ASPN - Aspen Aerogels: A Mixed Bag

Summary

- Aspen Aerogels continues to grow revenue nicely, but profits and cash flows are a major issue.

- To address this, management engaged in a highly-dilutive capital raise and it secured a loan with rather onerous terms.

- This creates a risky prospect that could offer strong upside or significant downside that investors need to be careful with.

One of the most unique companies I've come across in recent years is a firm called Aspen Aerogels ( ASPN ). As its name suggests, the company focuses on producing aerogels and related products. For the most part, the aerogels that it produces are high-performance aerogel insulations that can be used in the energy infrastructure and building materials markets. This was all based off their initial offerings, released in 2008, called Pyrogel and Cryogel. Since then, the company has diversified its product line and is continuing to focus on growth. Unfortunately, though, this is not the kind of play that most value investors would find appealing. Although growth has been reasonable recently, profits and cash flows are increasingly negative. Admittedly, the company did just raise a rather significant amount of capital. That should give it a good deal of time with which to push toward cash flow neutrality. It also serves as a vote of confidence that has gone over quite well with the investment community. In the near term, it wouldn't be surprising to see this narrative continue to drive shares higher. But until the company can demonstrate true improvement on its bottom line, it's a play that is too risky for my book.

Reward mixed results with strong upside

Back in early July of 2022, I found myself asking the question of what the future looks like for Aspen Aerogels. At that time, the company was going through something of a whiplash after initiating a rather large but massively dilutive capital raise only to then cancel it in response to the market’s reaction. The reaction in question was a 47.9% plunge in the company's share price in only two days. Since then, the company has been recovering slowly. Furthermore, it took the opportunity late last year to finally raise the capital it had sought. This much-needed infusion is a positive in and of itself because the cash outflows being experienced by the firm were otherwise unsustainable. But just as was the case with the prior raise, this infusion came at a rather lofty cost.

Of course, I could not have known when I wrote my article in July what all would have transpired. After all, I am no fortune teller. In general though, I found myself impressed by the company's sales growth but I was turned off by management's stumble and the continued cash flow problems of the enterprise. In response to these issues, I ended up rating the company a ‘hold’ to reflect my view that shares probably would not generate any significant performance for the foreseeable future. But so far, the market has proven me wrong. While the S&P 500 is up 3% since the publication of the aforementioned article, shares of Aspen Aerogels have generated upside of 11.8%.

{kind=link}

Author - SEC EDGAR Data

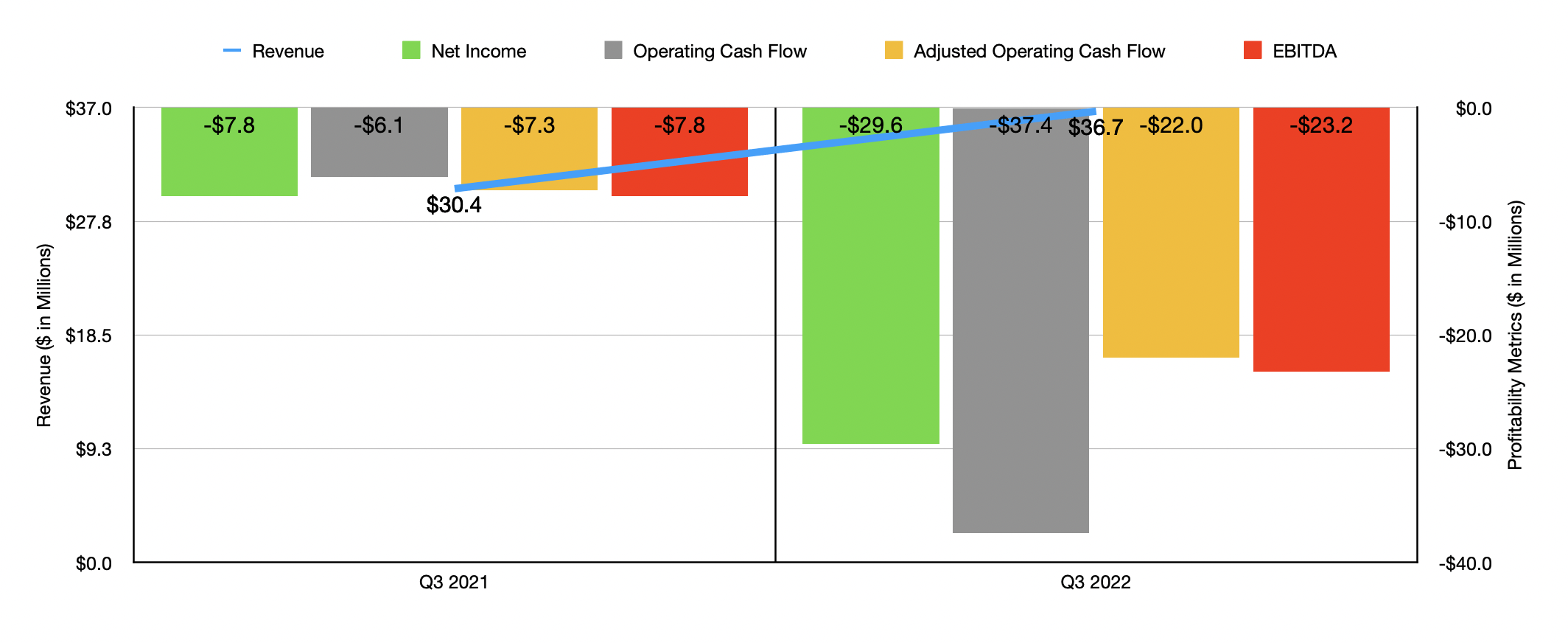

In evaluating whether or not Aspen Aerogels make sense for investors to buy into, it would be helpful to understand how its fundamental performance has been in recent quarters. For the third quarter of 2022 on its own, for starters, revenue came in at $36.7 million. That's 20.7% above the $30.4 million reported the same time one year earlier. Management attributed this growth increase pretty much entirely to increased demand for the company's thermal barrier and energy industrial products. Interestingly though, energy industrial product shipments, as measured by square feet, actually declined by roughly 12% year over year. Where the company made-up for this was a 16% increase in the pricing per square foot of its energy industrial products. Thermal barrier revenue, meanwhile, roared higher from $1.2 million to $30.3 million in response to two major US automotive OEMs and a major Asian automotive OEM.

Although revenue increased for the company, profits for the firm plunged. Net income went from negative $7.8 million to negative $29.6 million. This decline, management said, was largely attributable to a 66% surge in cost of revenue for the firm. This mostly came from $46.2 million increase associated with thermal barrier sales. This, management said, was driven by a $14.3 million impact caused from higher material costs and a $31.9 million impact associated with manufacturing. Unfortunately, other profitability metrics followed a similar trajectory. Operating cash flow went from negative $6.1 million to negative $37.4 million. Even if we adjust for changes in working capital, it would have worsened from negative $7.3 million to negative $22 million. And over that same window of time, EBITDA for the company went from negative $7.8 million to negative $23.2 million.

{kind=link}

Author - SEC EDGAR Data

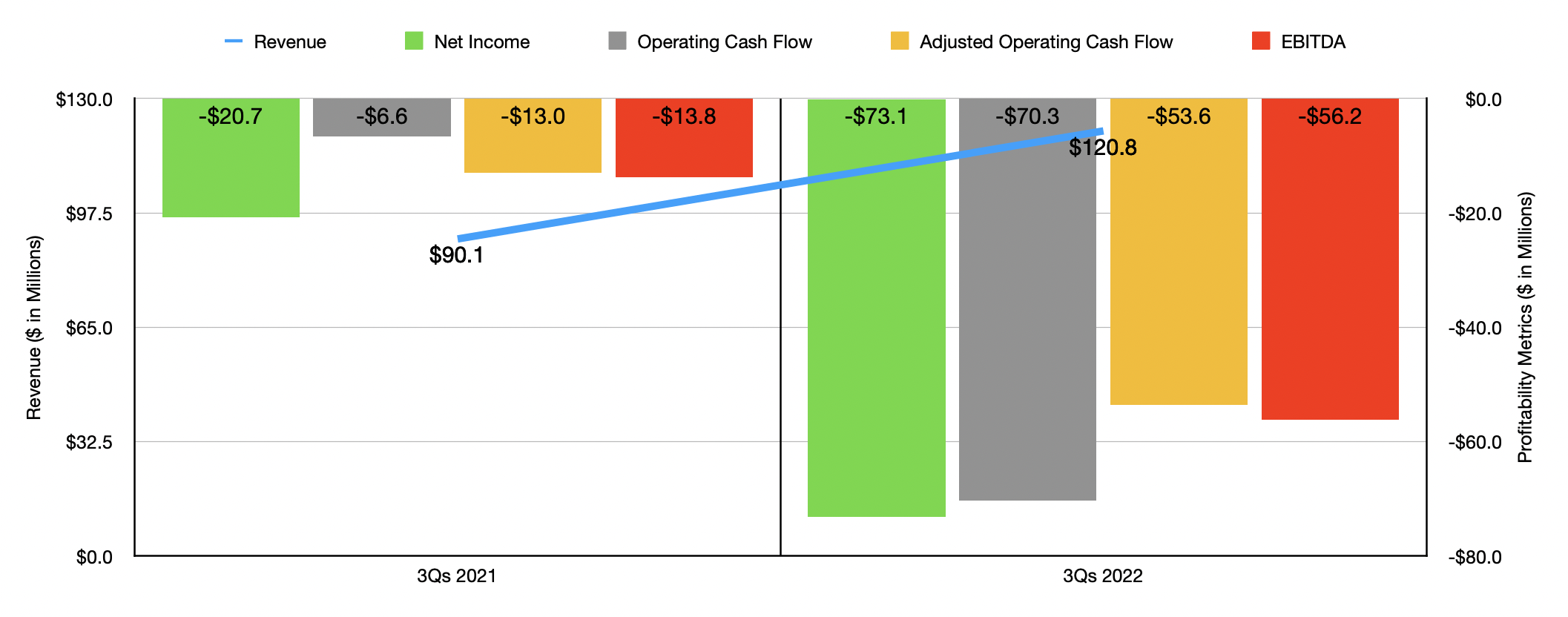

The story told by the results from the company's third quarter is the same story told when looking at the first nine months of the year as a whole. Revenue of $120.8 million dwarfed the $90.1 million experienced one year earlier. The firm's net loss expanded from $20.7 million to $73.1 million. Operating cash flow went from negative $6.6 million to negative $70.3 million, while the adjusted figure went from negative $13 million to negative $53.6 million. What's really awful is that management expects pain to persist through the entirety of 2022. Although revenue is expected to be around $180 million for the year, which would be 48% above the $121.6 million reported only one year earlier, profits and cash flows should worsen materially. In 2021, the company generated a net loss of $37.1 million. The loss for 2022 in its entirety should be between $82.3 million and $86.8 million. Meanwhile, EBITDA should go from negative $26 million to between negative $57.5 million and negative $62 million. No guidance was given when it came to other profitability metrics. But odds are, operating cash flow will also be negative to a rather significant degree.

As of the end of the third quarter, the company did have cash on hand of $102.4 million. At the same time, however, it had debt, admittedly convertible debt, of $105.2 million. But with cash outflows as significant as what we saw in the first nine months of 2022, the amount of cash the company had could only last it a short time. To rectify this, management initiated a couple of transactions. The first of these was a $100 million loan facility from Koch Investments. However, the terms of that debt are far from great. The debt can only be tapped under certain circumstances, with the first $33 million achievable only in the event that Koch Investments ends up buying $100 million or more of the company's stock. It also carries an annual interest rate north of 8%, with an in-kind option that comes in north of 9%.

Toward the end of 2022, management achieved the requirement of raising $100 million from Koch Investments when that party, through another firm, invested in a $240 million stock issuance for the enterprise. This massively dilutive transaction was all but necessary. And it resulted in net proceeds to the company of nearly $234 million. There is the option for another $36 million, on a gross basis, if the underwriter's option was exercised in full. But we don't know whether that was the case or not.

{kind=link}

Author - SEC EDGAR Data

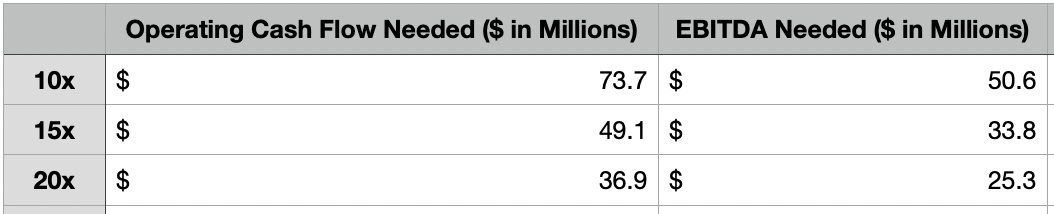

Now that the company has a sufficient amount of cash to hold it over, the next question would be whether or not it makes sense for investors to buy into. I'm not always opposed to buying companies with negative earnings and cash outflows. But I need to make sure that the company's fundamental data is even in the ballpark of achieving cash flow that would justify its current valuation. As you can see in the table above, there are three different scenarios for investors to consider. The first is that the company is worth 10 times either operating cash flow (on a price to operating cash flow basis) and 10 times EBITDA (on an EV to EBITDA basis). The second calls for the multiple to be 15, while the third calls for it to be 20. In the event that the company can scale cash flow figures to be at or above where the table demonstrates, then shares would be fairly valued in theory. But given recent developments with significant cash outflows, I have my doubts.

Takeaway

From a business model perspective, I really do think that Aspen Aerogels is an intriguing company. Having said that, this does not mean that it makes sense to invest in the firm at this time. It very well could see some nice upside in the months or years to come. But to me, the gap to bridge between how much cash flow needs to be generated versus how much in outflow we are currently experiencing, leads me to be somewhat pessimistic about the company. This pessimism is, however, offset to some degree by the vote of confidence the firm has received from other parties like Koch Investments, and by the fact that the company now has a great deal of cash and is growing at a nice clip. All combined, this gives me a rather neutral feeling that makes a ‘hold’ rating appropriate at this time.

For further details see:

Aspen Aerogels: A Mixed Bag