ATRO - Astronics' Commercial Exposure Might Not Be So Bad Anymore

2023-03-12 06:46:58 ET

Summary

- COVID-19 is still somewhat with us, but it's quite clear people are less scared now and the recovery is happening in commercial aviation.

- Leisure generally is coming back despite some inflation pressure, and we think that fleets that have shrunk around 20% over the last few years will start to replenish.

- Backlogs are growing, and general aviation also proves stable, a thesis we've long been following, where Astronics is the first mover in electronics for small airframes.

- The commercial recovery is what is driving results with lighting, power and other cabin products like in-flight entertainment systems.

- While the recovery is a good thing, Astronics is involved in mostly pretty commodified markets, and we're just not interested at the current valuation.

Astronics Corporation ( ATRO ) makes various implements for cabin lighting and power, as well as electronics systems, for the commercial, military and B&GA markets, but mostly commercial. We think that the commercial recovery has only just started now that people are tired of COVID-19, and the B&GA exposure is also quite appreciated, where business and general aviation markets have been consistently strong and have secular tailwinds behind it. While there are plenty of positives around a reignited CAPEX cycle for carriers, we just don't like this company's business enough to care about it at this valuation. For a producer of pretty commodified products, it's too expensive and this stock is an uncreative solution in a pretty difficult market environment.

The Business Trends

The company sells products like plugs, lighting systems, stuff for climate control, electronics systems like electronic circuit breakers and other modules, all for cabins and cockpits of aircraft. Their main customers (10%) in the commercial business is Boeing ( BA ), but they also sell to Panasonic ( PCRFY ) (10%) which makes in-flight entertainment systems, where Astronics provides the electrical systems and controls for those displays and systems. These are pretty commodified products for the most part. They also make avionics, and this is less commodified, but it's not their largest business within their aerospace segment.

Aerospace Segment - Products (10-K)

{kind=link}

Their markets are military, commercial and B&GA . B&GA (15% of revenues) has been stable for the last couple of years, and stable throughout the pandemic even relative to pre-pandemic levels, and in this market they do electronic circuit breakers and other systems that are a little more unique for these smaller airframes, in addition to their other products. Their decent positioning in this market has put them ahead substantially of 2018 levels.

The military markets have not been that great throughout the pandemic, and are actually a source of more than 20% decline YoY due to the finishing of some non-recurring effects from the previous year. Contract economics don't play in their favour here, and you can see the commodification relative to the military customers who are more discerning.

Aerospace Segment - Markets (10-K)

{kind=link}

They also have a segment called test, that's been a pretty mediocre performer, where Astronics sells electronics and components that are used in the test and simulation markets for aviation practice. These are substantially military exposed. However, they have won a new contract here, and while this means some upfront investment it is a contract that could be between $150-200 million in size when it becomes fully valued and awarded, although ATRO has been selected (it's for radios). This explains the operating losses that they have here.

{kind=link}

Outlook

Backlogs are growing, and it is primarily being driven by the commercial segment, where we have a lot of hope in the CAPEX cycle of carriers into new fleets. Even this year's sales growth in commercial has been significant at over 50%.

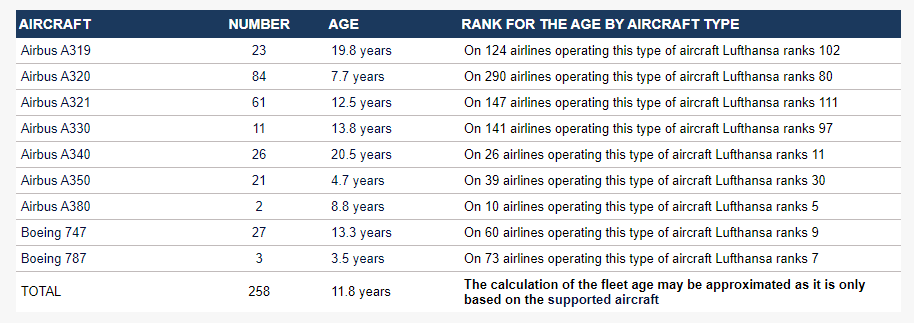

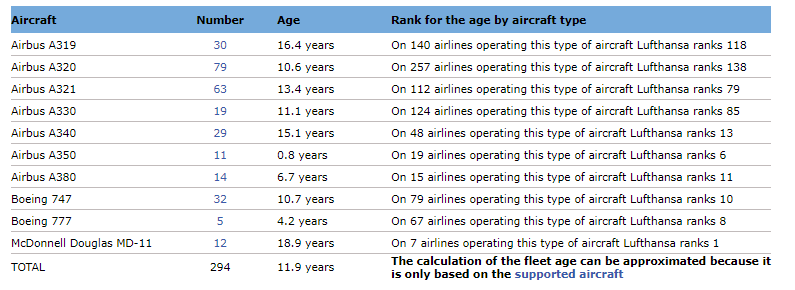

Using the Waybackmachine , you can compare the size of the fleets of a carrier like Lufthansa ( DLAKF ) since before the pandemic. It has declined by more than 20% . Moreover, the fleet ages have stayed the same, even though the first planes to retire were the older ones. While Lufthansa primarily buys Airbus ( EADSF ) planes, other carriers would show the same trends, and both ageing and shrunken fleets are bound to start growing again as traveling re-emerges. Even just looking at the latest payroll data, many of the job additions are in leisure . Even the reopening is a tailwind, since Astronics supplies the Embraer ( ERJ ) E2 with lighting systems, and these sorts of jets are perfect to supply regional Asian travel that the Chinese are most likely going to prioritise, due to restrictions on inbound Chinese in many countries. Revenge travel and general leisure recovery, even if not to pre-pandemic levels due to inflation, economic difficulty and more expensive tickets on higher fuel prices, is a good thing for Astronics, and we expect it to continue to trend to pre-pandemic levels in terms of growth.

{kind=link}

{kind=link}

The issue is the marginality of a business like this is bad, and it's not that cheap. If it continues its recovery, it will come out operating losses and into operating profits thanks to operating leverage but also the initiation of the new test segment contract with the US military. However, terminal margins aren't that high because the products are still commodified. Valuation of forward EBITDA isn't much better than 7x EV/EBITDA, and while that isn't expensive, there are way better deals in the market - companies that trade substantially cheaper with far superior economics. B&GA exposure and commercial recovery, where B&GA has demonstrated high levels of resilience to almost anything during the pandemic, are major positives for the company, and it could start recovering the stock price which is quite beaten down, but we look for more value than this to support our continued outperformance - this is just not compelling enough.

For further details see:

Astronics' Commercial Exposure Might Not Be So Bad Anymore