ALPMF - Astellas: Earnings Power Asset Factors Attractive Reiterate Hold On Valuation

2023-08-16 12:41:31 ET

Summary

- Astellas has closed its Iveric bio, Inc. deal in July and reported JPY 375Bn in quarterly sales in Q1.

- The company's earnings power and asset factors are bullish, but valuation factors are keeping me neutral.

- From this, I am closely watching the return on Astellas' Iveric investment to determine if it adds economic value.

- Net-net, reiterate hold.

Investment Summary

There are numerous investment updates that have emerged in the Astellas (ALPMY) (ALPMF) debate since my February publication . Chief among these are the firm's closing of its Iveric bio, Inc. deal in July, and the economic characteristics within its business model discussed here. It also printed JPY 375Bn in quarterly sales in Q1, on ~19x operating leverage for the period [ note, being a Japanese-based firm, its reports in JPY, consequently, for the purposes of consistency I'll be writing in terms of JPY in this report, unless otherwise stated, where USD $1.00. = JPY 145.56 at the time of writing].

Net-net, there are multiple facets to the investment case here. On earnings power and asset factors, I am bullish. But what has me sat at neutral are valuation factors. I believe its Iveric buyout could be accretive to value but we'll have to wait until the remainder of its FY'23 to see more of the details. I am watching ALPMF extremely closely from hereon in and will look to allocate if I see the return on its Iveric investment immediately adding economic value. Reiterate hold until then.

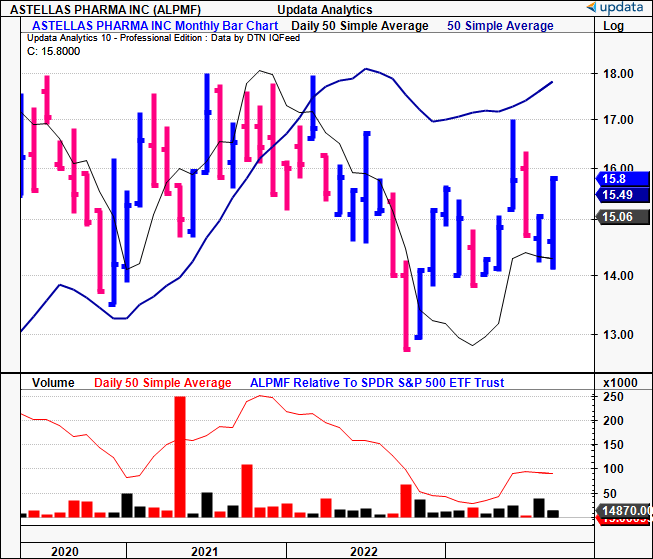

Figure 1. ALPMF Long-term price evolution (monthly bars, 2020—date)

{kind=link}

Recent developments in critical investment facts

1. Q1 earnings exhibit operating leverage

ALPMF printed its first quarter earnings the first week of August [note: the company reported its Q1 fiscal '23 numbers, corresponding to Q2 CY'23. For consistency and simplicity, I'll be talking in terms of Q1] . Revenues were down ~180bps YoY to JPY 375Bn. Still, this is ~25% of its full-year forecast of JPY 1,520Bn. Within this result was ~JPY 17.5Bn of Forex headwind.

It pulled this to core operating profit of JPY 65Bn, a 17.4% YoY growth schedule. Operating leverage was thus 9.6x and represents quality earnings in my view. Adding back JPY 9.1Bn in non-cash charges, the cash operating profit came to JPY 74.1Bn, up from JPY 66Bn the year prior.

Figure 2.

Sources: ALPMF Q1 FY'23 Investor Presentation, pp. 5

The divisional highlights are as follows:

- XTANDI sales were up 700bps YoY to JPY 174.1Bn. Critically, the bulk of this stemmed from outside the U.S. Looking at XTANDI's profit margins, ~50% of the sales revenue is allocated as co-promotion fees to Pfizer in the U.S. Ex-u.s., royalties range from 10%—20%, increasing proportionally increasing with sales growth.

- PADCEV, with global sales came to JPY 15.2Bn, noteworthy growth of 44% YoY. Unlike the former segment, growth was underscored by robust performance in the U.S.

- XOSPATA and VEOZAH sales were up 250bps and 60bps YoY respectively.

Moving down the P&L, it pulled the Q1 sales to 81.8% gross, a decompression of 450bps YoY and it clipped Q1 earnings of JPY 28.88 per share.

Figure 3.

Sources: ALPMF Q1 FY'23 Investor Presentation, pp. 6

2. Uses of capital and economic value

In July this year, ALPMF successfully completed the acquisition of Iveric bio (ISEE). The strategic acquisition was made to augment its operational capacity within the field of ophthalmology. It was first articulated in April, and there were talks that Bayer (BAYZF) and Amgen (AMGN) also looked at ISEE prior to ALMPF put up its bid.

Figure 4.

Sources: ALPMF Q1 FY'23 Investor Presentation, pg. 14

The critical facts of the deal are as follows:

- It bought ISEE on a valuation of $5.9 Bn, otherwise $40 per share, a 22% premium over ISEE's closing stock price on the day the deal was announced. This was above the average of comparable pharmaceutical M&A's completed in 2023 [Figure 4], excluding Pfizer's ( PFE ) purchase of Seagen ( SGEN ) of $43Bn. The acquisition was structured via funds obtained through a syndicate of bank loans and the issuance of commercial paper, totalling JPY 800Bn, and existing reserves of cash. For its efforts, it bought $4.42 in equity value per share and total assets of $666.8mm (ISEE's numbers as of FY'22).

- The strategic significance of this acquisition is worth paying attention too in my estimation. For one, it positions ALMPF to extend its operational purview into the ophthalmology market, a sector with strong growth potential. Estimates have the global ophthalmology market valued at $51.5Bn, and to grow at 6.5% per year into FY'30 reaching $84.6Bn by that time. We will have to wait until the subsequent quarter's earnings to decipher the exact value-add.

Figure 5.

Sources: BIG Insights, Bloomberg Finance

In addition, the firm continues to recycle capital to shareholders by way of dividends, allocating $0.26/share last quarter (this is in USD). It has grown dividends almost every year since 2005. You're looking at ~$0.52/share (in USD) for the yearend. Management forecasts don't rule out a potential growth to $0.69/share by FY'25 (in USD).

Figure 5.

Sources: ALPMF Q1 FY'23 Investor Presentation, pp. 26

{kind=link}

The economic value created by the firm since 2020 is listed below. I'll be talking in USD terms here, and will use a '$' sign to make the clear distinction from JPY. Looking at the details, ALPMF earned $1.40/share in earnings after-tax on $6.70/share of capital at risk, earning ~21% return on capital deployed in the business (TTM values). The company regularly produces these kinds of economic characteristics as you'll see in Figure 6.

Most impressively, the economic earnings produced off the $12Bn in capital hovers at ~1.4–2.5x reported earnings on average. For example—taking a 12% hurdle rate as the long-term market return on capital—in its Q1 FY'23, ALPMF produced $1.05Bn in economic profit ((0.21–0.12)x12,064 = $1,055) versus $741mm reported, a 1.4x spread. Critically, it spins off ~$4–$7Bn in cash flow to its owners each period (using TTM values and including dividends). Moreover, it has pared back operating assets by ~$3Bn and thus can redistribute this cash back into the business or return it to shareholders. The "implied market value" ledger is relevant to the valuation discussion later.

Figure 6.

Sources: BIG Insights, Company reports

{kind=link}

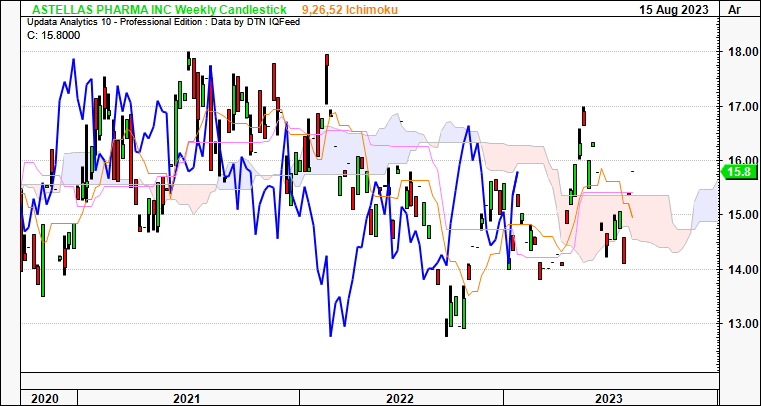

The technical take

Based on the long-term trend analysis seen in Figure 7, the stock still has some work to do in order to be firmly bullish in my view. The price line is trading into the cloud and the lagging line (in blue) has yet to nudge through the cloud's base. A move to the $16-$17 mark is required by December in order to push to this level and suggest traders are positioned bullishly.

Figure 7.

{kind=link}

We also have wide breadth in the point and figure studies shown below, with targets ranging to from $13–$23. The breadth in price objectives reduces the confidence on a specific band and thus supports a neutral view. This is exacerbated by the price action moving into congestion, backing and filling across the page.

Figure 8.

Data: Updata

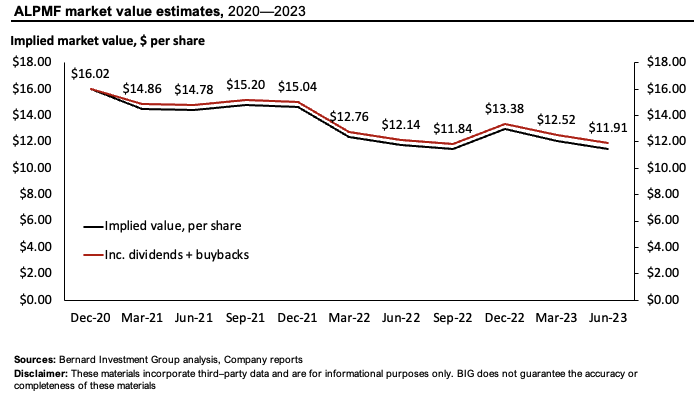

Valuation and conclusion

The stock sells at 38x trailing earnings and 10x forward EBITDA, and has produced ~$2.50 in market value for every $1 in net asset value as I write. ALPMF has superb economic characteristics, producing high profits off its capital base and demonstrating earnings power for the future. The issue in the valuation calculus is the amount of cash it is recycling into new opportunities at these rates of return. The ISEE purchase is a c.$6Bn outlay that we will have to wait until the remainder of the year to get more information on regarding integration, earnings accretion and so forth. But the point I see (no pun intended) is that the ability to deploy additional capital into growth initiatives (outside of acquisitions) has diminished over the testing period shown here today.

This creates an interesting dichotomy. On the one hand, it requires less cash tied up in asset values to grow the business. On the other, there's been no earnings growth due to this (note earnings here are defined as net operating profit after tax). I look to a firm's ability to create value as the function of its returns on capital multiplied by the amount it reinvests at these rates. If the reinvestment rate is tightening, so too, would be the growth in intrinsic value.

As a result, based on this calculus, the model spits out a fair value of ~$11.90/share, a shade off the current market value. In this vein, I am sitting neutral on the company for now, but am paying extremely close attention to the ISEE potential going forward. This could be a large upside risk to the valuation—but I've not got the economic factors to go by on this.

Figure 9.

{kind=link}

In short, I've got ALPMF rated as a hold based on valuation terms at the moment. The firm comes with superb economic characteristics but the potential headwind is the amount it can redeploy back into the business in order to grow its intrinsic value. It is returning cash to shareholders at an increasing rate, but I'd like to see evidence of surplus capital relayed back into growth initiatives. The key upside risk is the ISEE acquisition, but we'll need more time to extrapolate the potential value there. Management are tight-lipped on this at the moment, but subsequent quarters going forward will be revealing. Nevertheless, I'm watching the company very closely, and would urge my readers to do the same. Net-net, reiterate hold.

For further details see:

Astellas: Earnings Power, Asset Factors Attractive, Reiterate Hold On Valuation