ASUR - Asure Software: Growth And Margins Are Primed To Accelerate

2023-12-18 00:34:06 ET

Summary

- Asure’s revenue has grown impressive, with a CAGR of +17% into the LTM period. This has been driven by an aggressive go-to-market strategy, underpinned by a quality service.

- Asure is gaining market share from its peers, has low churn, and has very positive feedback from its customers. The company appears positioned to achieve more consistent growth.

- We are expecting adjusted EBITDA-M to exceed 20% in the coming years. We expect less volatility in the coming years due to its growing recurring revenue base.

- Asure is performing exceptionally well relative to its peers, with superior growth and margins. At a smaller size and targeting a fragmented market of small-cap clients, we see a solid runway to maintain this trajectory.

- Asure’s valuation does not reflect this attractiveness. It is trading at a discount to its historical average and a small premium to its peers.

Investment thesis

Our current investment thesis is that Asure Software ( ASUR ) is a high-quality business that is primed to grow substantially in the coming years. Product development is beginning to pay off, allowing it to gain market share and build its recurring revenue basis. Underpinning this is a superior value proposition to the micro-small cap segment in particular.

In the coming years, we expect volatility to subside and margins to improve, contributing to an improvement in outlook and a return of positive investor sentiment. With the company already pushing toward a FCF margin of >10%, investors are primed to win regardless, be it through share price appreciation or an initiation of distributions.

Company description

Asure Software is a leading provider of cloud-based Human Capital Management ((HCM)) software solutions. The company offers a comprehensive suite of workplace management solutions, including workforce management, workspace management, and asset management.

Share price

Asure’s share price performance has been volatile, with periodic bouts of impressive gains followed by noticeable drawdowns. This is a reflection of its inconsistent financial performance and the corresponding change in investor sentiment / long-term outlook.

Financial analysis

{kind=link}

Financials (Capital IQ)

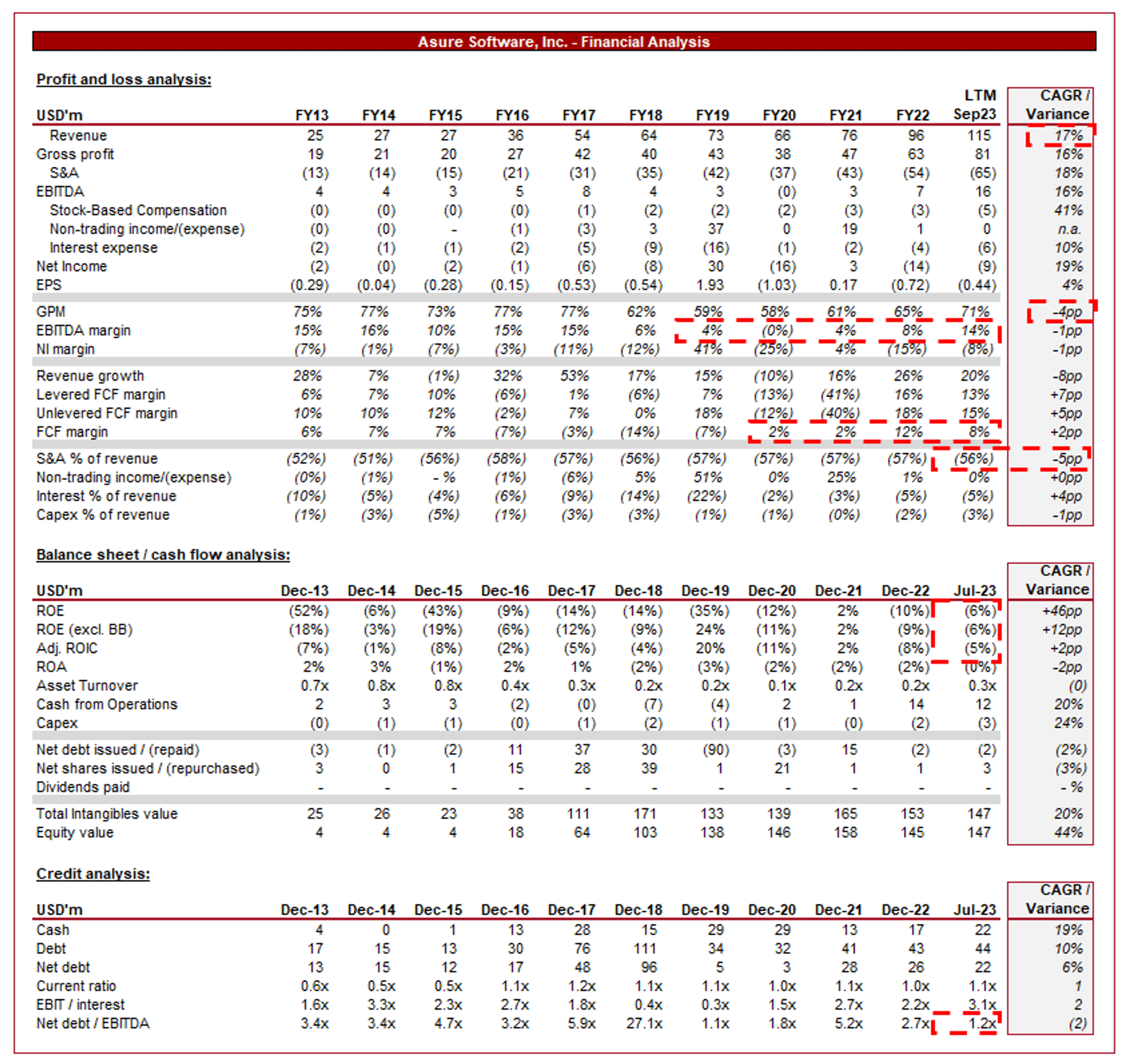

Presented above are Asure's financial results.

Revenue & Commercial Factors

Asure’s revenue has grown impressively, with a CAGR of +17% into the LTM period. This growth has been inconsistent, with a (1)% rate in FY15 followed by +32% and +53% in the following years. Further, the company’s EBITDA growth has also been volatile, broadly growing in line with revenue.

Business Model

{kind=link}

Asure

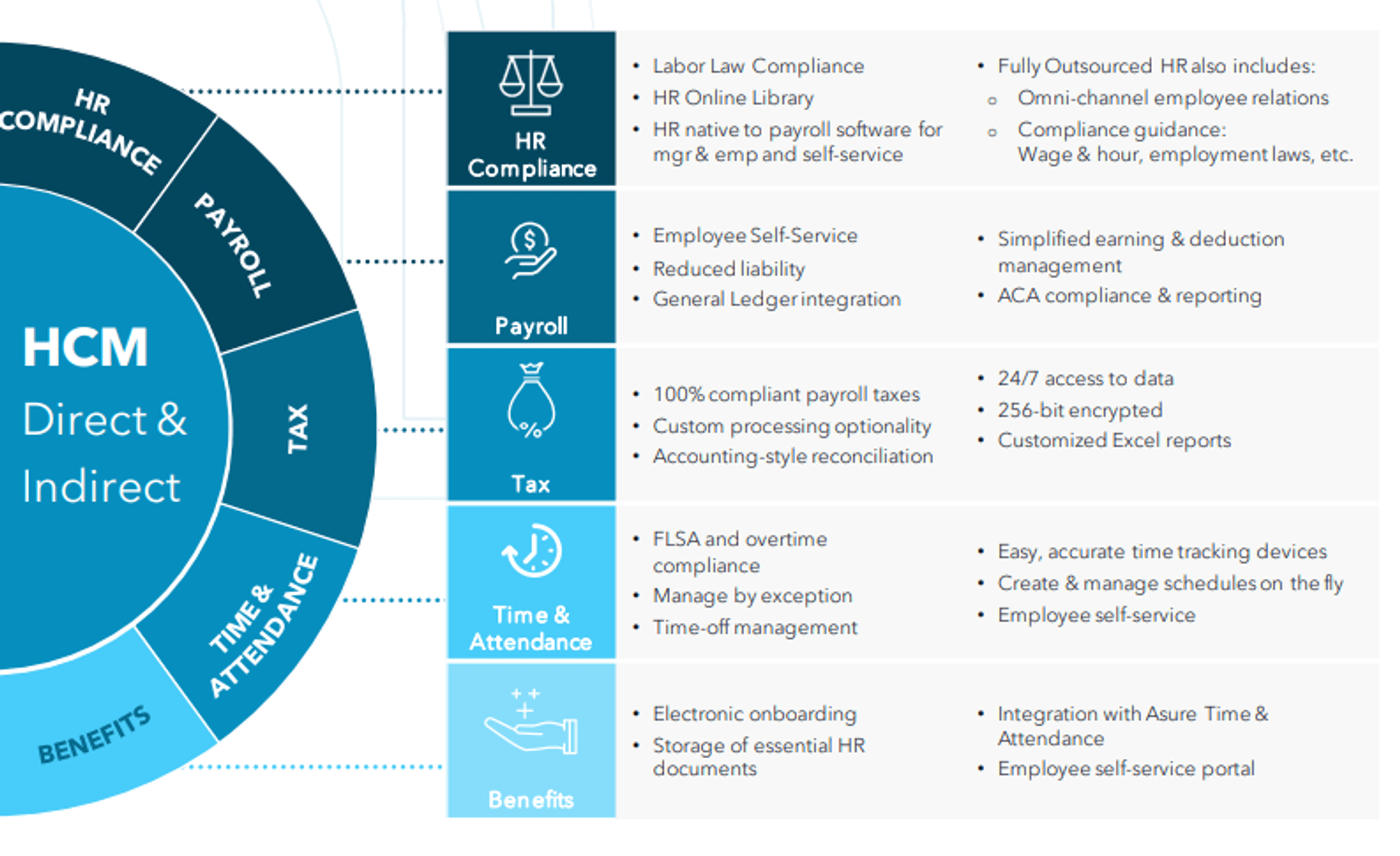

Asure offers a suite of HCM solutions that cover areas such as payroll processing, time and attendance tracking, benefits administration, and HR management. In addition to HCM, Asure provides solutions for workspace management. This includes tools for managing meeting rooms, desk reservations, and optimizing overall office space utilization.

These solutions are designed to streamline HR processes, reduce administrative burdens, and improve overall workforce management efficiency. With increased regulatory requirements, both from an administrative and security perspective, the importance of outsourcing to experts has grown.

Asure's offerings are delivered through a Software as a Service ((SAAS)) model. This cloud-based approach provides several advantages, including scalability, accessibility, and automatic updates. Clients can access the services from anywhere, promoting flexibility and ease of use. From a financial perspective, this has allowed Asure to generate recurring revenue, allowing Management to focus on new customer wins and cross-selling.

Asure's solutions are designed to be customizable to meet the unique needs of different organizations and scalable at the same time. This flexibility is crucial for winning new clients who often operate under unique circumstances.

strategic acquisitions have played a crucial role in expanding a company's market reach and offerings. Following a series of strategic acquisitions, the company has generated accretive returns in recent years through acquiring resellers, improving its unit economics.

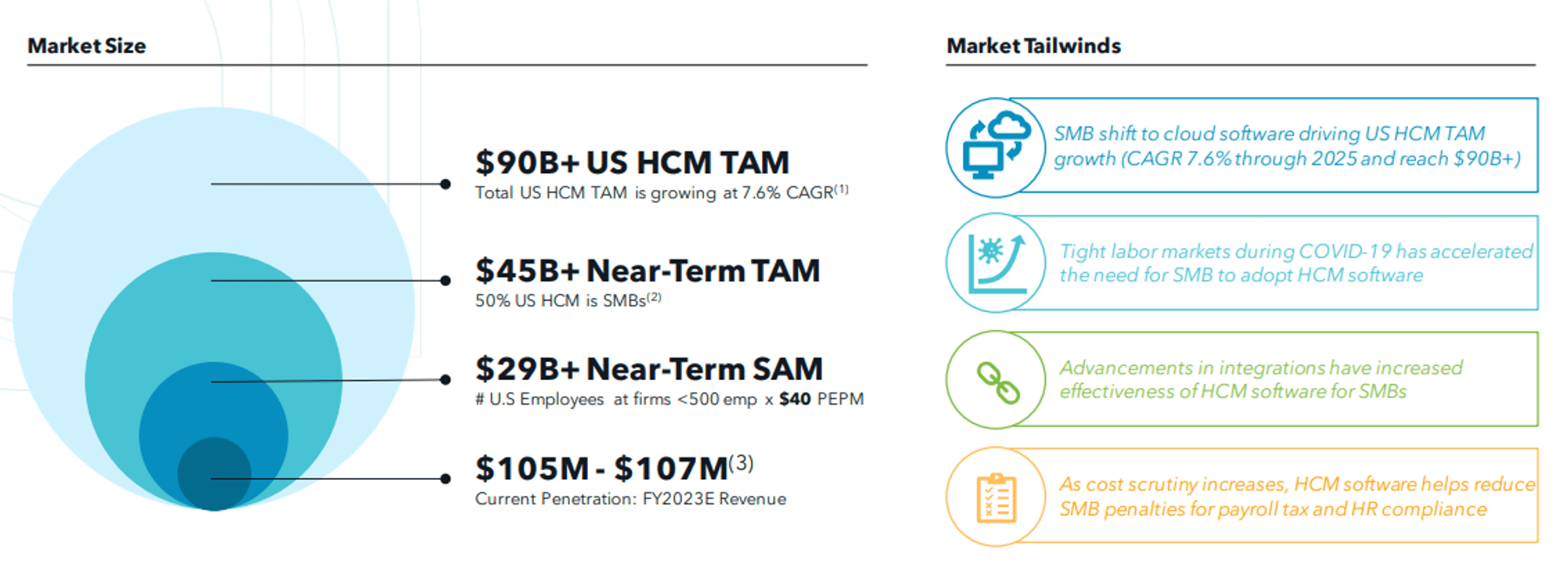

Management estimates its SAM in the near-term to be ~$29b and its TAM to be ~$45b. This represents the importance of the industry, which impacts almost every business across the US.

{kind=link}

Asure

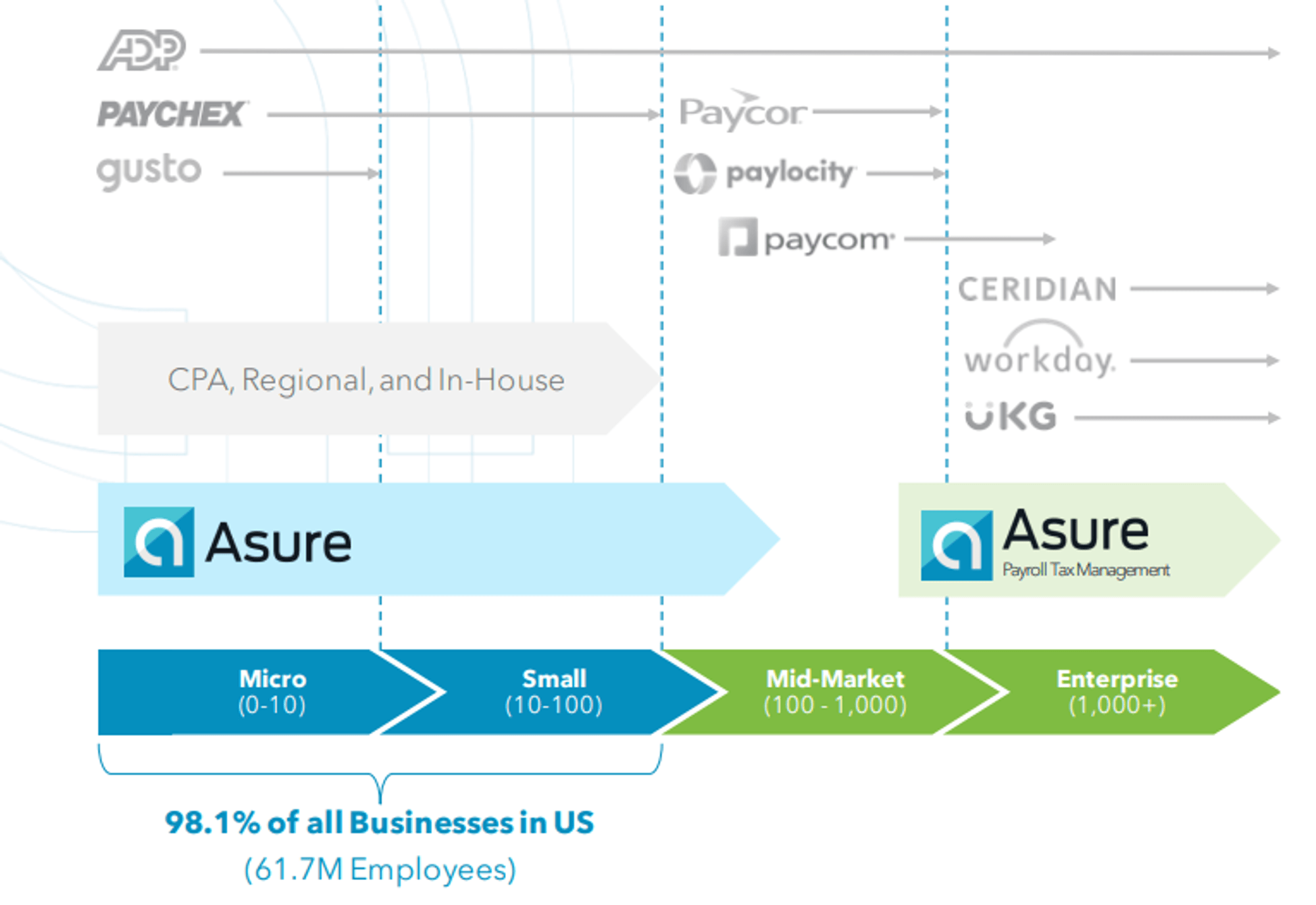

The size of its particular segment is a reflection of its focus on smaller businesses, which comprise an estimated ~98.1% of total businesses in the US. This gives the company a significant runway for growth and less competition, as larger providers have less incentive to specialize their service for smaller companies (competing on price).

{kind=link}

Asure

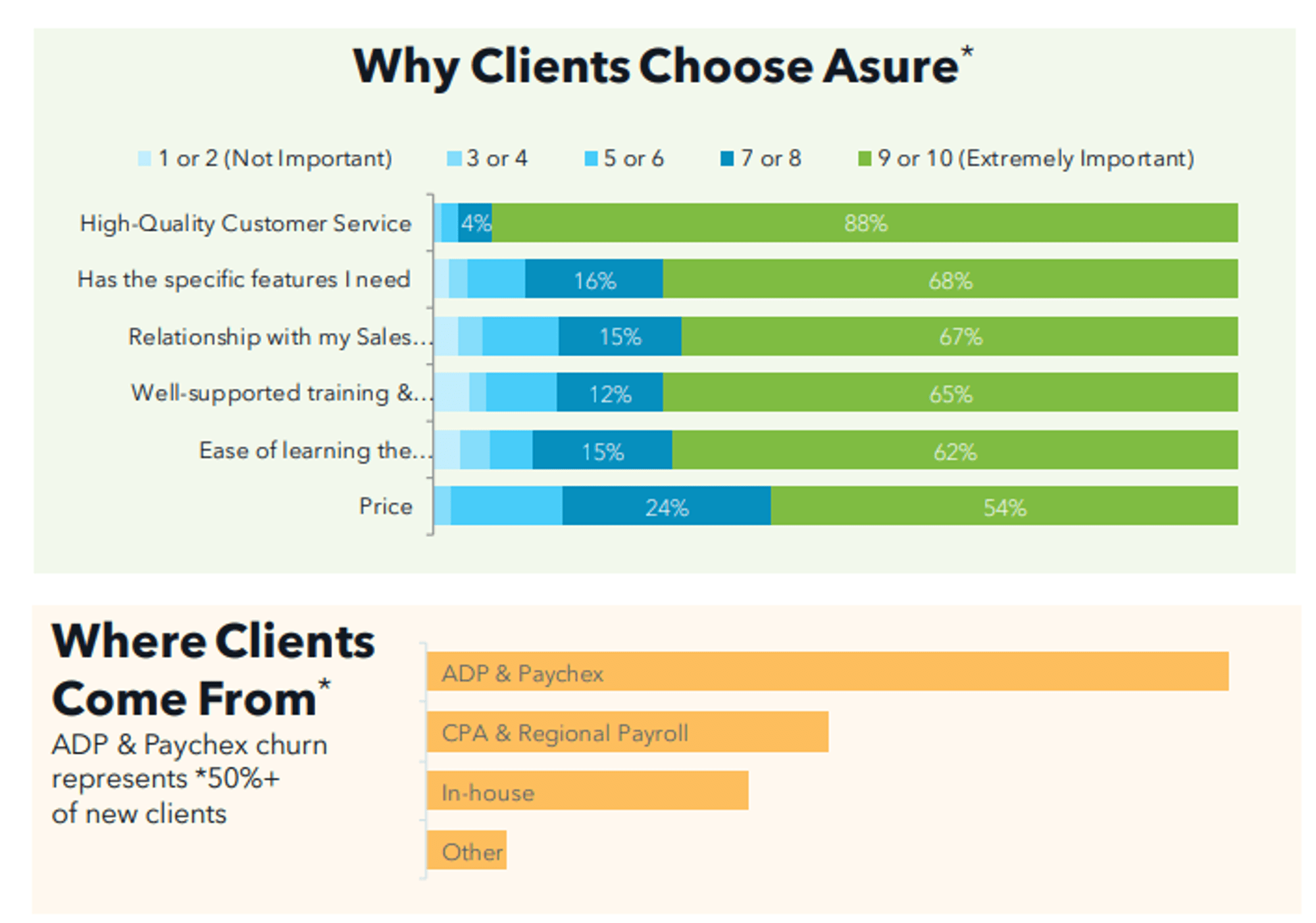

Not only has Asure differentiated itself through its technological qualities and segment specialism, but also how it supports its clients. The company scores well for customer service, relationships, and support.

{kind=link}

Asure

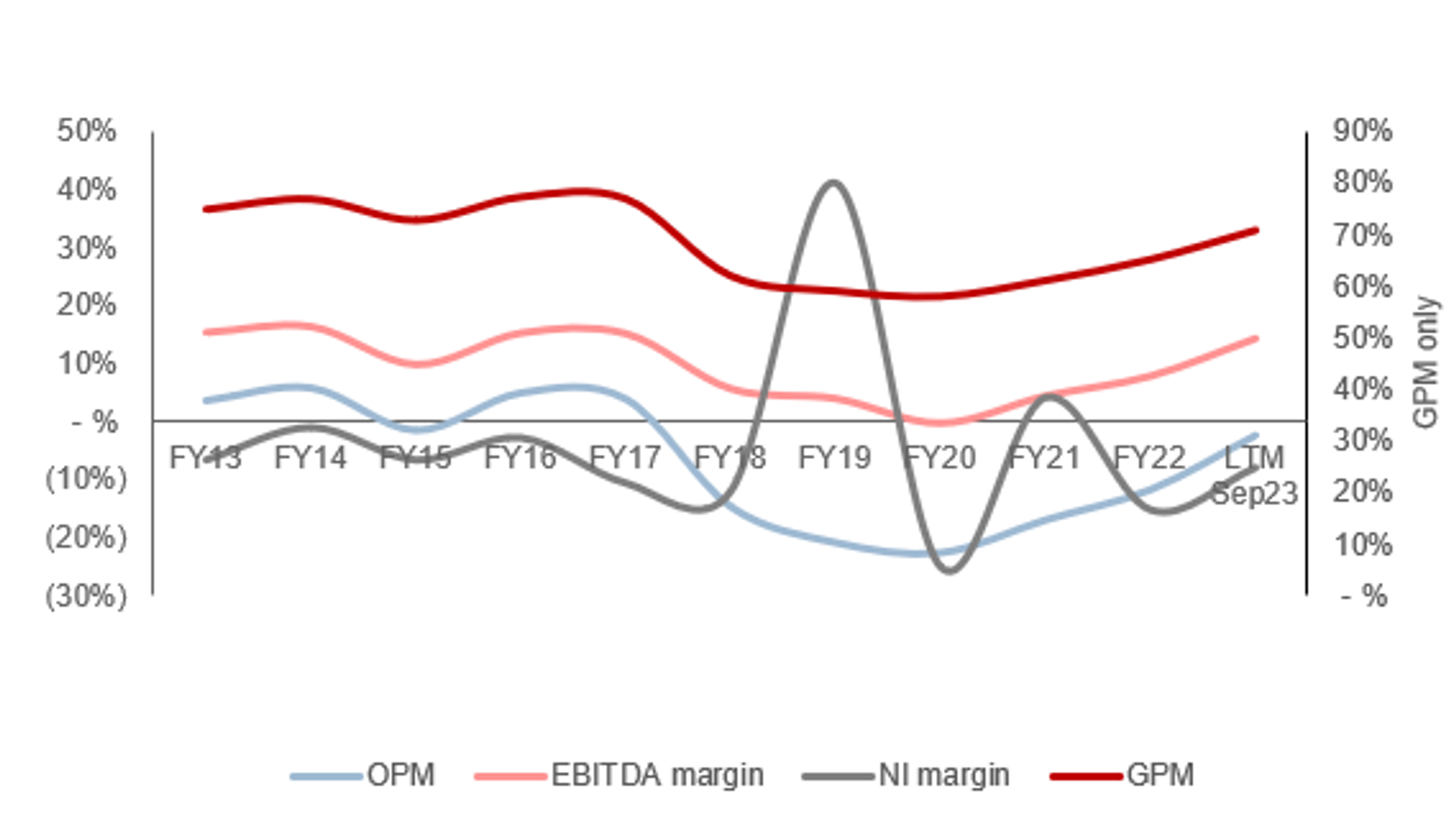

Margins

{kind=link}

Margins (Capital IQ)

Asure’s margins have been highly volatile, with a significant decline prior to the pandemic. This is important to distinguish as the pandemic period materially worsened its position, but the company was already struggling.

Following this, Asure has bounced back well, with EBITDA-M reaching 14% in LTM Sep23. This is a reflection of an upswing in demand and the roll-out of new services, allowing the company to improve its monetization.

Margin development has been inconsistent due to heavy competition within the industry, particularly in the technology-enabled segment that has grown well due to many new entrants.

Difficulties with differentiation create risk associated with incrementally margin improvement in the coming years, although its historical trading implies its current level is maintainable. We expect an uptick to occur, although a normalized level remains uncertain.

Quarterly results

Asure’s recent performance has remained strong despite the wider market weakness, with top-line revenue growth of +21.8%, +38.7%, +35.9%, and +49.9% in its last four quarters. In conjunction with this, margins have accelerated rapidly, with LTM EBITDA-M almost double FY22 (14%).

This impressive performance is a result of incremental improvements to its product offering over time. The company has materially developed its service offering, partnering with a range of leading firms to improve integration for wider business purposes, as well as broader technological enhancement (such as AI integration).

This is an impressive performance given the wider macroeconomic environment, as this is inevitably incentivizing reduced spending at a corporate level to protect margins. This is particularly the case as Asure targets small businesses, which are generally more sensitive to cyclicality. This is a reflection of the attractiveness of its services.

Key takeaways from its most recent quarter are:

- Recurring revenue comprises 80% of total earnings, creating the potential for a smoother growth trajectory.

- Revenue growth has also been supported by improved sales efforts, with conversion improving and greater penetration into the fragmented segment. This is having a compounding effect of building momentum.

- The company has partnered with Amazon Web Services’ ( AMZN ) “Application Modernization Lab”, which is “ an exclusive group comprised of 10 – 12 of AWS’ most innovative customers”. The objective being to enhance its HCM SaaS offering. This will focus on the improvement of its cloud and AI services.

- Added to the Russell 3000 Index in June.

- Guidance has been lifted for FY23, with an adj. EBITDA-M of 19-20% and top-line of $118-120m.

Balance sheet & Cash Flows

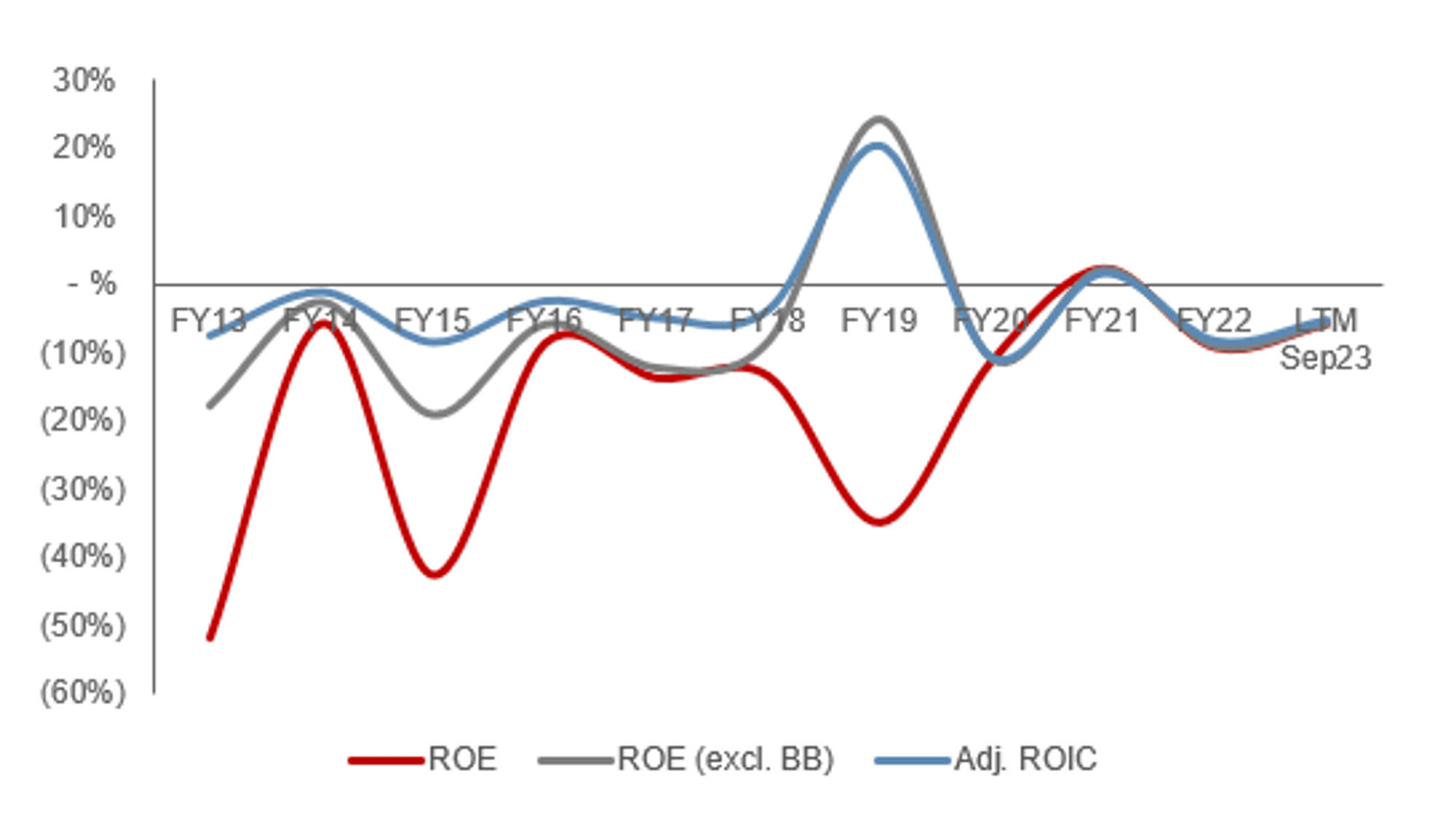

Asure is conservatively financed, with a ND/EBITDA ratio of 1.2x. This is not usually for a business of this profile, as it is already generating healthy cash flows to find operations. Historically, FCF generation has been lacking, primarily due to investment in growth. This is beginning to unwind and we expect FCF-M to remain in the HSD/LDD range.

This movement into the next stage of its growth story, with profitability accelerating, should allow for its ROE to transition to an attractive range. We can see Asure reaching ~20% by FY24 as profitability growth exceeds revenue.

{kind=link}

Returns (Capital IQ)

Outlook

{kind=link}

Outlook (Capital IQ)

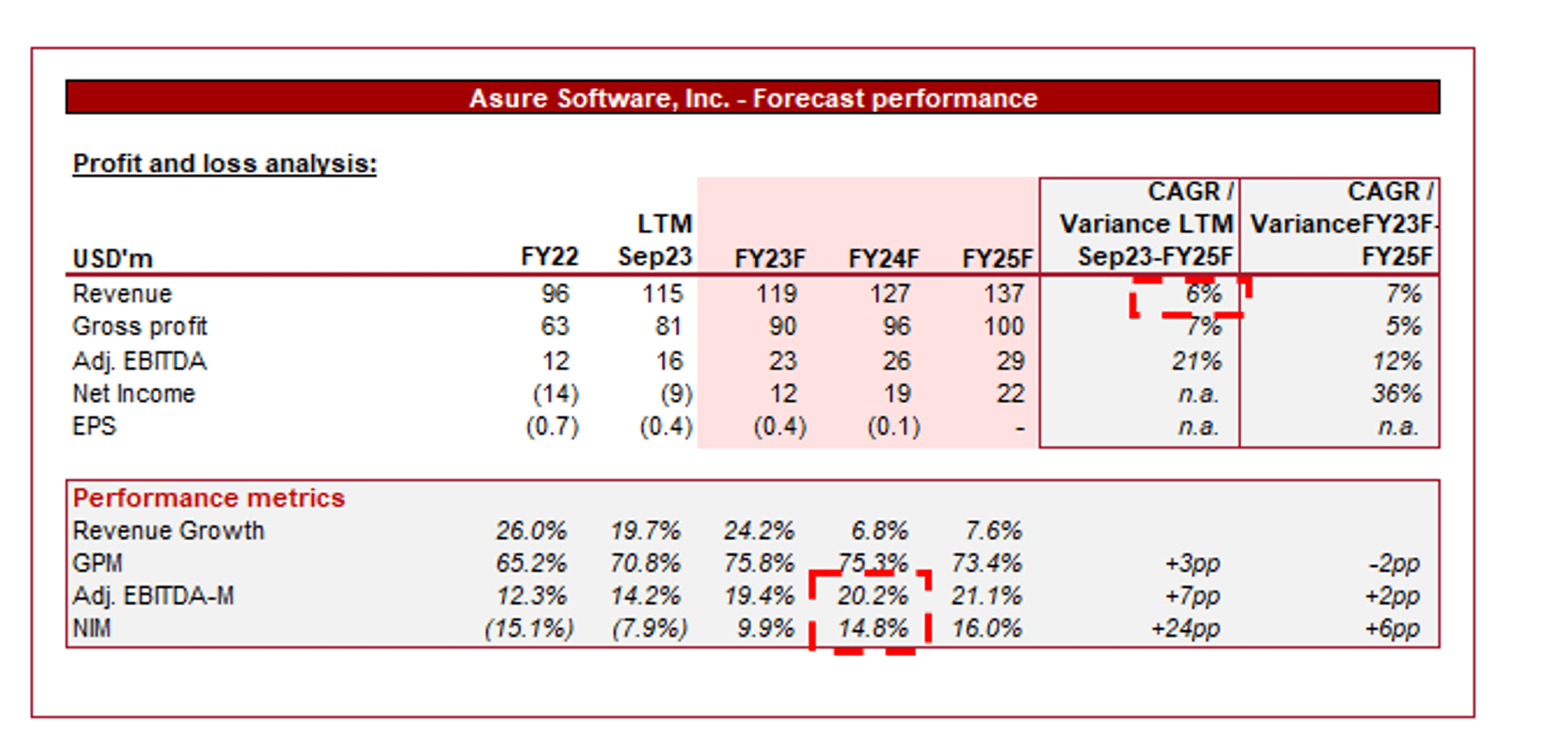

Presented above is Wall Street's consensus view on the coming years.

Asure’s revenue is forecast to grow below its historical level, with a CAGR of +6% into FY25F. In conjunction with this, margins are expected to accelerate, reaching an adj. EBITDA-M of ~21.1% in FY25F.

We consider the assumptions to be conservative given the recent revenue growth, implying a superior rate can be achieved, particularly given the stickiness of demand and the continued development of its product. Further, its underlying development should drive margin improvement as discussed previously.

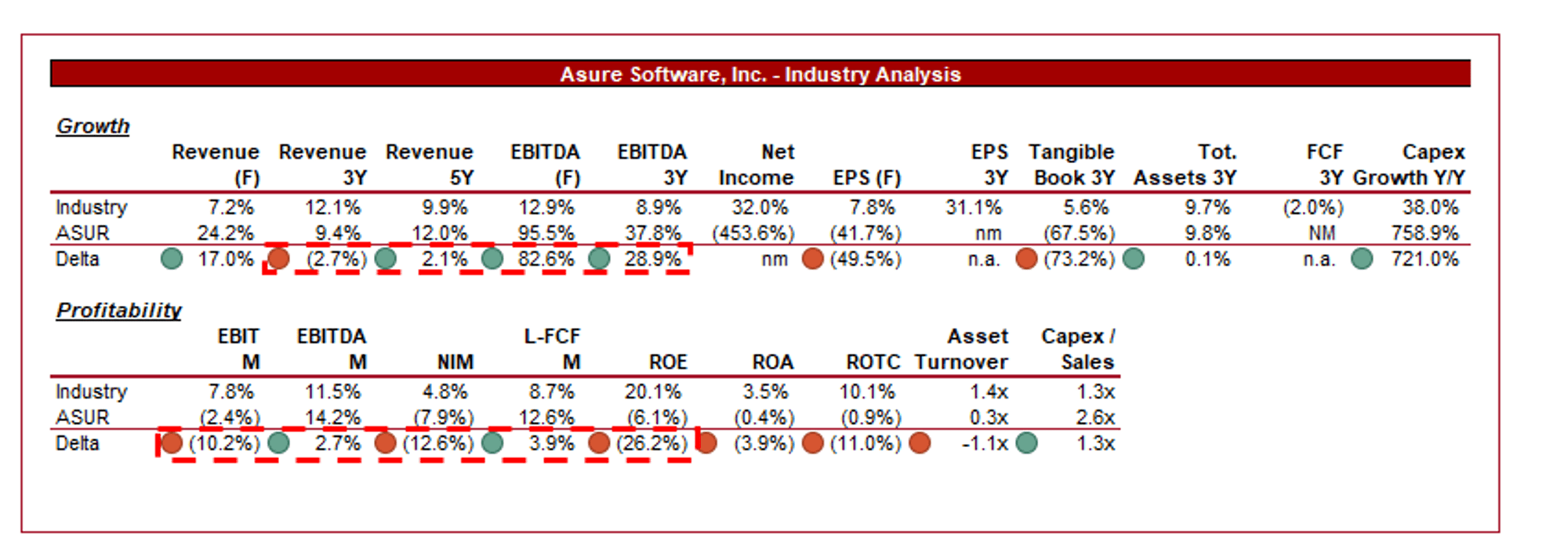

Industry analysis

{kind=link}

HR (Seeking Alpha)

Presented above is a comparison of Asure's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

Asure is performing well relative to its peers, particularly when you consider the upward trajectory of the company’s financials. It has achieved superior growth to its peers, owing to its aggressive growth strategy and relatively smaller base. Impressively, it already boasts a better EBITDA-M compared to the average, with greater scope for improvement in the coming years.

Based on this, alongside the medium-term upside, we believe Asure should be trading at a premium to its peers.

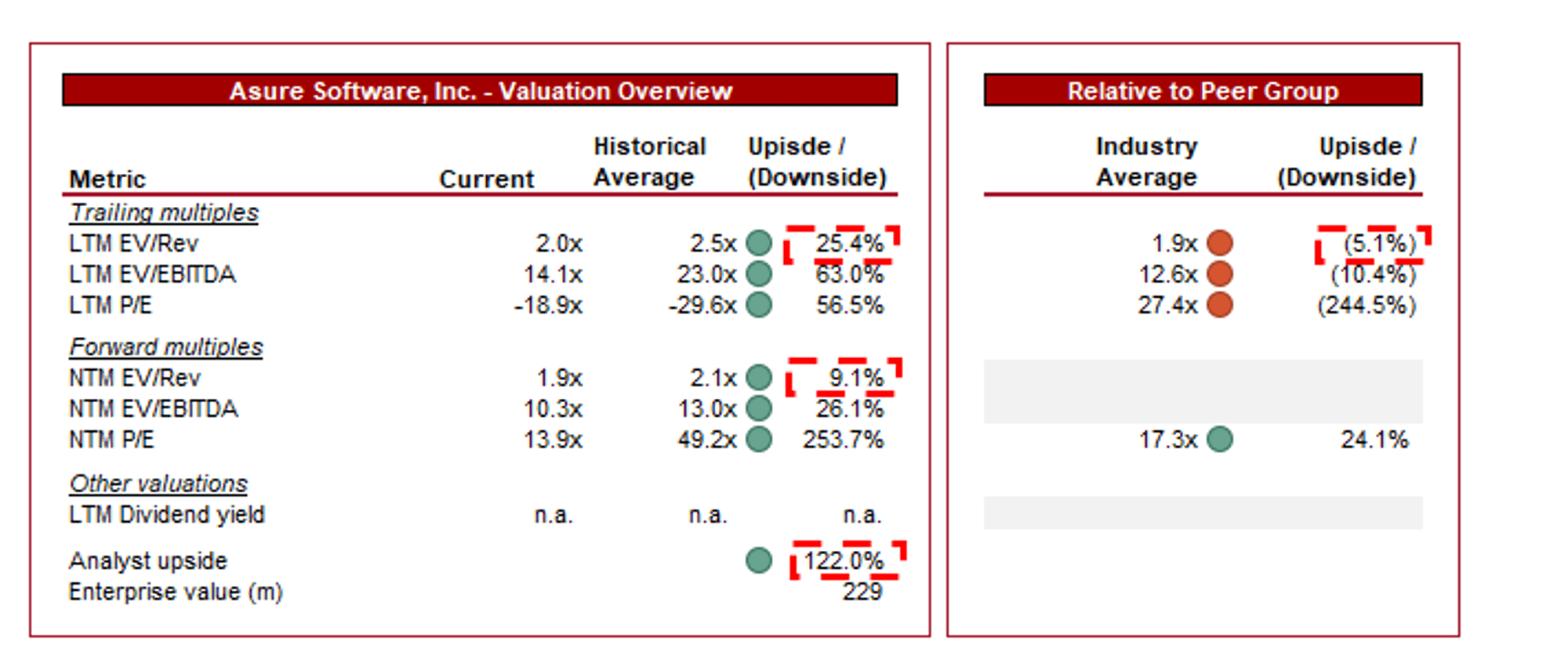

Valuation

{kind=link}

Valuation (Capital IQ)

Asure is currently trading at 2x LTM Revenue and 10x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is reasonable in our view. The company has had a volatile history and its share price has responded in turn. Broadly, it has not developed as expected. Offsetting this, however, is the improvement achieved thus far and the renewed scope for outperformance. Based on this, particularly if subsequently realized, a premium will quickly materialize.

Further, Asure is trading at a small premium to its peers on an LTM basis, although this transitions to a premium on a NTM basis. An LTM premium is justifiable for the reasons discussed, although the premium must be sufficient to be reflected on a NTM basis. This is not the case currently, further implying upside.

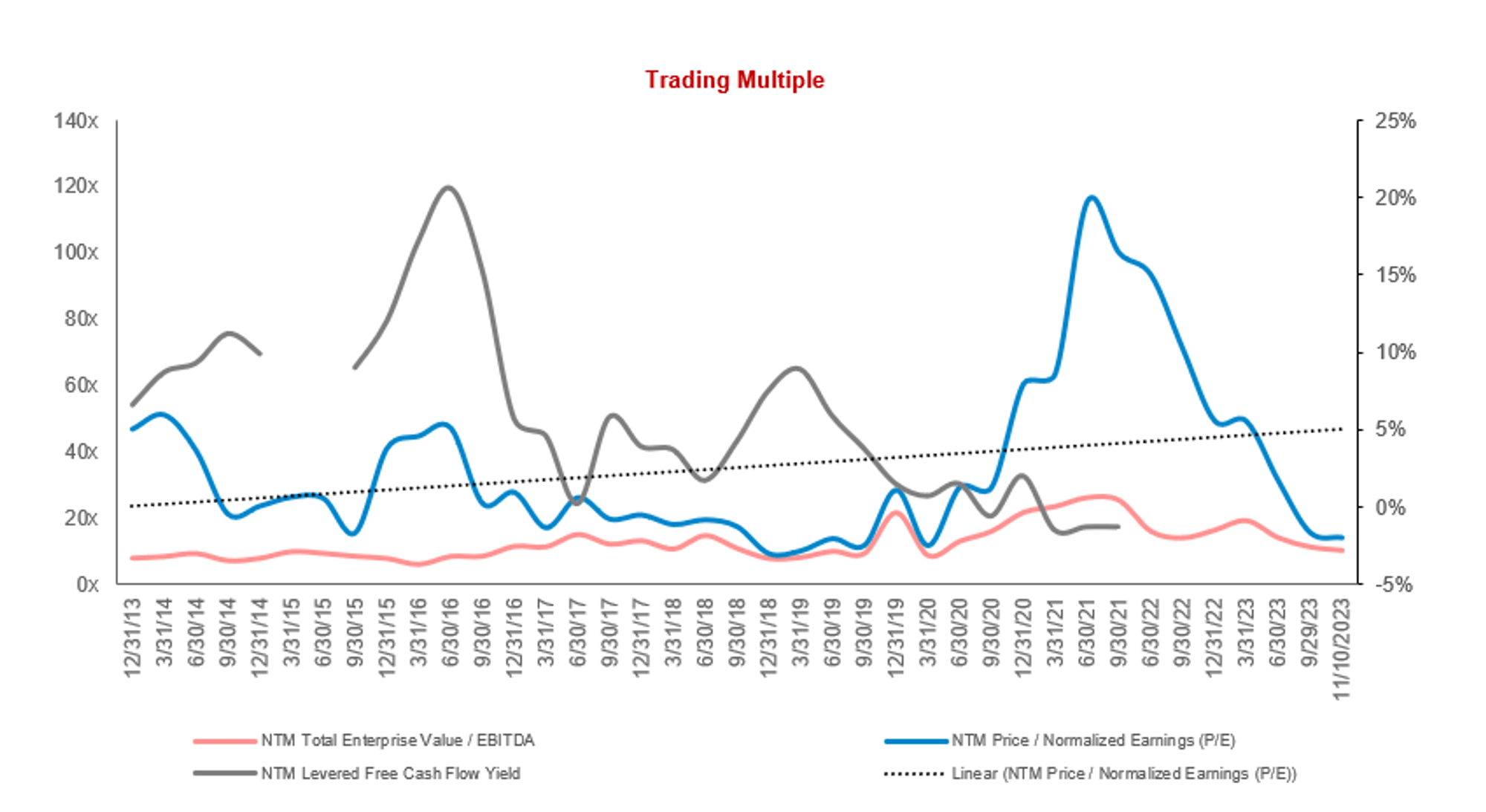

{kind=link}

Valuation evolution (Capital IQ)

Key risks with our thesis

The risks to our current thesis are:

- Economic downturn impacting client budgets for HCM solutions.

- Technological disruption or cybersecurity issues affecting client trust.

Final thoughts

Asure is a high-quality business with multiple levers for growth. The company is gaining market share quickly by targeting the largest segment of the market by volume, although benefits from its willingness to specialize, allowing for superior relationships and pricing. Underpinning this is a quality suite of products that have years of investment to improve, with new avenues such as AI representing future growth potential.

Although the company has had a volatile history, we believe it has reached a crossroads from which it will now experience an acceleration. At a discount to its historical average and a small premium to its peers, we see sufficient upside and margin of safety.

For further details see:

Asure Software: Growth And Margins Are Primed To Accelerate