ASB - Associated Banc-Corp: Limited Downside Strong Upside Potential

2023-07-21 14:44:57 ET

Summary

- Associated Banc-Corp's recent report shows a growing book value per share and a positive outlook for 2023, with total loan growth predicted to grow 6-8% YoY.

- ASB maintains a solid liquidity coverage for uninsured loans and prioritizes dividends and organic growth, offering a forward yield of 4.49% and a historical dividend growth rate of 8.19%.

- Associated Banc-Corp's loan portfolio is well diversified across regions, with a ROE of 9.9% making it easier to support the dividend.

Introduction

The very recent report from Associated Banc-Corp ( ASB ) shows that the company has been able to quickly grow the book value per share, now sitting at $18.42 as of the Q2 2023 report. Strong loan growth is set to accelerate earnings for 2023, and I want to be a part of that. ASB maintains a very solid loan portfolio and a fantastic real estate portfolio, which has a proven record of yielding larger returns that ASB passes down to shareholders. The outlook for the remaining part of 2023 is positive, as total loan growth is predicted to grow 6 - 8% YoY. The TTM numbers showcase ASB having an ROE of 9.93%, and with stronger expected growth I think this margin will grow further, making the current price of ASB appealing to get in at before the progress is visible.

ASB maintains a very solid liquidity coverage for uninsured loans, 177% to be exact. Besides just investing in a solid business, ASB has maintained a priority of diverting earnings to shareholders as much as possible. Per their own accord, the two highest priorities in the business are dividend and organic growth. With an FWD yield of 4.49% and a historical dividend growth rate of 8.19%, I believe investors will get a very satisfying return from here on out.

Company Structure

Associated Banc-Corp is a very old business, dating back to 1861 when it was founded. The company these days operates as a bank holding company, providing various banking and nonbanking products to clients in the United States. The primary regions where ASB operates however are Wisconsin, Illinois, and Minnesota.

Within the business, there are three different segments, Corporate and Commercial Specialty, Community, Consumer, and Business, and lastly Risk Management and Shared Services. Within the first segment, the operations revolve around lending solutions, which include commercial loans and lines of credit. Besides that, they also offer real estate financing and leasing services.

The second segment offers residential mortgage loans and installment loans. This broad exposure has netted the company a very solid deposit base of $30 billion.

Liquidity (Earnings Presentation)

During its many years of operations, ASB has made it a priority to ensure they maintain a very strong financial position where they don’t lack capabilities to cover deposits. The total uninsured and uncollateralized deposits into ASB is only at 24%, a decrease from 27% in Q3 2022. This is a healthy state to be in and doesn't deleverage ASB in any way. Besides, they have readily available liquidity to cover for 103% of these uninsured depositors.

Loan Portfolio (Earnings Presentation)

Looking closer at the loan portfolio, ASB is very well diversified when looking at the regions where the loans are made. Wisconsin makes up the largest portion at 27%. It seems that ASB has been able to further make its loan portfolio robust as the LTV has increased over the last 12 months. Mortgage LTV sits at 78% currently, which is a good place to be at. It indicates that they aren’t too freely lending out capital and fueling “unsafe” loans, in my opinion. Same with auto finance, an LTV of 83% displays competence on the side of ASB, and the market for that has been rather volatile , and ASB's ability to hedge with higher down payments makes their portfolio able to withstand downturns better.

Fundamentals

The ROE for ASB is a point to address and improve upon, I think. But seeing as interest has increased substantially in the last 12 months, the potential for stronger earnings seems to be ahead right now for ASB. As we saw with JPMorgan ( JPM ) and their last report , the impacts of higher interest rates are only now beginning to show.

Historically, the last 5 years have had an average ROE of 8.64%, which ASB has outgrown in the last 12 months and now has 9.93% instead. In the last 5 years, the asset base has grown by 4.05% yearly too, and seeing ASB able to leverage this into a higher ROE is comforting when viewing the investment potential of the business.

Earnings Call

From the last earnings call by ASB, there are some comments that stuck with me. CEO Andrew Hammering said the following

-

" To fund our growth and enhance our liquidity profile, we tap the wholesale markets to increase deposits by $1.7 billion during the quarter. This reliance on wholesale funding sources is expected to dissipate over time as we begin to realize the full impacts of our customer acquisition and relationship deepening initiatives ".

This shows that ASB is still seeing a lot of potential in some parts of the market and tapping into them is a priority to drive further earnings growth. With increased economic activity in the US, the incentive for a lot of the customers that ASB has for investing in expansions should be higher. This, of course, benefits ASB, as the total loan deposits will be rising as a consequence.

- " Over the last seven quarters, the expansion of our C&I business and growth in our new equipment finance and asset-based lending verticals, has helped us expand our offerings and sharpen our focus on high-quality relationship-based lending. This enables us to de-emphasize lower-yielding non-relationship asset classes such as third-party originated mortgage ".

The quote above here shows that the investment and strategic approach that ASB has had is paying off. Growing their loan portfolio with growth and high-quality loan categories should enable the ROE to continue rising over the coming quarters, a factor that further emphasizes the appeal of ASB right now.

Valuation & Comparison

{kind=link}

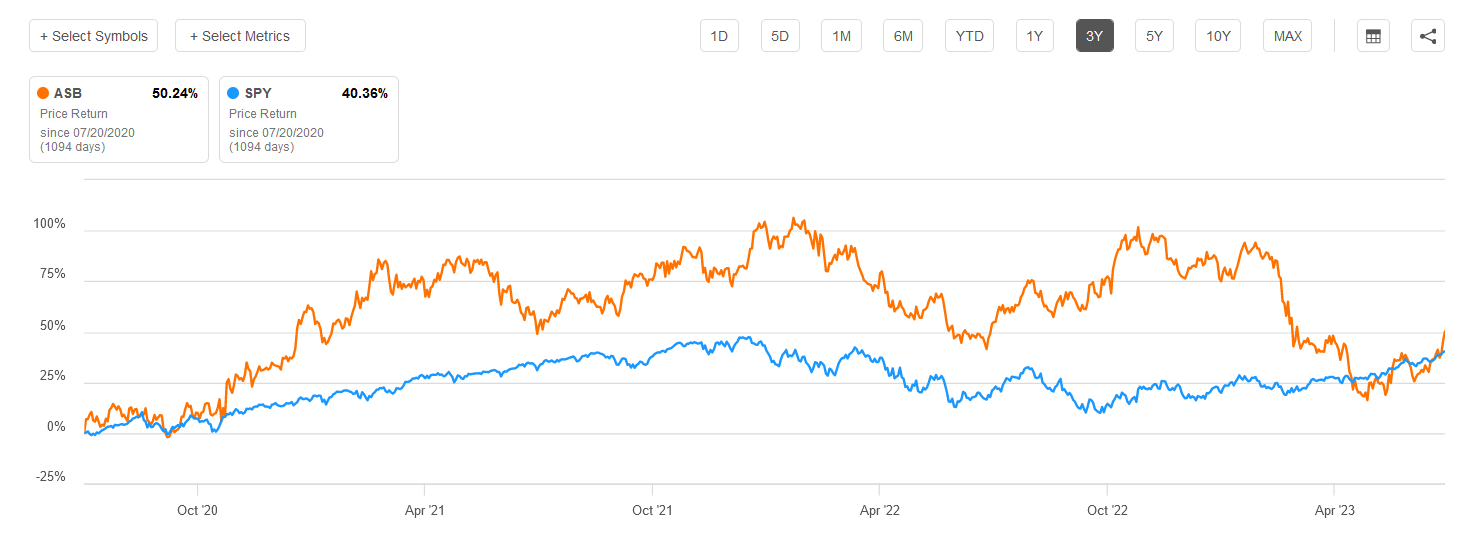

The performance of ASB in comparison to the SPY has been quite satisfactory. The share price for ASB is up 50% during the last 3 years, whilst the SPY is up 40%. This isn't accounting for the dividend yield, either, which for ASB has been around 4% at least during this period.

Dividend Summary (Seeking Alpha)

Going forward, the appeal with ASB comes for me largely with the dividend and the growth history of it. Increasing the dividend for 11 years in a row, and the last 5 years having a 8.19% yearly growth rate, paints a very bright future for investors in ASB. An 8% growth rate for the dividend would mean the yield will stay around its current 4.5% - 5% range. Pair that with the EPS growing 9.4% each year for the last 10 years, and ASB seems to offer investors the potential for a market-beating return. Some might question how reliable this dividend yield is, the payout ratio is 32%, and with strong prospects of a higher ROE thanks to higher interest rates, I’d say the sustainability of the yield is very solid.

Risk Associated

ASB appears to have a low likelihood of needing to sell its securities at a loss. However, it is not entirely out of the realm of possibility that the company might intentionally sell some assets at a loss. This strategic decision could be driven by the management's desire to generate additional funds to fuel income growth or to streamline operations and reduce costs.

By taking a calculated hit in the short term, the management may be looking to pave the way for more substantial growth and profitability in the long run. Such a move could demonstrate the company's forward-thinking approach and willingness to make strategic sacrifices to bolster its prospects. It is essential for the management to carefully assess the trade-offs and potential benefits of such actions to ensure they align with the company's overall objectives and long-term vision.

I find the current position that ASB is in to be good enough that the above-mentioned risks shouldn't weigh on the valuation of the business or discard a buy case for it, either.

Investor Takeaway

ASB has a very rich history dating back to 1861. The business is diversified and has in my opinion and very strong loan portfolio where the LTV is at a good percentage that doesn't open up risks to ASB. The ROE is at the highest rate in the last 5 years and I view them likely to go higher, resulting in more potential capital going towards the dividend and building up the portfolio. For investors seeking a market-beating return over the long run, ASB seems to offer such a potential right now, which is why I am rating it a buy.

For further details see:

Associated Banc-Corp: Limited Downside, Strong Upside Potential