AZPN - Aspen Technology Inc: Decent Growth But At A High Premium

2023-11-05 01:11:54 ET

Summary

- Aspen Technology Inc (AZPN) focuses on providing efficient solutions for asset optimization, but its stock is currently overvalued compared to sector averages.

- The markets that AZPN serves, such as digital grid management, offer potential for growth, but the company's revenue growth has slowed.

- AZPN faces risks from foreign exchange fluctuations and concentration in the energy and chemical processing sectors, as well as potential impacts from higher interest rates.

Investment Rundown

As more and more pressure is put on companies to be operating as sustainably as possible there has been a significant market opportunity for a company like Aspen Technology Inc ( AZPN ). The company focuses on providing efficient solutions to maximize the utility of assets or the operations performance for example. Over the years the company has grown quite well and is valued at over $11 billion as of now. The share price of the business has however been on quite a rollercoaster as we saw a significant drop back in late April following disappointing earnings results where the EPS came in at $10.3, a $0.73 miss. The company was also downgraded following that which further put downward pressure on the stock price.

Since then the share price has recovered quite well despite the last few week's quite hefty market sell-offs that have affected AZPN too. Even if the Q4 FY2023 report provided double-digit top-line growth and brought in a strong buyback program, I am not quite yet convinced the stock is a buy. AZPN still trades at quite a rich valuation in comparison to sector averages. The p/e is 35% above the sector and the p/fcf is 84% above. I don't see AZPN offering enough of a value price right now and it would have to drop to around the $150 range at least before I consider rating it any higher.

Company Segments

AZPN focuses on asset optimization. For years, AZPN has been at the forefront of empowering companies to operate with heightened safety, sustainability, and efficiency. The company's cutting-edge solutions are tailored to address intricate environments where optimizing the asset's design, operation, and maintenance lifecycle is paramount.

{kind=link}

AZPN versatile software solutions find application across a spectrum of critical areas, encompassing performance engineering, modeling, and design, as well as supply chain management. Furthermore, the company's expertise extends to predictive and prescriptive maintenance, digital grid management, and industrial data management. The comprehensive suite of offerings reflects AZPN's commitment to shaping a future where businesses can harness the full potential of their assets, thus underlining its pivotal role in driving industrial innovation and progress.

{kind=link}

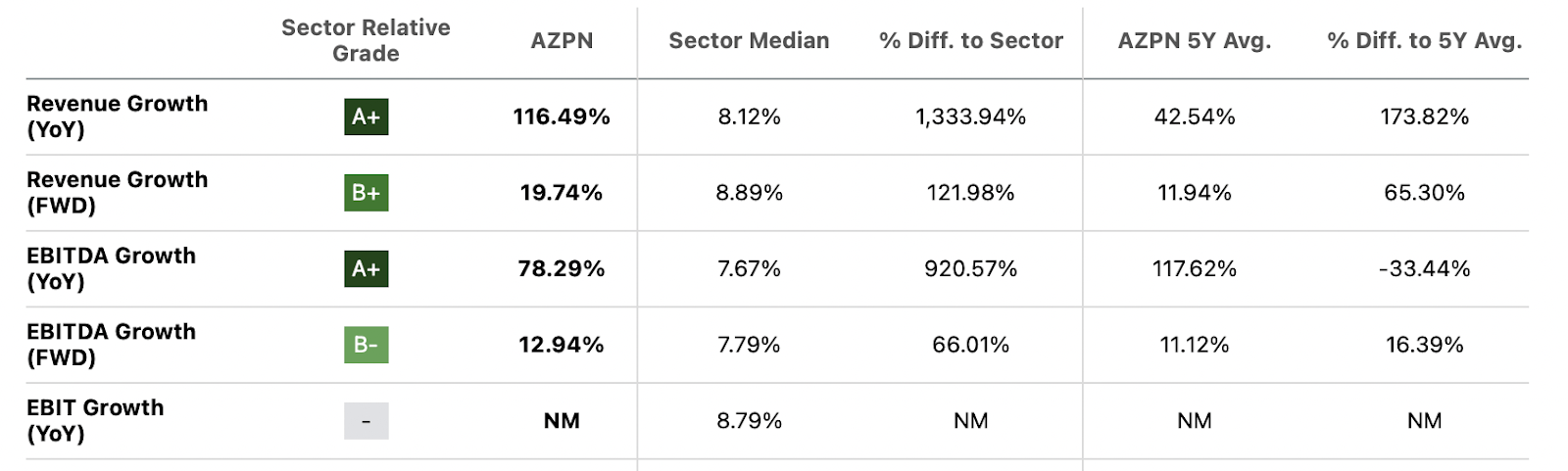

Over the last decade, this has meant strong growth for the company as the revenues have grown over 5 fold since 2019 . This certainly puts the company in the category of growth. However, the last Q4 FY2023 report showed revenues just growing at 11.8% YoY which I wouldn't necessarily equate to a significant growth company as AZPN has been. I would be looking for some closer to 20% YoY growth at least, especially seeing as the p/s is at a rich 9.3 right now on an FWD basis.

Markets They Are In

{kind=link}

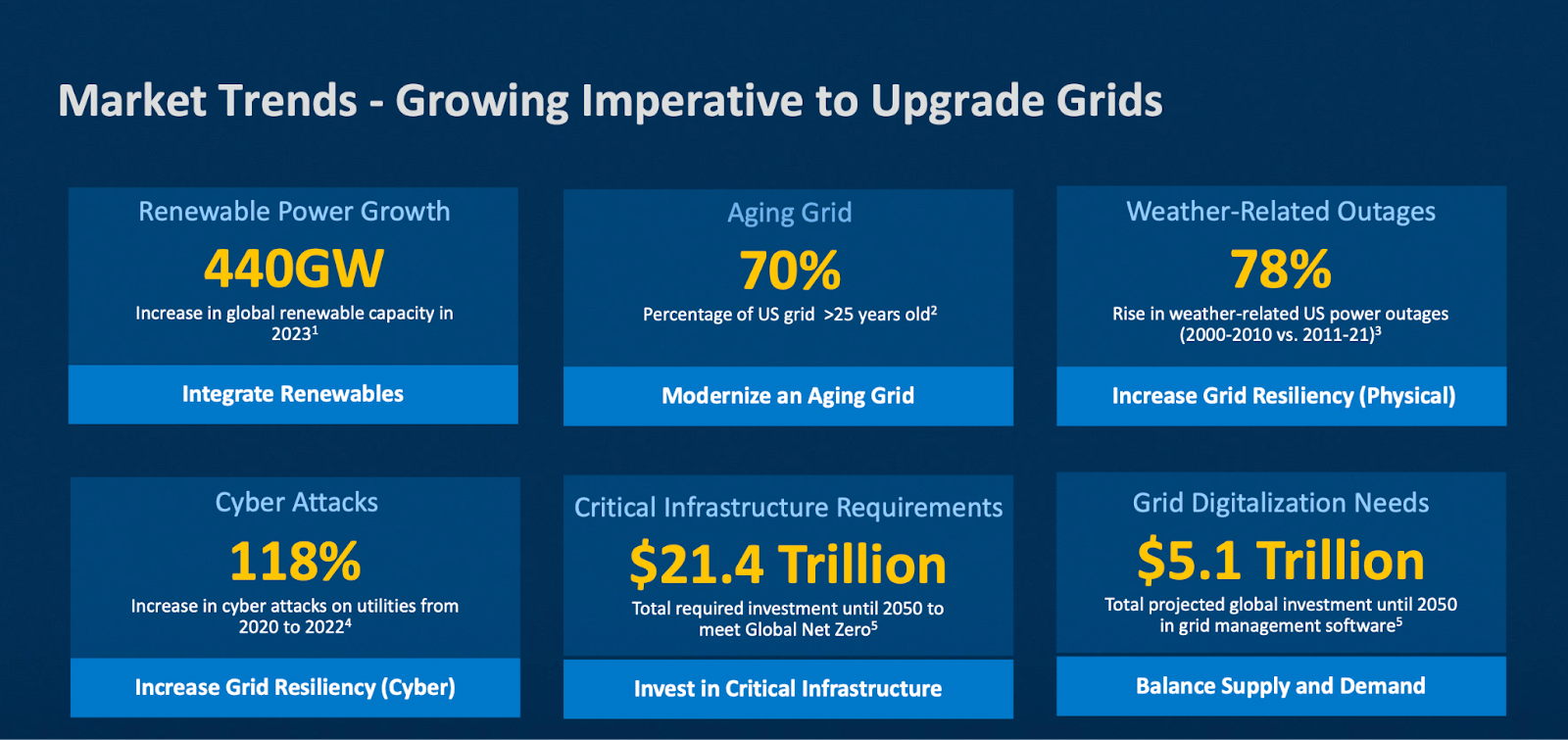

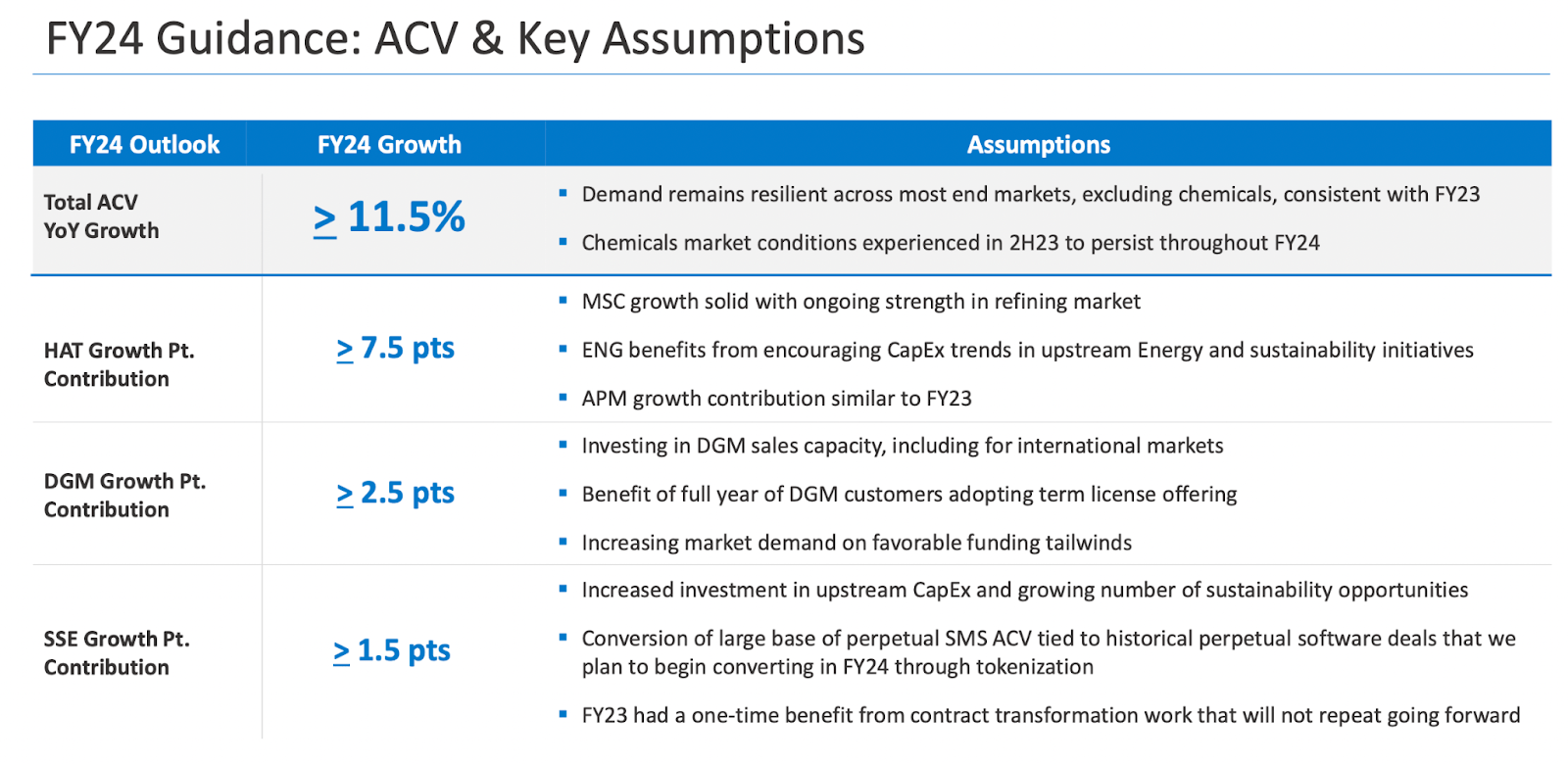

The markets that AZPN serves are quite broad and have been a key factor in the company's ability to drive strong growth over the last 5 years. Strong growth trends are appearing in the market for digital grid management or DGM. There is a large percentage of the current grid that is at a high age which means that quite soon there will need to be heavy investments in upgrading it and that is where AZPN could enter. Seeing as they focus on providing solutions that efficiently maximize assets and operations this investment need could bring strong demand in the way for AZPN. For 2024 for example the DGM contribution is set to help AZPN grow revenues by an additional 2.5% YoY contributed by the fact that AZPN is investing in their capacities in the space and supported by fundamental demand.

Earnings Highlights

{kind=link}

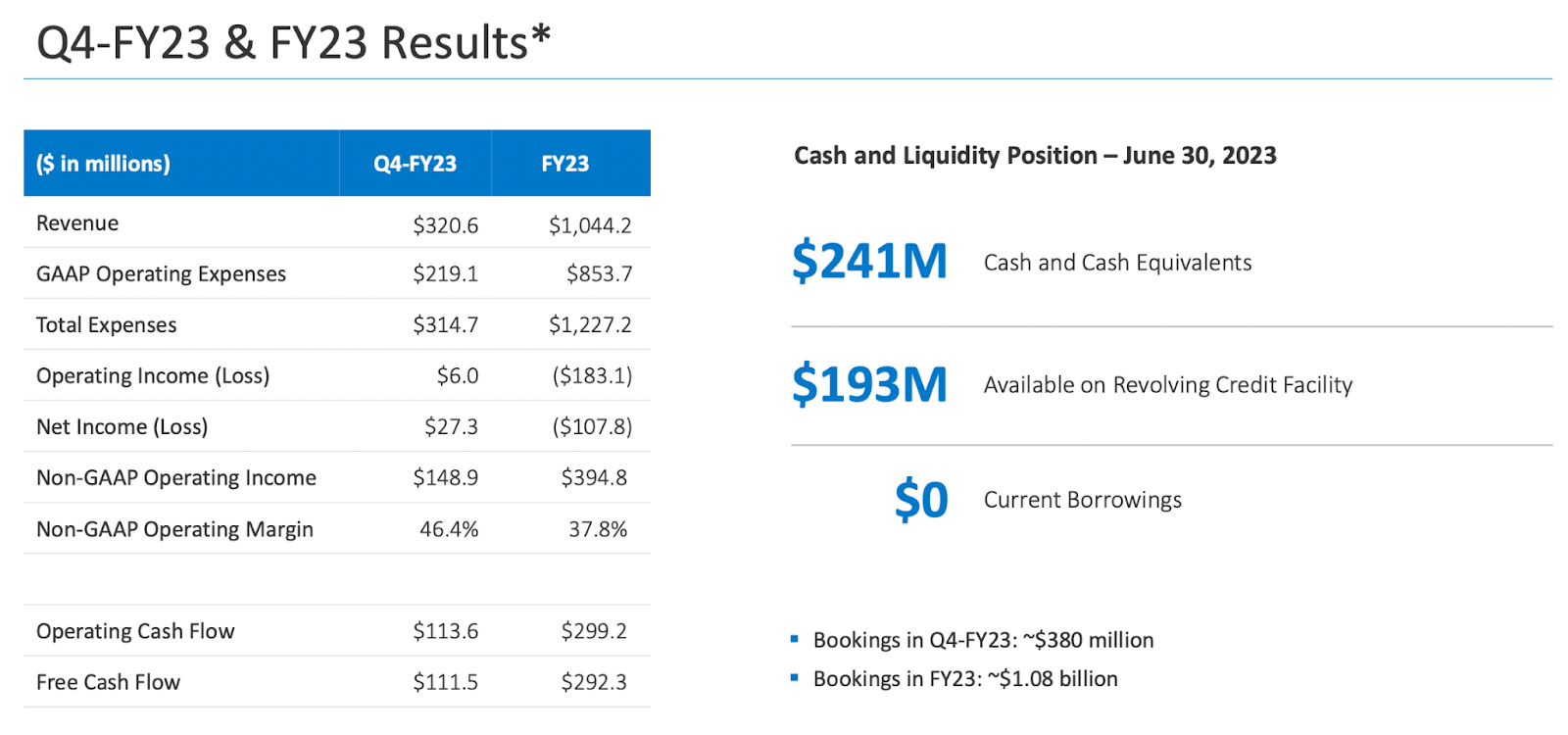

From the last earnings report provided by the company, we got some decent results, as the total revenues came in at over $1 billion which is a record for the business. This still puts AZPN at a very high p/s multiple of around 9.3 on a FWD basis. This sort of premium is most often associated with companies growing at faster rates than AZPN is right now.

{kind=link}

For example, the total ACV or contracted revenues for the business is set to grow 11.5% which is certainly very good, but I would expect something higher going forward for overall revenues. Estimates are that in 2024 the top line will have expanded by around 9.7% YoY. I don't think this number is enough to justify a 9.3x sales multiple. I would rather look for something closer to the sector instead as 9.7% is not far off from what a regular index fund would appreciate over a longer period. The sector that AZPN is in trades at a p/s of 2.3 which leaves substantial room for AZPN to fall should they be valued similarly. I think the reason for these high multiples is that AZPN has previously had very strong revenue growth numbers and the market may expect that to continue in some manner. I am more pessimistic as higher interest rates could certainly be a factor for reduced growth as the cost of borrowing goes up and economic activity slows down, affecting the sales growth of both AZPN and many others.

{kind=link}

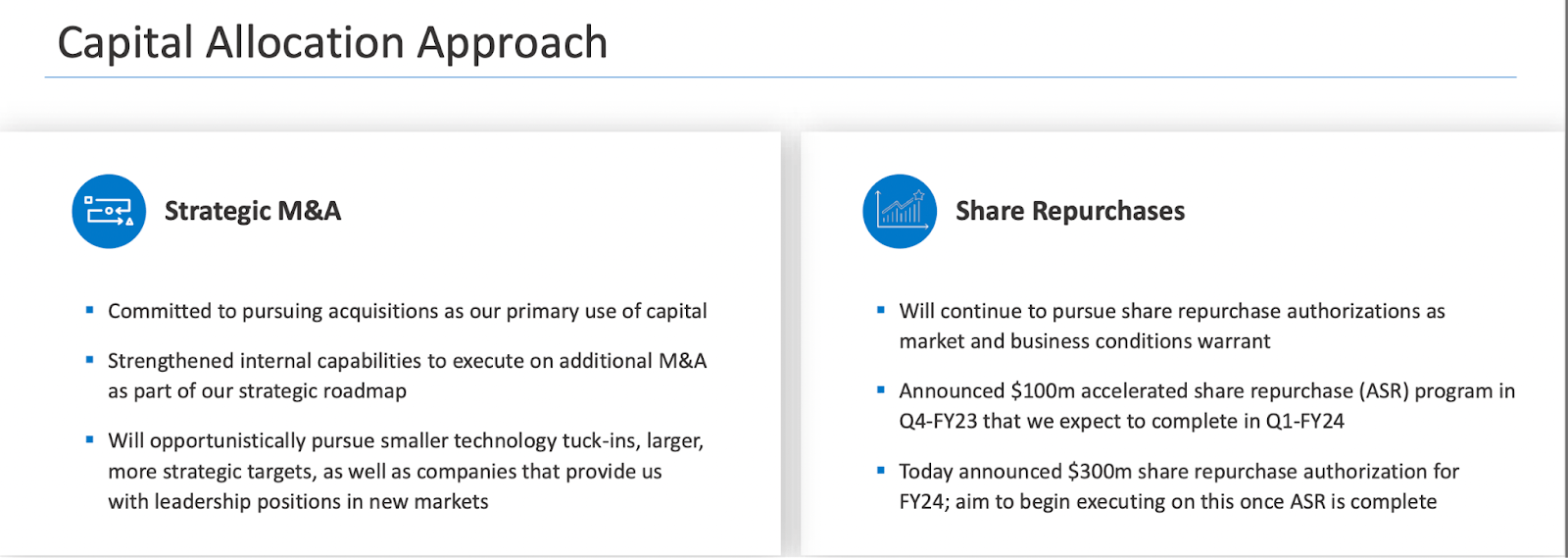

The company is using a lot of the capital it generated towards buying back shares, but I do find this to be quite irresponsible, especially when so much suggests that the share price is overvalued. When in the last quarter alone the company had $20 million in stock-based compensation it makes little sense to have such a high buyback program. They sort of cancel each other out in a way. We are not that far off from the next report by the company and I don't expect there to be higher growth numbers than the last quarter showed. Should the results disappoint as they did in late April I can see a significant valuation cut happening as well. The company is already trading at a high multiple which leaves more room to fall essentially. Putting a price target on the company, I would say I won't be a buyer unless the company drops to under $150 per share and the growth numbers start to accelerate further. That would provide me with a better entry point and more margin of safety as the valuation could be more justified with higher YoY growth numbers. I can certainly see AZPN also not falling back to the $150 range and instead trading at a premium, but I am perfectly fine with that which is why I am rating them a buy ultimately.

Risks

Being a company with a robust international presence, AZPN encounters a myriad of risks inherent to global operations. The foremost among these is the foreign exchange risk, where the company's earnings are intricately tied to the fluctuations in the currency exchange market. These shifts can significantly impact the financial performance of the company, necessitating a vigilant approach to currency risk management.

{kind=link}

AZPN grapples with a substantial concentration risk, primarily stemming from its heavy reliance on customers within the energy and chemical processing sectors. The company's revenue stream is intricately linked to these customers, who operate in markets characterized by inherent volatility. Furthermore, the financial well-being of these customers is significantly tethered to the fluctuations in commodity prices, thereby exposing AZPN to the intricacies of these highly dynamic markets. Should there be higher than expected increases to interest rates for example, then I can see it affecting the investment potential in some of the markets that AZPN operates in. They in a way live on their strong economic growth as that fuels business and investments and ultimately leads to higher demand for the solutions that AZPN provides. The higher cost of borrowing for capital reduces the economic activity and in the end demand for AZPN as well. A prolonged period of lacking growth numbers from AZPN could lead to the valuation being cut.

Final Words

The share price for AZPN has been on quite the roller coaster the last 12 months and saw in April a significant cut to the valuation. I don't see it as impossible that the same happens when the next report is released should the numbers be disappointing. I believe AZPN is also trading at a pretty high premium and suggesting a buy right now is not possible because of this. With all that said I land at a hold rating for the company for the moment being.

For further details see:

Aspen Technology Inc: Decent Growth But At A High Premium