INTC - ASML Q3 Earnings Preview: Lowering My Near-Term Outlook But Still Bullish

2023-10-16 10:00:42 ET

Summary

- ASML Holding N.V. shares are down 16% since my last article, with the price back to the €570 level at the time of writing, and this decline is not entirely surprising.

- ASML's Q3 results are expected to show little surprises, but market focus will be on management's forward commentary and industry growth outlook.

- I expect ASML to keep reporting disappointing EUV growth in FY23, but also into FY24 as I am not seeing a quick recovery of the semiconductor industry, impacting Capex budgets.

- Orders from China will likely stay strong in the second half of the year, similar to what we saw in Q2 when Chinese demand for DUV equipment grew rapidly.

- I do not view Canon’s “nanoimprint lithography” as a significant threat to ASML's EUV monopoly.

Investment thesis

I maintain my Buy rating on ASML Holding N.V. ( ASML ), but slightly lower my revenue and EPS estimates ahead of its Q3 results following recent developments and the possibility of a prolonged period of economic weakness and gradual recovery of the semiconductor industry in 2024.

ASML is set to report its Q3 results pre-market on Wednesday, October 18th. To get straight to the point, I expect little surprises but expect the market to be focused on management’s forward commentary and their industry growth outlook concerning the potentially falling demand for their products.

I rated shares a “buy” in July after the company reported its Q2 results , which did not disappoint. ASML continues to deliver incredible growth considering the challenges emerging from a downturn in the semiconductor industry. Management even upgraded the FY23 outlook, now expecting growth closer to 30% from a previous 25%, which is incredible in a market expected to be down over 10% in terms of sales in 2023.

Nevertheless, shares are down 16% since my last article, with the price back to the €570 level at the time of writing. This decline is not entirely surprising, as the company is facing plenty of headwinds, most likely leading to a weaker-than-anticipated FY24 outlook. ASML is facing demand issues for its high-end EUV equipment due to fab delays and a weak demand environment for its leading customers, resulting in orders being pushed forward and impacting ASML’s near-term financial performance.

EUV deliveries and orders will likely remain weak in the short term as industry weakness persists

While the company delivered a strong earnings report in Q2, some first signs of weakness were visible in the results. Most important was the disappointing growth in EUV shipments. EUV shipments in Q2 were somewhat lower and EUV orders were flat sequentially at just $1.6 billion.

However, this disappointing growth in EUV was not the result of a drop in demand for the product or operational issues but reflects an industry-wide problem in the foundry industry, which is a lack of skills to get fabs ready, practically meaning that the likes of Intel ( INTC ), Samsung Electronics ( SSNLF ), and Taiwan Semiconductor Manufacturing Company Limited ( TSM ) aka TSMC are having trouble getting fabs operational.

As fabs can’t get operational, these companies are telling suppliers to delay the delivery of high-end chipmaking equipment, which was reflected in the EUV delivery numbers of ASML in Q2. Crucially, orders are not being canceled but simply being pushed forward, yet still, this impacts ASML’s near-term financial results. As a result, management has lowered its EUV growth expectations for this year from 40% to 25%, reflecting the pushed-out orders.

However, I am expecting ASML to further lower these growth expectations with its Q3 earnings report as I expect it to keep reporting disappointing EUV growth in FY23, in part due to these fab delays continuing, but also into FY24 as I am not seeing a quick recovery of the semiconductor industry, impacting Capex budgets from ASML customers and therefore ASML’s order intake.

The current consensus is for the semiconductor industry to bottom out in the second half of this year, and while I do agree with this consensus and expect a bottom in Q4, I am not seeing a quick recovery. TSMC earlier guided for a gradual recovery, and this seems like the most realistic scenario with macro indicators still pointing to a potential recession or at least some prolonged economic weakness as interest rates remain high as well. Swiss VAT stated that it believes the bottom has been reached already and expects demand to recover gradually from here on out. In August, semiconductor sales were up 2.3% sequentially, as we are indeed seeing slight improvements quarter-over-quarter. However, YoY sales are still down by double digits at 11.8% as weakness persists.

I will add that while many analysts have been pointing to weakness in advanced node demand to impact ASML, these analysts are underestimating the impact of AI demand. While there clearly is some decreased demand for advanced nodes by the likes of Apple and Qualcomm, which continue to face lower demand for their hardware products, this is largely offset by demand for AI semiconductors from Nvidia, in particular. Recent monthly data from TSMC already showed better-than-expected numbers as high demand for AI semiconductors was able to offset some of the hardware weakness.

Still, according to Reuters , TSMC has already told suppliers of high-end semiconductor equipment, including ASML, to postpone deliveries, not just because of delays in fab completion but also due to a weak demand environment and growing concerns about customer demand. As a result of this and everything discussed above, I expect ASML to see continued weakness in EUV deliveries and orders, resulting in the EUV forecasts being cut further (potentially to 20% growth in FY23) for this year and into FY24, although management will likely hold back from giving concrete guidance for FY24 due to low visibility.

Normally, I would point to the massive backlog of €38 billion as a safety net for the company to keep its growth up even in times of lower demand, but this in combination with customers postponing machine deliveries is creating a tough near-term environment for ASML to navigate.

However, I will say again: these orders do not get canceled but simply postponed so ASML will realize this revenue at a later stage. As pointed out by JPMorgan analysts , the worse the outlook for FY24 and this will most likely disappoint, the better the outlook for FY25. The value of its machines in the long-term remains incredible to its customers and of high importance to their growth ambitions.

As ASML continues to operate a monopoly in the highest-end semiconductor equipment market, resulting in a stellar long-term outlook, I strongly believe that even if management were to cut their short-term outlook as I expect, investors have absolutely nothing to worry about. CEO Peter Wennink said in a recent interview with Reuters that he indeed sees some orders for its high-end tools being pushed back but called it a "short-term management" issue, indicating that the business remains sound and of incredibly high quality in the long term.

Furthermore, according to Allied Market Research, the semiconductor foundry market is expected to grow at an 8.1% CAGR through 2032, and I believe this should fuel the growth potential for ASML into the double digits, primarily driven by consistent semiconductor production capacity expansion requiring new ASML equipment. This is what I wrote previously, and this remains unchanged despite the short-term noise:

In the long run, the high demand for semiconductors and rapid industry growth, especially with the boost in production in the U.S. and Europe, should drive continued demand for these EUV machines as these are the only ones capable of producing the smallest nodes available today. As a result, the global EUV market is expected to grow at a CAGR of 21.5% through 2029, which includes further developments and new versions. With ASML holding a monopoly here, investors have nothing to worry about as the current slowdown in EUV orders is only temporary.

ASML management growth outlook (ASML)

New Canon machines are no reason for concern

Last Friday, Canon Inc. ( CAJPY ) announced a potential challenger to ASML’s EUV machines, resulting in a 2.5% price decline for ASML shares during the day. Canon announced its latest “nanoimprint lithography” system – a technology it has been working on since 2004. Nowadays, ASML’s EUV machines are the only ones capable of producing the most advanced nodes required for high-end technologies like Apple’s latest iPhones or Nvidia’s H100 datacenter/AI chips.

However, according to Canon, their latest machine could challenge ASML’s EUV machines as it can make semiconductors equivalent to a 5nm process and go as small as 2nm. Furthermore, due to the difference in technology, Canon says its machines are smaller than the container-size machines from ASML and require less power as these don’t use ultraviolet light. All sounds great - and quite bad for ASML.

However, the technology used by Canon has been around for multiple decades and has never really taken off in the world of increasingly complicated chips as wide acceptance of the technology has stayed out. This is in part due to ASML’s EUV technology in the past proving to work better during the chip printing process. Whether this has now changed with the latest machine from Canon remains a big question, but I highly doubt it will produce as high-quality products as ASML’s EUV machines.

Furthermore, it will probably have to blow EUV machines out of the water in terms of quality and price to be able to compete as the likes of TSMC, Samsung, and Intel have their whole production process built around EUV machines, making it hard to replace these with a whole new technology, most likely requiring further expensive technology changes. Also, ASML is already working on the next-gen variant of its EUV machine, which, even if Canon matches current generation equipment, will probably set it on the backfoot again.

Overall, what I am trying to say here is that investors should not get worried about news like this yet. ASML’s global moat is incredibly strong, and its technology is very dominant. It will take a significant competitor to replace ASML’s technology, and I do not view Canon’s “nanoimprint lithography” as such. Until proven otherwise, I do not see Canon’s technology actually replacing ASML’s EUV machines at the world's largest foundries. Still, I am keeping a close eye on any further product information from Canon regarding its new product.

DUV should offset some of the EUV weakness in the second half as China restrictions kick in on January 1 st

DUV orders and shipments allowed ASML to offset most of the weakness it saw in EUV in Q2, largely due to a boom in Chinese deliveries, and I expect this trend to persist in its Q3 earnings report.

Orders from China will likely stay strong in the second half of the year, similar to what we saw in Q2 when Chinese demand for DUV equipment grew rapidly. We are seeing this in response to stricter export regulations imposed by the US and Dutch governments, which will limit the export of the most advanced DUV equipment to China. As a result, Chinese semiconductor manufacturers are pushing forward orders now that ASML still has valid export licenses to ship its most advanced DUV equipment to China until the end of 2023. This will most likely drive strong growth for DUV equipment in Q3 and offset some of the continued weakness expected in EUV shipments, in line with management’s guidance. This strength in DUV has allowed it to increase its FY23 DUV forecast with it now guiding for this business to grow by 50% YoY compared to a previous expectation of 30%.

Furthermore, while the Chinese export restrictions are far from ideal for ASML, I stick by what I said in my previous article as, crucially, the new restrictions only forbid the export of advanced DUV systems:

Overall, the impact of Chinese export restrictions is expected to remain minimal. ASML has not been focusing on China for many years as its most advanced and expensive products were already under export control. Moreover, ASML has plenty of growth potential remaining outside of China, so I don’t view this as crucial to the investment thesis. Investors should definitely not make this larger than it really is.

While further export restrictions from the U.S. for the remaining DUV equipment could harm ASML further, this seems highly unlikely. Still, if this were to happen, this could endanger around 10% to 15% of its revenue, which is something investors need to be aware of. Nevertheless, I remain bullish.

Revised outlook & ASML stock valuation

As I said earlier, I am not expecting any major surprises in the Q3 results to be reported by ASML next Wednesday, as revenue will likely fall in the range guided for by management, with margins coming in slightly higher. Yet, I expect revenue at the low end of management’s guided range of €6.5 billion to €7.0 billion and a gross margin of around 50% due to continued weakness in EUV shipments. Following my research above, I have slightly lowered my expectations for Q3 to €6.69 billion in revenue and EPS of €4.61.

Furthermore, the order intake will most likely come in mixed, with a strong performance in DUV and a relatively flat to slightly down performance in EUV orders, resulting in the order intake remaining flat YoY and within my earlier guided range of €4 billion to € 5 billion. This compares to €4.5 billion in Q2 and €3.8 billion in Q1.

Yet, more important will be management’s forward commentary and their view on FY24. This is where I expect some disappointment for investors as management will most likely communicate a somewhat negative view for FY24 due to pushed-out orders and a struggling semiconductor demand environment. However, this already seems to be priced into the shares. Also, I expect Q4 guidance to be more resilient, resulting in expectations for €6.81 billion in revenue and EPS of €4.86.

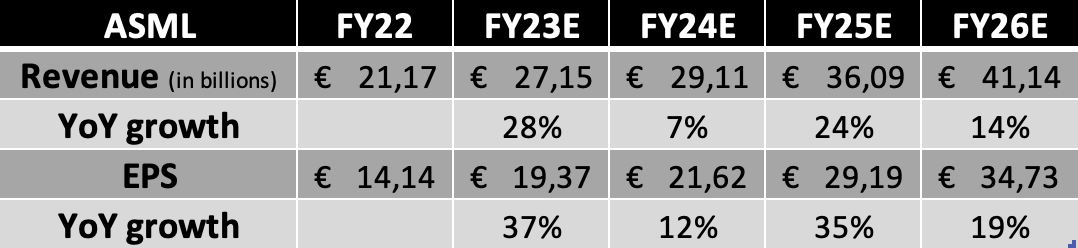

This leads to the following financial expectations through FY26, reflecting significantly lower expectations for FY24.

Financial projections (Author)

{kind=link}

These lower near and medium-term financial expectations in combination with increased uncertainty also impact my fair value share price estimate. Shares are currently valued at a forward P/E of 29.6x, which is fair at least in my eyes. As indicated before, ASML remains an incredibly high-quality company operating a virtual monopoly in the high-end semiconductor equipment industry, which is growing sales in the double digits through a cyclical downturn. The company still has a massively impressive growth outlook, even when considering the near-term weakness fueled by a growing semiconductor industry.

As a result, a 31x P/E is warranted here (down from a previous 33x) and adequately considers the near-term uncertainties coming from the industry's weakness. Based on this belief and my lowered FY24 EPS estimate, I calculate a target price of €692 per share (down from €812). Based on an annual return of 10%, I believe shares are trading at a 7% discount to their fair value of approximately €614 per share.

Conclusion

Therefore, I maintain my buy rating and believe that ASML Holding N.V. shares offer excellent value today and have largely priced in a disappointing FY24 outlook already. While we could see some more downside following the Q3 earnings call if management indeed turns slightly bearish on its near-term growth prospects, I believe this should be followed by a share price uptick shortly after, with shares returning to fair value territory above €600 per share, offering plenty of near-term upside today and a great entry point for long-term investors. Those bullish on the semiconductor industry should hold ASML Holding N.V. shares in their portfolio as one of the industry cornerstones.

For further details see:

ASML Q3 Earnings Preview: Lowering My Near-Term Outlook But Still Bullish