AC:CC - Assessing JetBlue Airways During A Time Of Significant Uncertainty Over Spirit Airlines Turmoil

2024-01-21 01:57:33 ET

Summary

- JetBlue Airways and Spirit Airlines' merger has been ruled out by a court, causing uncertainty for both companies.

- Spirit Airlines has not been profitable since 2019 and has significant net debt, making its future uncertain.

- JetBlue Airways, on the other hand, has positive cash flow and potential value for value-oriented investors.

- Regardless of what transpires with the merger, which is now being appealed, JetBlue stock makes for an interesting prospect.

The past couple of months now have been rather difficult for shareholders of both JetBlue Airways ( JBLU ) and Spirit Airlines ( SAVE ). As I wrote about in an article published in June of last year, the two companies were pushing toward a merger with the hopes that a combination of the two entities would allow for significant cost cutting. The end result could be between $600 million and $700 million of annual run rate synergies. At the time, I felt optimistic about both companies, with a recovery in air traffic to pre-pandemic levels and beyond likely proving bullish for the company. And as for Spirit Airlines, I was optimistic given the spread between the price at which shares were trading and the implied buyout price. Unfortunately, things have taken a rather nasty turn. A court just ruled that the merger could not proceed because it would essentially result in the elimination of low fare travel in a manner that would harm the most ‘price-conscious’ consumers.

Shares of both businesses are down quite a bit as a result of these developments. In particular, there is considerable uncertainty regarding the future of Spirit Airlines. As of the end of the most recent fiscal quarter, Spirit Airlines had net debt of $2.23 billion. And the last time the company had been profitable was back in 2019 before the pandemic ravaged the world. At this point, I will say that the picture for Spirit Airlines is far less certain than I expected it to be. But I do think that JetBlue Airways might make a lot of sense for value-oriented investors who don't mind a bit of risk.

JetBlue Airways is worth considering

Over the past year through January 19th, shares of JetBlue Airways are down and impressive 41.3%. Some of this downside can certainly be chalked up to some fundamental issues that the business has, while the rest is likely attributable to this proposed transaction regarding Spirit Airlines creating a tremendous amount of uncertainty. Regarding the transaction, there are both positives and negatives associated with the deal moving forward or the deal failing. I already mentioned the synergies as a positive. But the negative is that, as I stated already, Spirit Airlines has not been profitable since 2019. On top of this, there is the topic of debt that cannot be overlooked.

{kind=link}

Author - SEC EDGAR Data

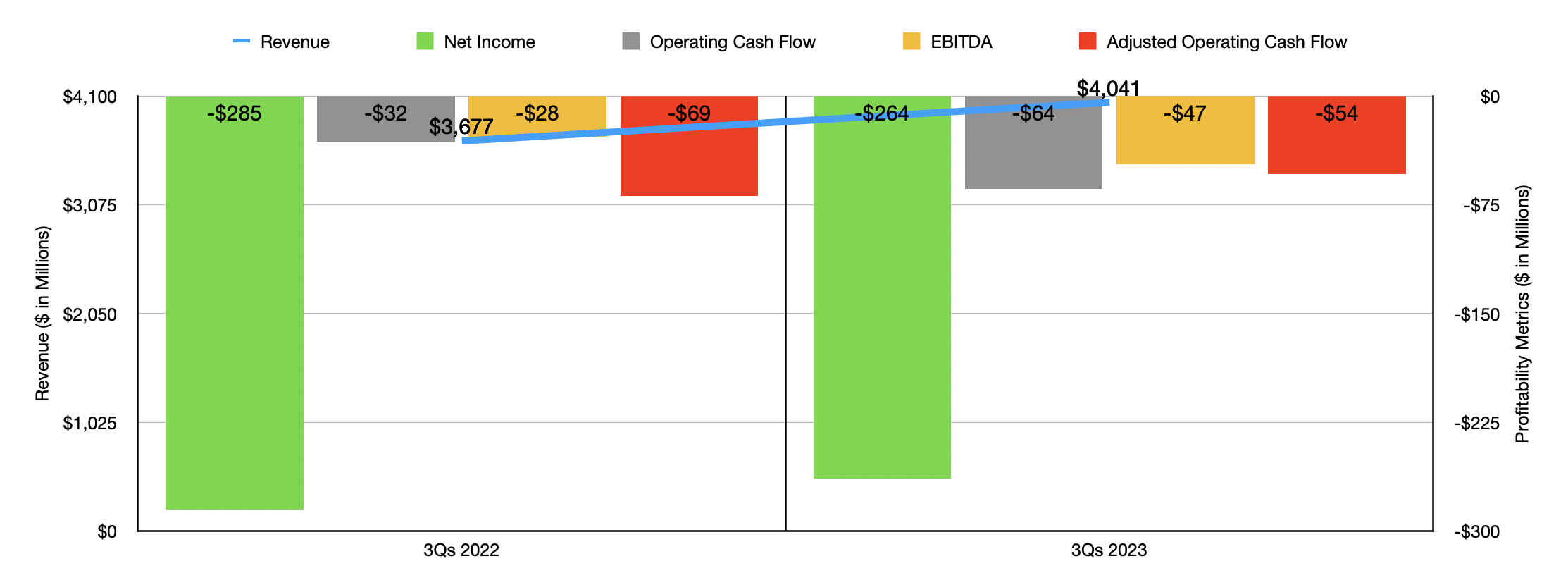

It might seem peculiar to hear that the company was not profitable last year. Of course, we don't yet have comprehensive data covering the final quarter of 2023. But we do know that, even as revenue rose from $3.68 billion in the first nine months of 2022 to $4.04 billion in the first nine months of 2023, the firm's net loss narrowed only marginally from $285 million to $264 million. A big part of this problem involves high fuel costs. Back in 2019, when the company last made a profit that totaled $335.3 million, fuel costs amounted to 25.9% of overall revenue. Even though fuel expenses dropped 7.1% year over year for the first nine months of 2023 relative to the same time last year, they still accounted for 33% of sales. While that may not sound like much, when applied to the revenue the company generated in the first nine months of last year, it amounts to $286.9 million in additional expenses. Salaries, wages, and benefits have also exploded higher, growing from 22.6% of sales in 2019 to 29.7% in the first nine months of last year. That's another $286.9 million in costs as well. I would be more optimistic about Spirit Airlines standing on its own two feet without the merger going through if cash flows were positive. But as the chart above illustrates, these were also negative during the first nine months of last year.

{kind=link}

Author - SEC EDGAR Data

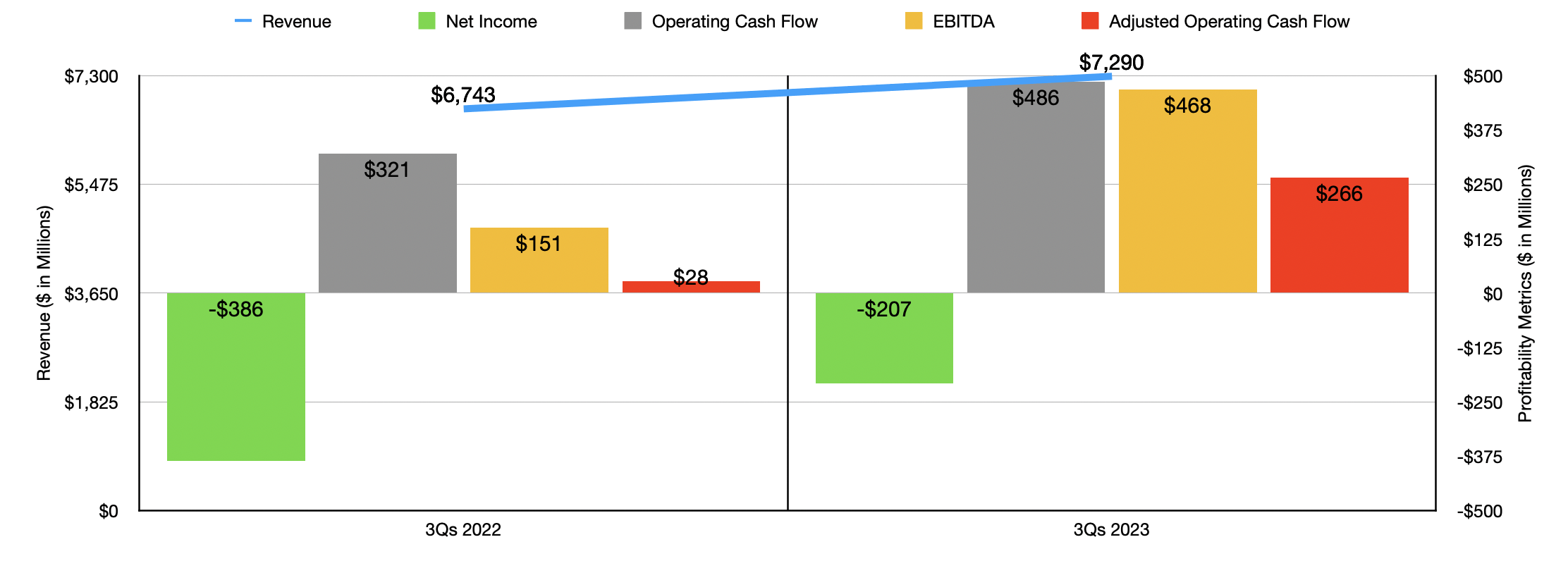

The other player in this equation, JetBlue Airways is another story entirely. It is true that during the first nine months of 2023 , the business generated a loss of $207 million. That's down from the $386 million loss reported one year earlier. But unlike Spirit Airlines, JetBlue Airways is actually significantly cash flow positive. During the first nine months of 2023, operating cash flow was $486 million. That's up from the $321 million reported one year earlier. Even if we adjust for changes in working capital, we get a rise from $28 million to $266 million. Meanwhile, EBITDA for the company expanded from $151 million to $468 million.

This doesn't mean that everything regarding the company is positive. Salaries and other related costs for the firm have actually increased quite a bit. They expanded from 30.5% of revenue in the first nine months of 2022 to 31.6% in the first nine months of 2023. The great news is that this was offset by a drop in fuel and related expenses from 34.2% of sales to 28%. This drop occurred even as the company went from consuming 626 million gallons of fuel to 677 million. But a drop in average fuel costs from $3.68 per gallon to $3.02 per gallon helped out tremendously. While the company did see a decrease in average fare from $217.34 to $211.77, a growth in revenue passengers from 29.08 million to 32.31 million helped boost revenue from $6.74 billion to $7.29 billion. To be very clear, Spirit Airlines also experienced a drop in fuel costs, with its decline from $3.70 per gallon to $3.04. However, with a lower price point of $123.97 per passenger flight, this improvement was not enough.

{kind=link}

Author - SEC EDGAR Data

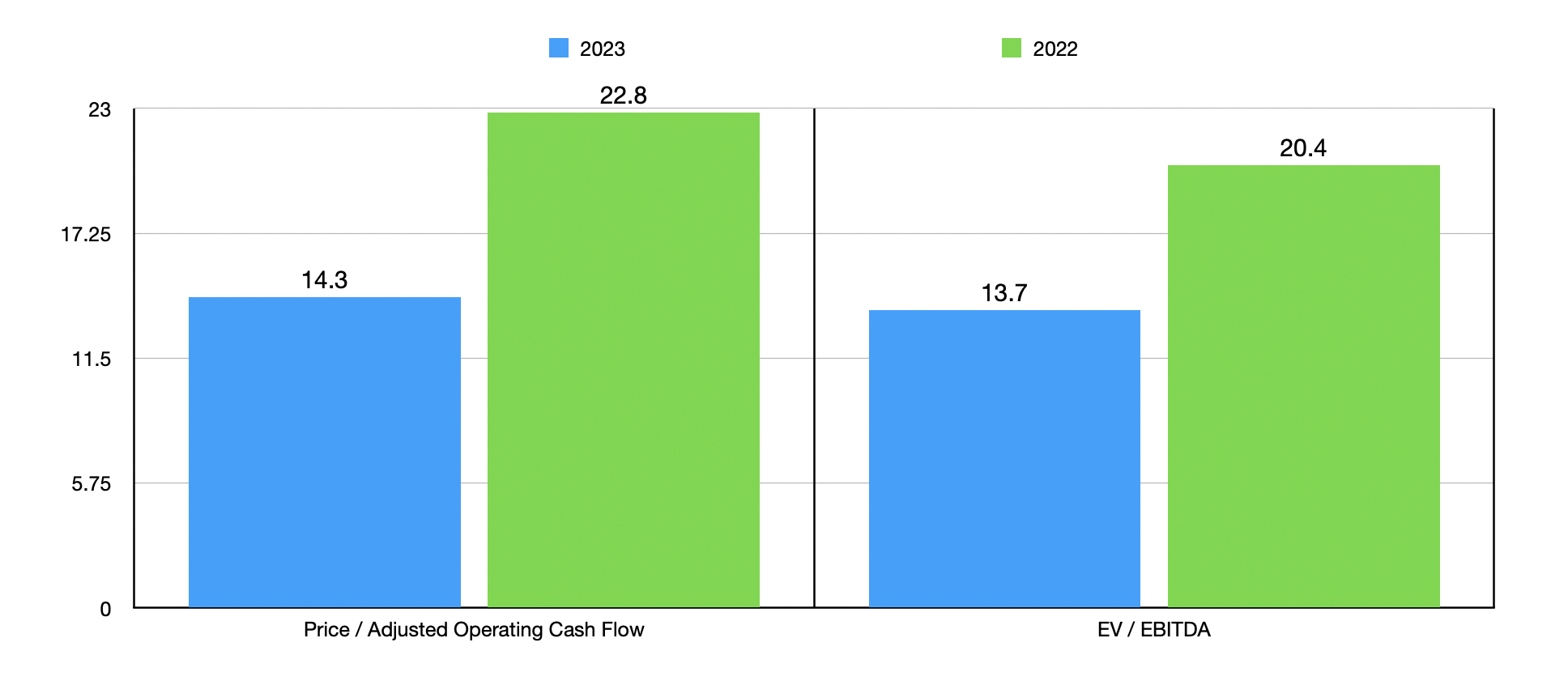

In terms of valuing JetBlue Airways, it's worth noting that over the trailing 12 month window of time, the company has generated EBITDA of about $665 million. This should translate to operating cash flow of around $574 million. As you can see in the chart above, this makes shares quite cheap, with a price to operating cash flow multiple of 2.9 and an EV to EBITDA multiple of 6.2. However, this does not mean that the business is the cheapest in its space. In fact, it's a bit toward the pricier end of the spectrum. In the table below, you can see what I mean. Of the five companies that I compared it to, four are cheaper on a price to operating cash flow basis. And when it involves the EV to EBITDA approach, three ended up being cheaper. Of course, leverage does need to be taken into consideration here. The net leverage ratio of JetBlue Airways is about 3.71, which means that two of the five companies that I compared it to are more heavily indebted relative to cash flows than it is.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Net Debt / EBITDA |

| JetBlue Airways |

| 2.9 |

| 6.2 |

| 3.71 |

| Allegiant Travel Company ( ALGT ) |

| 2.9 |

| 5.8 |

| 3.05 |

| SkyWest Inc. ( SKYW ) |

| 3.1 |

| 8.4 |

| 5.49 |

| Controladora Vuela Compania de Aviacion ( VLRS ) |

| 1.3 |

| 4.9 |

| 10.61 |

| Sun Country Airlines Holdings ( SNCY ) |

| 4.2 |

| 5.8 |

| 2.58 |

| Air Canada ( OTCQX:ACDVF ) |

| 1.7 |

| 3.2 |

| 1.90 |

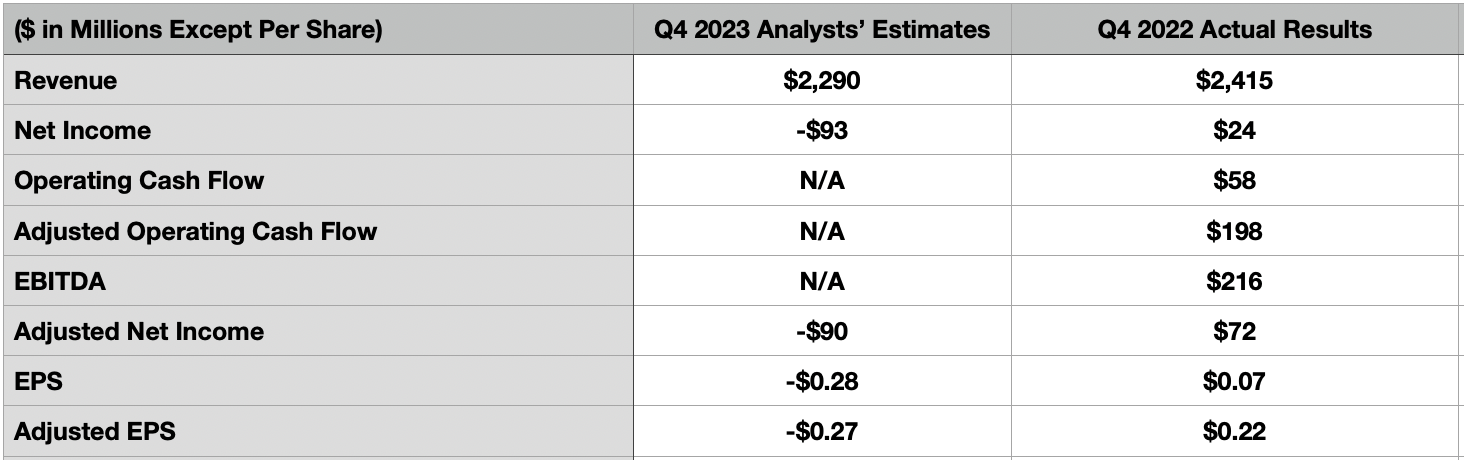

It will be interesting to see how things change when management reports earnings on the morning of January 30th. The current expectation is for revenue to come in at about $2.29 billion. Though if we take the midpoint of guidance provided by management, we are looking at something slightly lower at $2.21 billion. By comparison, revenue in the final quarter of 2022 ended up being $2.42 billion. So either way, we are looking at a year over year decline. The same holds true from a profitability perspective. As the table below illustrates, earnings and adjusted earnings are likely to be lower than they were in the final quarter of 2022.

{kind=link}

Author - SEC EDGAR Data

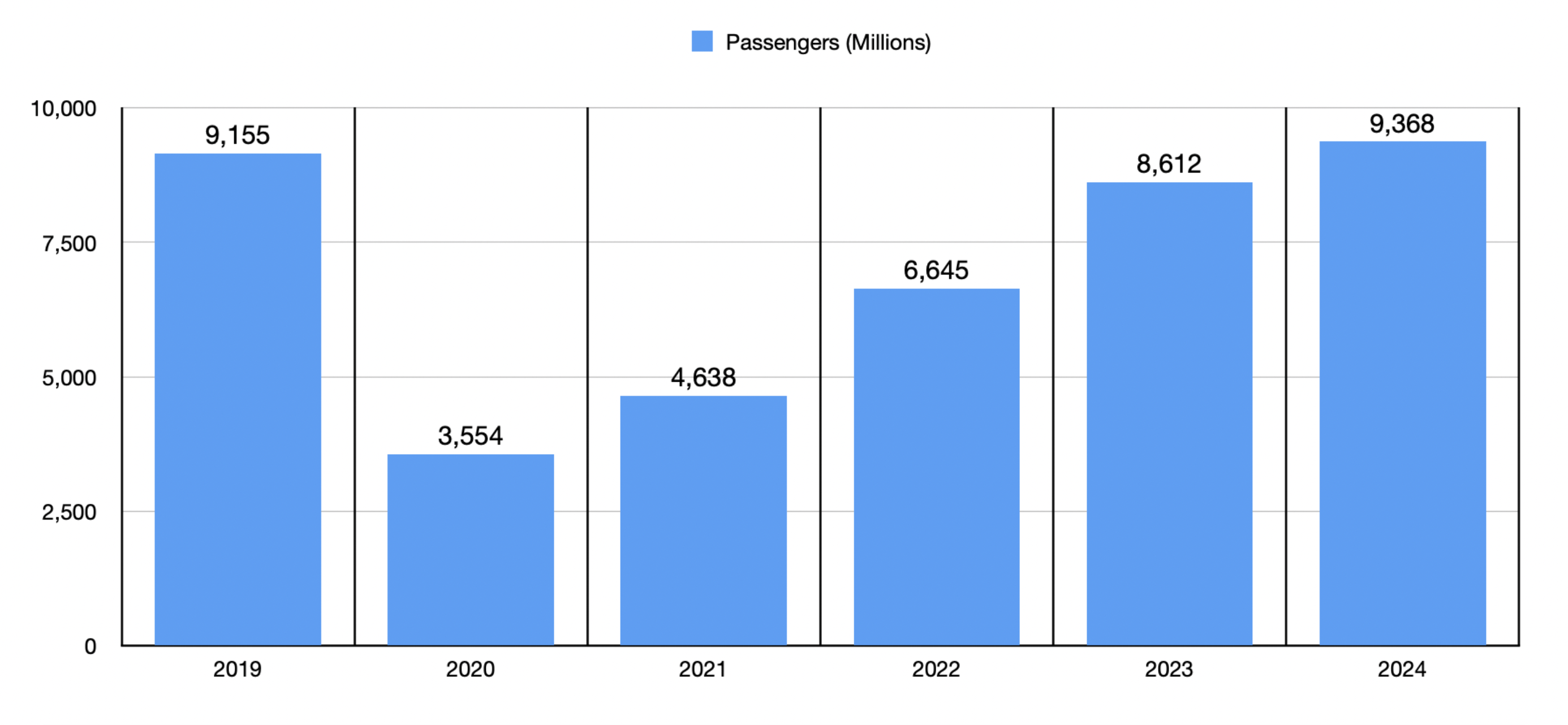

Regardless of what happens from an earnings perspective, the longer-term outlook for the company does look positive. I say this because global air traffic this year is expected to consist of about 9.4 billion passengers. That's up from the 8.6 billion estimated for 2023 and it compares nicely to the 9.2 billion that was the prior peak seen in 2019. Long term, I would be shocked if we don't see continued growth on this front, which should help the company from a revenue and, eventually, profit and cash flow perspective.

{kind=link}

Author - Airports Council International

Speaking briefly on the possibility of the merger between JetBlue Airways and Spirit Airlines still happening, it does look to be a long shot. But it's definitely not out of the question. I say this because, on January 19th, news broke that JetBlue Airways and Spirit Airlines filed an appeal with the First Circuit regarding the judgement against the merger. There's no telling how long this will take or what the outcome will be. Certainly, I would say that the odds are still against a merger happening at this time. But in the event that it does take place, shareholders of either company stand to benefit.

Takeaway

It will be interesting to see what happens when JetBlue Airways announces earnings in the coming days. Irrespective of where the company stands on that, the longer-term outlook for the company and the industry looks to be positive. I am less optimistic when it comes to Spirit Airlines at this time because of continued weakness on its bottom line. To management's credit, the firm did announce on January 3rd that it completed a sale leaseback transaction for 25 aircraft that resulted in a $465 million repayment of debt because of $419 million in cash proceeds. That should help the debt picture in the near term. But management continues to look for strategic alternatives that, they assert, do not include bankruptcy. As for JetBlue Airways, my overall view is that shares are fundamentally attractive at this point in time. This is based on relatively robust cash flows for 2023. If the deal does end up transpiring, synergies could create a lot of value for shareholders in both firms. So either way, I view JetBlue Airways in a positive light while looking at Spirit Airlines in a more neutral way because of the uncertainties involving the business.

For further details see:

Assessing JetBlue Airways During A Time Of Significant Uncertainty Over Spirit Airlines Turmoil