AMGDF - Aston Martin: Show Me The Story

2023-06-20 10:16:17 ET

Summary

- Geely increased its equity stake to 17%.

- Aston Martin is still in negative territory with higher working capital requirements and CAPEX.

- The company confirmed the yearly guidance; however, 2023 could be a pivotal year to rebuild investors' trust. We continue with our “wait and see” approach for now.

In our initiation of coverage called " Aston Martin Is A No Go ", we emphasized the latest development on the company's capital structure, providing an update on the principal shareholders. Last month, Geely Holdings decided to invest £234 million in the British automaker. During that day, Aston Martin ([[AMGDF]], [[ARGGY]]) stock closed with a 12.5% gain and rose to £2.60 per share on the heels of the news that the Chinese group will buy 42 million Aston Martin shares from the Yew Tree Consortium investment group of Lawrence Stroll, the current British automaker executive chairman. Geely can also purchase an additional tranche of 28 million stocks at £3.35 per share. Aston Martin will receive £95 million in cash from the capital raise. With this transaction (Fig 2), the Chinese group will have an equity stake of 17% , making Aston Martin's third largest shareholder. Yew Tree Consortium will still be the largest shareholder with a 21% stake, followed in second place by the Public Investment Fund of Saudi Arabia, owner of 16.7% of the capital of the famous 007 car manufacturer. As already mentioned, there is still Mercedes-Benz AG which is a strategic shareholder. Here at the Lab, we view Geely's investment as further validation of Aston Martin's progress and mid-term earnings potential, given that it comes from another insider. However, we should also report that Geely has tried to acquire Aston Martin in the past, with bids in 2020 and 2022. If we combined the major shareholders (Yew Tree Consortium, Public Investment Fund, Geely, Invesco, and Mercedes), we would arrive at ownership of almost 75%, and this offers risk mitigation and further protects the company's capital structure in our view.

Fig. 1

{kind=link}

Mare Evidence Lab's previous analysis

Aston Martin Main Shareholders (Market Screener)

Fig 2

Before analyzing the latest company's development, it is nice to recap Lawrence Stroll's words . " There is an expression, I didn't believe it, but we're experiencing it: race on Sunday, sell on Monday ." Thanks to Formula 1 results and the safety car partnership, Aston Martin's boss explained an $80 million top-line increase thanks to the Vantage F1 car edition (car below). In detail, he said that Aston Martin recorded sales volume between 300 and 400 units. Even if it sounds like a small number, it is essential for the company. Indeed, cross-checking the Vantage F1 edition price is in the £159,500 and $200,000 range. As a reminder, in 2022, Aston Martin sold about 6,400 units (2023 aims for 7,000 units, so the Vantage F1 car could represent 5% of the total deliveries).

Vantage F1 car edition (Aston Martin Q1 results presentation)

{kind=link}

CMD's Next Potential Catalyst

Aston Martin unveiled its next generation of sport cars (the new DB12) on the 24th of May. Industrial production will start in Q2, with deliveries in Q3. According to the latest news , the company will give additional details of the new cars at its capital markets day (CMD) scheduled for the 27th of June. With the launch of AM's next-generation front engines cars, such as the new Vantage and DBS (with both Volante and Coupe versions for each model), Aston Martin will offer unique style, a new engine (plug-in hybrids and BEV), and new interior architecture. This should support the company's more than 40% gross margin target. Here at the Lab, we believe that AM CMD will provide additional color on its future model line, providing essential updates to 2025 guidance (and beyond). This is key to better understanding the company's total earnings potential (at scale).

Changes in Estimates

The most recent quarterly figure shows that the company continues to record strong demand across its product portfolio. This was supported by the GT/Sports cars sold out for the current year, DBX solid order book, with the DBX707 representing more than 70% of total orders. In January, Aston Martin celebrated its 110th anniversary, and for that occasion, the DBS 770 Ultimate was unveiled and is arguably the most potent Aston Martin car ever built. All 499 units were sold out, and car deliveries are expected to begin in Q3. The company delivered broadly in-line Q1 numbers, with slightly lower-than-feared cash outflow. In addition, the 2023 guidance was left unchanged (Fig 4).

We should also recall that Aston Martin pricing should support the company's average selling pricing increases into 2024 (AVP moved to £180k from £151k). In addition, GT and sports model volume were already sold and booked a 95% of the AM's industrial capacity.

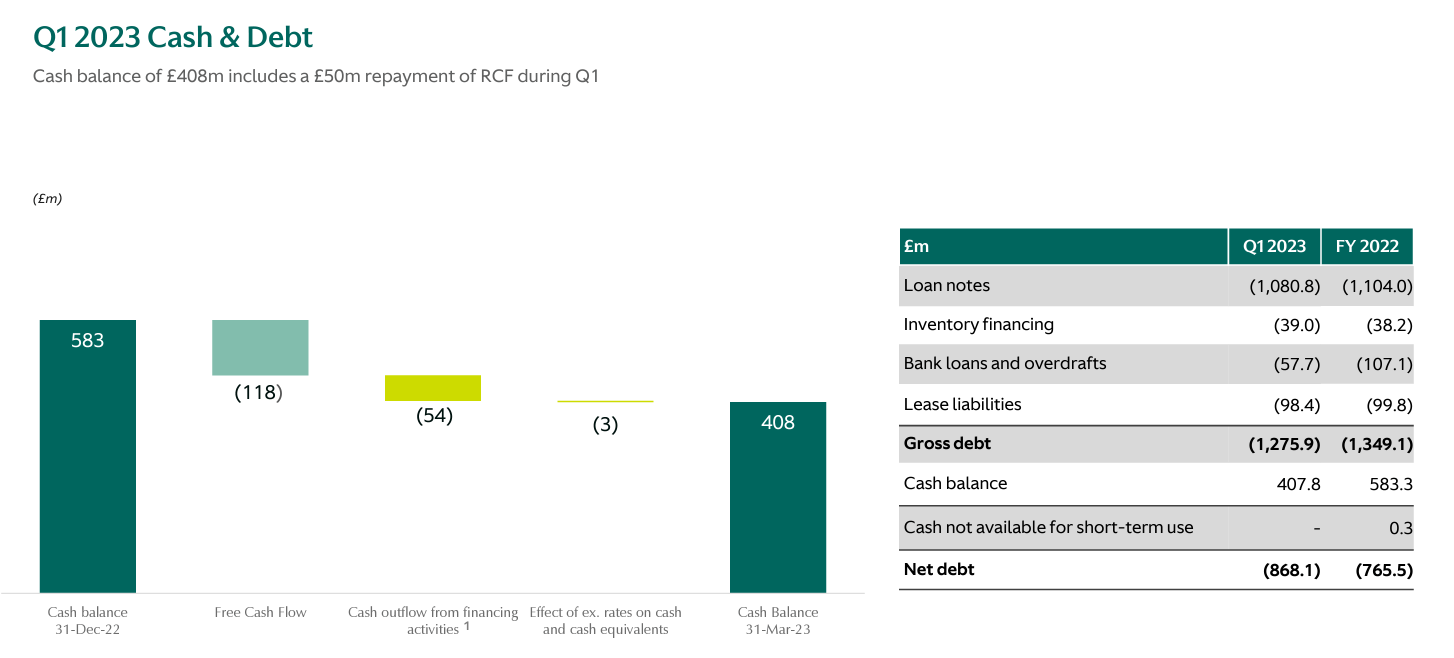

Looking at the negative notes, the company increased its operating expenses with higher marketing and brand activities costs. D&A increased due to the Aston Martin Valkyrie program and higher amortization of capitalized costs. FCF was negative for £118 million (Q1 2022 was at £25 million outflow). This includes 1) higher WC requirements due to inventories and 2) higher CAPEX for the upcoming vehicle launches and new model development (we should also add the Aston Martin new plans for electrification). Therefore, cash and cash equivalents were at £408 million from £583 million in the 2022 year-end, and net debt reached £868 million from £766 million on a quarterly basis (Fig 3). This is an ongoing key concern in our estimates. However, FCF was better than anticipated, with Wall Street consensus at a minus £135/150 million. Looking beyond the numbers, Aston Martin built inventories to smooth production (for the upcoming quarters) and the new models' ramp-up. Based on these numbers, we are slightly increasing Aston Martin's EPS and forecasting a -0.16, 0.08, and 0.16 for 2023, 2024, and 2025 respectively.

{kind=link}

Aston Martin's debt evolution

Fig 3

Conclusion and Valuation

Here at the Lab, we acknowledge the company's solid commercial progress and a plausible sustainable earning trajectory. The excellent Formula 1 starting season provides brand visibility and product consideration among Aston Martin fans. There was a 50% increase in web access with more than a 30% uplift in car configuration . This provides a " wait and see " stance for now. This current year could be a pivotal year to rebuild investors' trust. Transparent guidance has also de-risked Aston Martin's investment case. On the other hand, Aston Martin is trading at 4.5x its 2024 adjusted EBITDA projection. As a comparable basis, Dr. Ing. h.c. F. Porsche AG ( OTCPK:DRPRF , OTCPK:DRPRY ) is trading at 5.5x on 2024 EBITDA with a return on sales at 18.2% and a core operating profit of €1.4 billion in just a quarter. For this reason, we confirm our neutral rating of £300p and suggest that our readers have a look at Volkswagen: " The Most Discounted Auto Stock " . Risk to our neutral valuation includes supply-chain constraint due to Brexit, negative FX development, higher interest rates, weaker pricing power, and lower volumes.

Aston Martin guidance

Fig 4

For further details see:

Aston Martin: Show Me The Story