SSNLF - ASML: Should You Buy The Stock Heading Into Q4 Earnings?

2024-01-12 12:05:22 ET

Summary

- ASML Holding N.V. stock has rocketed by 24% since reaching a 52-week low in October 2023 amidst negative market sentiment.

- ASML is expected to report strong Q4 earnings, with sales expected to be between €6.7 and €7.1, representing a 30% YoY sales growth, while margins remain elevated.

- Management has highlighted 2024 as a "transitory year" with flat sales and a 2% growth in EPS, citing delays in new fabs and sales restrictions in China.

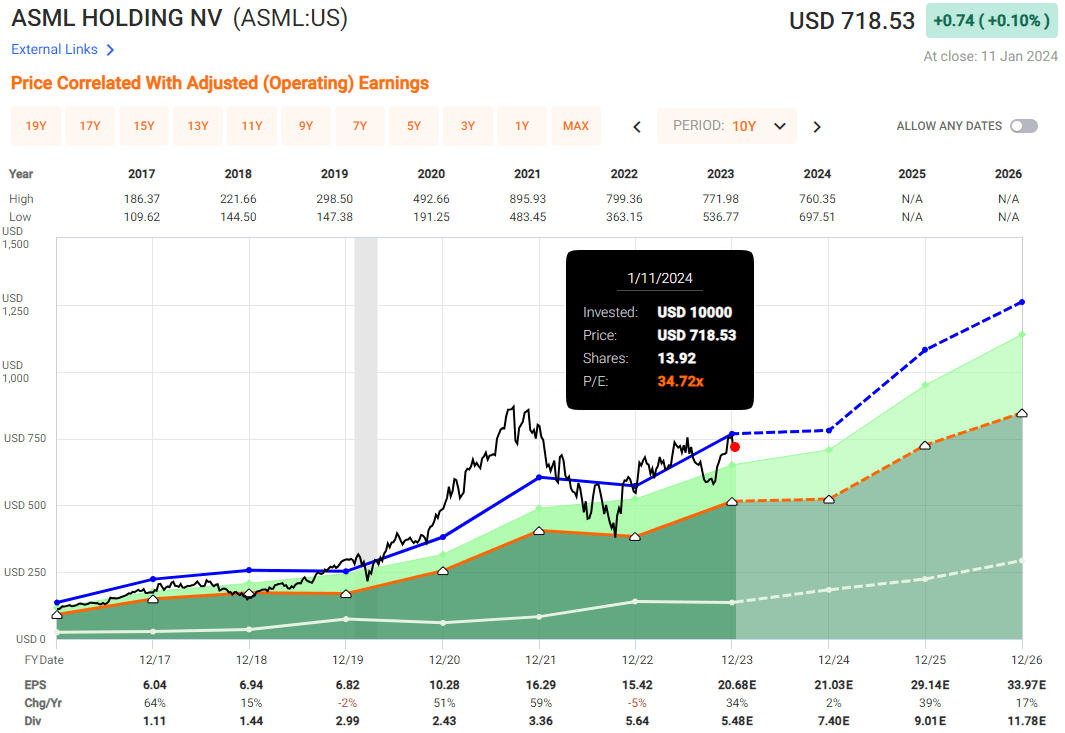

- ASML stock is currently trading at a blended P/E of 34.72x, just below its 10-year average, and with an expected EPS growth rate of around 18% annually over the next 3 years, ASML is poised to deliver double-digit returns.

I have been following and investing in ASML Holding N.V. ( ASML ) for a long time now. It is one of my largest positions among European stocks. After reaching the 52-week low of $564 back in October 2023, the stock has gone on to recover with the rest of the market, delivering a return of more than 24% since the low, which I was buying with both hands.

I covered ASML back in October on the day of the solid Q3 earnings , advising investors to capitalize on the favorable valuation driven by the negative sentiment around the slowdown in sales of consumer electronics and elevated interest rates. This negativity marked the bottom for the stock, and it has since recovered handsomely.

Those who bought ASML stock then have outperformed the market by more than 2x.

{kind=link}

With that, it's time for a reality check to determine whether ASML stock is still a buy heading into the Q4 earnings, which are going to be reported pre-market on January 23rd .

Still a Growth Story

ASML holds the title as the third-largest European company, boasting a market capitalization of $278 billion. It claims the position as the largest European tech company, with a keen focus on semiconductor lithography technology.

Their ultraviolet lithography technology, known as "EUV," stands at the forefront, driving the production of cutting-edge microchips for industry leaders such as Nvidia ( NVDA ) and Advanced Micro Devices ( AMD ). Taiwan Semiconductor Company ( TSM ) stands out as ASML's biggest client.

Riding the wave of increased chip consumption in our ever-growing digital world, ASML's EUV machines dominate the market as the most advanced and efficient, essentially operating like a monopoly for this specific product.

Canon ( CAJPY ) has recently unveiled its FPA-1200NZ2C, a nanoimprint semiconductor manufacturing tool capable of producing advanced chips, sparking concerns among ASML investors about potential competition. Canon's device utilizes nanoimprint lithography or "NIL" technology as an alternative to photolithography. Theoretically, it could pose a challenge to ASML's EUV and DUV lithography machines in terms of resolution.

It's crucial to recognize that ASML's equipment has already established strong ties with existing customers. Switching to new equipment which has not yet proven quality and efficiency, even if it's potentially more affordable than ASML's expensive $120 to $200 million machines , requires personnel training, adjustments to the production line, and the adoption of new software to operate the machinery. Considering these factors, I don't see Canon's technology as an immediate threat.

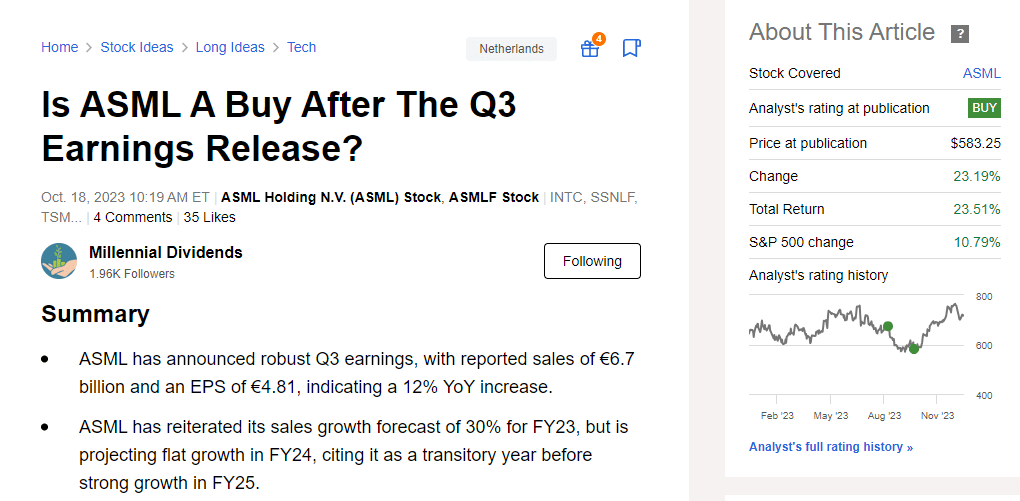

As I already have covered the previous earnings in detail, just to shortly summarize what happened: ASML's Q3 earnings were very solid. The company reported sales of €6.7 billion, in-line with analysts' expectations, but significantly higher than the €5.8 billion reported in the previous year. This translates to a net income of €1.9 billion or €4.81 EPS, representing a 12% increase from the previous year.

In Q3, ASML sold 112 lithography systems, a number similar to the 113 systems sold in Q2.

{kind=link}

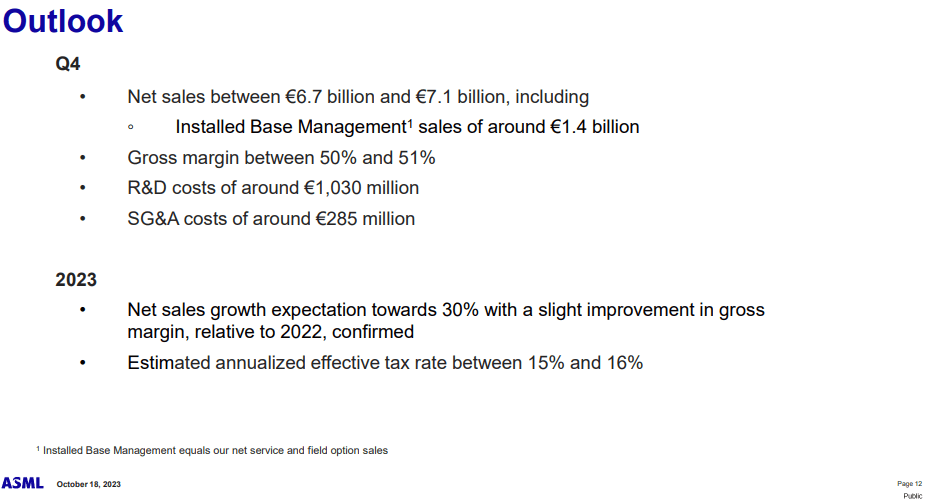

For Q4 earnings, which ASML as noted will report on Tuesday, January 23rd, ASML has reiterated its outlook for Q4, anticipating sales between €6.7 to €7.1 billion, with margins remaining at the higher end of the historical range. The company still anticipates a 30% YoY sales growth.

The consensus is for the EPS is to come at €5.02, but keep in mind that over the past 4 quarters, ASML has always beaten the expectations. With the improvements in economy and the most likely avoidance of the "hard landing" in 2024, the outlook looks promising and I am expecting ASML to earn closer to €5.15 EPS during Q4.

However, for 2024, the company does not foresee any top line growth, citing a transitional year with virtually flat YoY sales.

{kind=link}

The term "transitory year" indicates that ASML is currently navigating through a couple of challenges.

During Q4 2023, Taiwan Semiconductor (TSM), ASML's largest customer, decided to temporarily delay equipment deliveries as a cost-cutting measure while gaining a better understanding of customer demand, which now seems to be recovering.

Samsung's ( SSNLF ) $17 billion chip fabrication plant in Taylor, Texas, originally planned for mass chip production in the second half of 2024, will now be delayed until sometime in 2025, according to the original report. This delay is attributed to Samsung's concerns over the U.S. government's slow release of funds promised through Biden’s CHIPS Act. Under this Act, semiconductor firms are eligible for subsidies when committing to build new facilities in the U.S. However, only $35 million has been awarded out of the promised $52 billion, leading to concerns in the industry.

The decision to postpone mass production mirrors a similar announcement by Samsung's main chipmaking rival, TSMC, which stated it would delay production at its new Arizona fab until 2025 due to a shortage of construction workers and machine installation technicians. Both facilities are expected to use ASML's equipment to produce high-end chips. It's important to note that ASML can only recognize revenue for the sale once the machines are successfully delivered to the customer.

At the same time, both in Q2 and Q3 of 2023, China played a pivotal role in ASML's earnings, contributing to 46% of new system sales in Q3—a sharp increase from 24% in Q2 and 9% in Q1. The reason is straightforward: while delays in new fabs in the U.S. and Europe led to reduced sales in these regions, China has been striving to import as many devices as possible before access to ASML's top-tier DUV machines becomes restricted. EUV machines are completely banned from being shipped to China.

Starting from January 1st, top-tier DUV machines are now restricted for sales to Chinese companies, meaning Q4 will likely see a large chunk of China sales as a percentage of the total, squeezing in the last possible orders.

However, 2024 is expected to be impacted by these restrictions, as the license for the shipment of NXT:2050i and NXT:2100i lithography systems in 2023 has recently been partially revoked by the Dutch government.

The updated export restrictions would affect between 10% and 15% of the firm’s sales to China, as mentioned by ASML Chief Executive Peter Wennink during an earnings call in October. While I expect these to be offset by other areas, it will be a drag on growth.

Valuation

In the past 15 years, ASML's average blended P/E ratio has been 37.12x.

Today, the stock is trading at a blended P/E ratio of 34.72x. Naturally, the stock is no longer as inexpensive as it was last October, having surged by 24% since I recommended buying it when it dropped to 30x its earnings.

{kind=link}

Perhaps, for some investors, today's valuation might seem a bit high, and naturally, there isn't much margin of safety if execution were to stall.

Considering that the management has indicated 2024 to be a transitory year, we should not expect significant growth.

However, beyond that, the outlook appears promising.

- 2024 : 21.03E EPS, 2% YoY growth

- 2025 : 29.14E EPS 39% YoY growth

- 2026 : 33.97E EPS 17% YoY growth.

Despite the slow growth expected in 2024 due to delays in building new fabs and China sales-related restrictions, we should not overlook the bigger picture of growth. The average CAGR for EPS growth in the next 3 years is projected to be 18.2%.

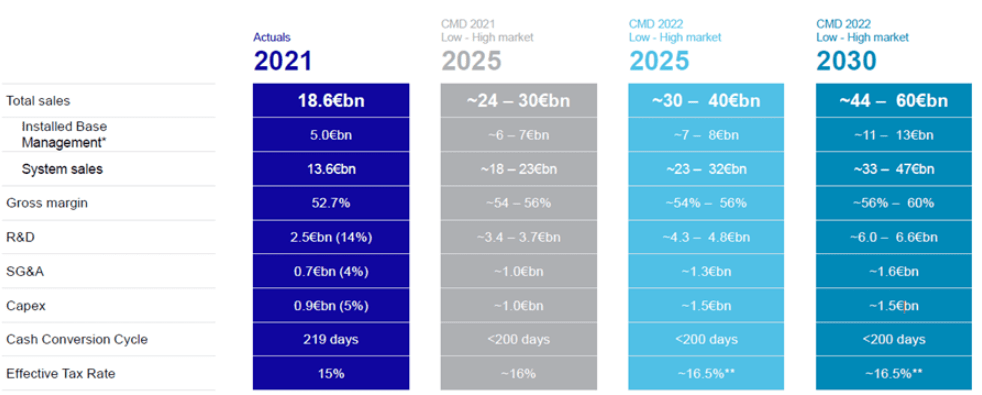

Management has also confirmed their commitment to long-term guidance, projecting sales to reach between €44 to €60 billion by 2030. This marks a significant increase from the €27 billion projected to be reported for the full year 2023.

{kind=link}

The EPS growth over the past 10 years has been 22.7%, and analysts are anticipating the growth to continue at a slightly slower rate. Given the strong growth outlook, yet a slight deceleration, I expect ASML should be trading closer to 35x its earnings, lower than its 10-year average of 37.12x.

If the projected growth materializes, and the valuation does not contract from today's level, we could potentially see total returns of around 19.6% annually over the next 3 years.

Return Potential (Fast Graphs)

{kind=link}

While ASML is no longer a bargain as it was just 3 months ago, I still rate it as a BUY due to its superior quality and the potential for close to double-digit returns.

Takeaway

With its monopoly-like EUV technology, ASML has experienced rapid growth over the last couple of years, capitalizing on the increasing digitization of the world and emphasizing the importance of chip production for national security.

Benefiting from the tailwinds of growing chip production and the establishment of fabs in the US, Europe, and Japan, ASML is a company at the forefront, providing key machines to these new factories.

As the economy recovers and chip demand becomes more predictable once again, I anticipate that ASML will report solid Q4 earnings, surpassing the initial guidance provided by the management.

Moreover, although the management has designated 2024 as a transitory year due to delays in fabs and China sales restrictions, the company is well-positioned for growth in the following years, with an expected EPS growth of 18.2% CAGR over the next 3 years.

At today's valuation, ASML may not be cheap, but it still presents compelling value with the potential for double-digit returns.

For further details see:

ASML: Should You Buy The Stock Heading Into Q4 Earnings?