ASUR - Asure Software Stock: Great Company But With A Premium Valuation

2023-03-31 09:18:23 ET

Summary

- Asure Software's impressive growth over the past year and strong financial performance make it look like a compelling investment opportunity.

- Despite potential economic challenges, the company remains optimistic - the management sets new benchmarks for revenue and adjusted EBITDA figures for FY2023.

- Based on my analysis, ASUR will likely beat consensus on its Q1 2023 report [May 8, 2023 - post-market].

- The company's end markets are estimated at over $90 billion today, and the entire TAM is expected to grow at a CAGR of 7.6% over the next few years.

- Unfortunately, ASUR stock seems to be quite richly valued to date - at about 25-30% of the industry's norms with no premium. It's a strong Hold rather than Buy.

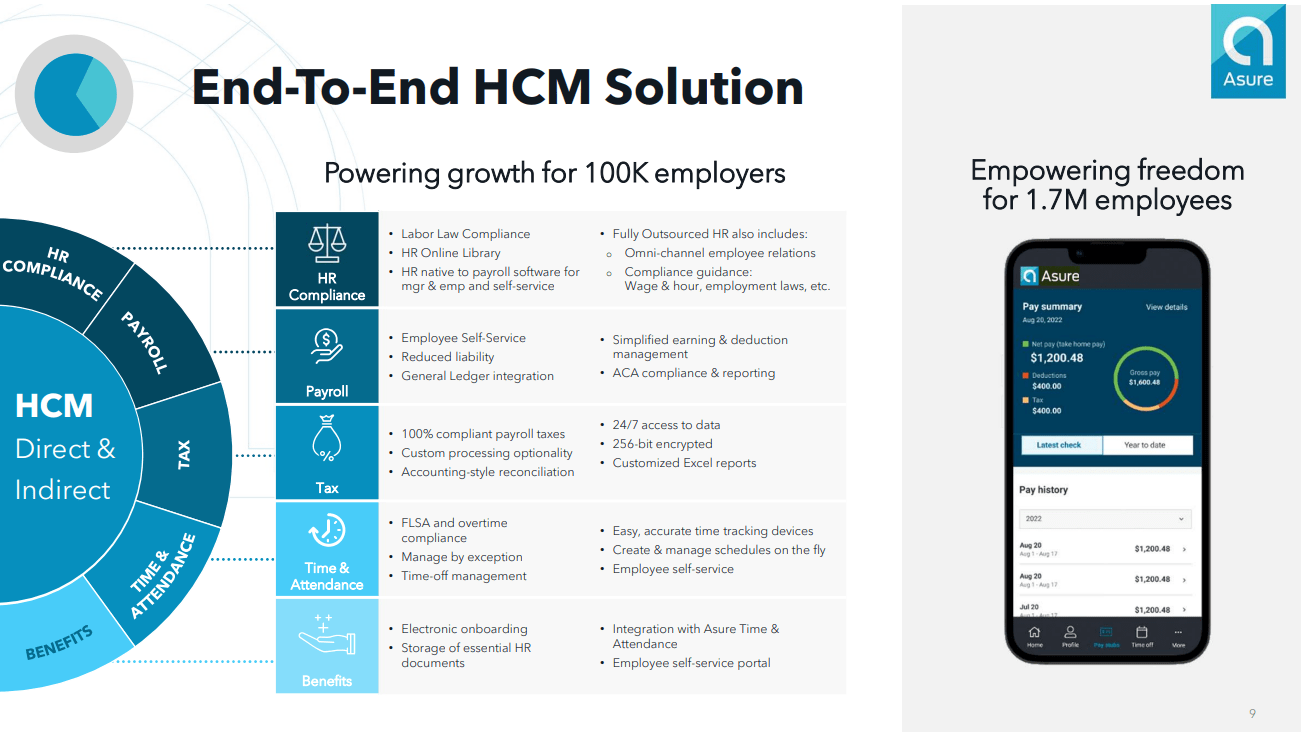

Asure Software, Inc. ( ASUR ) is a $290-million market cap cloud-based human capital management [HCM] software company that is headquartered in Austin, Texas and serves primarily the U.S. market. According to Seeking Alpha, the company provides solutions for small and medium-sized businesses to build productive teams, stay compliant, and allocate resources to grow their business.

Based on the most recent 10-K filling , Asure Software generates revenue from its software-as-a-service suite for human resource needs such as payroll, tax, HR compliance, time and attendance, and AsureMarketplace, as well as from quarterly and annual reporting requirements. Hardware-as-a-service revenue is generated from renting devices used to track time and attendance, while maintenance and support revenue is generated from servicing the hardware and providing training. Professional services revenue is generated from fulfilling clients' needs typically fulfilled by an internal payroll system or HR department. Additionally, the company earns revenue from tax management solutions and interest gained from client funds.

{kind=link}

Asure Software's stock has seen significant growth, almost 140% over the past year and over 51% year-to-date. The company's strong Momentum factor amid its superior Growth and above-average Profitability factors, place the company on the frontline of its industry, according to SA Quant System.

Seeking Alpha, ASUR, author's notes

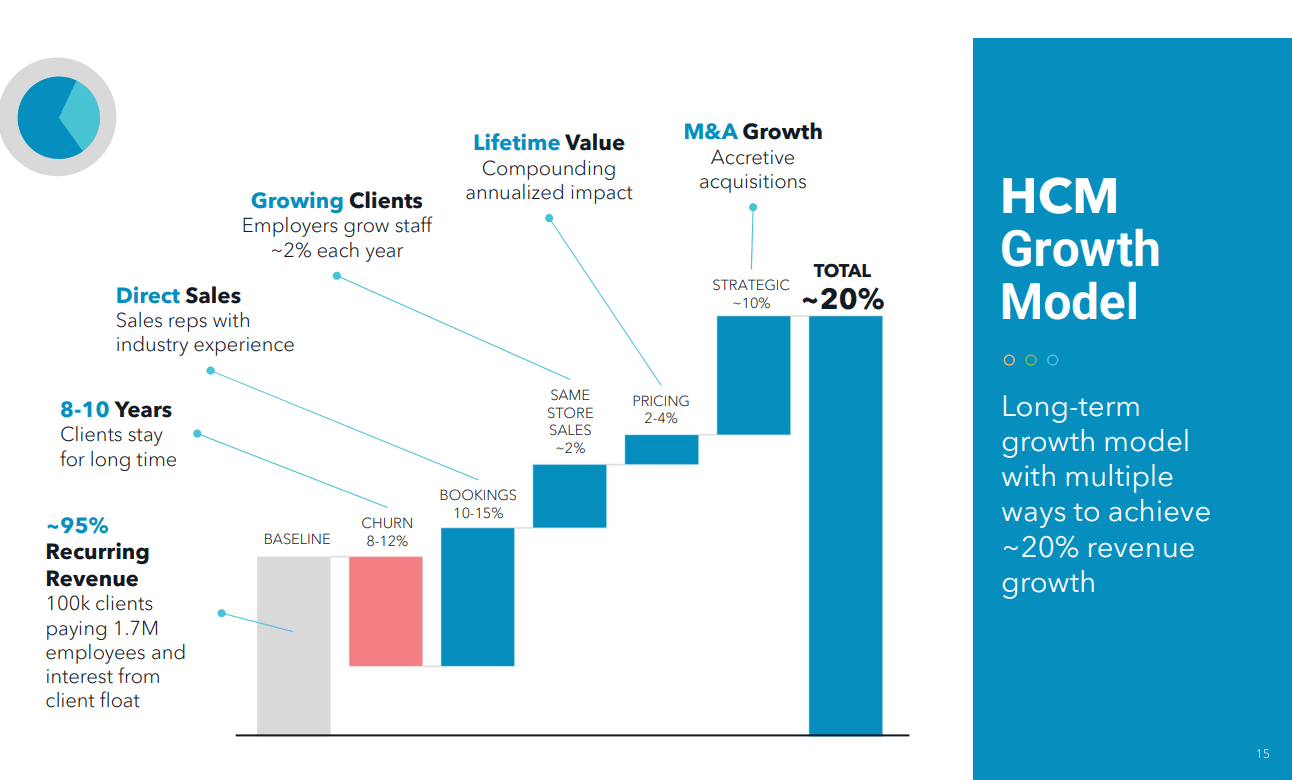

And that's not surprising - the company is trying to build its business model to achieve stable revenue growth of 20% over the long term, relying on both organic sources and accretive M&A transactions:

{kind=link}

Based on the CEO's statement , the company plans to focus on growing its customer base and suite of services while continuing to prioritize organic growth and profitability. Actual financial results are in line with management's target, as far as I can see. For Q4 2022, revenue increased 39% to $29.3 million and recurring revenue increased 25% to $24.1 million compared to the same quarter last year. For the full year 2022, revenue increased 26% to $95.8 million and recurring revenue increased 21% to $86.2 million compared to the prior year. The company reported a net loss of $1.1 million in Q4 2022 and a net loss of $14.5 million for the full-year 2022 but adjusted EBITDA increased $4.2 million year-over-year to $11.8 million. Asure Software also announced integrations with ZayZoon, H&R Block, and TurboTax, which are expected to provide new opportunities for revenue growth.

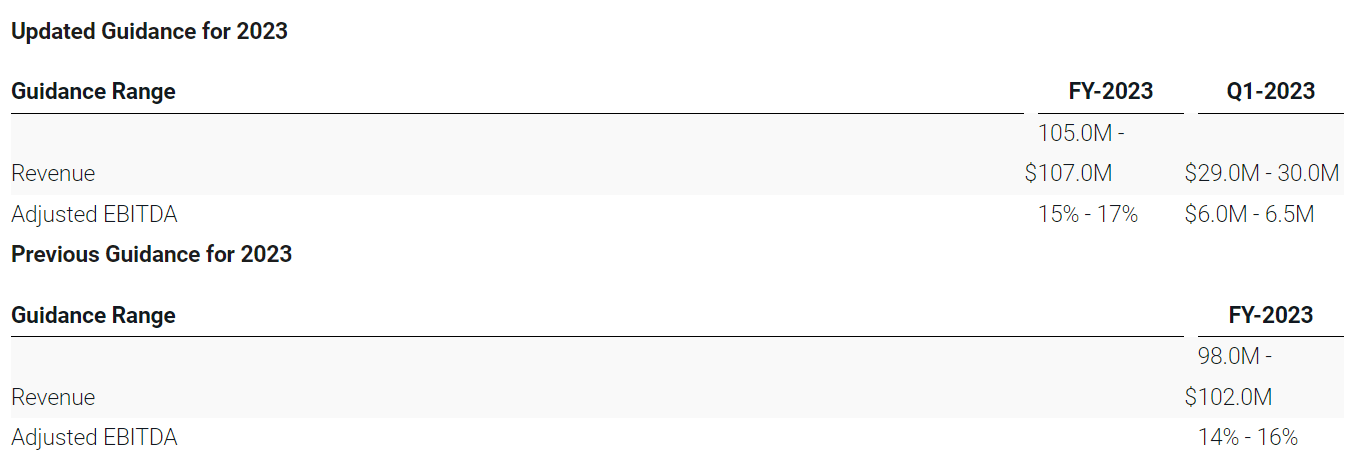

Despite potential economic challenges, the company remains optimistic - the management sets new benchmarks for revenue and adjusted EBITDA figures for FY2023:

{kind=link}

Asure Software's recurring revenue grew 21% YoY with a bookings growth of 126% in FY2022, resulting in an expected adjusted EBITDA margin expansion of ~400 basis points by the end of FY2023 [16% mid-range vs. 12% in FY2022]. So the management guides to an absolute EBITDA growth of 129.2% in FY2023 [ YoY] - that's a lot.

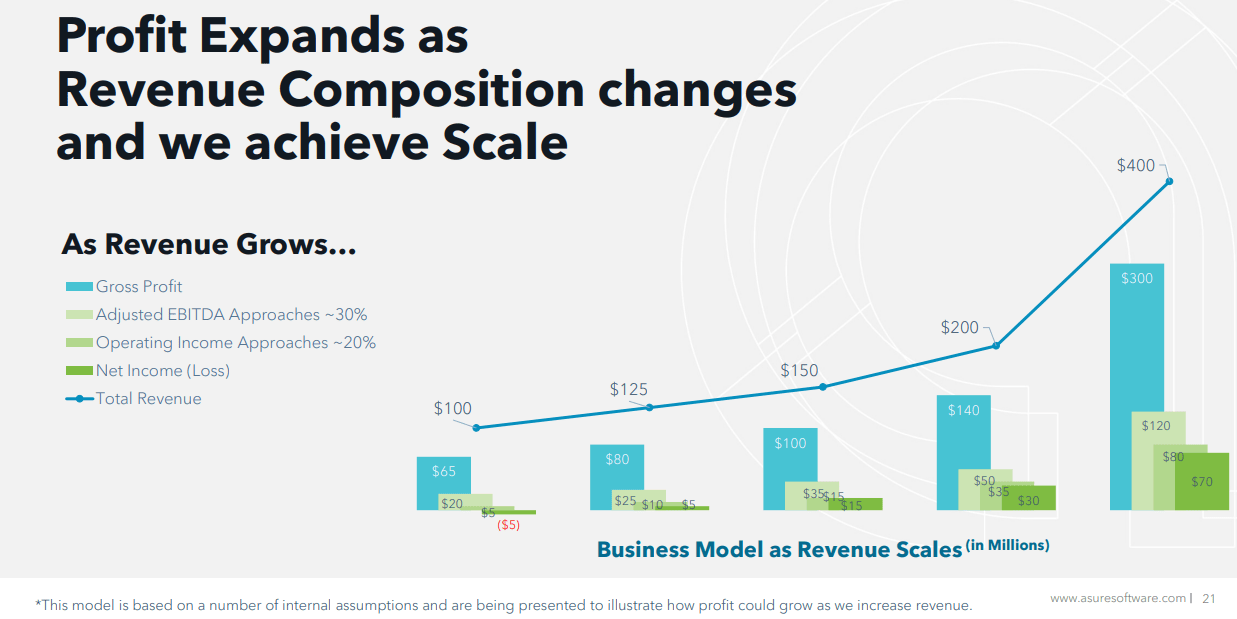

Looking at the historical dynamics of the company's growth, such a goal does not seem unattainable. ASUR shareholders should be glad that the company is not only looking for ways to grow but doing so qualitatively by trying to expand its margins and remain self-sufficient.

{kind=link}

Now that the company has reached a certain size and is relying on stable gross profit and EBITDA generation, free cash flow and operating cash flow does not look like a one-time success - most likely ASUR will continue to have positive FCF and will start actively buying back shares at some point. Either way, I'd like to see it happen at some point.

In general, I like the way the company is growing and developing, as well as the future it sees ahead. The company's end markets are estimated at over $90 billion today, and the entire TAM is expected to grow at a CAGR of 7.6% over the next few years. In other words, a nearly $300 million company definitely has room to grow and self-improve. The crux of the matter is its valuation - I'll get into that below.

Valuation & Expectations

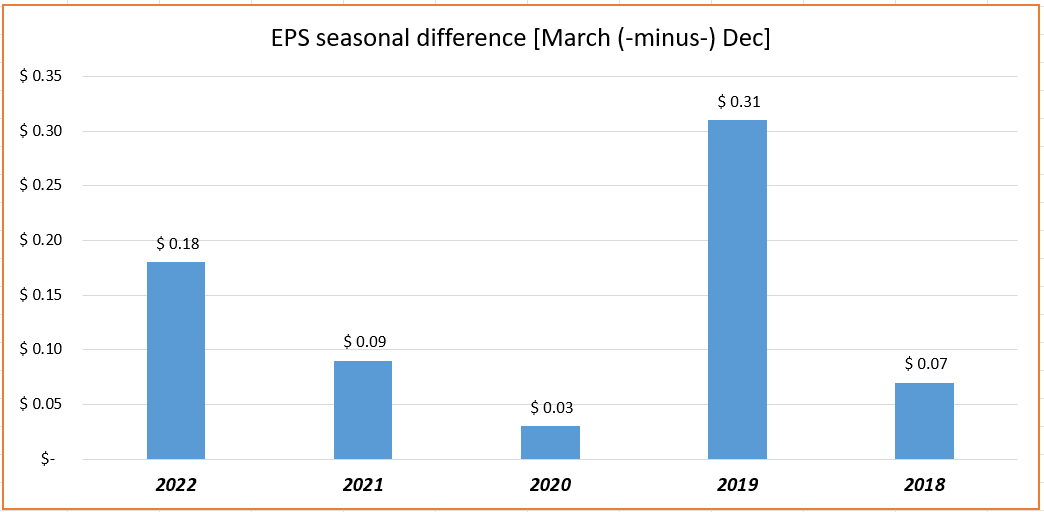

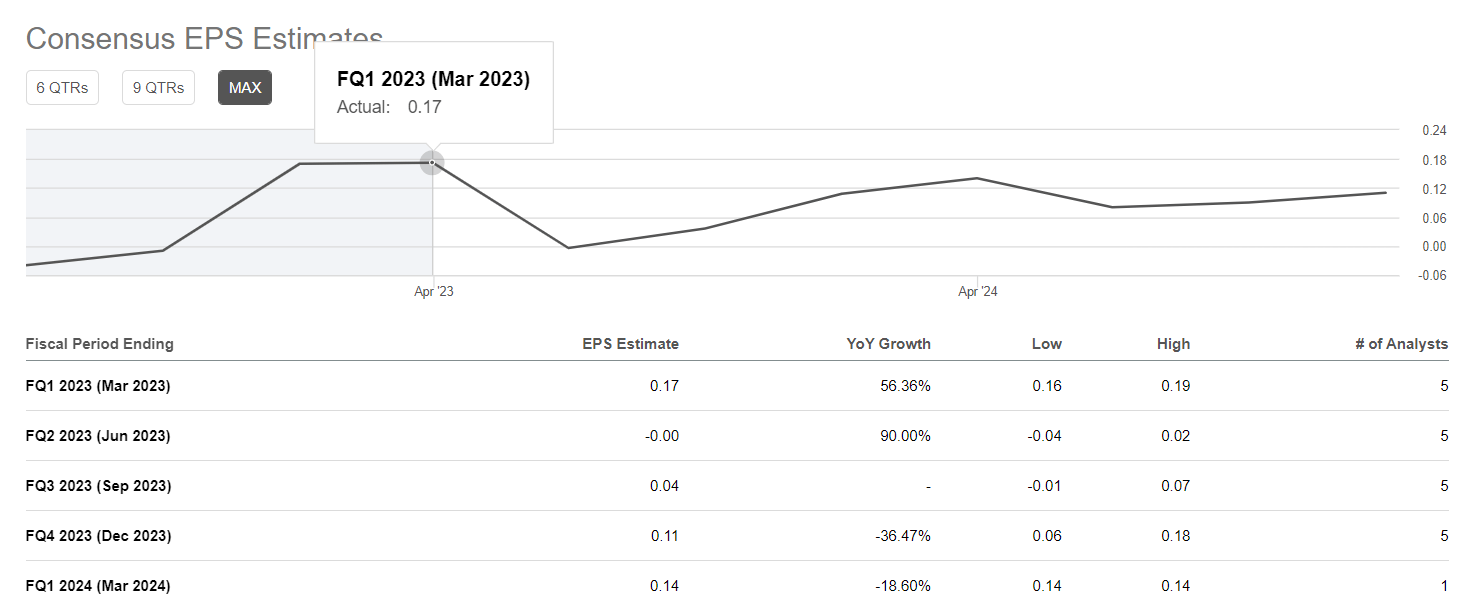

I notice a significant difference between the expected EPS and the actual seasonal trends in the company's business. Seeking Alpha data shows that The Street's EPS estimate for Q1 FY2023 is $0.17, which is the same as Q4 FY2022. However, if we analyze the previous Q4-Q1 quarters and their quarter-over-quarter changes, we can see a positive seasonal shift in absolute terms for the 1st quarter:

{kind=link}

{kind=link}

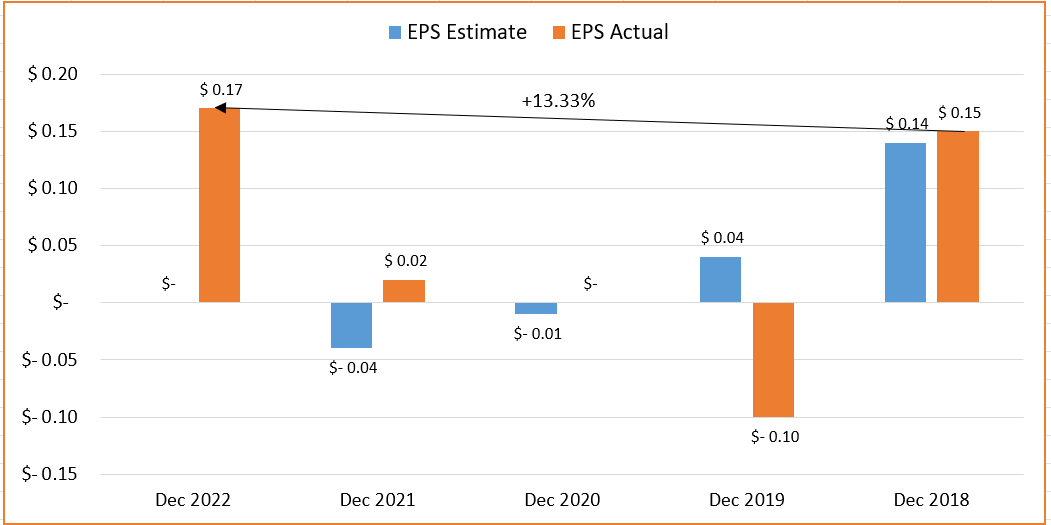

Yes, the projected YoY growth of 56.36% looks strong - however, there is also the effect of the low base formed at the time of the coronavirus. Now the company has just returned to pre-pandemic levels, showing only modest growth in Q4 2022 compared to 2018:

{kind=link}

In 2019, the company generated $26.76 million and adjusted EPS of $0.22; today, analysts expect Q1 2023 revenue of $29.4 million and EPS of just $0.17. At the same time, back then - in 2019 - there was a lot more debt (hence the interest expense).

{kind=link}

Something does not add up here. Therefore, I believe that a return to pre-pandemic levels, plus a seasonal factor, should allow ASUR to again beat current analyst forecasts for at least Q1 FY2023 - if these estimates are not raised before the report. Implementation of any of the proposed scenarios should theoretically drive ASUR stock price to new highs.

But is ASUR stock fairly valued today?

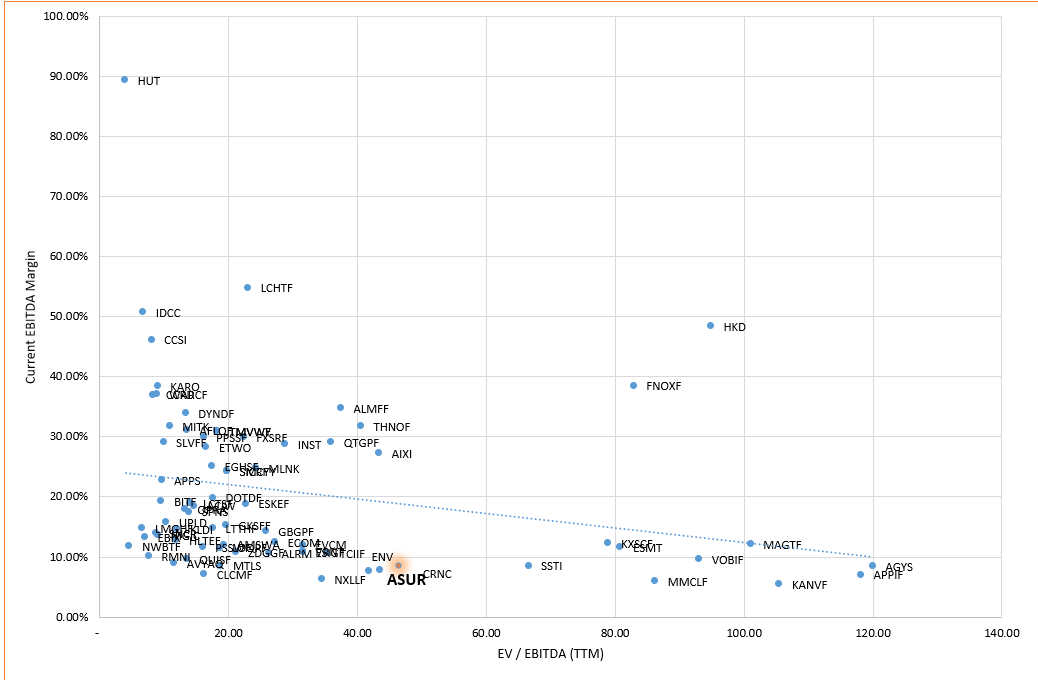

Out of the 214 Application Software stocks provided in the Seeking Alpha sample, I applied two simple screening criteria to narrow down the list to just 74 companies :

- Enterprise Value between $200.00 million and $4.02 billion;

- Trailing Twelve Months [TTM] EBITDA Margin between 5.00% and >70.00%.

Using this refined sample, I plotted the TTM EBITDA margin on the x-axis against the current EBITDA margin on the y-axis to analyze ASUR's position within its industry based solely on past data.

{kind=link}

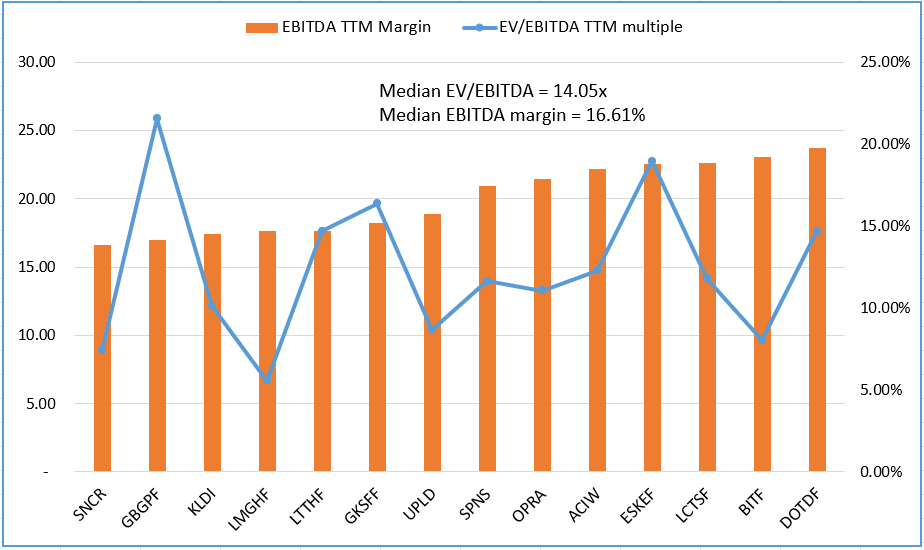

I selected several companies with different TTM EBITDA margins, but such that the group's median value was roughly at the 16% level - that's how much management sees by the end of 2023. Then I compared the EV/EBITDA [TTM] multiples of these companies and got the following picture:

Author's work, Seeking Alpha data

{kind=link}

But not all of these companies will grow at the long-term growth rate that ASUR's management is targeting, so there should be a premium to the valuation. I think 30% looks pretty fair. In this case, ASUR is rightly valued - but only on the condition that we leave the assumption of a premium for future growth and margin expansion:

| Valuation analysis |

| no premium |

| 30% premium to the multiple |

| Adj. EBITDA FY2023 |

| 16.96 |

| 16.96 |

| EV/EBITDA multiple |

| 14.05 |

| 18.27 |

| Enterprise value [EV] |

| 238.29 |

| 309.77 |

| Net debt |

| 26.20 |

| 26.20 |

| implied MC (EV - net debt) |

| 212.09 |

| 283.57 |

| current MC |

| 290.90 |

| 290.90 |

| upside (downside) |

| -27.09% |

| -2.52% |

Source: Author's calculations

So ASUR stock seems to be quite richly valued to date - at about 25-30% to the industry's norms with no premium.

Everyone decides for themselves whether they are willing to pay this premium. Personally, I am not ready today. Yes, ASUR will likely beat consensus on its Q1 2023 report [May 8, 2023 - post-market]. But the fundamental upside potential seems limited in my opinion.

Summary Thesis

Asure Software's impressive growth over the past year and strong financial performance make it look like a compelling investment opportunity. With a year-to-date growth of over 51% and beating EPS consensus for the last 4 quarters, the company has shown consistent growth and [adjusted] profitability. Additionally, Asure Software's recurring revenue of 92% and 126% bookings growth in FY2022, along with significant EBITDA margin expansion projected for FY2023 [+823 basis points], suggest a promising future for the company. I see a clear discrepancy in EPS projections for Q1 FY2023 and actual seasonality - if the company can successfully transfer EBITDA growth to EPS growth this year, it could potentially exceed the already richly estimated FY2023 EPS growth of 96.67%. This is especially true for the upcoming quarter's projections, which imply no seasonal effect on ASUR's EPS.

Unfortunately, ASUR stock is currently richly valued, at about 25-30% compared to the industry's norms. So I rate Asure Software as a strong Hold , indicating more bullish than bearish sentiment; the company's overvaluation restricts a Buy rating this time.

As always, your comments are welcome! Thanks for reading!

For further details see:

Asure Software Stock: Great Company But With A Premium Valuation