AIZ - Assurant Remains Cheaply Valued Even After Its Rally

2023-09-20 01:00:20 ET

Summary

- Assurant stock has offered a total return of 14% in nine months but remains cheaply valued from a long-term perspective.

- The company improved its business performance and outlook in the second quarter.

- Assurant's earnings per share are expected to grow by 11% this year, with sustained recovery and growth predicted for the future.

In the beginning of this year, I recommended buying Assurant ( AIZ ) for its nearly 5-year low valuation level and an expected recovery in its business performance. Since my article, the stock has offered a total return of 14%, in just nine months. I first recommended buying this high-quality insurer in the spring of 2021 and I have maintained my “buy” rating since then, as some temporary business headwinds have kept the stock cheaply valued from a long-term perspective. Notably, the company significantly improved its business performance and its outlook in the second quarter. The stock has rallied 33% off its bottom in March but it remains cheaply valued from a long-term point of view. Therefore, investors should not rush to take their profits.

Business overview

Assurant is a property-and-casualty insurer that sells its insurance products in North America, Latin America, Europe, and Asia Pacific. It operates in two segments: Global Lifestyle and Global Housing. The former includes insurance products for the owners of vehicles, mobile phones, electronics and appliances while the latter involves insurance for homeowners.

Assurant has been hurt by high inflation, which has had a double impact on the performance of the company. First of all, high inflation has greatly increased the repair costs incurred by the company in its auto insurance business. While the Fed has managed to drive inflation from a 40-year high of 9.2% in the summer of 2022 to 3.6% now, inflation still weighs on the performance of the auto insurance division of Assurant.

Fortunately, management is doing its best to address this issue. Assurant recently implemented material hikes in its insurance premiums in order to offset the effect of inflation on the amounts of repairs. In addition, the company has begun to partner with its clients in order to achieve cost savings on some claims. Management expects inflation to continue to weigh on the performance of the auto insurance division for a few more quarters but it expects a strong recovery in this segment afterwards.

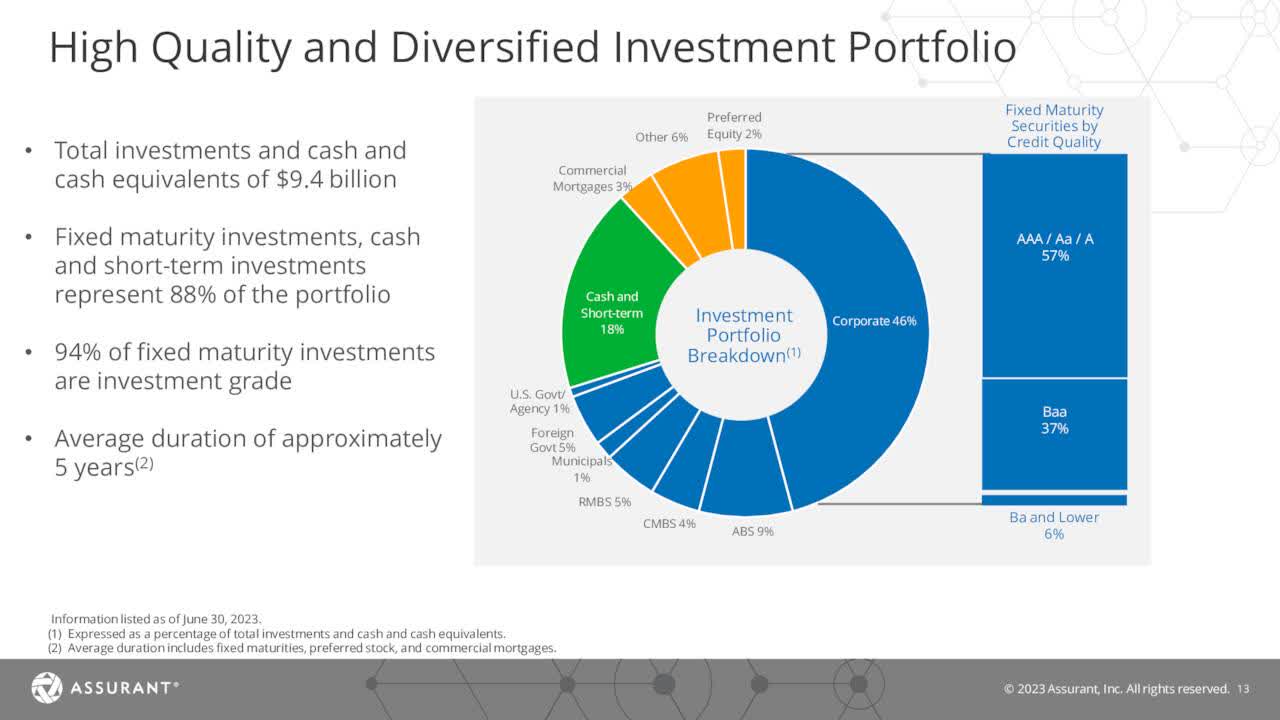

Inflation also has an adverse effect on the investment portfolio of Assurant. Fixed-maturity investments comprise 88% of the total value of the investment portfolio of the insurer.

{kind=link}

Source: Investor Presentation

The surge of inflation last year and the resultant surge of interest rates to a 15-year high this year have caused material losses in the mark-to-market value of the bonds that comprise the investment portfolio of Assurant.

However, it is important to realize that most of the damage has already been done. The Fed has raised interest rates to 15-year highs and hence it is not likely to raise them much further. As a result, Assurant is unlikely to incur further losses in its investment portfolio. Moreover, the average duration of its fixed-maturity securities is 5 years. Whenever some securities mature, Assurant can reinvest the proceeds at much higher yields and thus enhance the average yield of its investment portfolio. To cut a long story, the damage from inflation has already been done and the yield of the investment portfolio of Assurant is likely to significantly improve in the upcoming quarters, as the insurer will invest its cash at multi-year high yields from now on.

It is also important to note that Assurant exhibited improved business performance in the second quarter . Its home insurance business benefited from much higher insured values and state-approved rate hikes due to higher claim severities. As a result, this segment more than doubled its adjusted EBITDA over the prior year’s period.

While the Global Lifestyle segment faced the aforementioned headwind from high repair losses, the strong performance in the insurance of mobile phones and appliances partly offset this headwind. As a result, the adjusted EBITDA of this segment dipped only 11%. Overall, the adjusted earnings per share of Assurant grew 32%, from $2.95 to $3.89, and exceeded the analysts’ estimates by an eye-opening $1.14. Assurant has exceeded the analysts’ estimates by a wide margin in each of the last three quarters, thus confirming its sustained business momentum.

Indeed, management recently improved its outlook for the full year. It raised its guidance for the growth of annual earnings per share from low-single digit to high-single digit. Analysts seem to agree with the outlook of management, as they expect the company to grow its earnings per share 11% this year, from $11.13 to $12.36.

Even better, analysts expect a sustained recovery of Assurant, as they expect its earnings per share to grow by an additional 14% next year and 18% in 2025. Thanks to the aforementioned expected recovery of the investment income of Assurant, the anticipated recovery of the earnings of its auto insurance business and the continued investment of the company in its technology platforms, the company has good odds of meeting the above analysts’ estimates.

Valuation

Assurant is currently trading at a forward price-to-earnings ratio of 11.4x . This valuation level may seem extremely cheap to some investors but it is important to realize that property-and-casualty insurers tend to have a cheaper valuation than the broad market due to the unpredictable nature of catastrophe losses. Nevertheless, the price-to-earnings ratio of Assurant is lower than the 10-year historical average of 13.8x of the stock.

It is also remarkable that the stock is trading at only 10.0x times its expected earnings in 2024 and 8.5x times its expected earnings in 2025. These earnings multiples are certainly extremely low. Whenever the company recovers from the above mentioned effects of inflation, its valuation is likely to revert towards its historical average level. Therefore, the stock has great upside potential. For instance, if Assurant meets the analysts’ estimates next year and its price-to-earnings ratio expands from 10.0x to 13.8x, the stock will rally 38% from its current price. While valuation is not likely to expand at such a fast pace, the stock has significant upside potential in the upcoming years thanks to its solid earnings growth and its cheap valuation.

Risks

Just like all the property-and-casualty insurers, Assurant bears the inherent risk of its business, namely the risk of a year with extremely high catastrophe losses. However, the company has proved capable of pricing its risks efficiently. To be sure, Assurant has grown its earnings per share in 7 of the last 9 years, at a 6.5% average annual rate. Investors should also keep in mind that insurers raise the premiums they charge significantly after a year with high catastrophe losses. As a result, they eventually get compensated for the loss claims they paid in the previous year. Overall, Assurant has proved capable of enduring high catastrophe losses over the long run.

The other risk is the adverse scenario of prolonged inflation for years. In such a case, the company is likely to continue paying excessive amounts for the repair claims in its auto insurance business. On the other hand, its investment portfolio is likely to benefit from high interest rates, as the new premiums and the funds from matured investment securities will be invested at high yields. While the net outcome is hard to predict, Assurant is not likely to be severely hurt even in such an unfavorable scenario.

Final thoughts

Assurant has begun to recover strongly from the impact of high inflation and thus its stock has rallied 33% off its bottom in March. Nevertheless, the stock remains cheaply valued while the company is likely to keep growing its earnings significantly in the upcoming years. Therefore, investors should remain invested in this high-quality insurer.

For further details see:

Assurant Remains Cheaply Valued, Even After Its Rally