AZPN - Aspen Technology: A Solid Long-Term Bet But Not At Current Stock Price

2023-07-28 13:42:40 ET

Summary

- Aspen Technology is leading in its niche, but financial performance is still volatile.

- The company demonstrates solid revenue growth but frequently misses quarterly consensus revenue estimates, making it a risky investment prior to the upcoming quarter's earnings release.

- My valuation analysis suggests the stock is overvalued.

Investment thesis

Aspen Technology's ( AZPN ) stock trades with a substantial premium to its fair value, according to my analysis. The company is well-positioned in its niche, and AZPN's offerings create significant customer value. But profitability metrics are volatile, and the company frequently misses consensus estimates. AZPN might be a good long-term bet, but my valuation analysis suggests that better buying opportunities will likely be ahead. Therefore, I assign AZPN a "Hold" rating .

Company information

Aspen Technology is an industrial software company developing solutions for complex industrial environments. The company's offerings help users to optimize their manufacturing processes for maximum performance. According to th e latest 10-Q report from May, AZPN operates globally in 82 countries.

The company's fiscal year ends on June 30 with a sole operating and reportable segment. During the nine months that ended March 31, 2023, AZPN generated about half of its revenue outside the Americas.

{kind=link}

It is important to note that Emerson Electric Co. ( EMR ), which is AZPN's parent company, owns 55% on a fully diluted basis as of March 31, 2023. On October 10, 2021 , EMR entered into a definitive agreement with AspenTech Corporation to contribute the Emerson industrial software business and $6.014 billion in cash to create AZPN [the Transaction]. The Transaction closed on May 16, 2022.

Financials

Over the last four years, AZPN demonstrated a solid revenue growth of about 41% CAGR, but profitability metrics below the gross profit were volatile. Last full fiscal year's free cash flow margin [FCF] ex-stock-based compensation [ex-SBC] was negative.

Author's calculations

There is a big gap between the gross and operating profitability partially because of heavy investments in R&D. The R&D to revenue ratio has moderated recently but is still in double digits. I think this is a good sign of the management's long-term approach to creating shareholder value. On the other hand, the fact that revenue has more than doubled over the last four years did not help much in the improvement of the SG&A to revenue ratio.

The balance sheet looks healthy, with vital liquidity metrics and low leverage. As of the latest reporting date, the company had substantial net cash of $200 million. The company does not pay dividends and prefers to reinvest positive cash flows from operations to innovation.

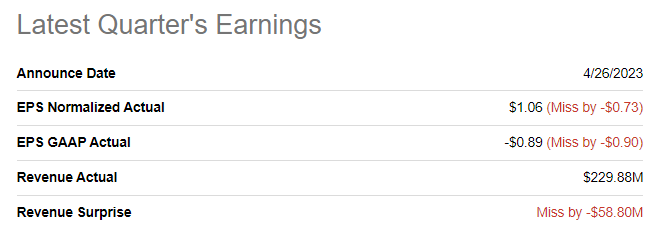

The latest quarterly earnings were released on April 26 , when the company significantly missed consensus estimates. The EPS contracted YoY from $1.38 to $1.06 despite the 22% YoY growth for the top line.

{kind=link}

I like that the revenue growth was solid in the latest quarter, even amid the uncertain environment of cautious business spending. Annual contract value [ACV] returned to the double-digit growth path, which is also strong. Overall, revenue growth was due to the Transaction. The business combination also helped to expand the gross margin from 48% to 59%.

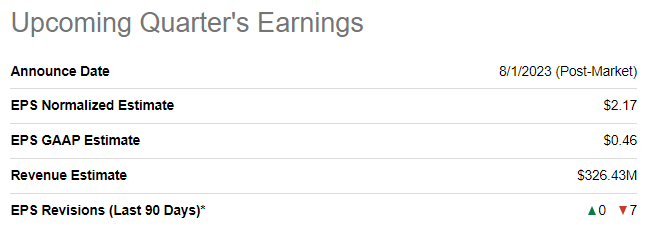

The upcoming quarter's earnings release is planned on August 1. Revenue growth still has strong momentum, with the upcoming quarter's sales expected to demonstrate a 36% YoY growth. On the other hand, consensus estimates forecast the adjusted EPS to shrink YoY from $2.43 to 2.17.

{kind=link}

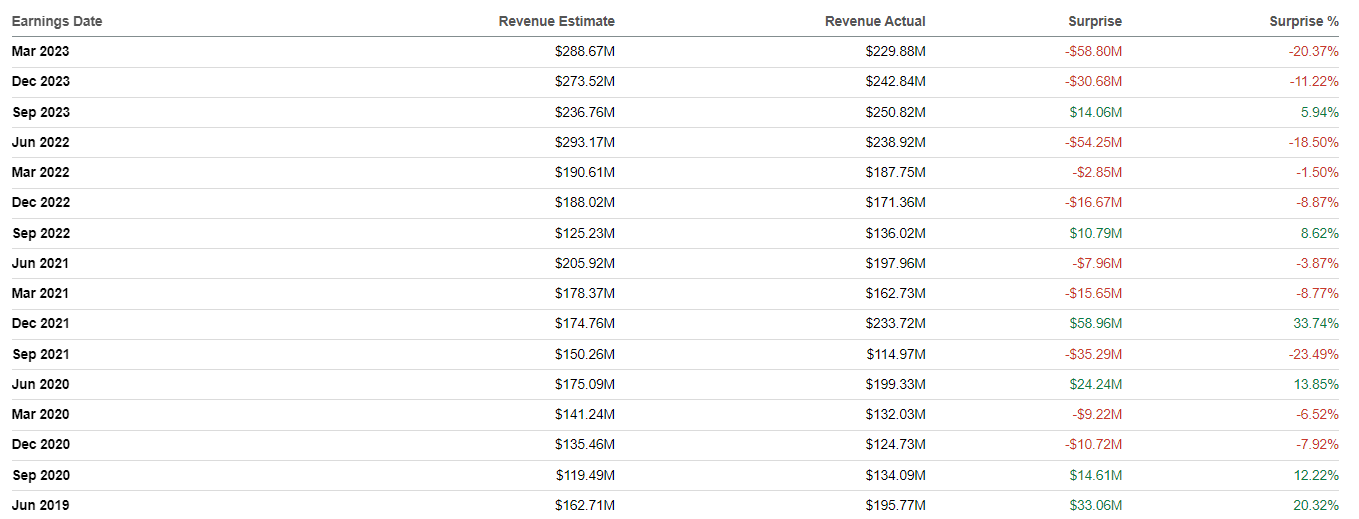

Since the upcoming quarter's earnings release is close, I think it is important to emphasize that the company has a weak track record of performance against consensus estimates. Especially that relates to the top line. Out of the 16 latest quarters, AZPN missed the consensus revenue forecast ten times. That said, buying the stock before the report looks like a fifty-fifty game.

{kind=link}

Overall, I believe that secular trends are favorable for AspenTech. Businesses strive to achieve higher profitability metrics by streamlining operations and eliminating inefficiencies. Aspen's offerings are aimed to help, and the revenue growth pace suggests that customers see big value in the software. I also like that the company invests substantial resources in R&D, which means the software will likely become more sophisticated and bring more value to customers. I also believe customers' switching costs are high, meaning AZPN has a solid competitive advantage. I do not like the unstable trend in profitability metrics, and I would like to see how the nearest quarters will unfold.

Valuation

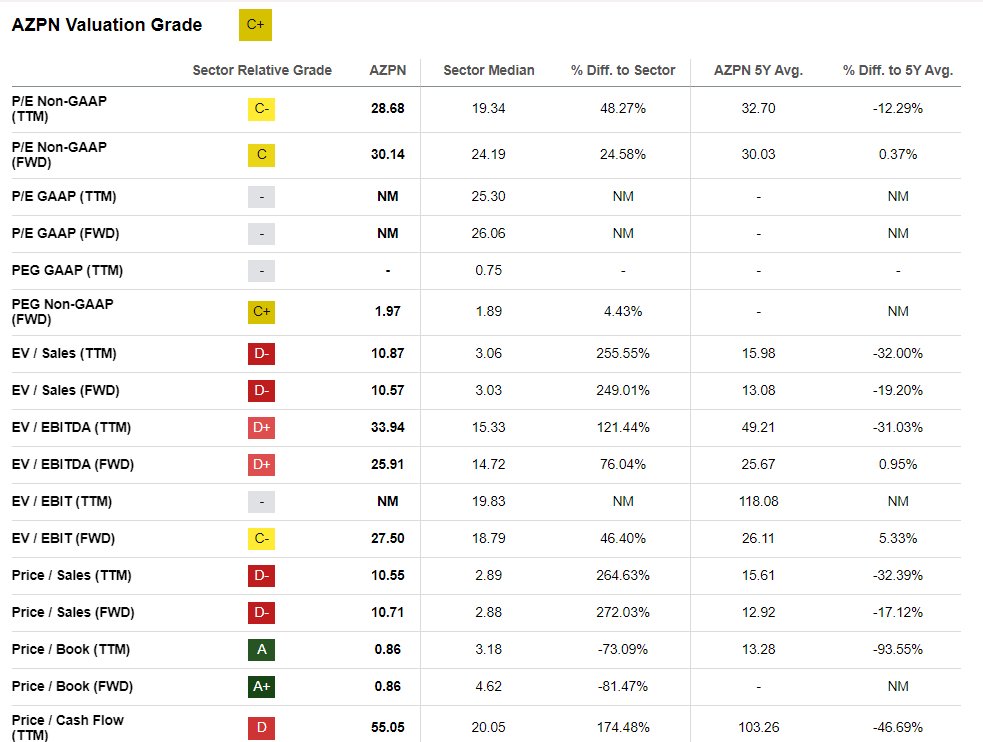

The stock significantly underperformed the broad market year-to-date with a 16% share price decline. Seeking Alpha Quant assigned AZPN a "C+" valuation grade, meaning the stock is approximately fairly valued. If we dig deeper into valuation multiples, we can see that price-to-book ratios are the ones that saved the day, with other ratios being substantially higher than the sector median. Therefore, based on the valuation ratios analysis, I believe AZPN looks overvalued. On the other hand, current multiples are mostly lower than the five-year averages.

{kind=link}

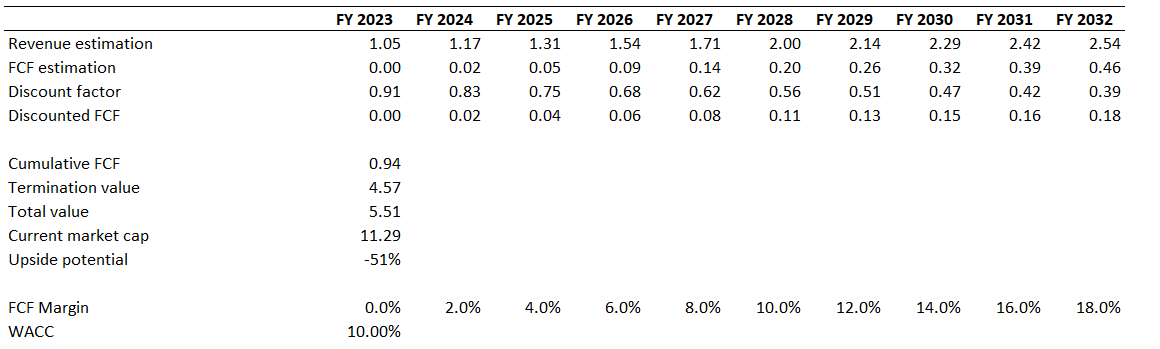

To expand my valuation analysis, I will proceed with the discounted cash flow [DCF] approach. I use a 10% WACC as a discount rate. Earnings consensus estimates forecast a 10% CAGR for the top line over the next decade, and I consider it conservative enough. From the FCF margin perspective, AZPN is still not generating sustainable positive figures, so I expect a zero from FY 2023. But I expect the FCF margin to expand by two percentage points yearly starting from FY 2024.

{kind=link}

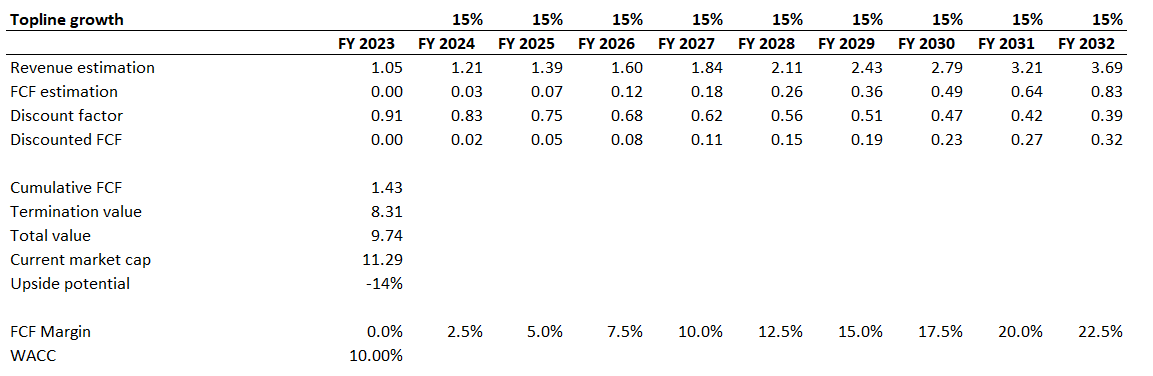

As you can see, the stock seems massively overvalued, with the business' fair value at $5.5 billion, about two times lower than the current market cap. Even if I implement a much more aggressive revenue CAGR of 15% and FCF margin expanding by 250 basis points yearly, AZPN still looks overvalued.

{kind=link}

The company's balance sheet is in good shape but does not have substantial net liquid financial assets, which can significantly affect the valuation. Of course, the company has a strong brand and its software is highly valued by customers. But the company still is not generating sustainable positive free cash flow [FCF], meaning the level of uncertainty regarding future FCF margin is high. That said, I believe the stock is significantly overvalued.

Risks to consider

AZPN is a growth company, and substantial revenue growth and profitability expansion expectations are priced in. If the company fails to deliver the expected financial performance, it is highly likely to lead to investors' disappointment and could ultimately lead to a stock sell-off. Several quarters of consistently strong financial performance might be required to regain investors' confidence and the stock price to recover the company's bright prospects. That said, the stock is a very risky investment for short-term investors.

The company operates internationally, therefore facing all risks inherent to global operations. First is the foreign exchange risk, meaning the company's earnings depend on currency exchange market fluctuations. Second is the challenge related to the diversity of the company's jurisdictions. That said, the company needs to allocate substantial resources to ensure that it complies with the regulations and laws of different countries. Failing to do so might lead to legal obligations and fines.

AZPN also faces high concentration risk because its revenue is heavily dependent on customers from energy and chemical processing customers. Very high volatility is inherent to these end markets, and these customers' financial health heavily depends on commodity prices, which in turn face significant geopolitical risks.

Bottom line

To conclude, AZPN is a "Hold". Of course, the company is highly likely to absorb favorable secular tailwinds, but the valuation looks too generous. Moreover, the company has a "rich" history of missing quarterly consensus earnings estimates, meaning that sell-offs will likely happen in the nearest quarters.

For further details see:

Aspen Technology: A Solid Long-Term Bet, But Not At Current Stock Price