ASOMF - ASOS: 'Driving Change' To Reiterate Buy

2023-10-17 10:56:37 ET

Summary

- ASOS is focused on reducing its inventory levels to pre-COVID levels by FY24, with progress already made through its Driving Change agenda.

- The company reported a decline in Q4 trading, but we expect sales growth and improved gross margins in H2'24.

- ASOS trades at a favorable valuation compared to its peers, but risks include elevated inventory levels and competitive pressures.

Investment Thesis

In continuing with our coverage of ASOS Plc (ASOMF), we had rated the stock a Buy driven by its improving profitability and rightsizing of inventory levels under its Driving Change agenda, strong cash generation efforts and relative valuation comfort. The company continues to make meaningful progress to its elevated inventory levels and remains committed to bringing it down to £600 mn by FY24, in line with its pre-COVID levels. We believe the company is likely right prioritizing the clearing of its older inventory for long term gains, as well as making substantial progress through its Driving change agenda to improve profitability per order and accrued cost savings worth £300 mn this year. We reiterate our Buy rating driven by 1) Gross margin expansion with the worst likely to be over by H1'24 and company being able to rightsize its inventory during the first half itself 2) Freight costs tailwinds and improvement in distribution due to lower inventory handling costs 3) New assortment of products driving sales growth in H2'24 and 4) Balance sheet improvement as a result of lower debt driven by shrinking inventory

Short Term Pain for Long Term Gains

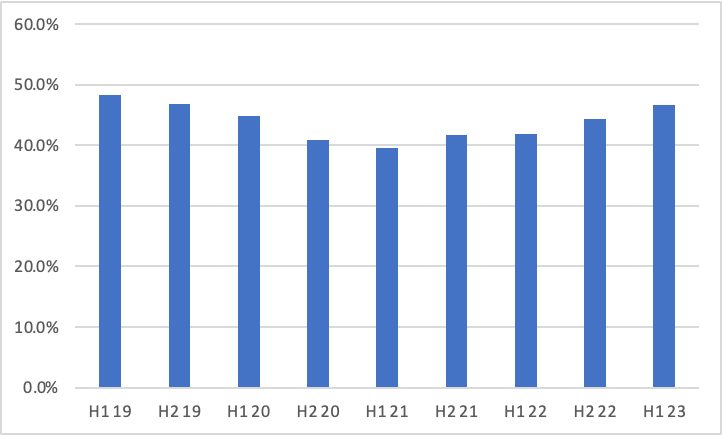

ASOS reported soft Q4 trading with constant currency sales down 15% YoY (excluding the 3 percentage point contribution from the additional 3 days) with net revenues declining 12% YoY below consensus estimates. The decline was driven by broad base declines across regions with RoW being the weakest, declining 26% YoY while US declined in high teens, UK declining in low teens and Europe faring relative better, down mid single digits. The decline is in line with the management's guidance of a low double-digit decline. Adj. Gross margin came in at the lower end of the guidance, up 150 bps, as lower freight was partially offset by investments in promotion to clear its older inventory.

It guided that H2 Adj. EBIT would be at the lower end of its £40 - £60 mn range while expected FCF inflow of £60 mn compared to £150 mn in guidance as a result of timing differences, primarily on working capital which we expect to phase in H1 24, as well as weaker than expected sales. In addition, management maintained that the discount is likely to persist throughout FY24E as it looks to clear its autumn/ winter collection from last year which remains their oldest inventory, as it continue to prioritize inventory rebalancing. What remained noteworthy is the inventory position continues to improve down over 30% YoY ahead of the -20% guide and remains on track to <£600 mn in inventory by FY24. Order profitability was up 35% as a result of continued targeted action on its least profitable customers.

FY24 Expectations 'Driving Change'

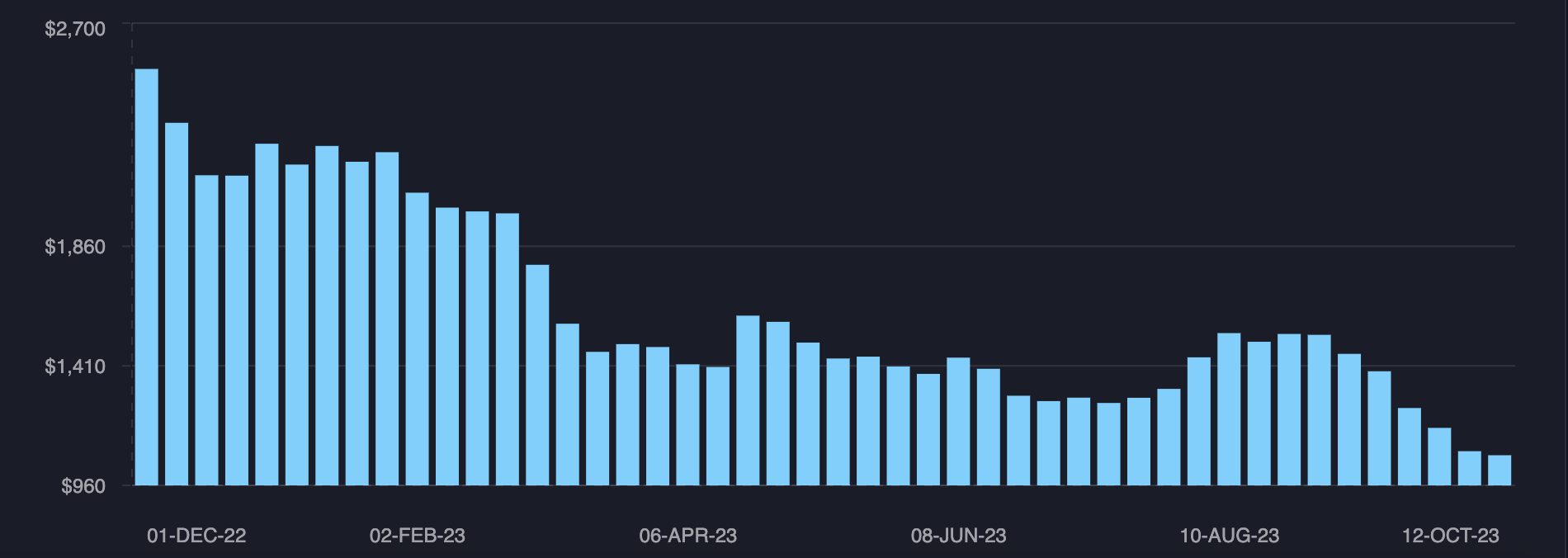

The company has delivered £300 mn in cost savings through its Driving Change agenda which has largely been offset by higher input costs, distribution costs due to elevated fuel costs along with adverse Fx. We believe the company is likely to benefit from lower raw material costs (cotton and polyester) in FY24 which have been trending lower, with cotton spot down double digits. Opex to sales costs have trended higher largely as a result of an increase in warehousing and distribution costs.

{kind=link}

We believe the company is likely to have lower inventory handling costs going forward as a result of the clearance of its older inventory along with easing of gas prices and lower freight prices would lead to a meaningful expansion of its gross margins in 2024.

{kind=link}

ASOS' focus on driving clearance of old inventory along with lower new assortment of products has led to a declining sales in FY23. We believe the company is likely to report a low single to mid single-digit declines in revenues for FY24 with the most of the pain experienced in Q1. The decline in sales during H1 would likely be partially offset by positive sales growth in H2 as the company completes its rightsizing of the inventory and bring its inventory levels under £600 mn (management's guidance for the year) as H1 generally has lower inventory levels. The growth in H2 would be driven by the newness in its assortment with initiatives like 'test to react' after the old Autumn/ Winter inventory clearance helps them back to growth ways.

Its net debt has increased substantially along with its burgeoning inventory levels since late 2020/ beginning of 2021. We believe with the rightsizing of the inventory the company will be able to lower its net debt meaningfully as well as bring in new inventory which will drive sales growth as well as improve its gross margins meaningfully.

Valuation

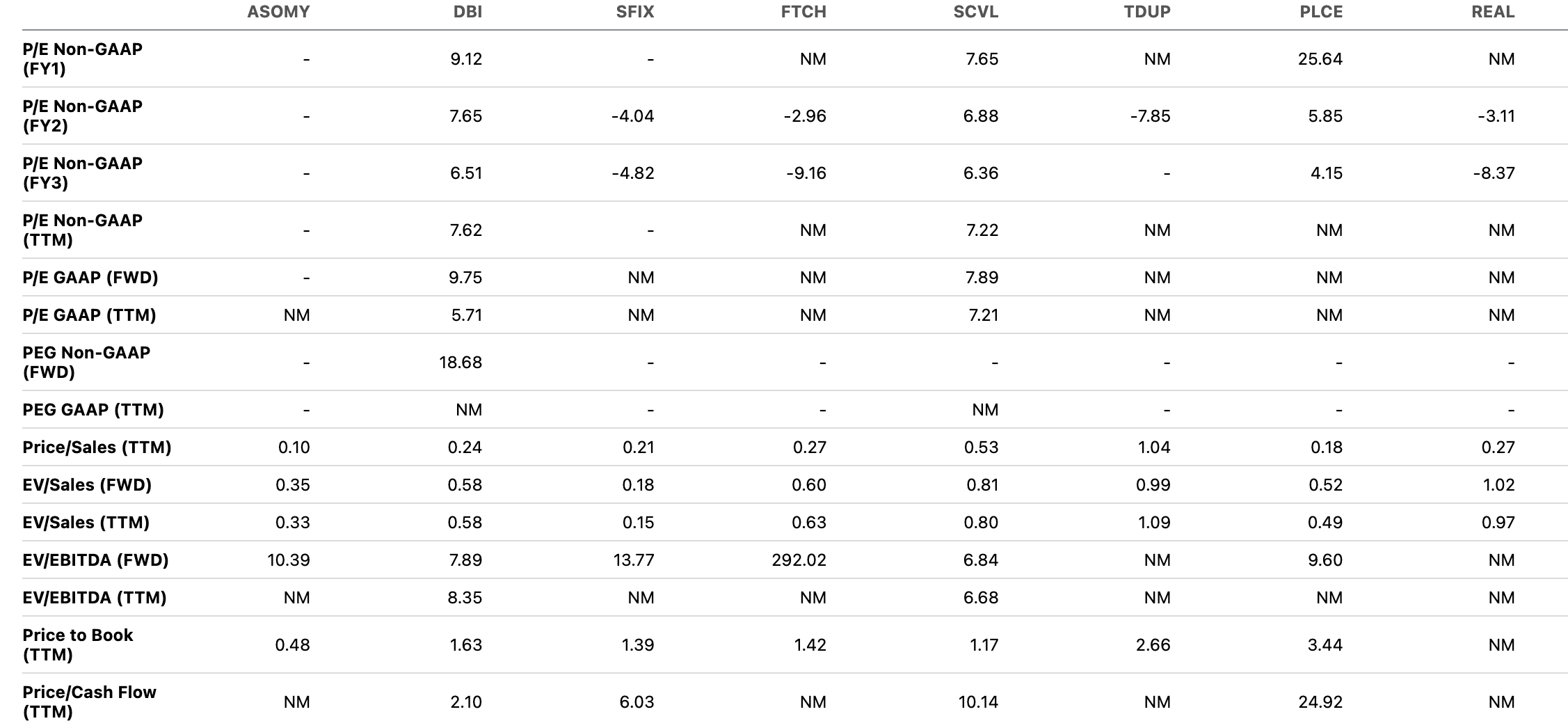

ASOS trades at 0.3x EV/ Fwd Sales and ranks second to best compared to other peers. In addition, from an EV/ Fwd EBITDA perspective, it trades at ~10.4x and ranks among the middle quartile compared to its peers. We believe the expectations are currently lower due to soft Q4 with overhang of the older inventory

{kind=link}

Risks to Rating

Risks to rating include

1) Elevated inventory levels and its inability to bring down the inventory levels profitably could lead to pressure on gross margins

2) Macroeconomic conditions can lead to a decline in consumer discretionary spends and dampen sales growth

3) Competitive pressures from other online retailers such as Zalando and Shein as well as other retailers with their own omni channel offerings can lead to higher promotional activities and further delay its path to profitability

Final Thoughts

We believe ASOS had made meaningful progress over the past year through its Driving change agenda focus on rightsizing its inventory levels and improving its profitability per order which has been trending higher throughout the year. We believe with most of its inventory levels balanced out, the company is likely to report positive sales growth and substantially higher gross margins for the latter half of FY24. In addition, its driving change agenda has been a major contributor to its operating margins which has been offset by higher distribution costs, lower sales and old inventory. We believe with easing of freight, raw material costs as well as lower handling costs, the driving change would further contribute about £50 - 100 mn in cost savings which will yield to operating profits of over £60- 80 mn for FY24, consensus at the lower end of the guide. We Reiterate our Buy rating driven by management's focused approach on inventory at the cost of near term pain on gross margins, improvement in cash generating efforts and relative valuation comfort.

For further details see:

ASOS: 'Driving Change' To Reiterate Buy