AZPN - Aspen Technology: Industrial Software Leader Valuation Appealing After Plunge

2023-05-09 11:37:37 ET

Summary

- Aspen Technology, Inc. is a leader in industrial software with diversified end markets and strong long-term growth opportunity.

- The company has a solid growth strategy, incorporating both organic and inorganic growth strategies.

- With its strong market positioning, it has a solid free cash flow generation ability and a strong balance sheet.

- While Aspen Technology is trading at 30x 2024 P/E, I do think that it should be trading at a premium to peers given its market leading position, strong growth strategy, and solid financials.

- I aim to relook at the name when Aspen Technology is closer to 25x 2024 P/E, which translates to a share price of $143.

Aspen Technology, Inc. ( AZPN ) recently plunged after it released its fiscal Q3 earnings report. In this article, I want to introduce Aspen Technology's business, including a brief introduction to the company, its recent strategic transaction, its end markets, growth strategy and financial profile, amongst others.

Brief introduction into Aspen Technology

Aspen Technology is a leading player in the asset optimization software space. The company helps industrial manufacturers design, operate, and maintain their operations to optimize performance. It provides capabilities like modeling, simulation, and optimization, along with expertise in industrial operations and advanced analytics.

At the end of the day, Aspen Technology enables its customers to improve their profitability and long-term sustainability of their assets in production. This includes helping customers to maximize productivity, lower risks, enhance value, and lower energy use and emissions.

What I like about Aspen Technology is not just that it is a leader in asset optimization software, but that its technology enables and accelerates its customer's sustainability and decarbonization efforts. This is done through enabling a circular economy for its customers by using better industrial technology, plastics that are biodegradable or recyclable. It helps with the energy transition through usage of advanced solutions for carbon capture and storage, batteries and energy storage and power transmission and distribution.

Recent strategic transaction

Heritage AspenTech and Emerson Electric Co. (EMR) entered an agreement where Heritage AspenTech shareholders will get $6 billion in cash as well as Emerson Electric's Open Systems International ("OSI") business and Subsurface Science & Engineering ("SSE") business, while Emerson Electric will get 55% of Aspen Technology's stock.

This combined entity is expected to deliver superior value to shareholders. The new combined entity is expected to have significant scale, diversified end markets, and a platform for growth through acquisitions.

{kind=link}

Diversified end markets

Aspen Technology serves customers in capital intensive industries.

This includes the energy market, chemicals market, power transmission and distribution market, engineering and construction market, metals and mining market, and pharmaceuticals market.

As a result of the complex industry operations of these capital intensive industries and large scale of operation, any slight improvement in the operation, design or reliability can have a huge positive impact on the productivity of the operations.

These capital intensive industries have extensive technical requirements and need software that is highly sophisticated to help them to design, operate and maintain their production assets. As a result, they require software from Aspen Technology to meet their needs.

Strong market growth

The asset optimization software industry alone is expected to grow at a CAGR of 12% until 2030.

I expect that Aspen Technology will continue to be a leader in the space and grow faster than the market given its innovative product portfolio and growth strategy, which I will highlight next.

Growth strategy

Aspen Technology's key growth strategy is organic expansion within its own core verticals by increasing usage and adoption of more products. It currently has more than 3,000 customers and most of these customers only use a subset of its product portfolio.

In addition, Aspen Technology is looking to acquire to accelerate its growth, be it to expand on its asset optimization offering, product portfolio to enhance sustainability, or to penetrate new markets with an industrial focus. In 2022, Aspen Technology acquired AZPN),(approximately%20%24623%20million%20USD)." > Micromine , a leader in design and operational management solutions for the mining industry.

The company continues to bring to market innovative and market-leading solutions. For example, its recent product release, aspenONE V12, incorporates artificial intelligence across the product portfolio, utilizes the cloud for delivery as well as analytics for the entire enterprise and insights for better margins, improves sustainability and safety profile. Aspen Technology also provides more than 60 sustainability models and more support for its industrial AI solutions.

Along the top of sustainability, management expects its current product portfolio to be highly suited for the energy transition and the circular economy. As a result, I expect to see more green energy customers over time, as well as customers looking to meet sustainability goals.

Aspen Technology expects to increase its total addressable market over time, through both organic and inorganic innovation. The company regularly makes and analyzes the option to make or buy and has made several acquisitions over the years.

The company looks to expand into complementary adjacent industries as well as market segments. With continued innovation, I expect that Aspen Technology will continue to deliver new products for new markets and industries over time. A good example is how Aspen Technology has met the changing requirements of pharmaceutical customers as they require more agility while still maintaining high quality.

Solid financial profile

Given that Aspen Technology is a leader in industrial software with significant scale, it has strong recurring revenue and solid free cash flow generation.

With the new OSI and SSE businesses from Emerson, I expect these will also be converted to recurring revenues, bringing a larger mix of recurring revenue and stronger free cash flow margins.

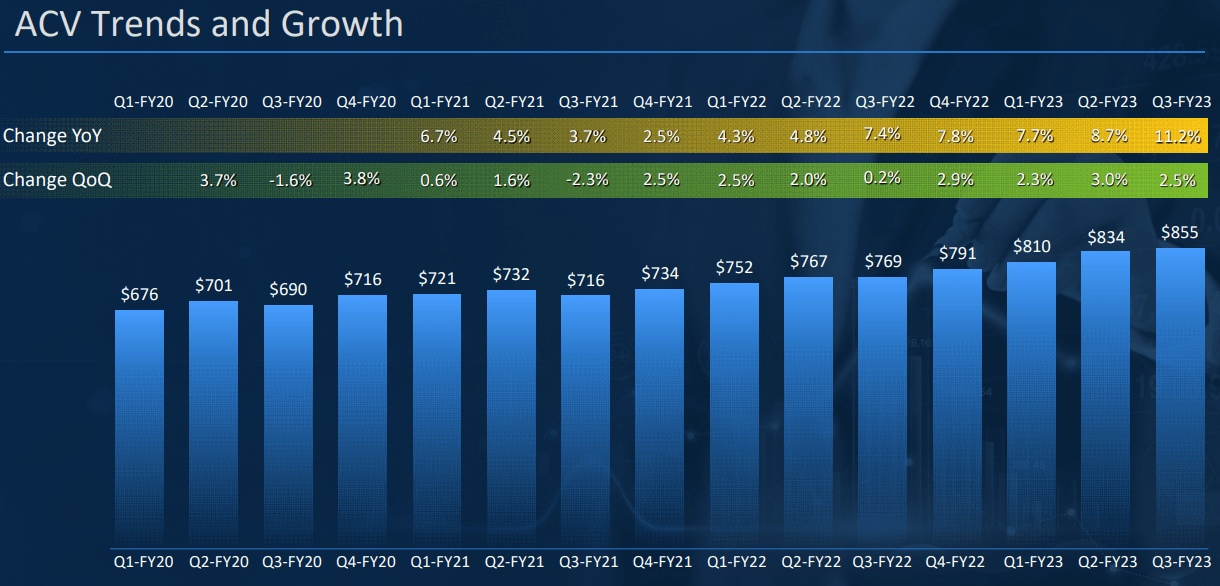

As can be seen below, ACV trends were strong, with 8.7% year-on-year growth and 3% growth sequentially.

{kind=link}

With the recent $129 million in free cash flows generated in FY3Q23 and revenue of $230 million, this means that the free cash flow margin is at 56%.

Recent earnings

In fiscal Q3 , Revenue grew by 22% year-on-year to $230 million, missing consensus by 11%.

Non-GAAP EPS for FY3Q23 came in at $1.06, missing estimates by $0.73.

Full-year FY2023 guidance was also updated to between $1.04 billion to $1.06 billion and adjusted EPS was updated to between $5.63 to $5.83.

There are multiple reasons for the weak quarter relative to expectations.

Firstly, Aspen Technology realized that the improvement in OSI's project delivery organization could take longer than expected and thus, delay revenue in the near term.

Second, management also highlighted that they were over-optimistic about their ability to accelerate the sales cycle of the digital grid management segment. Instead of the initial 9 to 12 months expected, management expects this to take 12 to 24 months on average to complete.

Lastly, within the chemicals industry, as a result of a difficult operating environment, including elevated energy costs and supply chain issues, Aspen Technology's chemicals customers reduced software spend in the quarter more rapidly than expected.

For the first time in the FY2023 fiscal year, management saw an elongation of sales cycle in all regions and more postponements in deals and pushing out of the existing pipeline. I think that this was one of the reasons investors were more cautious on the name and presents near-term challenges for Aspen Technology.

Share repurchase program

Aspen Technology recently announced that its Board has authorized a new share repurchase program for up to $100 million of its common stock for FY2023 and FY2024. This includes an accelerated repurchase agreement and the last settlement is expected to be in the first quarter of FY2024.

As explained by the CEO of Aspen Technology, their primary priority continues to be acquisitions that will generate long-term strategic growth, but their solid balance sheet and recurring free cash flows allow management to have the flexibility to proceed with this recently announced buyback program.

Valuation

Aspen Technology is trading at 30x 2024 P/E and 29x P/FCF.

I think that the company should be trading at a premium to its peers given the strong free cash flow generation, solid balance sheet, and long-term growth runway in industrial software with drivers from trends like sustainability and decarbonization.

That said, at 30x 2024 P/E, I do think the opportunity is limited in the near term for outsized returns in Aspen Technology, Inc. stock. I would like to see the company trade nearer to 25x 2024 P/E before I turn constructive on the name. As a result, I am neutral on the name at the moment and will not be adding to the name at current valuations.

Risks

Industry risks

The weakness in a particular industry could have near-term negative implications for Aspen Technology. For example, a weakness in the oil and gas sector could lead to a slowdown in the company's growth as a result of a slowdown in its customers.

Macroeconomic environment

While Aspen Technology has a diversified end market, as most of them are in capital intensive industries, in times of weak economic conditions, these industries could look to reduce spend. As a result of this, it could result in additional near-term headwinds for the company.

Acquisition risks

As highlighted above, Aspen Technology looks to acquire businesses to grow its business in the long term. There are dilution risks, synergy, and integration risks when acquisitions are involved and this could add more downside to the company if the acquisition strategy is not strong.

Conclusion

I can see a strong investment case for Aspen Technology, Inc. It is operating within a niche in software that is growing at a CAGR of 12% until 2030, while it has differentiated and hard to replicate offerings as it provides customers with highly sophisticated software and solutions for their complex and capital intensive industries. While Aspen Technology is trading at 30x 2024 P/E, I do think that it should be trading at a premium to peers given its market leading position, strong growth strategy, and solid financials. I aim to relook at the name when Aspen Technology, Inc. is closer to 25x 2024 P/E, which translates to a share price of $143.

For further details see:

Aspen Technology: Industrial Software Leader Valuation Appealing After Plunge