ASPN - Aspen Aerogels: No Reason To Be In A Hurry Ample Headwinds In 2023

Summary

- Aspen Aerogels: With plenty of headwinds in 2023, there is no reason to take a position in this stock at this time.

- Since November 2021, the company's share price has plunged, and there are no visible, short-term tailwinds to support the company if things get worse.

- With the company sticking to its guidance, a lot of things will have to go right and problems solved if it has to have a chance of meeting expectations.

Aspen Aerogels, Inc. ( ASPN ), which designs, develops, manufactures, and sells aerogel insulation products targeting the energy infrastructure and building materials markets, more than tripled its share price starting on May 17, 2021, when it was trading at approximately $18.00 per share. It then soared to about $66.00 per share on November 22, 2021, before collapsing to a 52-week low of $7.93 on June 27, 2022.

After that low it has since rebounded to trade in the mid-$10s as I write. From its June 2022 low till now, it has traded in a range of close to $9.00 per share to $14.00 per share, with no visible catalyst that would point to a potential breakout.

{kind=link}

The company noted that its performance has been somewhat disrupted from the supply chain, inflation and high interest rates affecting the cost of capital over the last year or so. That's of specific importance because it has had an impact on its Plant 2 project in Georgia, which will probably take longer than expected to complete, and will likely cost more than originally thought.

With the factory, which is being designed to be a top-of-the-line aerogel manufacturing facility, expected to be a big part of the company having a chance at meeting its guidance of generating $720 million in revenue in 2025, it's imperative that it doesn't fall too far behind schedule if the company has a chance at achieving its revenue goal.

Taking into consideration the dilution associated with its recent stock offering, supply chain constraints, challenges relating to completing its new facility, and the macro-economic issues like inflation and high interest rates, there isn't anything I can see that will mitigate those issues in the short term that will allow the company to break out of its recent share price range and return to sustainable growth.

In this article we'll look at its recent quarterly numbers, some of its guidance, and why I don't think there's any hurry to take a position in the stock because likely to take another big dip before finding a bottom.

Recent numbers

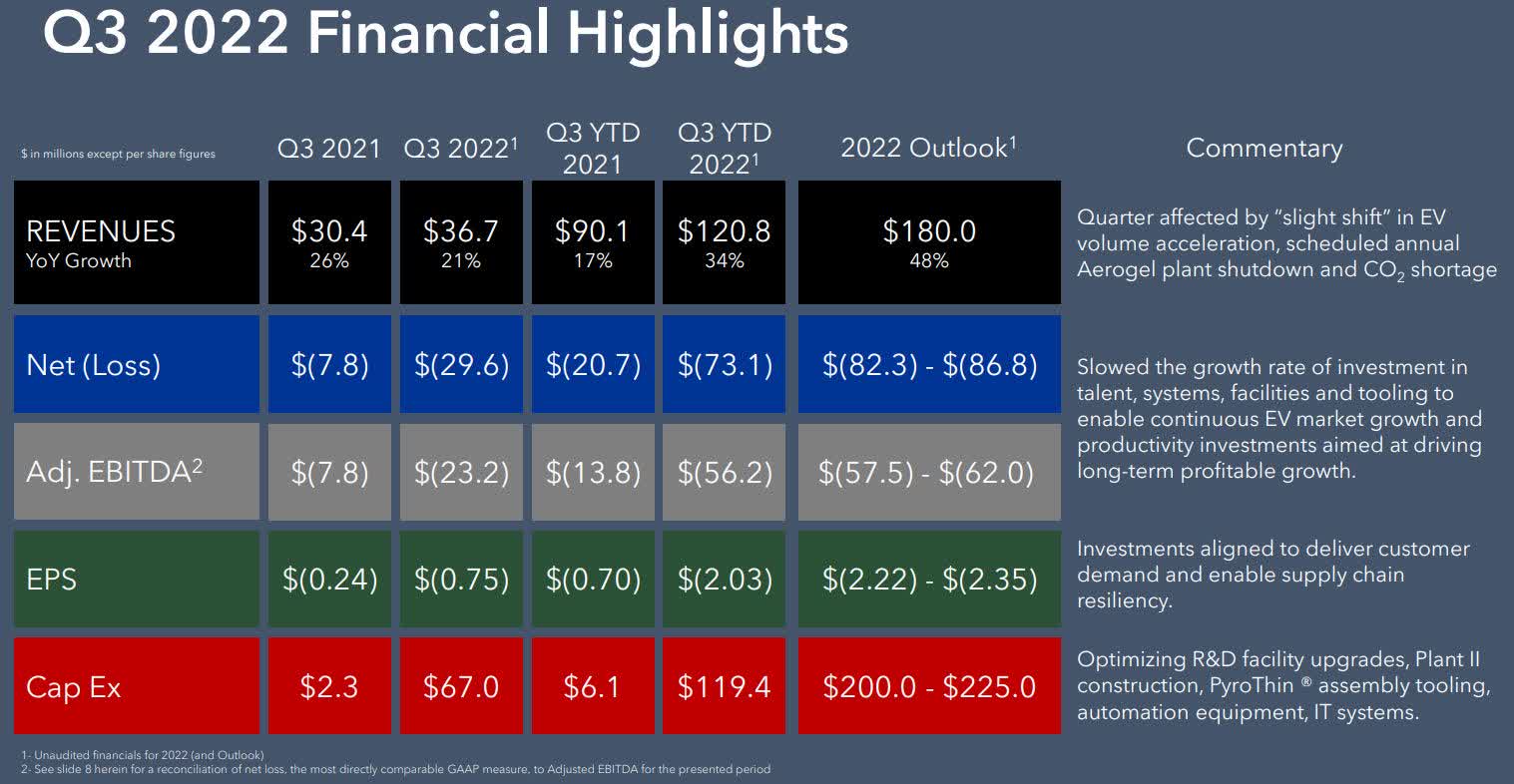

Revenue in the third quarter of 2022 was $36.7 million, an increase of 21 percent over the revenue of $30.4 million in the third quarter of 2021. Revenue in the first nine months of $2022 was $120.8 million, compared to revenue of $90.1 million in the first nine months of 2021.

{kind=link}

EV thermal barrier revenue in the third quarter was $11.9 million, up 11 percent sequentially, and about 12 times what it was in the third quarter of 2021.

Revenue from energy industrial was $24.7 million, down 16 percent from the same reporting period last year, and down 29 percent sequentially. The decline in revenue from the segment came from nationwide CO2 shortages and its prescheduled annual plant shutdown.

In order to mitigate potential future disruptions associated with CO2 shortages, the company added storage capacity on site, as well as using its own trailers to transport some of it.

With material expenses accounting for approximately 57 percentage points of sales, which is over 10 percentage points higher than the company wants it in the future, it has taken some immediate steps to lower material costs. Included in that initiative was phasing out a complex part design as the company moves toward higher volumes, while transferring assembly of its EV thermal barrier products from Rhode Island to Monterrey, Mexico, because of higher scrap levels and the ability of the Monterrey facility to process higher volumes.

Unfortunately for the company, the move was frustrated by a drop in demand from its three automotive customers it was supplying, resulting in a drop in volume for its EV thermal barrier products.

Consequently, the drop in demand ended up with gross margin in thermal barrier of negative 70 percent, down from negative 67 percent in the prior quarter, which meant it wasn't able to absorb fixed costs of about $12.9 million, resulting in the company not being able to generate momentum toward lowering percentage of sales by improving its absorption of fixed costs.

Net loss in the reporting period soared to $29.6 million, or $0.75 per share, compared to a net loss of $7.8 million, or $0.24 per share in the third quarter of 2021. Net loss for the first nine months of 2022 was negative $(73.1) million or negative $(2.03) per share, compared to the net loss of $(20.7) million or negative $(0.70) per share in the first nine months of 2021.

Adjusted EBITDA in the third quarter of 2022 was negative $(23.2) million, compared to negative $(7.8) million in third quarter of last year.

Cash flow from operating activities in the reporting period were $44.7 million, which included $44.9 million in net proceeds from its ATM offering at an average price of $10.63 per share.

At the end of the third quarter of 2022, the company had cash and cash equivalents of $102.4 million. As for guidance, management looks for revenues of $180 million for full-year 2022, with a net loss in the range of $82.3 million to $86.8 million, and adjusted EBITDA in a range of $57.5 million to $62 million.

CapEx for all of 2022 is projected to be from $200 million to $225 million.

Current and future headwinds

The company added some caveats concerning its ability to deliver over $59 million in revenue in the fourth quarter of 2022, which I believe will remain in place for at least the first half of calendar 2023.

Concerning the two major headwinds in meeting revenue guidance in the near term and long term, they remain ongoing CO2 shortages and the tight labor market, especially at the local level at its aerogel facility in Rhode Island. Another significant challenge outside the company's control is whether or not its customers will be able to maintain production volumes going forward, as mentioned earlier. There are also the ongoing supply chain constraints in relationship to foundational raw materials beyond CO2, including batting and silanes.

In order to at least partially mitigate supply chain issues, the company has added storage capacity for silanes and batting so it can execute on its production goals.

With a lot of its guidance heavily dependent on its Plant 2 project, the combination of headwinds is a significant barrier accomplishing its revenue goal of $720 million in 2025. My thought on that is the company, in my opinion, is overly aggressive and optimistic with the $720 million revenue goal. The key thing is to get the project completed and running at full capacity. If it does fall behind in the construction phase, investors are smart enough to know it's only a delay.

It would of course temporarily be a hit to the share price of the company if it's not completed in a timely manner, but as long as it eventually completes it within a reasonable time frame, I think it shouldn't be a drag on the company.

Now that it has raised $200 million in capital via a stock offering, and an additional $100 million in a secured loan agreement with General Motors affiliate, it has the capital in place to complete and launch operations at its aerogel manufacturing facility in Georgia.

Through the third quarter of 2022 ASPN has invested $129.4 million in Plant 2.

Conclusion

Based upon the headwinds mentioned in the article in the near term, I don't see a reason at this time to take a position in ASPN, as it's highly unlikely it'll be able to successfully mitigate them to the point it makes a difference in its performance.

More than likely, they're going to remain significant headwinds in 2023, and I see the share price of ASPN having a much higher chance of dropping further before it finds a bottom, and I'm not including the potential effects of a weakening economy and higher interest rates when developing that thesis.

Taking those into consideration, it looks even more challenging for ASPN, although raising the additional capital, even though it diluted shareholders and will also add expenses, it needed to be done to give the company a chance at regaining momentum sometime in the future.

As for the long term, I think the company could get a lift once its Plant 2 is completed. Depending on the economic conditions and remaining headwinds at the time, that may or may not hold in regard to its share price.

Once the economy starts cooperating and the headwinds are mostly mitigated, ASPN has a chance to enter a sustainable growth stage which will probably reward patient shareholders.

But for now, for those interested in taking a position in the company, I think waiting to see how things unfold and whether or not there's more downside would be the prudent thing to do, as there are far too many negative catalysts in play to comfortable take a position under the current circumstances and share price, in my opinion.

For further details see:

Aspen Aerogels: No Reason To Be In A Hurry, Ample Headwinds In 2023