AZNCF - AstraZeneca: Our 2023 Growth Pick

Summary

- Japan just approved three drugs against cancer and leukemia.

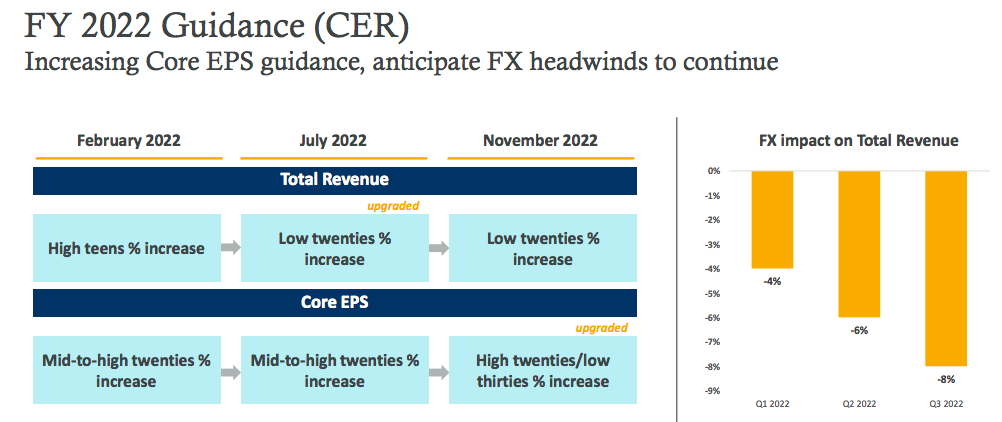

- AstraZeneca increased its 2022 guidance.

- As already mentioned, premium pipelines deserve a premium valuation. The company is confirming a positive trajectory both in its internal R&D area as well as inorganically.

Following our initiation of coverage called AstraZeneca ( AZN ) - Our Next Growth Pick , after a few months, today we are back to comment on the British-Swedish pharmaceutical giant. Since our buy rating target released in May, AstraZeneca's stock price performance is almost flat but outperformed the S&P 500 average return by almost 10%. Our buy rating was based on macro and micro reasons, the former upside was due to the inflationary environment and the fact that pharmaceutical companies have low manufacturing costs and extremely high levels of discretionary spending. The latter was supported by the latest Alexion acquisition, the company's supportive pipeline, and its continuous positive quarterly results.

Very briefly, AstraZeneca delivered solid 3Q22 numbers , with topline sales 3% ahead of Wall Street consensus estimates. In detail, the positive beat was due to higher COVID-19 turnover, and excluding COVID-19 group turnover, there was a 2% miss. The company's core operating profit was 8% ahead of consensus, and this was driven by higher external collaboration. Looking at the numbers, this result was supported by Enhertu income following the strong performance in the quarter. Going down to the P&L, the gross margin reached 79.4% with operating costs 2% higher than what we anticipated. Core R&D and SG&A will be key inputs to monitor in the future. However, thanks to the recent AstraZeneca pipeline success, here at the Lab, we positively view higher investment in the R&D area. The company's tax guidance estimate was left unchanged, and in our numbers, we foresee a 20% deduction (the range is between 18% and 22%). On the core business, key product performance was in the oncology area. There are signs of improving revenue momentum post-COVID-19, with Imfinzi and Calquence beating consensus by 5% and 8%, respectively. This positive outcome was partially offset by weaker Lynparza, but again Tagrisso's topline sales were solid.

Despite lower sales on unfavorable FX development, for the above reason, AstraZeneca now expects to increase its 2022 EPS by high twenties to low thirties % (the company's previous expectation was a mid to high twenties increase). This is well in line with Mare Evidence Lab's previous publication with results higher than market expectations.

AstraZeneca Guidance Increased (AstraZeneca Q3 Results Presentation)

{kind=link}

Aside from the financial performance, what is key to emphasize is the company's ability in discovering new drugs and getting them approved . Just today, the Japanese Ministry of Health turned the green light on three of the company's drugs: Calquence, Imfinzi, and Imjudo. The first treatment is a selective inhibitor of Bruton's tyrosine kinase and, according to recent studies, it extends patients' life, avoiding the progression of the disease compared to the more common chemo-immunotherapy. Already approved for the treatment of other diseases, the drug can now be used in adults with chronic lymphocytic leukemia (CLL), including small lymphocytic lymphoma. On the other hand, Imfinzi and Imjudo are two immunotherapies for liver tumor treatment in an advanced stage. In this case, Japan's approval is a victory for the AstraZeneca team. Japan has one of the highest rates of liver and biliary tract cancer diagnoses in the world, and lung cancer is the leading cause of cancer deaths. With Imfinzi and Imjudo, Japanese patients can be treated with new immunotherapy-based therapeutic regimens that have demonstrated significant survival benefits in three complex cancer prognoses. Calquence's introduction also represents a turning point for the country. Considered among the most common types of leukemia among adults worldwide, CLL falls into the category of rare diseases in East Asia and Japan, where there is less than one diagnosis per 100,000 people each year. Just pricing in these positive results, revenue potential could be $10 billion for the next 5-8 years.

AstraZeneca is also working on two new molecules, Capivasertib and Camizestrant, to improve progression-free survival in patients with metastatic breast cancer. This was supported by the latest demonstrated results of the CAPItello-291 and SERENA-2 studies. This research was presented at one of the most important breast cancer international congress called the San Antonio Breast Cancer Symposium.

Aside from the internal R&D, over the last months, the company announced two other acquisitions. 1) Neogene Therapeutics , a clinical-stage biotechnology company specializing in T-cell receptor (Tcr-t)-based therapies to fight cancer. The first investment tranche is set at $200 million and will be paid at transaction closing (expected in Q1 2023), and a further amount of up to $120 million will be paid based on the milestones achieved. And secondly, AstraZeneca signed a licensing deal with C4X Discovery for $402 million to develop an oral therapy for the treatment of inflammatory and respiratory diseases under the Nrf2 Activator program.

Conclusion and Valuation

2023 should be a very supportive year with positive growth led by Enhertu sales and Alexion's integration. All in all, we forecast a 9% growth at CET excluding COVID-19 revenue, and we are just a bit ahead of Wall Street average revenue estimates. Our key product growth drivers are Lynparza, Tagrisso, Farxiga, and Ultomiris. The company raised its 2022 guidance, and assuming a -7% negative FX development, we implied an EPS of 6.3, deriving and confirming a target price of £12,000p . As already mentioned, AstraZeneca's operating leverage is still expected and will drive lower SG&A costs as a percentage of sales. We know that the company is still trading at a premium valuation versus its peers, in detail, based on our forecast number, the company's 2023 P/E is 21x with a 30% premium to European pharmaceutical peers; however, premium pipelines deserve a premium valuation. Our buy rating is then confirmed and additional risks to our target price include litigation loss, sales slowdown, and pipeline failure.

For further details see:

AstraZeneca: Our 2023 Growth Pick