CRMD - Assertio Holdings: Acquiring Good Products Is The Key To Success

Summary

- Assertio Holdings is a pharmaceutical company based on a niche model that is focused on digital, non-personal promotion.

- Last Q3 showed great revenue and cash flow growth.

- The company's growth strategy is based on market acquisitions.

- The share price valuation seems to be very convenient.

According to Assertio Holdings, Inc. ( ASRT ), the classic model of selling pharmaceutical products through direct sales in person is becoming too competitive and able to reduce productivity. The company, therefore, decided to implement a highly technological digital platform that also exploits artificial intelligence [AI] to position itself on the market with a multi-channel and multi-product approach.

Assertio has grown through its cost-saving ability and above all through targeted and strategic acquisitions of products on the market. The last two acquisitions made in 2021 and 2022 are called OTREXUP and Sympazan and represent new assets that have rightfully entered Assertio's technological sales funnel. There seems to be no shortage of results and with strong growth in turnover (exceeding expectations) and an EBIT Margin of 29.9%, we can state that the corporate strategies have worked well at the moment.

The Capital Turnover is a ratio (0.43 - TTM) that indicates a very high use of capital in the company compared to the revenue generated and this implies that the company needs to grow a lot precisely in terms of revenue. The road is marked and soon new acquisitions could join the existing portfolio. This point represents, in my opinion, the main risk elements in this business, or if a new acquisition does not prove successful, Assertio could easily find itself in great financial difficulty. What happened in the last year in any case underlines the management's ability to deal with acquisitions in a profitable manner.

Last but not least the share price evaluation seems to be particularly advantageous and my rating is buy.

General Overview

Assertio Holdings, Inc. is a pharmaceutical company (currently focused only on drug marketing and not on production) that sells a diverse portfolio of products to patients.

The portfolio is divided into three areas: neurology, hospital, and pain.

The business marketing strategy is based on a niche model that is focused on digital, non-personal promotion. The business growth strategy is based on the external acquisition of the new asset.

The company was officially born on May 2020 through a merger with Zyla Life Sciences and this acquisition has enabled the company to realize cost savings of approximately $40M annually.

In 2021 Assertio acquired Otrexup from Antares and in Oct 2022 completed a deal to acquire the license of Sympazan (clobazam) from Aquestive Therapeutics, Inc. ( AQST )

{kind=link}

Financial & highlights

Revenue and Profitability

{kind=link}

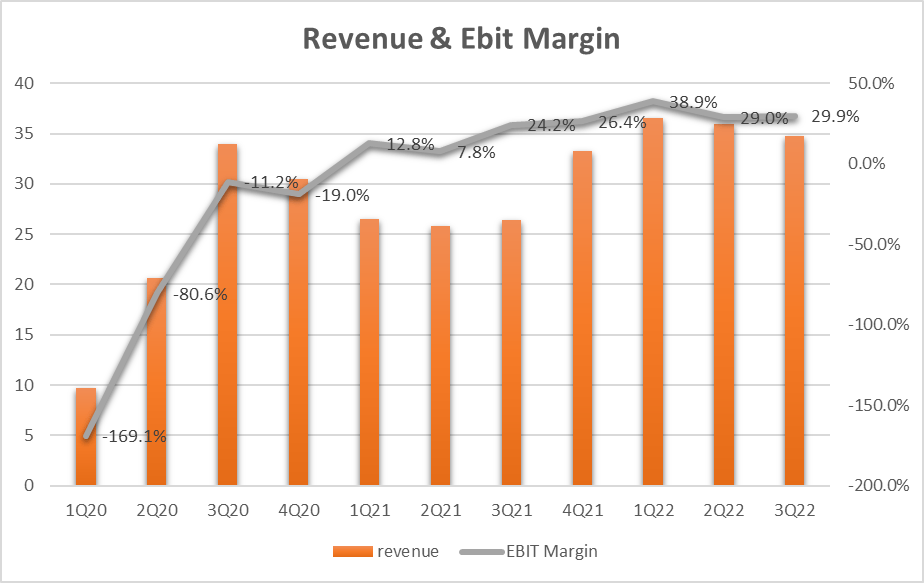

The orange bars show the revenue trend for each Quarter starting from 1Q 2020. We can record a growing and apparently stabilized trend in the 3 Quarter of 2022. In terms of EBIT Margin instead, we can see how the value goes from a strong negative in Q1 2020 up to a margin of more than 30% in 2022. This last figure represents a positive value and a solid starting point for future growth.

{kind=link}

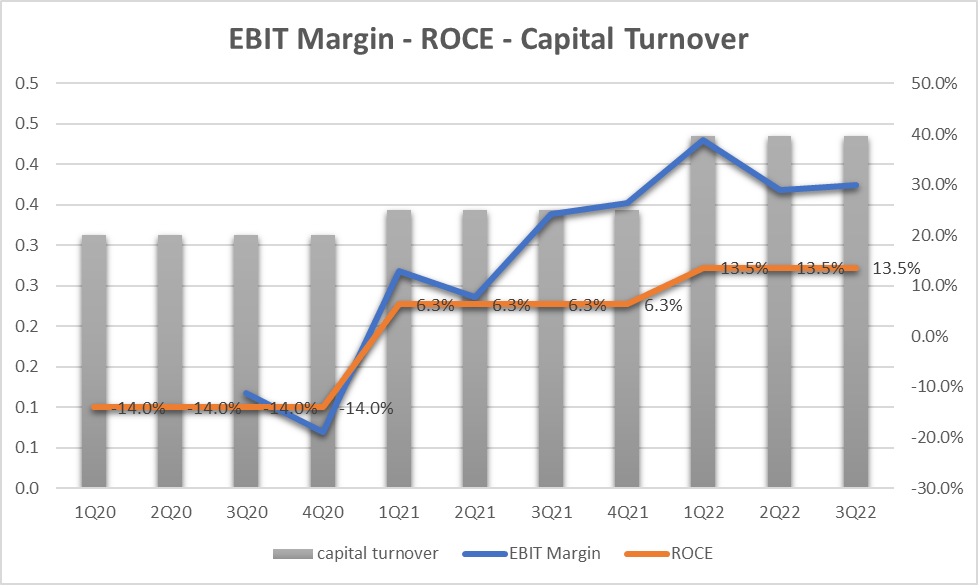

The gray bars represent the Capital Turnover of the company always referring to the Quarters starting from 2020. We can see a growing trend which, however, settles on still very low values equal to 0.43 in 2022. This means that for every $1 of capital employed in the company this produces $0.43 in revenue. The trend is growing but the figure is still low and we will have to wait for more sustained growth in revenue to be able to record values close to unity.

The orange line represents the ROCE (Return on Capital Employed) and in this case, too we can see a growing trend with values standing at 13.5% in the last quarter. The figure in absolute value is not bad but we can see how the EBIT Margin (blue line) is well above the orange line and this is precisely due to a low value of the Capital Turnover. The objective of the next Quarters should be to see the gap between orange and blue decrease until an intersection and possible overtaking.

Free Cash Flow and EPS

{kind=link}

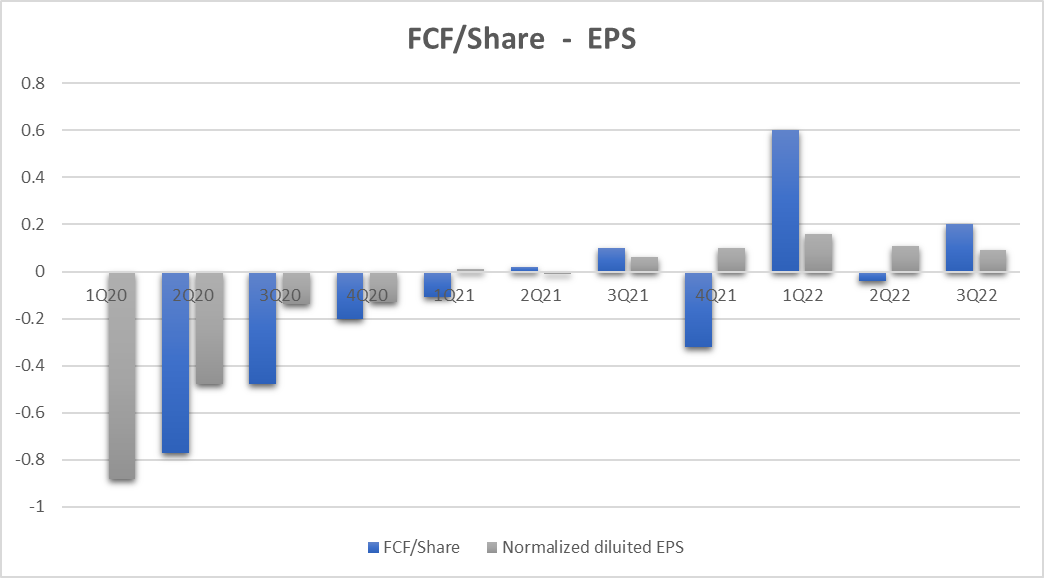

The gray bars represent the EPS in the various Quarters. We can see how the 2Q of 2022 represented the company's profitability reversal. The trend is growing and underlines good management. The blue bars represent the Free Cash Flow per Share and we can see how the company is able to constantly transform EPS into Cash Flow. The 4Q of 2021 and the 2Q of 2022 are exceptions.

In December 2021 Assertio acquired Otrexup for $18 million and this is why the 4Q 2021 Operating Cash Flow was fully utilized for this acquisition and went into the negative flow. In October 2022 the Company acquired the license of Sympazan from Aquestive and this is why in 2Q 2022 the operating cash flow was fully used for this acquisition and went to generate a negative flow.

The graph shows very well how the company's cash flow closely follows the earnings and that as soon as there is the availability of cash this is used to make acquisitions and these soon after bringing new positive results.

Listening to the last earnings call we can understand how the last acquisition has worked:

We think the M&A environment is very robust and buyer friendly right now which the Sympazan transaction exemplifies. We're able to acquire that asset for $15 million, including the milestone for the new patent. In the trailing 12 months ended September 30, Aquestive recorded $9.9 million in net sales. We've acquired an asset that is growing. We'll soon have patent protection to 2039 and has gross profit margins very close to our corporate average for 1.5x trailing revenues.

Future financial target

In terms of our goal to further diversify our business, while mathematically Sympazan does help, it was on the smaller side. As we had mentioned, we were seeing the smaller-sized acquisitions and our M&A pipeline accelerate, while the larger ones are being delayed. We are still pursuing those larger transformative transactions. We had originally set a goal of acquiring products that brought us an additional $50 million in gross profit by 2024.

This is what was reported in the latest earnings call in terms of the gross profit target by 2024.

The approximate $10 million from OTREXUP and now $8 million from Sympazan, we are a little over 1/3 of the way to accomplishing that goal. We have another year to go, a deep pipeline, a favorable M&A environment and the capabilities to multitask, so I'm confident we can accomplish this goal.

If we consider that the last 2 acquisitions (OTREXUP and Sympazan) brought about $18M we can deduce that the plan is working by more than 30% and that, if the company continues in this way, it is probable that the target could be fully achieved.

Valuation

Earnings Power Value Model

Assuming that the cash profit remains constant over the long term, I use the EPV (earnings power value) method to calculate the share price

The method starts with EBIT. The second step is to add depreciation and amortization and then subtract stay-in-business CAPEX.

The result is the Cash Trading Profit

I then subtract the taxes by calculating the amount using the actual tax rate that the company pays.

The result is the After-Tax Cash Trading Profit

At least to calculate the total company enterprise value I divide the After-Tax Cash Profit by the interest Rate I define as fine for this kind of Company (ASRT is a high-risk company so I decided to use 15%)

The result is the Total Company Earnings Power Value. Dividing the result by the total number of shares we find the value per single share.

The table below shows the calculation for ASRT

| EBIT |

| 43.80 |

| Dep & amort |

| 32.50 |

| CAPEX |

| -35.40 |

| Cash Trading Profit |

| 40.90 |

| TAX |

| 4.80% |

| TAX |

| -1.9632 |

| After TAX cash profit |

| 38.94 |

| Interest Rate |

| 15% |

| EPV |

| 259.5787 |

| Shares in issue |

| 48.2 |

| EPV per share |

| 5.4 |

$5.4 represents the share price valuation using the EPV method. If we compare the data with the current market price ($3.6) we see that the current price could be seen as cheap.

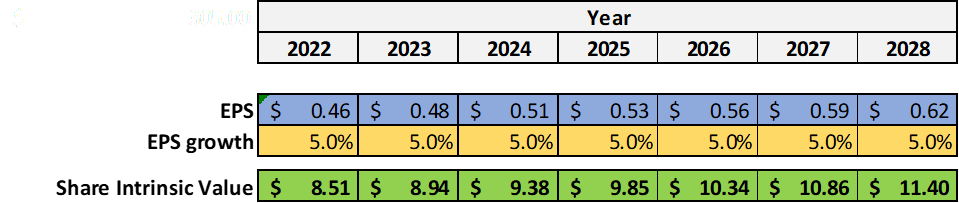

EPS Growth Model

Since the company is showing growth in terms of Revenue and EPS, I decided to use a conservative estimation of the EPS growth parameter of 5%.

The Formula is (by popular investor Benjamin Graham):

Intrinsic value per share = EPS x (8.5 + 2 g)

Where

EPS = earning per share

g = EPS growth rate = 5%

{kind=link}

Example of calculation for 2023:

Intrinsic value per share = EPS x (8.5 + 2 g) = 0.48x(8.5+2x5) = $8.94

The last intrinsic value of $11.4 for 2028 underlines an annualized return [CAGR] of 21.2% as the current share price is $3.6.

21.2% is the annualized expected return for the investment in ASRT. It's a very good figure and it requires a low risky confidence that the EPS growth rate can remain at 5% for the next 7 years.

FCF/Share Model

To define a maximum buying price, I use also a formula based on FCF/Share and interest rate.

The formula is:

Maximum buying price = Cash profit per Share/interest rate – 20% (safety discount)

If TTM Cash Profit per share is $0.45

Interest Rate=inflation Rate = 7.1%

Maximum price before Safety discount = 0.45/7.1%= $6.33

The maximum price at 20% discount = $5.3

Under the FCF/Share analysis, it seems that the actual price of $3.6 is fair.

All valuation models converge on a share intrinsic value above $5 and this represents a highly interesting element in terms of investment in the long run.

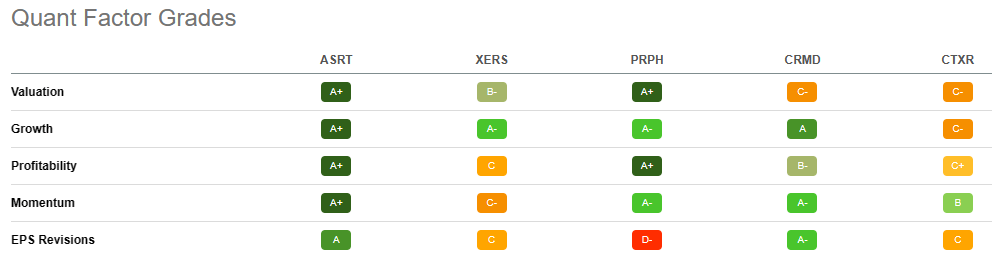

Peers

To compare ASRT with similar companies in terms of market capitalization in the Pharmaceuticals industry I have defined the following peers:

- Xeris Biopharma Holdings, Inc. ( XERS )

- ProPhase Labs, Inc. ( PRPH )

- CorMedix Inc. ( CRMD )

- Citius Pharmaceuticals, Inc. ( CTXR )

Using Seeking Alpha's Quant Ratings we have a ‘Strong Buy’ verdict related to the ‘Hold’ or ‘Strong Buy’ rating of the others company.

{kind=link}

{kind=link}

Under the Quant Factor Grades point of view, we can see how Assertio is really outstanding in every area from Valuation to Growth, Profitability, and Momentum. Only in EPS Revision the grade is not outstanding but is a respectable ‘A’. This comparison allows us to understand how at this moment Assertio is experiencing an astral alignment of all the positive ratios in his favor and that his peers are unable to reach this rating.

Future acquisition for growth is the main Risk factor

We have seen how the generation of profits and cash flow was immediately used by the company to make purchases on the market. The last two acquisitions we can say have been a success at least from the point of view of growth in profits and free cash flow. The company must grow and will do so through new acquisitions of existing products on the market. If one of the forthcoming acquisitions fails to meet the profitability requirements necessary for growth or worse proves to be a draining element of resources, this could be a devastating event for the corporate accounts.

From my point of view, the choice of new products to be included in the catalog represents the greatest element of risk if this choice is made incorrectly. It is true that the economic basis is positive but it is also true that it is still very fragile and even just one wrong choice could be harmful.

Conclusion

Assertio was born in 2020 but already in just two years, it managed to bring the company accounts into profit and create an important cash flow that was promptly used to make targeted acquisitions on the market. These acquisitions have led the company to lay the foundations for sustainable and profitable growth.

With an EBIT Margin of 29.9% and revenue growth of 13.6% [CAGR] on a quarterly basis, we can state that the fundamental parameters travel fast and along the correct road. With a share price valuation that turns out to be very convenient and using different valuation models all converges on an intrinsic value greater than $5, I believe that an investment in Assertio can bring important returns in the long run. My rating is Buy.

For further details see:

Assertio Holdings: Acquiring Good Products Is The Key To Success