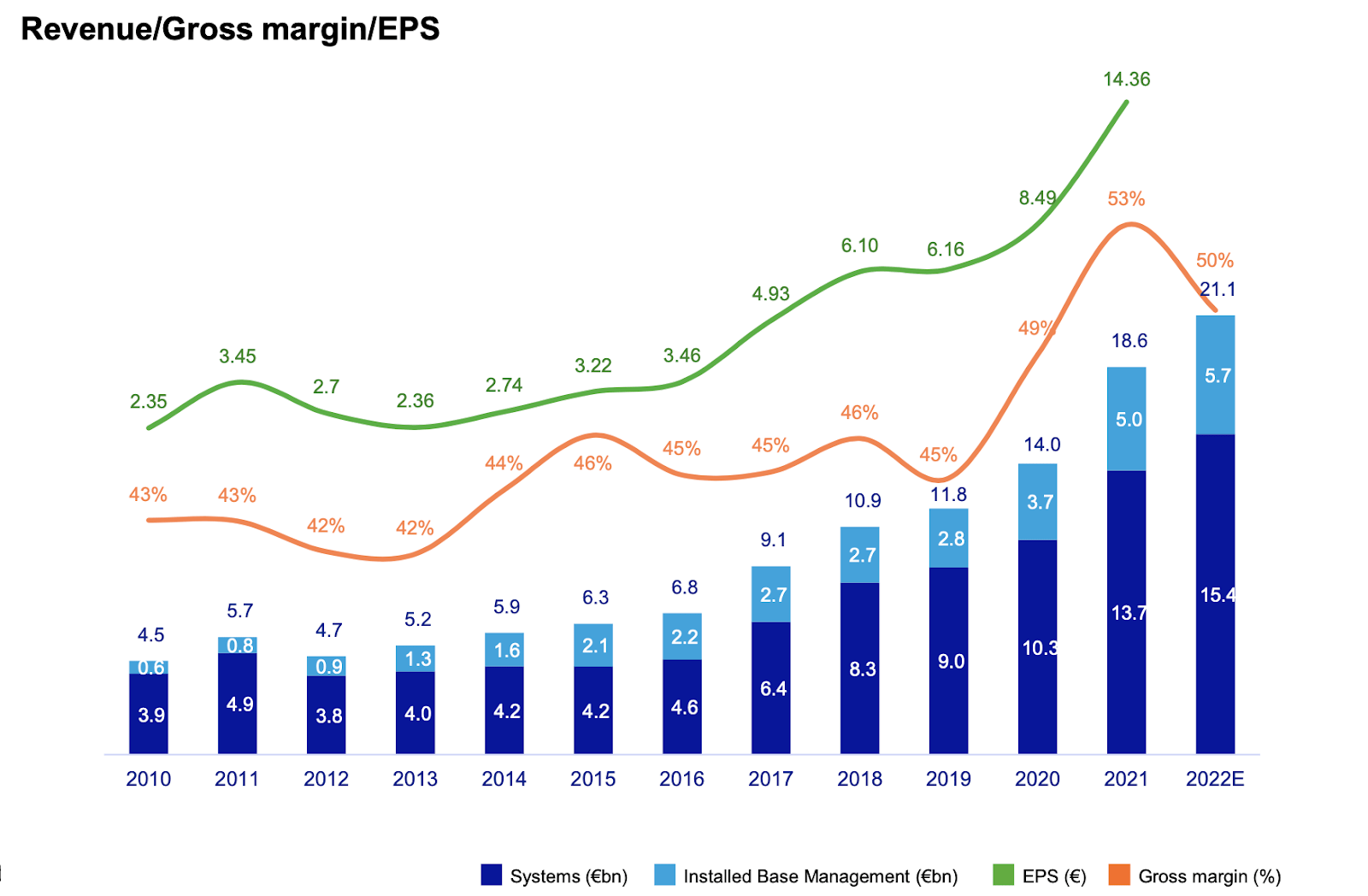

Perhaps some ultra-bullish investors might make the argument that consensus estimates are too conservative. But I’d counter that consensus estimates are already using the high end of management guidance and revenue growth has not exactly been exponential over the last couple of years, meaning that any inevitable deceleration in growth rates is not coming off of a high starting point.

{kind=link}

I can acknowledge that ASML has delivered stunning secular revenue growth, robust profit margins and free cash flow generation, and shown alignment with shareholders through a growing dividend and generous share repurchase program. But the bursting of this tech bubble has only reinforced the reality that valuation always matters at some point over the long term, even for the highest quality of companies.

Problem 2: The Geopolitical Risks with ASML Stock

The above argument is in my opinion already sufficient to raise red flags about the current stock price. But we can go one step further in analyzing the stock of its customers. As stated in its annual filing , ASML has extremely high customer concentration risk:

The recognized total net sales to our largest customer amounted to €7,046.9 million, or 33.3% of total net sales in 2022, compared with €6,881.1 million, or 37.0% of total net sales in 2021. In 2022, 55.8% of total net sales were made to two customers.

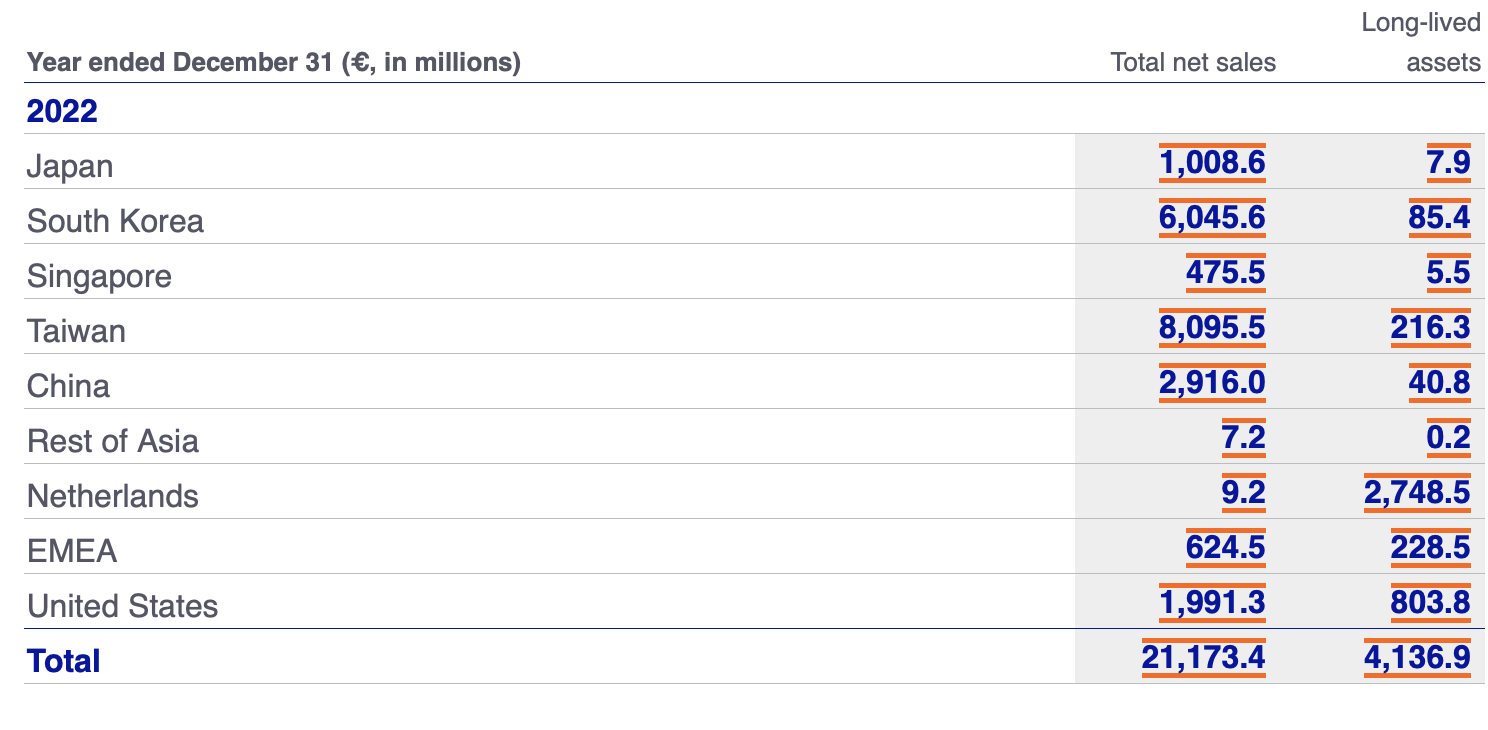

It is well known that these two customers refer to Taiwan Semiconductor ( TSM ) and Samsung (SSNLF), respectively. TSM is perhaps more well known than ASML due to both its foundry dominance as well as its entanglement in geopolitical tensions with China. TSM is based in Taiwan. Taiwan is often viewed as an argument piece between China and the United States, as the former asserts that it is not an independent country whereas the latter tends to support its independence. Geopolitical tensions have risen between the United States and China, with politicians moving to restrict the sale of semiconductor equipment to China . We can see below that sales to China made up just under 14% of overall net sales (this does not include the $8.1 billion in net sales to Taiwan).

{kind=link}

Yet the stock of TSM has sold off dramatically in recent years, likely due to the Russian-Ukraine war leading many investors to fear a similar outcome between China and Taiwan. That has led TSM stock to trade at just around 16x forward earnings.

{kind=link}

I’d argue that given TSM’s dominant position in the foundry business, the forward outlooks for ASML and TSM are much more correlated than is suggested in the stock prices. One could make the argument for a pair trade (long TSM, short ASML) given that view, but I will not make that argument today. TSM stock seems to be pricing in the potential of a Chinese invasion and subsequent ban on working with the company. But if such an outcome were to occur, then this would also materially impact the financials of ASML considering that TSM made up over 33% of net revenues in 2022. Moreover, I suspect that investors would also grow skeptical of its relationships with its Korean and Japanese customers, which made up another 33% of its net revenues. Adding that together, 85% of ASML’s net revenues are subject to Chinese geopolitical risks.

I stress that I am not saying that I view an invasion of Taiwan by China to be likely, or that one is necessary for ASML stock to suffer losses. Instead, I am raising the possibility that ASML stock undergoes similar multiple compression as seen at TSM to account for geopolitical risks, as its high exposure to the Asian region make the stock a very likely candidate for a vicious selloff if any event were to occur. As the chess grandmaster Aron Nimzowitsch once said , “the threat is stronger than the execution,” and this saying is applicable in the forward-looking nature of the stock market.

Conclusion

Even before accounting for geopolitical risks, ASML stock appears priced for perfection as the stock looks richly valued even based on the high end of management’s long term guidance. The stock is priced as if it is a consumer staple or one holding an impenetrable monopolistic position. But if confidence in such a position were to deteriorate, perhaps due to the geopolitical risks outlined in this report, then I could see the multiple compression significantly, especially given that many tech peers have seen a significant reset in valuations. The lack of near term downside catalysts make it difficult to recommend shorting the stock, but I am resolute in my conclusion that the stock presents a very dangerous proposition especially for long term investors as the “buy quality at any price” trade may lead to substantial underperformance over the long term.

For further details see:

ASML: Priced For Perfection, Market Ignoring China Geopolitical Risks