AMGDF - Aston Martin: A Lot Still To Prove

2023-06-06 21:39:12 ET

Summary

- Luxury carmaker Aston Martin's sales have improved, but the company remains heavily indebted and consistently loss-making.

- Strategic shareholders, including Mercedes-Benz, Geely, and Saudi Arabia's Public Investment Fund, have increased their stakes in the company.

- With a history of heavy shareholder dilution and losses, I have no plans to invest.

Luxury carmaker Aston Martin ( OTCPK:AMGDF ) has had a short but uninspiring life as a listed company. Still, its shares have been performing better lately. They are up 1% over one year, but between November and March they more than tripled.

I last covered Aston Martin last July in Aston Martin: Beware Of The Crocodiles , rating it “hold”. That was my second piece with that rating, after a string of “sell” ratings.

Although some key business trends are improving, there is a lot of work still to be done at the indebted, lossmaking company.

Strategic Shareholders

For me perhaps the most interesting development at Aston Martin over the past year has been the growth of key shareholders. Mercedes-Benz ( OTCPK:MBGAF ) and Geely ( OTCPK:GELYF ) both now hold sizeable positions. Geely now holds around 17% of the company , making it the second largest shareholder after executive chairman Lawrence Stroll's Yew Tree consortium, which holds 21%.

Another interesting investor is Saudi Arabia’s sovereign wealth fund, the Public Investment Fund. As of the end of May, it held around 18% of voting rights, meaning that as the Geely stake beds in, it will be close to Geely in terms of ownership.

These are the big boys, and they know what they are doing. Mercedes’ interest may be in selling components as much as making a financial return, but it presumably has also considered the long-term potential for a stronger commercial tie-up with the prestigious luxury marque. For Geely, I see the chance of a larger long-term involvement as a distinct possibility, based on its involvement in other marques.

As for the Saudis, I’m less clear. Financially, Aston Martin has been a disaster for shareholders. There has been massive dilution and the shares are down 94% since their 2018 listing. Is it a vanity investment or do the Saudis think the worst is over financially for Aston Martin?

Financial Performance

I would say that the financial performance at Aston Martin remains a mixed bag. The soaring share price at the end of last year and start of this reflected investor optimism as the company completed a £654m equity raise and declared itself on track to achieve its medium-term targets.

However, the performance remains unenviable in some ways. The big achievement has been volume growth (9% year-on-year in the latest quarter) and, especially, revenue growth ahead of volume growth thanks to pricing moves and product sales mix. In the first quarter, indeed, that 9% volume growth was accompanied by 27% revenue growth.

The issue is that the company is still bleeding red ink.

{kind=link}

The picture may be getting better over time, but it remains unattractive.

Balance Sheet

On top of that, although the balance sheet improved over the prior year (which meant further shareholder dilution, Aston Martin remains heavily indebted. Its next debt at the end of the first quarter of £868m, is equivalent to 45% of market capitalisation. Servicing debt is expected to have a cash cost of £120m in the current year.

At the end of March, the company had cash of £408m. Free cash outflows in the first quarter were £118m. Since that date, the company has been set to receive approximately £95m in cash from Geely buying newly issued shares.

For now, then, that seems to be the plan: grow revenues, pay down debt, issue yet more shares if necessary (based on what has gone before) and get to some sort of breakeven. The company says it “remain(s) on our way to achieving our target of c.10,000 wholesales” although that has now been decoupled from the 2024/25 date previously targeted. That looked unrealistic to me given the sales run rate and I do not think it affects the investment case beyond raising more doubt about how reliable/realistic management forecasts are. Aston Martin reckons it remains on-track to hit its financial targets of c. £2bn revenue and c. £500m of adjusted EBITDA in 2024/25. Revenue last year was £1.3bn, up 26%, and first quarter revenue growth this year came in at 26%, so that revenue target looks realistic albeit challenging.

Investability

Separately from the business quality or valuation, one concern I would have about investing in Aston Martin is the role of major shareholders. Four key large shareholders collectively control a majority stake in the company.

The relentless dilution of shareholders since listing, not to mention that 94% fall in share price, makes it hard to perceive small shareholders as a big priority for the firm’s board.

Optimistic Valuation

Even after that massive shareholder destruction, I think the current valuation for consistently lossmaking Aston Martin looks difficult to justify.

On the plus side, sales revenues and volumes are rising, the brand has great prestige, it has a deep-pocketed customer base and a move into SUVs has helped expand its appeal.

On the downside, the net debt remains substantial, the business is lossmaking and continues to burn cash at a significant rate and the economics of what a successful achievement of its medium-term financial targets remains to be seen. The EBITDA target is one thing (as yet unmet), but interest alone is a real and substantial cost for Aston Martin.

Accepting the current valuation as reasonable, let alone a bargain, involves believing that the company will break into the black and make, say, £100m or more in annual profit (which would give a P/E in the 20s, viable for a luxury brand although in my view challenging to justify for one without a consistent profit history).

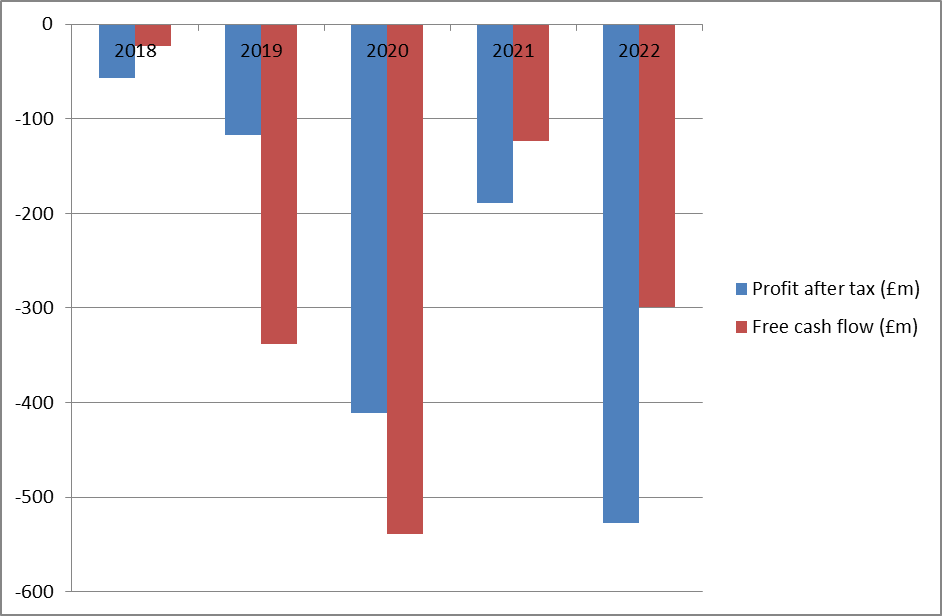

Compare that to the past five years of performance at the business, which changed top management in 2020 and has since cycled through multiple chief executives alongside the executive chairman.

Chart compiled by author using data from company filings

{kind=link}

Despite improving revenue and volume trends, there is a lot for the firm still to prove even to justify its current valuation let alone a higher one. I maintain a “hold” rating not a “sell” because the momentum is at least in the right direction. But I have no plans to buy into Aston Martin.

For further details see:

Aston Martin: A Lot Still To Prove