ARGGY - Aston Martin: Still Neutral

2024-01-04 17:08:35 ET

Summary

- We are lowering our estimates due to higher D&A and interest expense.

- The company's guidance has been revised due to complications with the DB12 production.

- Here at the Lab, we like the luxury OEM segment but are still cautious about Aston Martin's target price. Our neutral rating is then confirmed.

Our readers know that we deeply admire Ferrari (RACE), and on Seeking Alpha, our supporting buy rating is widely shared. Even in our recent analysis, we reported how Ferrari is an unusual car company that combines auto and luxury virtues. With a unique order book that now extends until late 2025, the company faces the lowest volatility among OEMs, and arguably, this is well reflected in its valuation. However, we believe the right momentum is coming for Aston Martin ( AMGDF , ARGGY ), and within our coverage, post-Q3 results, we also increased our rating of Dr. Ing. h.c. F. Porsche AG or P911. Here at the Lab, we view the auto luxury segment positively and see Aston Martin on a path for a brighter future. Despite that, we still see a lot of uncertainty in the short-medium time horizon. For the above reason, we reiterated our neutral rating on a 12-month visible period; however, given the recent stock price decline, our valuation is skewed to the upside. As a reminder, in our initiation of coverage, we started with a no-go investment , and in June 2023, we reported a " wait and see " approach with a publication called Show Me the Story . Looking back, this was a good call. Indeed, Aston Martin's share price is down by more than 30% since then.

{kind=link}

Why are we still neutral?

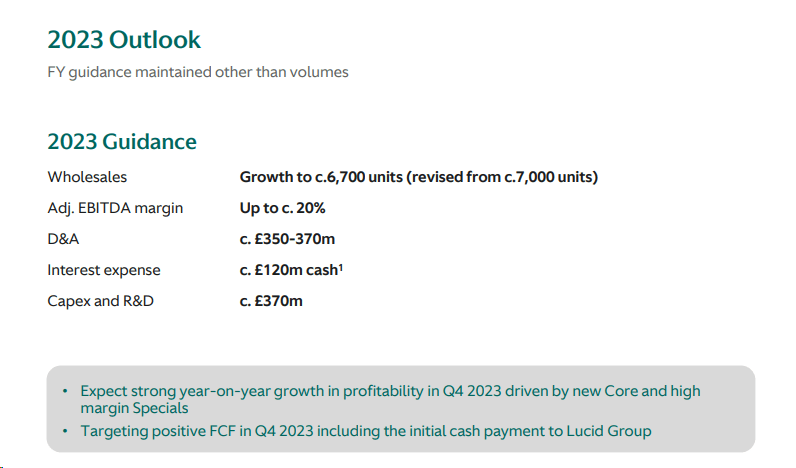

During the Q3 results, the company lowered its 2023 volume guidance from approximately 7,000 to 6,700 units. This revision was due to a delay in the ramp-up production of the DB12. Looking at the press release, the company explained how production " was temporarily affected as supplier readiness and integration of the new EE platform that supports the fully redeveloped infotainment system was delayed ," confirming that these issues were resolved. Therefore, software integration issues and supplier readiness will cause a shortfall in production by year-end. Having said that, the company confirmed its fiscal year-end guidance with an adjusted EBITDA margin of 20%. Reverse engineering the 2023 company's estimates with lower units and a decrease in top-line sales; this would imply an EBITDA margin north of 25% in Q4. In addition, Aston Martin expects to turn free cash flow positive in the last quarter. Here at the Lab, we are not positive, and given AML's negative track record, we are concerned about the Q4 financials.

Our negative view is supported by a notch weaker than expected Q3 performance. The company missed estimates in all P&L lines. Despite that, with lower units than anticipated (1,444) in the quarter, Aston Martin delivered £362.1 million in sales and an EBITDA margin of 13.9%. In our estimates, on a full-year basis, we forecast sales and adjusted EBITDA at £1.58 billion and £277 million. Going down to the P&L analysis and keeping the new 6.7k units target, our core operating profit and earnings per share move slightly down. This is due to higher D&A and increased net financial expenses. In our 2023 numbers, we arrived at a net loss of £135 million. The interest rate is based on £735 million indebtedness by year-end.

Having participated in the Q3 analyst call, the company anticipated re-stocking from dealers in Q4. If we consider this development, it would probably result in higher inventory at year-end, and this might impact AML's 2024 revenue recovery. Here at the Lab, we view the upcoming Vantage and the new DB12 positively, but we are rather pessimistic about the DBX. On this car, AML projections are set at 3,000 unit sales per year. Therefore, our team is projecting an adjusted EBITDA forecast for 2024 below Wall Street consensus. In number, we anticipate sales and adjusted EBITDA at £1.85 billion and £390 million, respectively. On a positive note, the new DB12 reception is very positive, and the CEO seems confident that 2024 production will be fully booked by year-end.

{kind=link}

Source: Aston Martin Q3 results presentation

Conclusion and Valuation

The current fiscal year result is heavily backed by earnings perspective and higher volumes. This increases AML's importance on the possibility of missing guidance (again). Having said that, we lowered our target price from GBp300 to GBp250 on the recent auto peer group de-rating and our lower earnings estimates. We also believe the AML stock price significantly de-rated because the company still has high leverage, and free cash flow will likely turn positive starting from 2025. Given the high interest rate environment, Wall Street is punishing the premium OEM. Despite that, our upside/downside risks are skewed in the positive area. Although our forecast is (again) below consensus for 2025, we believe that potential share purchases by Geely will likely limit AML's stock price decline. Here at the Lab, we believe that a re-rating would happen if the company exceeded its internal financial outlook, which our team is not anticipating.

For further details see:

Aston Martin: Still Neutral