ASTE - Astec Industries: Strong Balance Sheet To Help Navigate Current And Potential Headwinds

2023-04-27 09:30:57 ET

Summary

- Net sales have set a new record in 2022 and are expected to increase again in 2023 and 2024 as the backlog is unusually high.

- The company's profit margins remain depressed as a consequence of current macroeconomic headwinds.

- The company's debt doesn't represent a significant risk as inventories are unusually high.

- The dividend is safe and the management will likely be able to execute its ambitious share repurchase program thanks to historically low cash payout ratios.

- This represents a good opportunity to acquire shares of the company at reasonable prices.

Investment thesis

Astec Industries ( ASTE ) is currently facing a very complex macroeconomic context. Inflationary pressures, supply chain tensions, labor shortages, and increased production costs are causing a significant negative impact on the company's gross profit and EBITDA margins. Furthermore, investors are increasingly concerned about a potential recession as a result of recent interest rate hikes aimed at stabilizing currently high inflation rates. This is why the share price has suffered a drop of almost 50% from all-time highs despite record sales and expectations of even higher sales for 2023 and 2024.

Despite this, I strongly believe that the current pessimism among investors represents a good opportunity to acquire shares of the company at more than reasonable prices since the balance sheet is very robust thanks to very low debt and huge inventories that can be converted into cash in the coming quarters. This means that, despite the current headwinds, the dividend presents a safe profile and the company can likely execute a large part of its ambitious share buyback program, which has the potential to deliver high returns for long-term shareholders.

A brief overview of the company

Astec Industries is a designer, manufacturer, and marketer of equipment and components used primarily in road building and related construction activities, as well as equipment for the mining, quarrying, construction, demolition, land clearing, and recycling industries and port and rail yard operators; industrial heat transfer equipment; commercial whole-tree pulpwood chippers; horizontal grinders; blower trucks; commercial and industrial burners; and combustion control systems. The company was founded in 1972, and its market cap currently stands at ~$917 million, employing over 4,000 workers.

Astec Industries logo (Astecindustries.com)

Astec operates under two main business segments: Infrastructure Solutions and Materials Solutions. Under the Infrastructure Solutions segment, which provided 66% of the company's total net sales in 2022, the company designs, engineers, manufactures, and markets a complete line of asphalt plants, concrete plants, and their related components and ancillary equipment as well as supplies asphalt road construction equipment, industrial thermal systems, and other heavy equipment, and under the Materials Solutions segment, which provided 33% of the company's total net sales in 2022, the company designs and manufactures heavy processing equipment, in addition to servicing and supplying parts for the aggregate, metallic mining, recycling, ports, and bulk handling markets. The company also manufactures and sells replacement parts for its products and for products of other manufacturers.

Currently, shares are trading at $40.15, which represents a 49.81% decline from all-time highs of $80.00 on April 28, 2021. This fall occurred as a consequence of a series of headwinds linked to the current macroeconomic landscape, including manufacturing inefficiencies due to supply chain issues, inflationary pressures, increased production costs, and a potential recession due to recent interest rate hikes in order to stabilize high inflation rates worldwide.

Despite this, the balance sheet continues to be very robust and the company's fundamentals remain intact as it operates in an essential industry and, in addition, has expanded its operations through both high CAPEX and some recent acquisitions. That is why I consider that the current fall in the share price represents a good opportunity for long-term dividend growth investors.

Recent acquisitions

The company has historically boosted its growth through acquisitions and performed four acquisitions since 2020, which are poised to help it continue along the path of growth. Nevertheless, these acquisitions are relatively minor compared to the size of the company as the management is quite conservative in relation to the use of cash.

In July 2020, the company announced the acquisition of CON-E-CO, which provided the company with a broader line of concrete batch plant manufacturing. The business was owned by Oshkosh Corporation ( OSK ) and Astec Industries paid $13.8 million for the acquisition. In August 2020, the company also announced the purchase of concrete equipment from BMH Systems located in Canada for $15.6 million. And during the same year, the company also acquired certain assets of Grathwol Automation, which develops and provides advanced telematics and remote diagnostics for construction equipment and related products and services, for $6.0 million.

More recently, in March 2022, the company announced the acquisition of MINDS Automation Group, a leader in plant automation control systems and cloud-based data management in the asphalt industry, which is headquartered in Canada but has locations in the United States, United Kingdom, France, and Belgium, for $19.3 million.

These acquisitions are poised to help the company maintain its leading position in the road building industry, but as a consequence of these investments and a recent build-up of inventories in the current context marked by contracting margins due to increasing production costs, further acquisitions will likely require some time to happen.

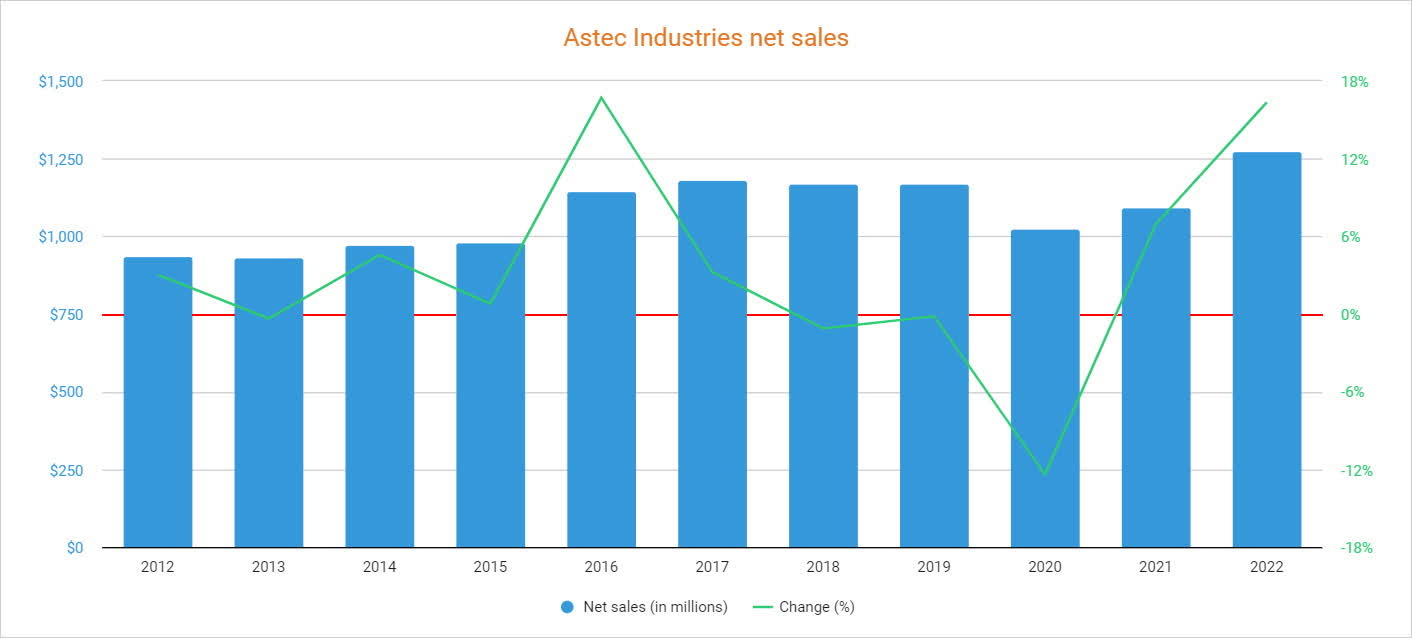

Net sales broke records in 2022 and are expected to keep rising

Overall, the company's net sales have increased over the years at a more than acceptable rate, but declined by 12.4% in 2020 as a consequence of disruptions caused by the coronavirus pandemic. Nevertheless, they partially recovered in 2021 with an increase of 6.94% and reached new highs in 2022 with a further 16.34% increase to $1.27 billion.

{kind=link}

More specifically, net sales increased by 2.39% year over year during the first quarter of 2022, 14.63% during the second quarter, 18.10% during the third quarter, and 31.25% during the fourth quarter. Furthermore, the backlog for the Infrastructure Solutions segment is currently at ~$567.1 million, which represents a 26.21% increase compared to 2021, whereas the backlog in the Material Solutions segments currently stands at $341.2 million, which represents an 8.91% increase compared to 2021. This means that net sales are expected to remain high in the coming quarters as they are expected to increase by 9.45% in 2023, and by a further 5.04% in 2024.

In order to drive sales growth, the management plans to expand its parts and service business, its product portfolio, its dealer networks, and operations outside the United States. In this regard, and using 2022 as a reference, 80% of the company's total net sales are generated through operations within the United States, whereas 20% take place in the rest of the world, with a stronger presence in Canada, Australia and Oceania, and Africa.

Still, the company's depressed margins have caused a drop in the share price despite increasing net sales, which caused a significant decline in the P/S ratio to 0.720.

This means the company currently generates net sales of $1.39 for each dollar held in shares by investors, annually. This ratio is 28.22% below the average of the past decade of 1.003, and represents a 59.48% decline from decade highs of 1.777, and shows the current high pessimism among investors as the company's capacity to convert sales into actual cash has been seriously affected by current headwinds.

Margins remain depressed as inflationary pressures and supply chain issues persist

The company's gross profit and EBITDA margins have been relatively high over the past decade and allowed it to generate generous amounts of cash, but they declined in 2018 and, despite a significant recovery in 2019, 2020, and 2021, a series of headwinds are again having a strong impact on profit margins, including inflationary pressures, rising production costs, negative manufacturing efficiencies due to supply chain issues that have recently shown signs of improvement, and labor shortages.

During the fourth quarter of 2022, the gross profit margin remained at 20.58%, and the EBITDA margin showed a slight improvement to 3.09% as the company is raising the price of its products while volumes are high and inflationary pressures are starting to stabilize. Nevertheless, these profit margins are still depressed and are not enough to keep the company profitable enough, and inflationary pressures, although more moderate, are expected to remain a headwind during 2023.

In order to improve the company's profitability by simplifying its operations, the management decided to close its Mequon facility in 2020, and its Tacoma facility in 2021, transferring their production lines to other manufacturing facilities. Also, the company is currently planning to implement a standardized ERP system in its operations and is investing in more efficient equipment to improve gross profit margins by 2024. Even so, no significant improvement can be expected in the short term as the headwinds have not been completely resolved due to the complex macroeconomic context, which is why the share price remains depressed. Luckily, the balance sheet is, in my opinion, strong enough to overcome these headwinds and even a potential recession.

The balance sheet is very robust as inventories are highly inflated

The company's debt has historically been near non-existent but increased to $78.1 million in 2022. In this regard, the company's cash position suffered a strong weakening due not only to the recent acquisition of MINDS Automation Group (and the other three acquisitions in 2020) amidst current headwinds but also due to increased CAPEX in order to increase capacity and productivity, as well as the fact that the company has built vast amounts of inventory in order to respond to its unusually high backlog.

In this regard, inventories of $298.7 million at the end of 2021 increased by $94.7 million to $393.4 million at the end of 2022, which has caused cash from operations of -$73.9 million. Still, cash from operations is expected to be strong in the coming quarters as such inventories are used to meet the current high market demand. Furthermore, the company currently holds $62.80 million in cash and equivalents, which will also help navigate current and potential headwinds.

That is why the debt does not pose a significant risk to the company as it is most likely of a temporary nature. Even so, the high CAPEX used to improve the efficiencies of the company's operations and integrate the operations of the recently acquired companies remain high as trailing twelve months' CAPEX currently stands at $40.70 million, although this expense should be reduced over time once such projects are completed. In this regard, CAPEX is expected to significantly decline to the $25 million to $35 million range in 2023.

But in addition to depressed profit margins, the acquisition of MINDS Automation Group, increasing inventories, and heavy investments in efficiency and capacity improvements, the company has also delivered a growing dividend and performed share buybacks in 2022, which has been a way of returning cash to investors, but also a relatively significant expense for the company.

The dividend is safe as the cash payout ratio has historically been very low

Since 2018, the company has performed three dividend raises from a quarterly dividend of $0.10 per share to a quarterly dividend of $0.13. The latest raise was announced in October 2022 when the company announced a quarterly dividend of $0.13 per share, which represents an 8.3% increase from the prior dividend of $0.12 per share.

Said quarterly dividend (which represents a dividend yield on cost of ~1.30% at current share prices) has enormous potential thanks to a very low cash payout ratio, but due to the current (and potential) headwinds, high increases will likely be postponed as the management may opt for more gradual raises until the macroeconomic context allows for larger ones. To calculate the cash payout ratio, in the following table, I have calculated what percentage of cash from operations has been allocated each year to cover dividends paid and interest expenses, as in this way one can see the sustainability of the dividend through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $18.86 |

| $30.87 |

| $134.81 |

| $41.88 |

| -$29.79 |

| $112.43 |

| $141.5 |

| $7.4 |

| -$73.9 |

| Dividends paid (in millions) |

| $9.17 |

| $9.19 |

| $9.22 |

| $9.23 |

| $9.63 |

| $9.92 |

| $10.0 |

| $10.2 |

| $11.2 |

| Interest expenses (in millions) |

| $0.72 |

| $1.61 |

| $1.40 |

| $0.84 |

| $1.05 |

| $1.37 |

| $0.7 |

| $1.1 |

| $2.5 |

| Cash payout ratio |

| 52.41% |

| 35.00% |

| 7.87% |

| 24.03% |

| - |

| 10.04% |

| 7.56% |

| 152.70% |

| - |

As you can see, the company has been very conservative with cash usage over the years by issuing payouts well below its ability to generate cash from operations, which suggests that operations have a lot of potential to grow thanks to the large amounts of excess cash generated and, therefore, the dividend has great potential to increase over the years.

Although it is true that cash from operations has been negative at -$73.9 million in 2022, inventories increased by $94.7 million compared to 2021, and accounts receivable by $25.4 million while accounts payable increased by only $25.0 million, which means results weren't that bad after all as the company reported net income of -$0.1 million, which is actually very acceptable considering current headwinds. In addition, said low cash payout ratio allows the company to perform share buybacks, which is another way of passively returning cash to shareholders. But nevertheless, profit margins still need to improve so that the company can sufficiently cover dividend payments and CAPEX through operations, for which inventories will be essential to deal with said headwinds until they (at least partially) fade away.

Buybacks are expected to significantly decrease the number of shares outstanding

Whenever possible, the company has performed share buybacks in order to reduce the number of outstanding shares. In this regard, the company bought back $10.1 million worth of shares in 2022, and $115.7 million still remains available under the approved share repurchase program.

This means that investors can expect their position to passively increase over the years by holding the company's shares, which will eventually improve per-share metrics as there are fewer shares outstanding among which to divide its results.

Risks worth mentioning

Certainly, and despite the current and potential headwinds, I view Astec Industries' risk profile as very low thanks to its historically positive profit margins, low cash payout ratios, low debt level, and huge inventories. But still, there are certain risks that I would like to highlight for the short and medium term.

- Due to the expansion of its operations, the company could have trouble emptying its inventory without negatively affecting its profit margins. In this regard, unabsorbed labor could have a material impact on gross profit and EBITDA margins if demand does not exceed the company's current production capacity.

- Road construction projects could be limited in the event of a potential recession in the short to medium term due to recent interest rate hikes in order to moderate high inflation rates to healthier levels in the world's economies.

- Although the current level of debt does not pose a significant risk due to highly inflated inventories, the company could continue to borrow if supply chain and inflationary issues continue to impact its profit margins.

- Although the dividend cash payout ratio is very low, the management could freeze it if current headwinds extend for longer than the balance sheet allows without being significantly deteriorated.

- The company could pause or even cancel its share buyback program if profit margins remain depressed for much longer and do not allow for strong cash from operations.

Conclusion

Certainly, the situation that Astec Industries is facing is not easy, and proof of this is in its current share price, which already suffers a decline of ~50% from all-time highs. Inflationary pressures, increased production costs, supply chain issues, and labor shortages have had a significant impact on profit margins. In addition, inventories are highly inflated at a time when the world economy could face a potential recession as a result of recent interest rate hikes.

Still, I think times like these are the times when the most patient dividend investors should not lose sight of companies like Astec Industries as it finds itself with a very robust balance sheet thanks to very conservative cash usage over the years. Furthermore, the company operates in an essential industry that has changed very slowly over the years. That is why I believe that the company is prepared to navigate current headwinds and a potential recession and that the current share price represents a good opportunity for patient dividend growth investors interested in essential industries.

For further details see:

Astec Industries: Strong Balance Sheet To Help Navigate Current And Potential Headwinds