ARGGY - Aston Martin: Success With Formula 1 Not So Much With Finances

2023-03-13 11:21:39 ET

Summary

- Aston Martin is a legendary high-end car manufacturer, famously driven by James Bond.

- Lawrence Stroll is revolutionizing the brand through the re-branding of his Formula 1 team.

- The growth in Formula 1 will drive significant interest in Aston Martin, especially as the team becomes more successful.

- Economic conditions should pose short-term headwinds but the company has remained resilient so far.

- The biggest issue with the company is that we see no route to profitability, due to the massive S&A expenses.

Investment thesis

Things at Aston Martin Lagonda ( AMGDF , ARGGY , AMLRF ) are looking up commercially, with the luxury vehicle segment as a whole showing impressive growth. This represents an opportunity for AM to grow its deliveries and transition toward profitability. Our objective is to assess if this is possible and how current market conditions are impacting the business in the short term.

Company description

Aston Martin is a company that creates high-end sports cars, marketed and sold globally under the Aston Martin and Lagonda brand names. The company has a prestigious history of producing high-end cars, servicing many wealthy clients over the decades including Queen Elizabeth II and James Bond.

Share price

Investors in Aston Martin have not had a good time since the company was listed, with the share price heading in one direction at a rapid rate. We followed the initial IPO several years ago and it must be said that the company did not deserve the valuation it received, with the following years being an inevitability. The reason for the decline is the company's inability to produce consistent profits, at a time when many luxury businesses are going from strength to strength.

Lawrence Stroll

Lawrence Stroll, a Canadian Billionaire, and race car fanatic purchased the F1 team Force India in 2018 . This was before Formula 1's recent boom in popularity, driven by the hit Netflix series, Drive to Survive. Since then, Lawrence Stroll has purchased a controlling stake in AM , now owning 28.4% ( Source: Tikr Terminal ) and instilling himself as Chairman. Since then, Mr. Stroll has made impressive commercial moves in an attempt to revitalize AM. We will discuss the key points in further detail below.

Winning in Formula 1

Mr. Stroll has re-branded the Formula 1 team to AM. Formula 1 is the pinnacle of motorsport but has historically been a sport for the rich when helmed by Bernie Ecclestone. Since Liberty Global's takeover, they have opened the sport to the masses with a big marketing push and changes to rules. This has rapidly increased the interest in the sport and by virtue, the value of the teams. Mr. Stroll has invested heavily in Formula 1, focusing on bringing in the best personnel to the team as a means of becoming a title challenger. Formula 1 is a highly technical sport, with the real value being the engineers as the best car will always beat the best driver in an inferior car. We are only 1 race into the 2023 season but AM looks to have built the second-best car on the grid, beating Ferrari ( RACE ), Mercedes ( MBGAF ), Renault ( RNSDF ), and McLaren. It is likely that Fernando Alonso (AM's lead driver and a top 5 of all-time F1 drivers) will win a race this season. This rapid development from being outside of the top 5 teams to being a race-challenger is driven by the recruitment of the best talent in the sport. Success in Formula 1 is imperative to the success of AM's car business as the marketing value that comes with Formula 1 dwarfs any other realistic options the company can invest in. AM has stated that >60% of new customers in 2022 were new to the brand ( Source: FY22 investor pack ). Toto Wolff, the head of Mercedes' formula 1 team, said several years ago that Formula 1 was worth several hundred million to the car business. This was before the recent increased interest in the sport. For context, AM's entire S&A expenditure is £570M ( Source: Tikr Terminal ).

Winning on the road

Not only has Mr. Stroll's investment been on the F1 front but also pushing for developments on the vehicle side. AM has received a lot of positive press for the release of its Valkyrie car , which was dubbed the $3M "Formula 1" road car. This was designed in conjunction with Adrien Newey, who is arguably the greater race car designer in history (Also the previous mentor to Dan Fallows, the man who designed AM's incredible 2023 car. This is not a coincidence). The Valkyrie isn't expected to drive growth but instead represents a proof-of-capabilities and marketing exercise. Our view is that this has been highly successful, with many famous individuals advertising that they have taken delivery of the car.

Long-term, we are very bullish on the commercial side of AM. Mr. Stroll is a car fanatic who is looking to truly revitalize AM rather than achieve short-term success. To us, he is similar to a founder/family-led owner where the decision-making is also focused on commercials first, with the understanding that financial success will follow. With a Formula 1 team to support the car business, we can see consistent growth achieved.

Economic conditions

We are currently experiencing a decline in discretionary income as inflation rapidly deteriorates real incomes. Supply-side issues and post-pandemic disruptions have contributed to this, with interest rates showing weak effectiveness in bringing it back under control. Interest rates have compounded the issue as the cost of borrowing has rapidly risen. More broadly, this has contributed to a bear market, reducing the wealth of many individuals. This has led to a softening of demand across many industries, with the luxury segment expected to be disproportionately impacted. This is clearly not a good thing for AM, whose average selling price is more than £200k. Unsurprisingly, individuals will become more defensive, reducing excess purchases while they consider how the economy will develop.

What is unusual is that the reality does not necessarily align with the theory. AM has seen its number of deliveries increase from 6,178 in FY21 to 6,412 in FY22, a 4% increase. Further, c.80% of the current range GT/Sports are sold out for 2023 ahead of upcoming launches, with the DBX order book full until Q3-23 ( Source: FY22 investor pack ). This represents the general resilience of the luxury car segment in general, with Ferrari's much anticipated Purosangue already having a 2-year waitlist .

The reason for this we believe is that this is not a "normal" downturn. Demand in many industries has remained surprisingly robust while others have followed the expected route. One of the reasons the vehicle industry has likely gone against the grain is due to the delays in shipping cars due to the industry-wide chip shortages, which has likely led to deferred demand being slowly unwound as deliveries are made.

Looking ahead, our economic forecast would be more of the same, as inflation remains stubborn in its decline. This will likely extend to much of 2023, with early 2024 likely being when rates can begin to decline. AM is forecasting deliveries to increase to 7000, which represents a 9.2% increase ( Source: FY22 investor pack ). Our macro-mindset says this looks impossible but with a large number of deliveries locked in and industry resilience, it is difficult to argue against growth in the year.

Financials

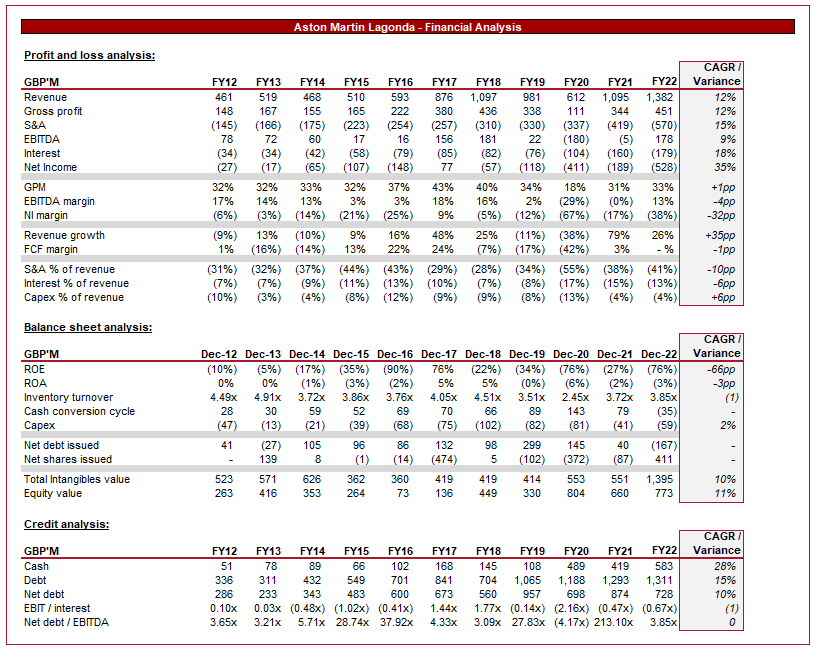

Aston Martin's financials (Tikr Terminal)

{kind=link}

Presented above is AM's financial performance for the last decade.

Revenue has grown at a CAGR of 12%, driven by a consistent increase in vehicle deliveries and an uptick in average selling prices. Excluding FY20 due to the pandemic, AM has achieved a decline in sales 3 times, with growth above 10% 6 times.

The company has struggled to achieve production scale economies, with GPM remaining flat across the historical period. Gains were being made before the pandemic but cost pressures following this have destroyed all gains made. Our wider research suggests cost pressures should begin to ease, which will allow a natural normalization toward the 40% level again.

Another issue the company has is its S&A expenditure. The company's overheads are a serious issue in the transition toward profitability. This expense has increased at a 15% rate which is greater than revenue. This would not necessarily be an issue if it was generating outsized returns but it is not, the marginal gain is inferior. Further, the expense represents an eyewatering 41% of revenue, giving the company no hope of profitability at these levels. The inability to generate any scale gains suggests the company does not have a cost-effective way to grow the business and/or produce cars in a profitable way.

Moving onto the balance sheet, the company does show some signs of operational improvements. Inventory turnover has improved compared to the past 3 years and AM's cash conversion cycle is now negative.

Despite these efforts, the company is still burning cash. The company has maxed out the amount of debt it can raise at reasonable levels, with its ND/EBITDA ratio at 3.85x. S&P rates AM a CCC , which is a speculative grade. This has led to equity raises, with the most recent one being supported by the Saudi PIF and being used to repay debt .

Overall, it is clear that the issues with the company are on the financial side. We cannot see AM's route to profitability due to the terrible relationship between S&A expenditure and Revenue. GPM is not fantastic by any means but at a 37%+ level, we can see profitability.

Outlook

Aston Martin forecast (TIkr Terminal)

Presented above is the Street's consensus view on AM's performance in the coming 4 years.

Revenue forecasts are weaker than historical performance, suggesting deliveries may begin to slow in the coming years. Our view is that revenue growth will need to normalize but will likely be over 3-6%. Formula 1 will drive improving marketing efficiency, with greater vehicle innovation supporting this.

On the other hand, analysts see improving margins from as early as FY23. With GPM and EBITDA-M both up to impressive levels. Our view is that these gains can be achieved but within 12 months seems optimistic.

What we do agree on is bottom-line profitability, which analysts cannot see becoming sustainably positive.

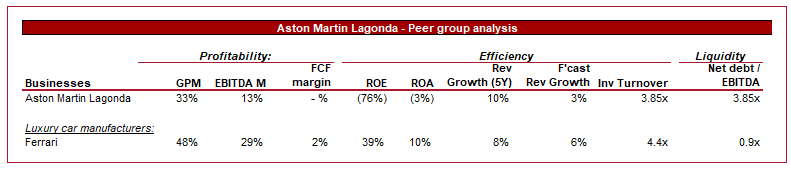

Peers

The majority of luxury car manufacturers are owned as part of a group, such as Volkswagen ( VWAGY ). From a standalone basis, Ferrari and Porsche are the most comparable although serve more as an aspirational level for AM.

As the following illustrates, the biggest issue for the business is its cost base. AM's operational deficiency stops the business from operating at a profitable level.

{kind=link}

Valuation

AM & Ferrari valuation (Tikr Terminal)

Presented above is a comparison between AM's valuation to Ferrari. We recently wrote a paper on Ferrari and considered it slightly overvalued (can be found here ). Despite this, AM is trading at half the EBITDA multiple. To an extent, this represents an opportunity, if AM is able to achieve the level of profitability Ferrari has, it could equally be valued at this level. The issue is that this is almost impossible. The question is thus, where on the spectrum AM falls? This is a potential exercise that can be undertaken but the reality is that the route to profitability still looks materially uncertain.

Final thoughts

Aston Martin is a legendary car manufacturer which will likely continue to operate (in some form) for another 100 years. From a commercial perspective, we see the possibility for the company to experience a golden age with an incredibly talented F1 team driving interest in the brand. The problem is that passion doesn't produce profits. The boring side of the business, the finances, are a complete mess. We cannot stress this enough that the step-by-step route to profitability is invisible. If this could be established, our view on the business will change very quickly. Until then, the future value to shareholders is less than nil and the company does not represent an attractive takeover option.

Thus, we rate the stock a sell.

For further details see:

Aston Martin: Success With Formula 1, Not So Much With Finances