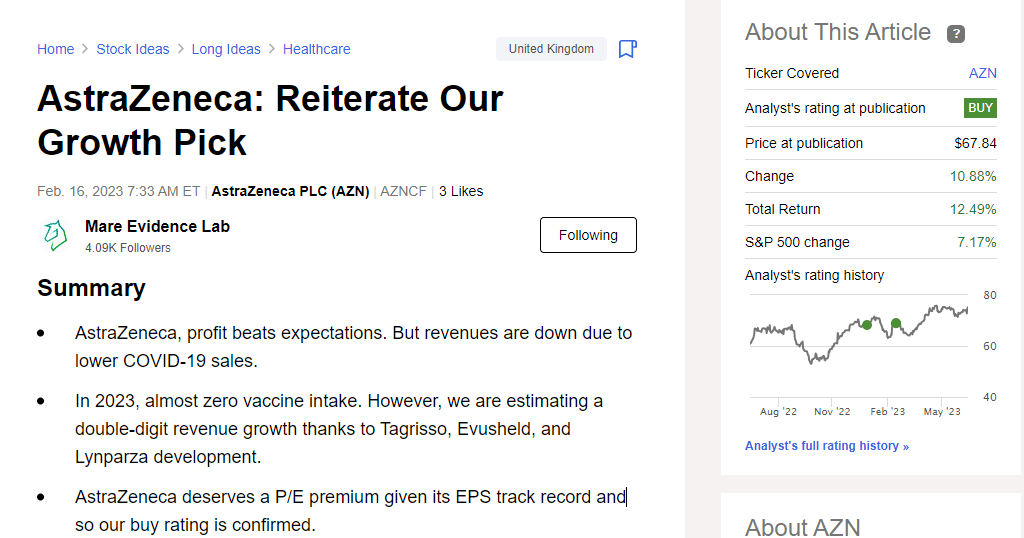

AZNCF - AstraZeneca: What's Next? (Rating Downgrade)

2023-06-20 07:27:45 ET

Summary

- AstraZeneca is considering spinning off its China operations and listing a separate division in Hong Kong or Shanghai. This move could protect the company's Chinese sales.

- In 2022, China accounted for 13% of AstraZeneca's total sales, making it an attractive market for pharmaceutical companies.

- We applied minor changes in our estimates. The company almost reached our target price. Therefore, our rating is now an equal-weight valuation.

Today, we are back to analyzing AstraZeneca ( AZN ). This year, we published a detailed note commenting on the Fiscal Year 2022 results, and since then, the company has been up by 12.49% (including the dividend payment). Our buy case recap was supported by a robust pipeline and a high level of discretionary spending combined with low manufacturing costs. In Q1, the company delivered a solid turnover (3% above Wall Street estimates); more importantly, AstraZeneca had a core operating profit beat of 10%. The giant pharmaceutical outperformance thanks to Pulmicort, Imfinzi, Farxiga, and Enhertu, which offset some weaknesses of Calquence and Lynparza. Lower COGS mainly drove the higher profitability; however, the CEO cautioned that this would ease over 2023, confirming the yearly outlook.

{kind=link}

Following the Q1 results and the latest news on the company's pipeline (ASCO June 2023), we made little changes in our internal estimates.

Changes in our Estimates

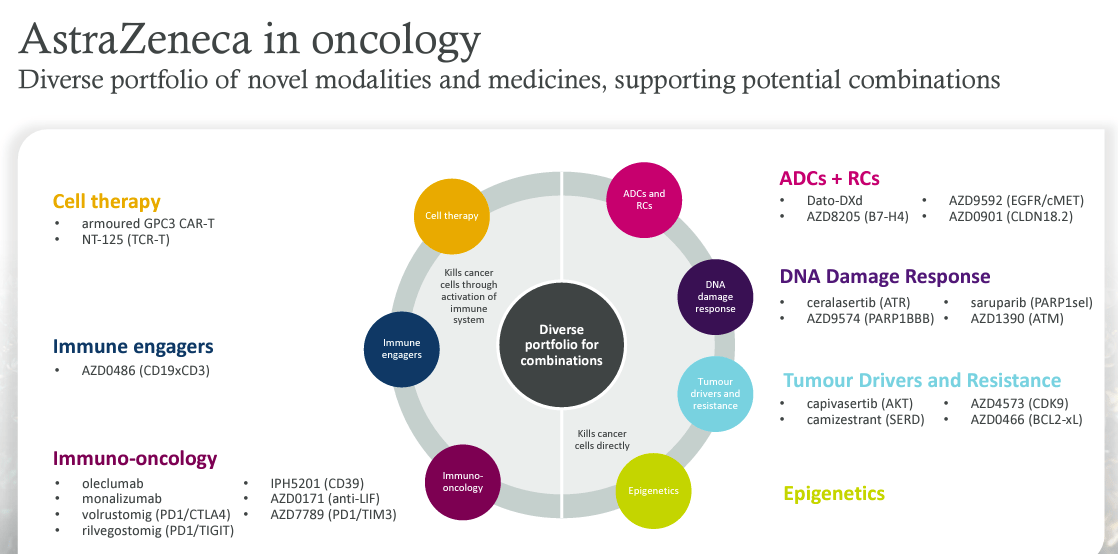

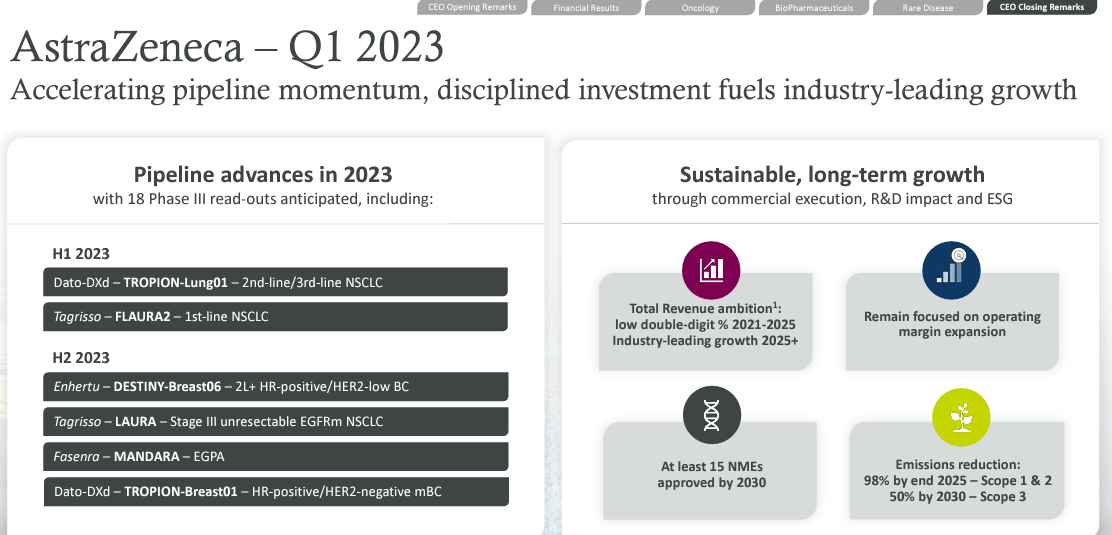

- Firstly, we are increasing expectations for Imfinzi/Imjudo thanks to better results than previously anticipated. In addition, we should report the approved new drugs Topaz, Himalaya, and Poseidon, which are already supporting AstraZeneca sales. Regarding Himalaya and Poseidon, the company is seeking approval in the EU (Fig 4). Astra's R&D engine continues to deliver, especially in small-cell lung cancer (Fig 1);

- As already mentioned, Q1 gross margin was significantly better than anticipated. In line with CEO's words, here at the Lab, we assume higher cost inflation over the year, continuing to be above consensus in R&D ramp-up expense. Indeed, AstraZeneca continues to expand its P3 trial. For this reason, we are lowering our core operating profit by 1% until 2028;

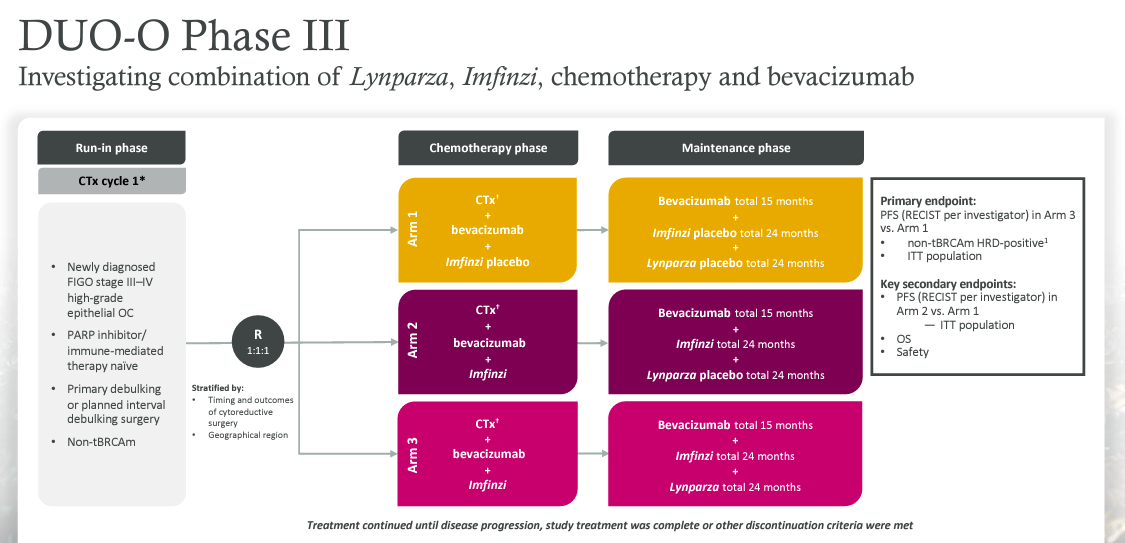

- We removed ALX1840 from our model on the pipeline due to negative regulatory feedback. On the top-line sales, we note some pressure on Calquence (rebates) and Lynparza (prostate all-comers) - Fig 3. In detail, with Lynparza, we are lowering our US sales expectations given the newcomers' competition. As a consequence, in our model, AstraZeneca will no longer reach $4.5 billion in sales but only $3 billion (in 2026);

- On the other hand, thanks to a better assumption in breast cancer, we are increasing peak sales for Capivasertib and Camizestrant;

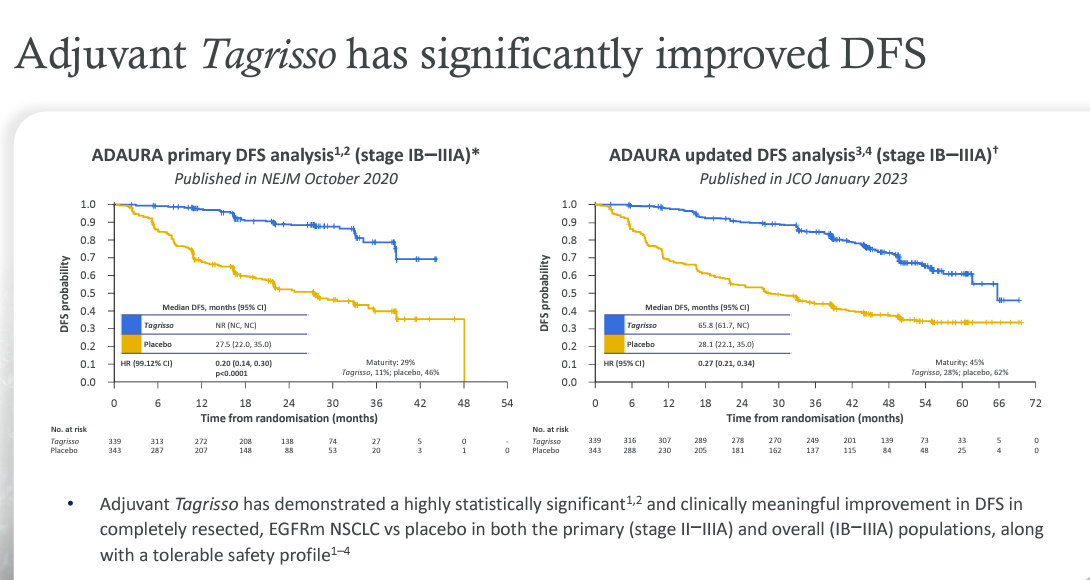

- We still see an upside for Tagrisso here at the Lab (Fig 2). We assume patients treated with FLAURA-2 will need an additional 6 months of treatment. This is due to the latest data supporting a higher probability of success. Therefore, we are increasing sales by 25% regularly.

{kind=link}

Source: ASCO 2023

{kind=link}

{kind=link}

Fig 3

Topaz, Himalaya, and Poseidon dev (ASCO 2023 Meet AZN Management)

Fig 4

A potential upside (not priced in)

According to the FT , the Anglo-Swedish pharmaceutical giant is considering spinning off its operations in China and listing a separate division in Hong Kong. Here at the Lab, we are not usually commenting on speculation; however, we are making an exception this time. First, looking at the source, the Financial Times specified that the spin-off might not even occur. However, this is a possibility. In detail, in 2022, China accounted for 13% of AstraZeneca's total sales. The Chinese market is beautiful for pharmaceutical companies because the nation has an aging population, and the government is speeding up regulating innovative medicines.

In recent years, AstraZeneca launched several local partnerships in the region to help foster innovation and even collaboration for an herbal treatment. Last year, it announced plans to build an inhaled drug manufacturing site in Qingdao to support its respiratory product portfolio. Listing the separate division in Hong Kong and/or Shanghai may protect the company from China's moves to crack down on foreign companies. It would also offer an independent source of capital and could reassure investors that the company is less exposed to China-related risk. Not to mention that an IPO could help AstraZeneca court Beijing's support for drug innovation and gain faster approvals for therapies developed in the country. It wouldn't be the first time the pharmaceutical group has sought separate funding for its operations in China. In 2017, AstraZeneca created an R&D joint venture with a Chinese company. The joint venture, Dizal Pharmaceutical, was listed in Shanghai two years ago.

Conclusion and Valuation

Here at the Lab, we consider AstraZeneca a clear leader in pharma innovation, and Wall Street's near-term expectations are also high. In our model, we are estimating $10 billion in incremental sales in the next 4 years. This is supported by success across the company's pipeline and the Enhertu/Dato-DXd ADC partnerships combined. Despite that, we believe that investor consensus is unrealistic and R&D costs are not fully reflected. The company almost reached our target price of £12,000p (and $72.5 in ADR). Therefore, we decided to move our rating from Buy to Neutral, confirming our target price (regarding the potential Chinese listing, we are not making any changes). On the valuation, the company is currently trading at a 2024 estimated price earning of 21.0x, which is at a 40% premium compared to EU majors player peers (Sanofi, Roche, Novartis). We should also recall that AstraZeneca has always traded at a premium valuation compared to the sector average; however, the company's EPS three-year historical average was a 120% premium, while on a one-year basis, the premium is at 130%. Risk/reward is skewed on the downside. The near-term catalyst is P3 data DS-1062, Tagrisso LAURA, and DS-106. Downside risks include pipeline failure, litigation costs, lower drug launches with poor commercial execution, and higher competition. Plus, we should add the US drug pricing reform.

{kind=link}

Source: AstraZeneca Q1 results presentation

For further details see:

AstraZeneca: What's Next? (Rating Downgrade)