AIZ - Assurant: Growth And Sticky Rate Hikes Reduce Upside Downgrade To Hold

2023-06-28 00:14:03 ET

Summary

- Assurant, a global provider of risk management products and services, has risen 6.79%, since my last article, outperforming the S&P 500.

- The company's diversified businesses have enabled a 6.45% YoY increase in Q1 revenues, but potential recessionary pressures and increasing interest rates may dampen potential upside.

- Despite Assurant's strong operational position and growth potential, I rate the stock as a 'hold' due to the aforementioned concerns.

Assurant ( AIZ ) is an Atlanta, Georgia-based global provider of risk management products and services, with operations across a range of specialty niches, P&C, technological device, etc. insurance markets.

Since my last article, Assurant has appreciated 6.79% - before dividends - versus the S&P 500, which has grown 5.98% in the same period.

{kind=link}

The insurance firm's diversified businesses, which span connected living, auto, rent, and P&C, have enabled $2.64bn in Q1 revenues, a 6.45% increase YoY; a net income of $113.60mn, a 21.92%; and a free cash flow from $211.20mn, a 138.95% increase.

Introduction

Broadly, Assurant's corporate strategy remains the same; the company reaffirms its core, alpha-rich business, enabling superior cash flow generation and subsequent deployment strategies, scale through leadership, talent-retaining and ESG capturing sustainability targets, and ensuring value leadership through the synergetic confluence of these strategies.

{kind=link}

Although Assurant has rallied upwards, in line with my expectations, and remains operationally strong, positioned for megatrend growth, and maintains a strong capital allocation strategy, I believe potential recessionary pressures, constantly increasing interest rates, and profitability concerns dampen potential upside levels. Therefore, I rate Assurant a 'hold'.

Valuation & Financials

General Overview

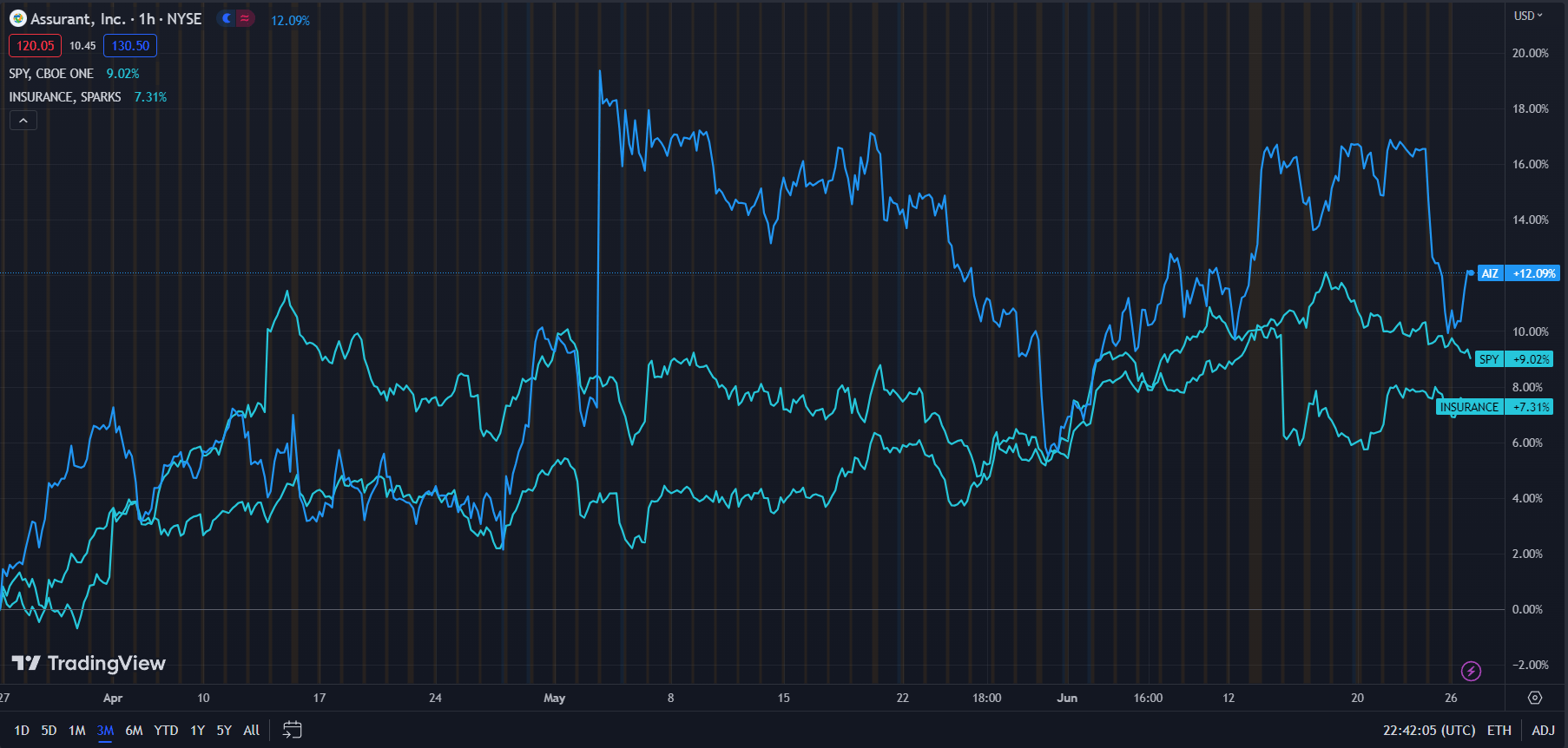

In the trailing three-month period, Assurant- up 12.09%- has experienced superior price action to both TradingView's Insurance Index- up 7.31%- and the broader market, represented by the S&P 500 ( SPY ), up 9.02%.

{kind=link}

This mirrors Assurant's superior cash flow performance and growth QoQ and YoY versus the general market and insurance companies as a whole.

That said, I do not believe Assurant's momentum can be sustained over the next few quarters, with interest rates continuing to remain above 10Y average levels- working against the firm's fixed-rate heavy portfolio- and recessionary pressures reducing discretionary purchases.

Comparable Companies

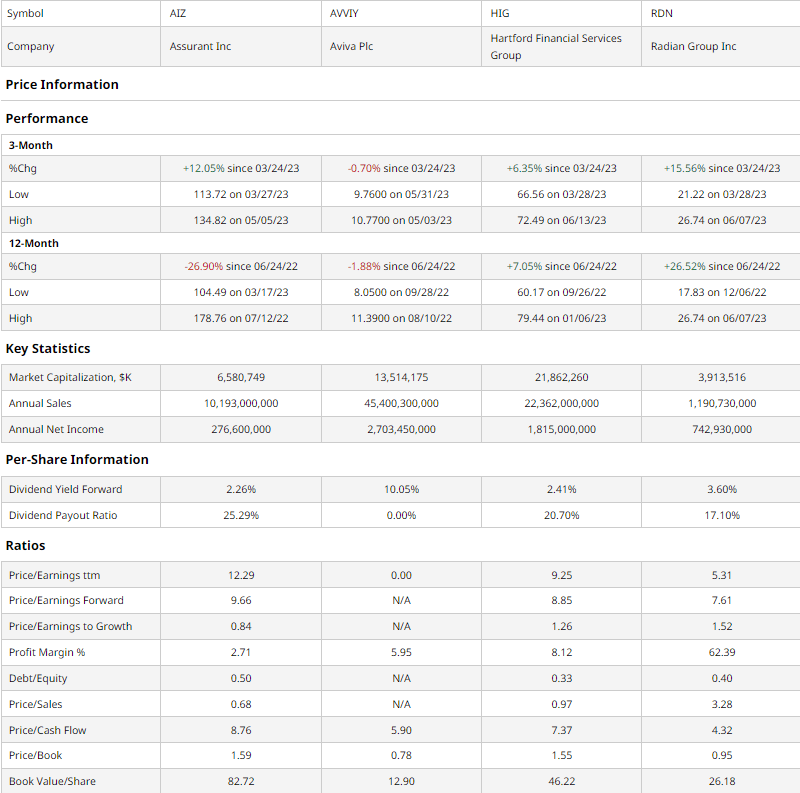

As I mentioned in my previous article, Assurant operates across niche markets and can therefore not be directly compared to other insurers. Thus, Assurant is most comparable to other multi-line insurers, such as British insurer Aviva (AVVIY), banking and credit insurer, Hartford Financial ( HIG ), and mortgage and title insurance provider Radian Group ( RDN ).

{kind=link}

As demonstrated above, Assurant has experienced the second-best quarterly performance, rallying in the face of the poorest YoY price action. However, while I do believe Assurant has space for the upside, I believe there is a greater chance for volatility due to higher valuation and operational pressures.

For instance, Assurant maintains the poorest multiples-based valuation when considering trailing and forward P/E, P/CF, and P/B ratios. However, when assessing PEG, P/S, and book value per share, Assurant sustains a balanced value proposition for investors.

However, Assurant continues to contend with profitability concerns with a relatively higher debt/equity ratio limiting reinvestment and inorganic growth capabilities.

Valuation

According to my discounted cash flow analysis, at its base case, the fair value of Assurant is $134.53, meaning, at its current price of $126.36 the stock is undervalued by 6%.

My model assumes a discount rate of 9%, incorporating a moderate equity risk premium and balanced cap structure of the company, with a relatively average debt/equity ratio. Additionally, to address the impact of sticky interest rates on its bond-heavy portfolio and downstream impacts on connected living insurance demand, I chose a conservative revenue growth rate of 6%, despite an average 5Y CAGR of 10.83%.

{kind=link}

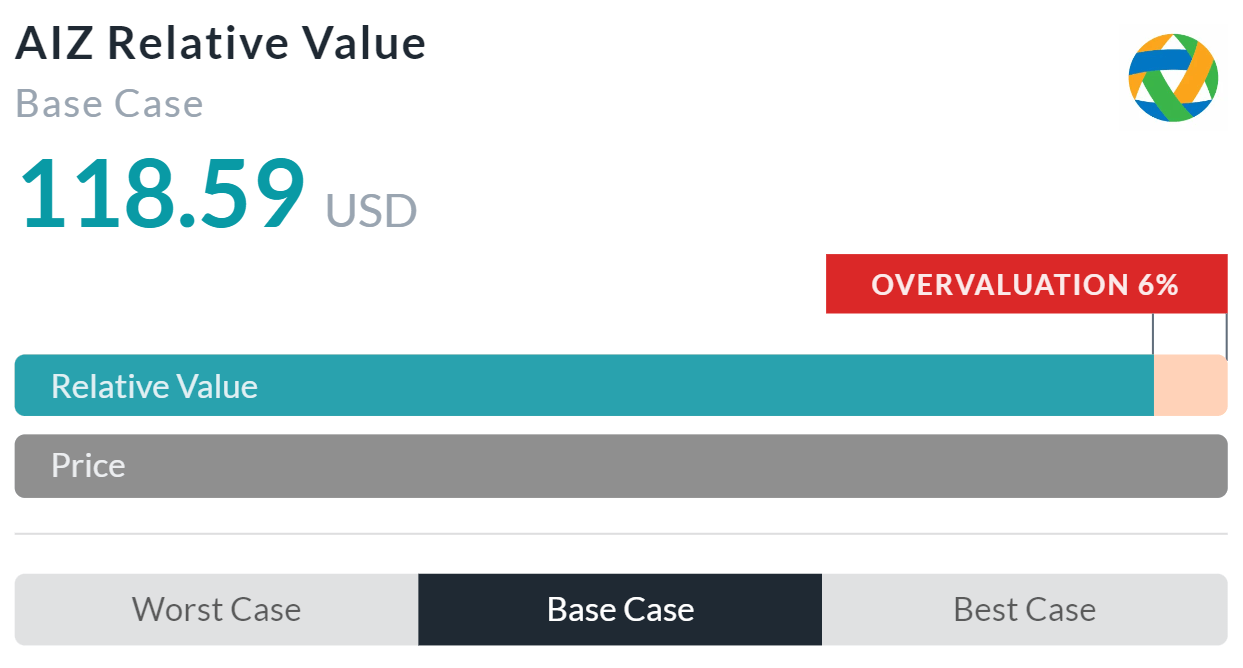

Alpha Spread's multiples-based relative valuation tool largely supports my 'hold' rating, calculating a base case overvaluation of 6%, meaning the stock's relative value should be $118.59.

While this inverses my analysis, Alpha Spread only projects a moderate overvaluation, and I only project a moderate undervaluation, supporting a fair value proposition with potential upside in the mix.

Therefore, averaging out my DCF valuation and the Alpha Spread's relative value, Assurant trades at its fair value, with income potential for investors and potential long-term positive price action.

Assurant Remains Operationally Strong, But There Is Greater Forward Uncertainty

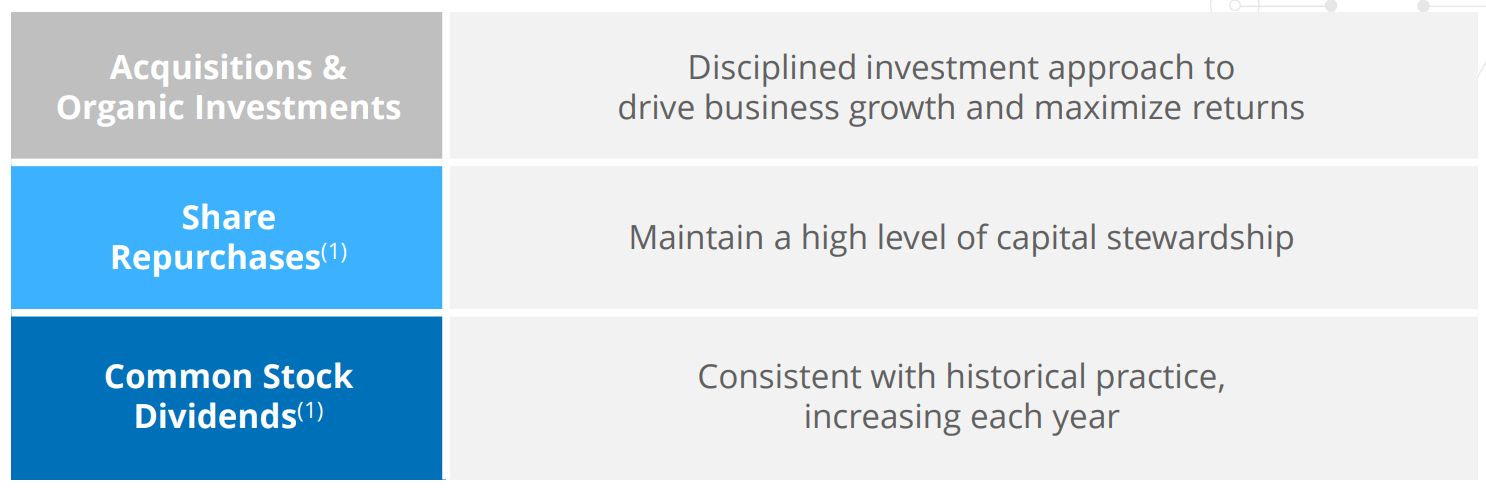

Central to Assurant's recent success has been its ability to deploy capital in a disciplined and judicious manner. The firm prioritizes operational growth, both via organic reinvestments and M&A activity. This reinvestment has enabled Assurant to dominate the niche of connected living and position itself for IoT, megatrend-driven growth. After the growth-centric investment, Assurant aims for prudent capital stewardship via its stable and growing 2.26% dividend and consistent share repurchases, with over 68% of shares repurchases since IPO.

{kind=link}

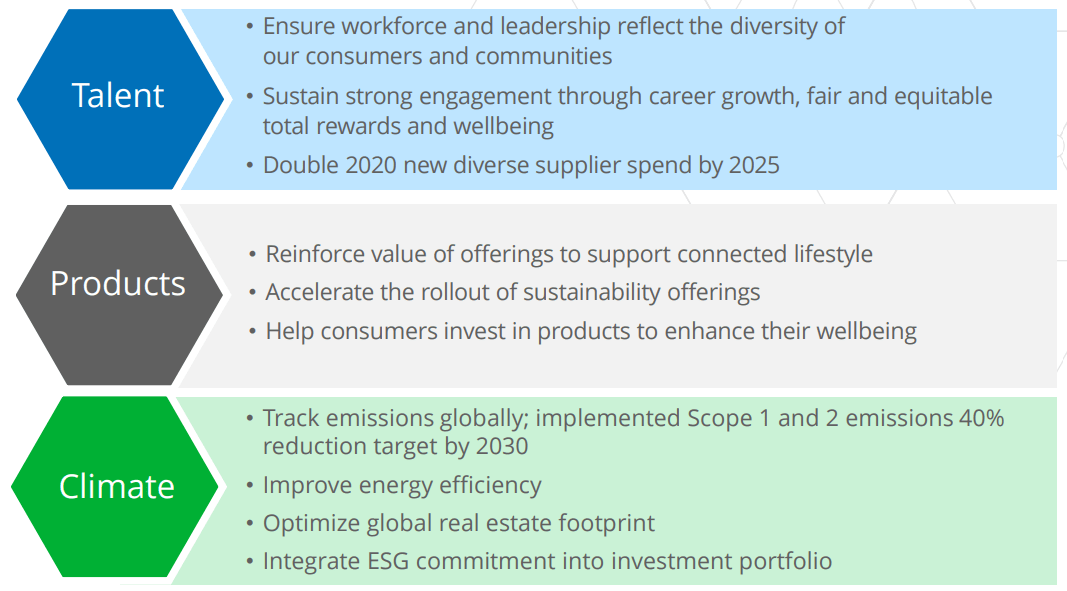

To additionally drive shareholder value, Assurant has aimed for an ESG index inclusionary policy which would additionally support superior business operations. For instance, through greater consumer-facing lingual diversity, the firm is able to enhance consumer engagement, while expanding its product variety across sustainability enabling Assurant to capture growth in developing industries and markets.

{kind=link}

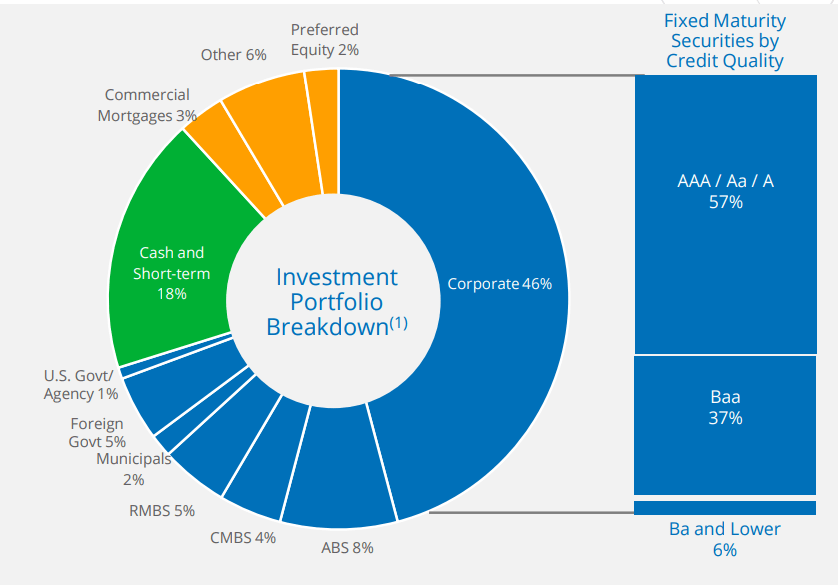

However, although the insurer maintains a stable portfolio of fixed income assets, primarily with high grade fixed maturities, this asset mix also presents concerns with sticky interest rates, reducing the net asset value of Assurant's portfolio. This may reduce long-term income capabilities, with profitability already a point of contention for Assurant.

{kind=link}

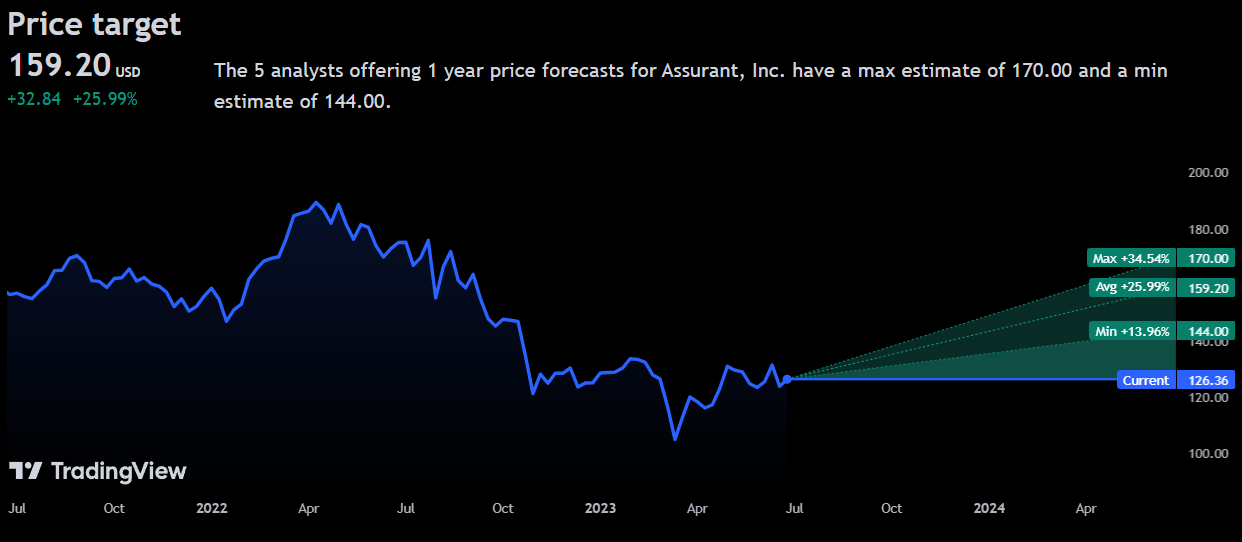

Wall Street Consensus

Analysts nonetheless paint a more positive outlook for Assurant, projecting an average 1Y price increase of 25.99%, to a price of $159.20.

{kind=link}

Even at the minimum predicted price increase, analysts expect a 13.96% share price growth to $144.00.

I believe analysts overestimate Assurant's 1Y prospects due to expected reversion from a historic TTM price decline and lower hesitancies about interest rates and profitability than I hold.

Risks & Challenges

Interest Rates Continue to Threaten Already Weak Profitability & Balance Sheet Quality

As aforementioned, Assurant's balance sheet is primarily comprised of fixed-maturity bond securities. Although these assets are highly rated and do not necessarily promise the highest yields, Assurant risks a poorer balance sheet and even weaker returns with continually rising or high-interest rates. With profitability and net income margins declining over the past few quarters, Assurant is especially sensitive to this risk.

Third-Party Demand Risk Is Increasingly Prevalent in Growth Industries

Assurant's dominance in connected living insurance products has been a key growth driver over the past 5Y period. However, insurance products such as mobile carrier insurance and device protection are linked with inherent demand for these products. With higher interest rates, consumers are finding it increasingly difficult to finance these products which may cause a mid-term slowdown in demand.

Conclusion

Looking forward, although I believe Assurant is positioned for long-run operational success, in the medium-term, Assurant is exposed to downward cash flow pressures from higher interest rates and laggard demand.

For further details see:

Assurant: Growth And Sticky Rate Hikes Reduce Upside, Downgrade To Hold