ASUR - Asure Software: Multiple Tailwinds To Sustain Profitable Growth

2023-06-06 08:30:00 ET

Summary

- Asure Software is poised for growth and margin expansion in FY 2023, driven by improving US employment rates, successful product launches, and cost-saving initiatives.

- I set an FY 2023 target price of ~$18 per share. With the stock trading at $12 per share today, there is attractive upside potential.

- Risk remains minimal to moderate. Investors should monitor the development of ASUR's tax processing and interest revenue streams, as they are sensitive to macroeconomic changes.

Asure Software (ASUR) provides cloud-based Human Capital Management / HCM software solutions primarily for SMBs. Their revenue comes from a combination of recurring and professional service fees. They generate recurring fees from payroll, tax management, time and labor management, and HR compliance activities done within its platform as well as from the payment made by reseller partners for white-labeling ASUR's solution. They generate professional services revenue from implementation fees, consulting projects, maintenance, hardware devices, and transactional revenues from the Employee Retention Tax Credit / ERTC.

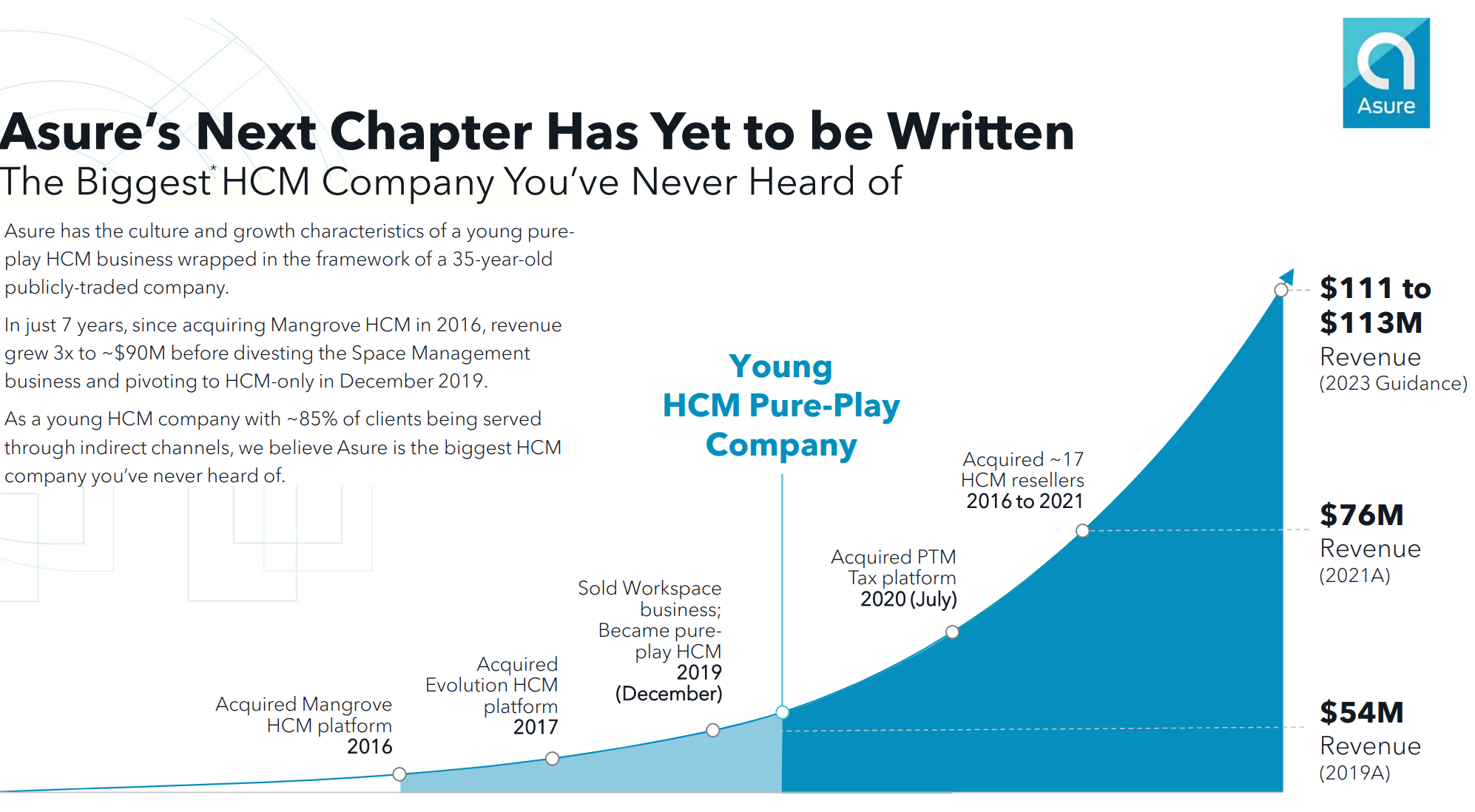

85% of ASUR’s clients are served through ASUR's white-labeled solution provided by the resellers. As part of its growth strategy, ASUR had been strategically acquiring their HCM resellers between 2016 - 2021. This allows them to expand their distribution channels and reach a broader customer base.

The business faced a challenge during COVID-19 in 2020, though growth has significantly accelerated since, and the current outlook suggests a high chance of continued growth followed by margin expansion due to some catalysts on the stock. Downside risk remains minimal to moderate in the near term.

In this coverage, I upgrade the stock to overweight. It appears that ASUR has progressed very well since my first coverage in 2021 , where it was trading at ~$6.3 per share then. Today, the stock is trading at ~$12 per share.

Catalyst

I think that three near-term catalysts may continue to benefit ASUR into FY 2023 and beyond. The first one is the continuing improvement in the US employment rate since the pandemic, the second one is the timely introduction of several solutions since 2021, such as ASUR marketplace, that have proven to be successful and demonstrated the potential to sustain growth beyond 2023. Finally, I view the $5 million annual cost-saving initiative mentioned by the management as an opportunity to maintain the relatively solid gross margin level as seen in Q1 as well as to unlock margin expansion.

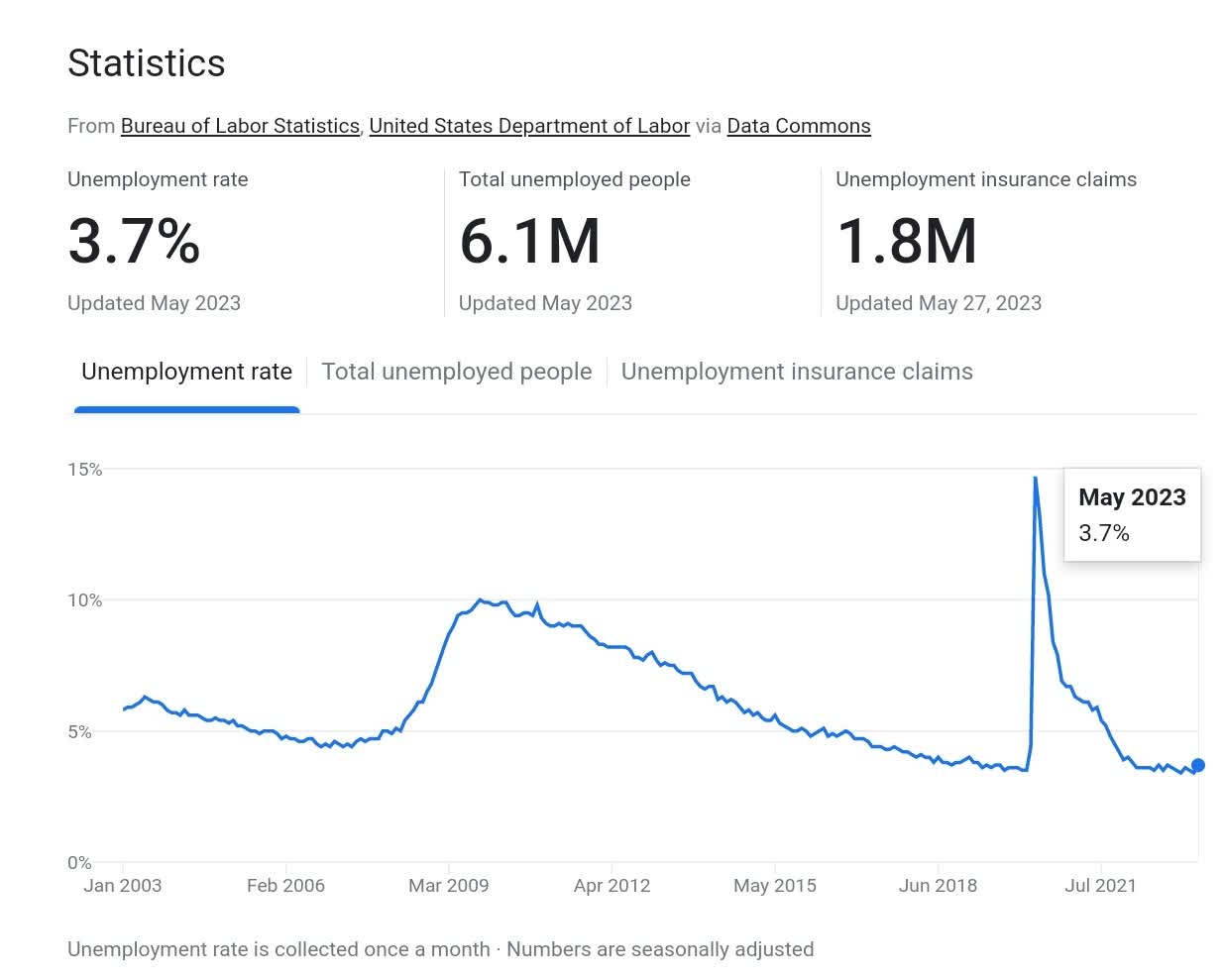

As an HCM platform provider, ASUR generates revenue from fixed and additional per-employee fees charged to its SMB users for the use of its tax processing or payroll services. As such, despite the mission-critical nature of the platform, businesses like ASUR still rely on an optimal employment rate as a key growth driver. During the COVID-19 pandemic in 2020 when the mandated nationwide lockdown created massive layoffs and headcount adjustments across businesses of all sizes, the unemployment rate saw a steep increase to +14%. Eventually, this seems to have affected many of ASUR’s SMB clients too, as it reported a 10% decline in its revenue then.

{kind=link}

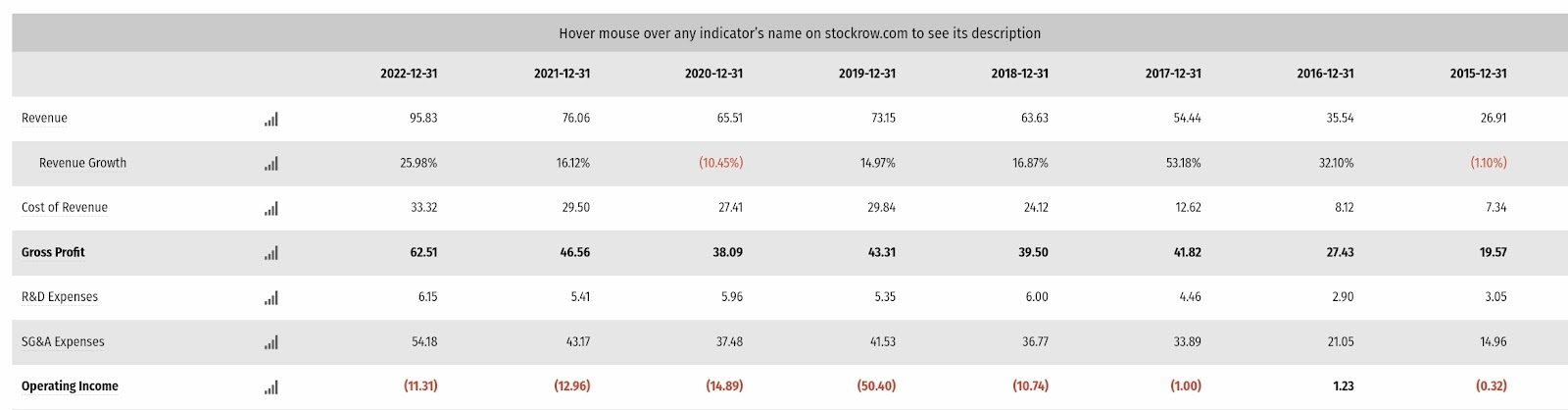

Since then, the labor market has gradually normalized and the unemployment rate as of May 2023 was 3.7%, which is pretty much at the pre-pandemic level. Consequently, ASUR has also benefited from such macro improvement. Just a year after seeing a 10% decline, ASUR recovered quickly and reported a +16% growth in FY 2021. Growth even reaccelerated further to ~26% in FY 2022.

I think that at 3.7%, unemployment rate is also around the low end of the pre-pandemic range in 2019. As is apparent with the layoff trend and fear of recession, it is possible that unemployment rate may see soft uptick in the near term, though I believe that we may expect less volatility. In the near term, I expect that the unemployment rate to probably vary within 3.4% - 5% range, and if any, the impact on ASUR's business would also be minimal and in stark contrast with what we saw during COVID 19. As a result, I believe that ASUR should continue to benefit from the macro tailwind with its growth path remain intact in and beyond FY 2023.

{kind=link}

On the other hand, ASUR has also demonstrated a strong ability to execute its growth strategy to capture the macro-driven growth opportunity, particularly in effectively leveraging strategic M&As to create value. Recognizing that resellers play a vital role in its sales motion, ASUR acquired ~17 HCM resellers between 2016 and 2021. This move seems to align with the fact that by gaining control over the reseller network, ASUR may maintain and optimize its growth better.

{kind=link}

Furthermore, I expect Asure Marketplace, which was launched in May 2022, to continue driving growth for ASUR beyond 2023. In Q1, the marketplace business already contributed 20% to the total increase in recurring revenue. The key driver in any third-party integration marketplace business is the continuing usage and addition of new complementary HCM services by working with more partners. These activities would then create cross-sell opportunities.

I think that it is relatively surprising to see how quickly the marketplace business has gained meaningful traction in just less than 12 months after launching. As such, it is quite possible for the marketplace to make up 30% - 40% of ASUR’s business in the future, as per the management’s remarks in Q1.

Similarly, the HR compliance service, enhanced by ASUR in 2022, has exhibited consistent strength in Q1. These achievements are reflected in ASUR's impressive Q1 results, where it reported 136% growth in bookings and 36% growth in revenue, suggesting that the business is still in the early stages of its momentum and likely to continue its growth throughout FY 2023.

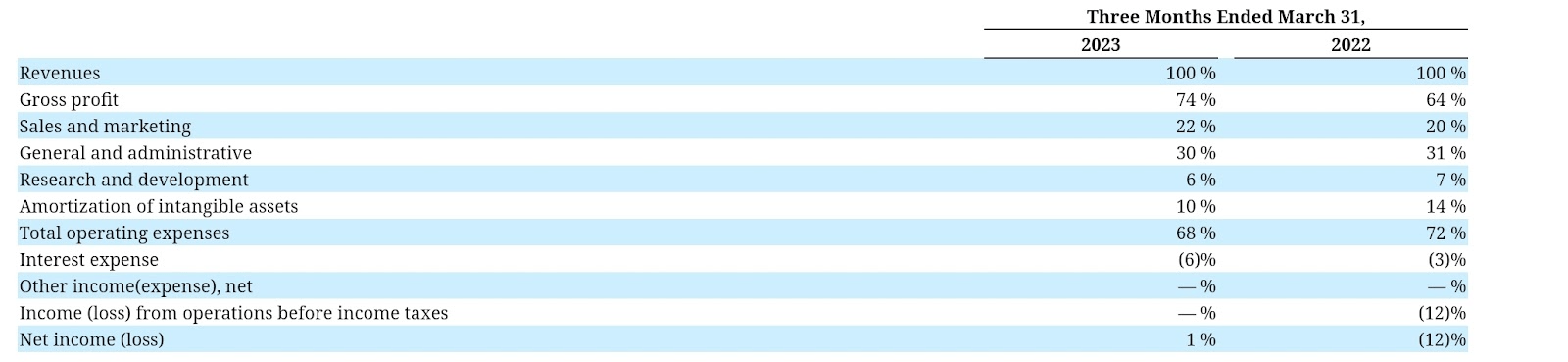

In the end, I also expect ASUR’s $5 million annual cost-saving plan to drive margin expansion. I think that there is a lot of room for optimization across cost of sales, S&M / sales and marketing, as well as G&A due to the possible operational inefficiencies from the recent corporate initiatives over the last few years, including the 17 HCM reseller M&A roll-ups. In FY 2022 and 2021, for instance, increase in corporate expenses resulted in G&A expenses being 35% - 36% of revenue, a relatively high figure. Similarly, cost of sales was also ~35% of revenue in FY 2022 - resulting in 65% gross margin.

{kind=link}

I think that as recurring revenues continue to increase alongside the cost-saving initiative activities, such as consolidation and standardization efforts, taking place internally post-M&As, we should be seeing margin expansion due to cost structure becoming more efficient. Early signs of improvements were seen in Q1, where gross margin expanded to 74%, while G&A was already ~30% of revenue, 500 bps better than the FY 2022 annual figure, and 100 bps better than Q1 2022.

{kind=link}

Assuming costs stay flat and an expected $5 million annual cost saving is applied in 70:30 proportion only towards G&A and cost of sales (using the FY 2022's figures), that means we may expect an FY 2023 G&A expense of +$30 million and cost of sales of +$28 million, representing ~31% of revenue and 74% gross margin respectively. As it stands, we are basically looking at a similar financial outlook to Q1 2023, suggesting that the initiative is highly achievable and ASUR remains on track to realize margin expansion for the FY.

Risk

I believe that near-term downside risk remains minimal to moderate. Into the next 18 months, I would probably suggest investors keep tabs on the development of ASUR’s tax processing (under professional services / PS) and interest revenue (under recurring revenue / RR) streams. I view these two revenue streams to be much more sensitive to the change in the macro situation.

{kind=link}

Since 2021, ASUR's tax processing revenue has been driven by the increasing ERTC filing activities in its platform. ERTC is a tax relief program for businesses impacted by COVID-19. In FY 2022, ERTC revenue contributed to the significant 93% YoY growth in PS revenue. In Q1, PS accelerated further as it grew by more than 3x also due to the growth in ERTC revenue. As a result, PS ended up being +15% of ASUR’s overall business as of Q1 2023. At the same time last year, it was merely 5% of the business.

However, as per the 10K , the program is expected to be discontinued in 2025 or possibly even earlier, suggesting that ASUR should expect a negative impact on its professional services revenue at most in the next two years.

Additionally, ASUR has also been generating interest revenue, which comes from the client’s funds collected for the purpose of employee payment disbursement. ASUR would typically invest these funds into low-risk short-term financial instruments, and recognize the return as an interest revenue under the RR stream. Due to the current high-interest rate environment, interest revenue has increased and contributed meaningfully to RR growth in recent times. In Q1, an increase in interest revenue contributed almost 36% of the total increase in RR and was the single largest increase, more than an increase in HR compliance or marketplace revenue, as per the quarterly report :

Recurring revenue for the three months ended March 31, 2023 was $27,956, an increase of $4,952, or 22%, from $23,004 for the three months ended March 31, 2022. Recurring revenue increase is primarily due to an increase of approximately $1,874 in interest earned on funds held for clients, an increase of $1,336 in HR compliance revenue, and an increase of $1,157 in revenue from AsureMarketplace™.

As with the ERTC outlook, ASUR's interest revenue may potentially experience a decline, following the downtrend of interest rates probably in the second half of FY 2023 and beyond as inflation softens.

Valuation / Pricing

For FY 2023, the management guided to revenue of $111 million - $113 million and an adjusted EBITDA margin of 17% - 18%. To estimate the target price for ASUR in FY 2023, I assume the following bull vs bear scenario:

- Bull scenario (80%) - ASUR to finish FY 2023 with $113 million of revenue, at the high end of its guidance, and an EBITDA margin of 17.5%, the midpoint of the guidance.

- Bear scenario (20%) - ASUR to miss FY 2023 estimate with $107 million of revenue. This means that ASUR falls short of its upward revised guidance and performs more in line with its old guidance of $105 million -$107 million instead . Likewise, I expect EBITDA margin at 15%, missing the new estimate but in line with the old guidance of $14 million - $16 million.

{kind=link}

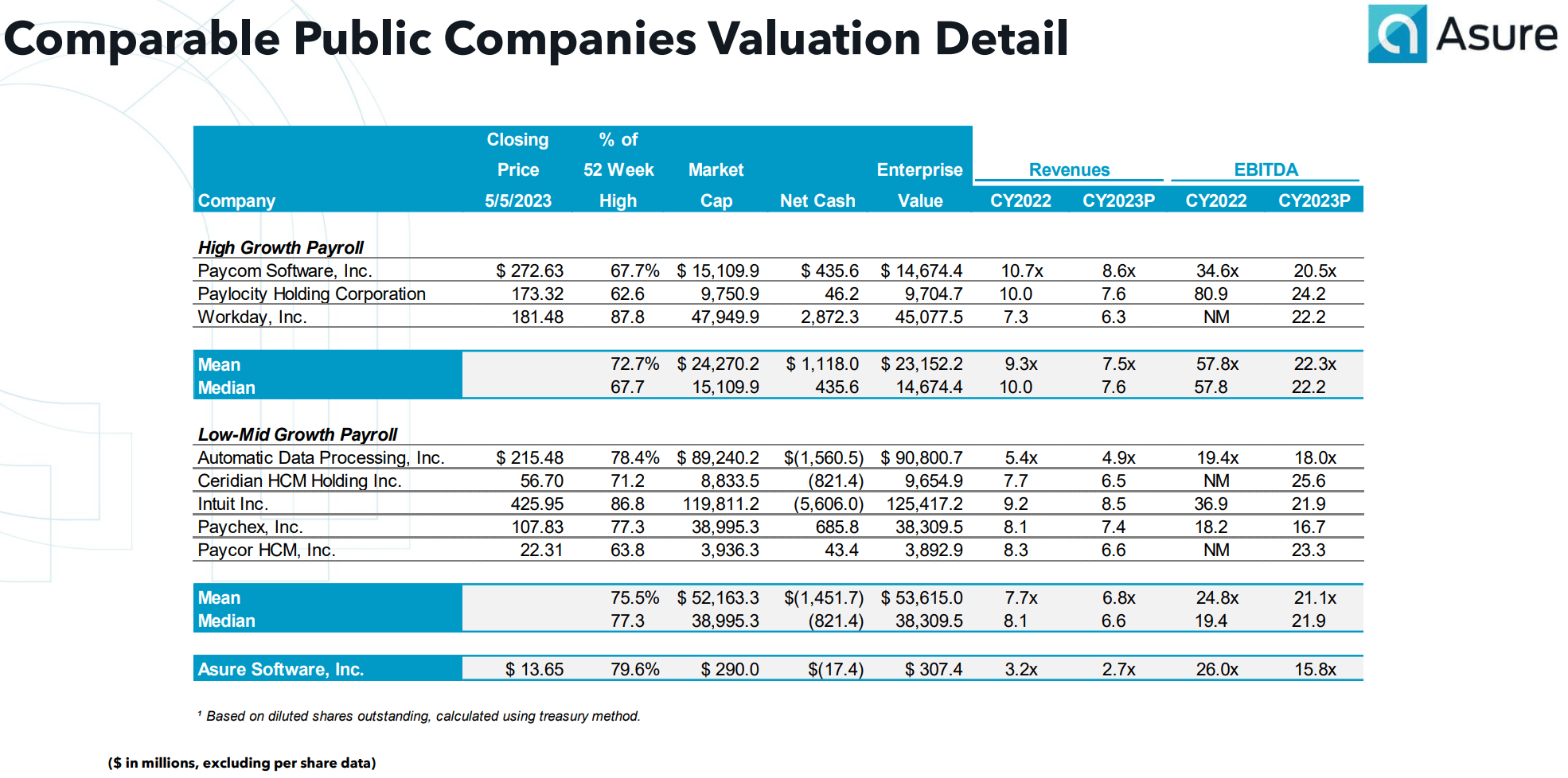

I arrived at a probability-weighted adjusted EBITDA of $19 million for FY 2023. Considering the momentum on the stock, ~18% growth, and high teens adjusted EBITDA margin, I think that it is possible for the FY 2023 EV/EBITDA to trade closer at the higher end of 21x - 25x, which is a valuation range based on the low-mid growth payroll sector average for FY 2022 and FY 2023.

Nonetheless, applying a rather conservative 21x multiple with an assumption of $17.4 of net cash and ~21 million average shares on a diluted basis, I arrived at an FY 2023 target price of $18.17 per share.

Considering that ASUR is trading at ~$12 per share today, there is an opportunity to realize a ~50% upside if the stock ends up at the modeled target price of ~$18 at year end, and therefore, ASUR is an attractive buy opportunity at present.

Conclusion

ASUR has three near-term catalysts that can benefit the company going into FY 2023 and beyond. The downside risk in the near term is minimal to moderate, with particular attention needed on the development of tax processing and interest revenue streams, which are sensitive to macro changes. Despite rather conservative assumptions, I found that ASUR is undervalued based on my target price model. I set a target price of ~$18 per share for FY 2023. At ~$12 per share today, the stock presents an attractive buying opportunity. I give the stock an overweight rating.

For further details see:

Asure Software: Multiple Tailwinds To Sustain Profitable Growth